A $53 billion unsolicited bid for PayPal is sitting unanswered on a boardroom table, and the first thing sophisticated observers noticed is how low the price looks relative to what this asset could realistically fetch if the process becomes competitive.

Stripe and Advent International jointly submitted a non-binding proposal of $60.50 per share for PayPal on 14-15 July 2026, backed by approximately $50 billion in committed bank financing. PayPal shares surged roughly 14-17% on the news. The board has not formally responded. Nothing is agreed. But the structure of what has been proposed, and who else might have reason to bid, is already telling you something important about where this situation is likely to go.

Here is the strategic logic behind each party’s interest, the financial conditions that make PayPal a leveraged buyout target, the credible competing bidder field, and what the distribution of outcomes looks like if you are holding or evaluating the stock today.

What Stripe and Advent are actually proposing

The headline number is $60.50 per share, implying a valuation above $53 billion for PayPal. The bid carries a 28-30% premium to PayPal’s pre-announcement share price, and it is backed by approximately $50 billion in committed bank financing from a consortium of lenders.

| Data Point | Figure | Notes |

|---|---|---|

| Offer price | $60.50 per share | Non-binding, unsolicited |

| Implied valuation | Above $53 billion | Based on fully diluted share count |

| Bank financing | ~$50 billion | Committed debt package |

| Premium to pre-announcement price | ~28-30% | Depends on reference day |

| Ownership split | 50/50 (Stripe / Advent) | No planned break-up at closing |

| Share price reaction | ~14-17% surge | On announcement day, 14-15 July 2026 |

That $50 billion debt figure is the detail that defines everything else about this proposal. This is structured as a leveraged buyout (an LBO, where the acquisition is funded primarily with borrowed money), not a strategic equity deal. The entire thesis rests on PayPal’s ability to generate enough free cash flow, the cash left after operating costs and capital spending, to service an enormous debt load.

Three structural facts keep this firmly in “proposal” territory rather than anything approaching a done deal:

- PayPal’s board has not agreed to anything or formally responded to the offer

- There is no certainty that the approach will result in a transaction

- No timeline for board engagement or a potential market check has been stated

When big ASX news breaks, our subscribers know first

Why Stripe wants what PayPal has built

Stripe is a business-to-business infrastructure provider. It builds the payment processing layer that merchants, software companies, and marketplaces use behind the scenes. What it does not have is a consumer-facing brand that sits at the checkout.

PayPal fills that gap with three assets Stripe cannot cheaply replicate. First, a globally recognised checkout presence spanning hundreds of millions of consumer accounts, with a button that merchants have long treated as a conversion-driving standard across online retail. Second, Venmo, a peer-to-peer payments platform whose network effects and demographic reach give Stripe access to a consumer segment it has no existing route into. Third, Braintree, an enterprise-focused payment gateway serving large merchants and platforms, whose capabilities sit alongside rather than duplicate what Stripe already offers.

The strategic calculus is not about synergies on a spreadsheet. It is about whether the consumer checkout layer and Venmo’s network effects are things Stripe could realistically build from scratch within a decade. The honest answer is probably not.

Three synergy vectors make the combination analytically compelling:

- Software cross-sell: Stripe’s higher-margin tools, including invoicing, tax, and billing products, could be extended to PayPal’s merchant base, unlocking revenue without building a parallel distribution network from scratch

- Data scale for fraud and authorisation: Combining transaction flows from both networks would produce a substantially richer data set, with the potential to sharpen transaction approval rates and reduce fraud losses across the merged entity

- Consumer payments gap closure: PayPal’s wallet and Venmo would give Stripe an immediate consumer presence it currently lacks

A combined entity’s total processed payment volume would place it among the largest merchant acquirers globally, with each business currently handling roughly $1.6-1.7 trillion annually, implying a combined figure in the region of $3.2-3.4 trillion (this figure has not been independently confirmed and is based on publicly available estimates for each company individually).

What Advent brings and what makes PayPal an LBO target

Advent International is the financial engineering partner. Its role is to provide LBO structuring discipline alongside Stripe’s strategic rationale.

What makes PayPal attractive to a private equity buyer is a specific combination of financial characteristics: predictable, high-volume transaction revenue; a track record of generating substantial free cash flow; and relatively little existing debt, leaving meaningful room on the balance sheet for acquisition financing. Alongside that sits the option to divest individual units over time. Venmo, Braintree, or regional businesses could be separated after closing to accelerate debt repayment, even if the stated intention at signing is to hold the company intact. PayPal stock had declined roughly 18% year-to-date and approximately 35% over the prior year before the announcement, which means the bidders are approaching an asset they believe is undervalued by the public market.

Strategic divestiture dynamics of the kind that allowed Etsy to refocus its capital and operations after the Depop sale are directly relevant to how Advent International would approach PayPal post-closing; the private equity playbook often involves separating units that command premium standalone multiples to accelerate debt repayment, even when the stated intention at signing is to hold the combined entity intact.

For Stripe, the strategic rationale means it will be motivated to raise its bid if PayPal’s board pushes back. This is not a purely financial transaction for Stripe the way it is for Advent, and that asymmetry matters if the price has to move.

The competing bidder field and why this bid may go higher

No alternative bidders have formally emerged. But the absence of a formal competing bid today means nothing definitive about whether one will surface, because the board’s response and any quiet market check it conducts will likely happen before competing interest becomes public.

The realistic universe of potential buyers segments into two categories, and each faces distinct structural barriers.

| Potential Bidder | Strategic Logic | Primary Barrier |

|---|---|---|

| Apple | Expands payments reach beyond iOS ecosystem | Deterred by Braintree’s low-margin segment; significant regulatory scrutiny |

| Amazon | Extends Amazon Pay beyond its own platform | Sellers on competing platforms would be unwilling to route transaction data to a company they regard as a rival |

| Bolsters its wallet offering against Apple’s competing product | Meaningful antitrust review uncertainty | |

| PE Consortia | Replicates LBO thesis with similar financing model | No integration complexity; financing availability is the primary constraint |

For each large technology platform, antitrust exposure and merchant-data conflicts are genuine deal-killers rather than abstract risks. Apple, Amazon, and Google would all face substantially higher regulatory hurdles than Stripe. Financial sponsors, whether private equity firms acting alone or alongside sovereign wealth funds, represent the more plausible competing bidder pool in practical terms. They sidestep the integration and data-conflict questions entirely and can structure a financing package along lines similar to the Advent model.

The 2023 Merger Guidelines, released jointly by the FTC and DOJ, establish the analytical framework agencies apply when reviewing large-scale payments and technology combinations, with market concentration and network effects among the factors that would receive close scrutiny in a Stripe-PayPal review.

Michael Burry, who holds PayPal shares, has publicly stated that “the bid will have to rise” and that PayPal is “well below intrinsic value” at $60.50, arguing that any successful bid should be well above intrinsic value to reflect a control premium.

The composition of this competing bidder field determines the realistic ceiling on where a deal could clear, which is the single most important variable if you are evaluating position sizing today.

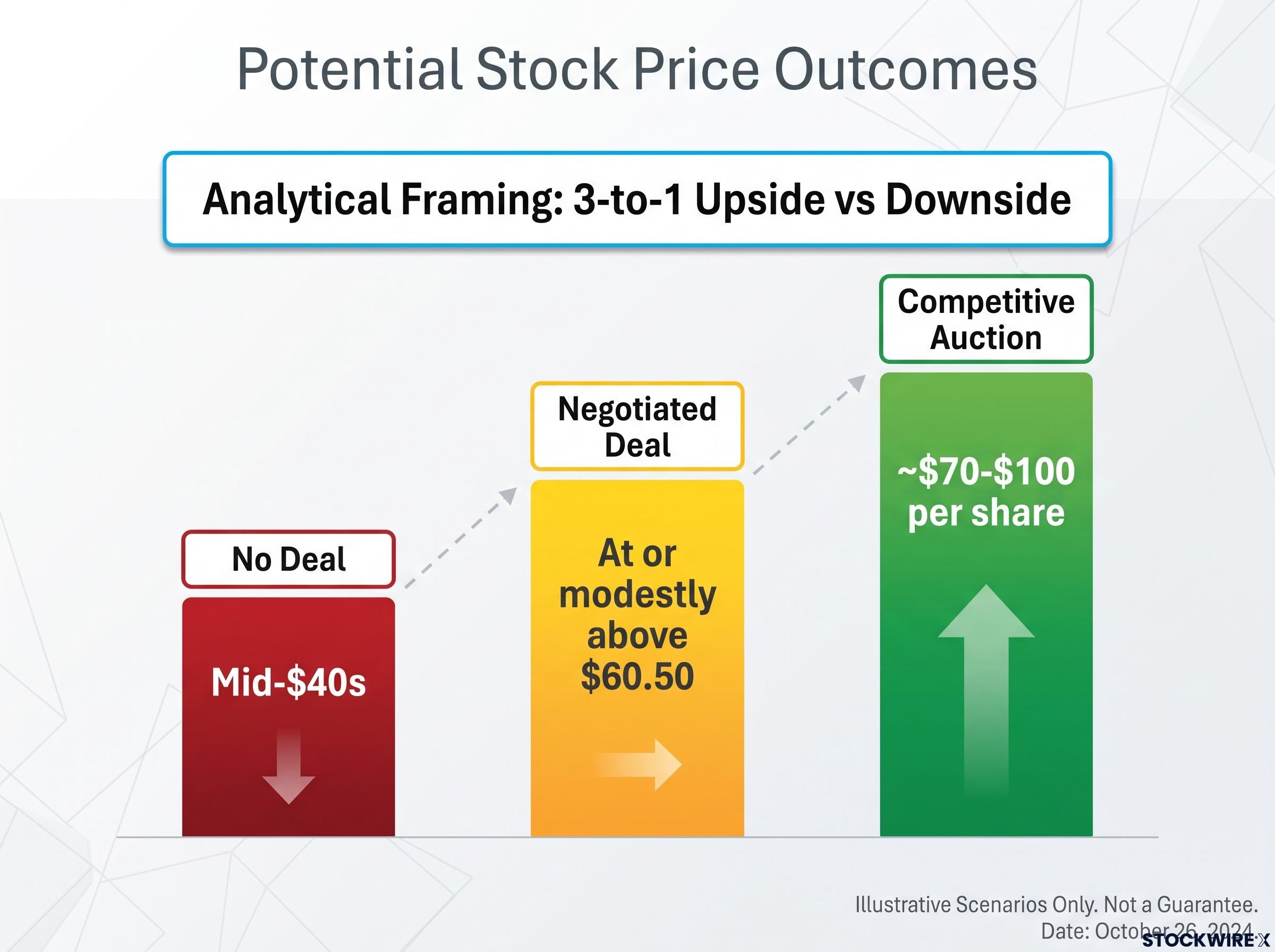

The investor risk-reward calculus at current prices

Start with the downside. In a scenario where the process collapses entirely, with no revised offer from Stripe and Advent and no other party stepping in, the stock would likely give back most of the announcement-driven gains and return toward the mid-$40s level at which it had been changing hands before the news emerged.

| Scenario | Approximate Price Range | Key Condition |

|---|---|---|

| No deal | Mid-$40s | Board rejects; no competing bidder emerges |

| Negotiated deal | At or modestly above $60.50 | Board engages; terms refined with limited competition |

| Competitive auction | ~$70-$100 per share | Multiple credible bidders engage the process |

The market has already partially priced the deal premium into the stock, which means the risk-reward is asymmetric but not one-sided in the buyer’s favour.

The three-outcome structure used here, assigning price ranges to no-deal, negotiated, and competitive auction scenarios, reflects a scenario analysis framework that probability-weights outcomes against an entry price to produce a blended expected return, a discipline that becomes essential when a stock is mid-transition between standalone and acquired status.

One analytical framing positions the potential upside against the downside at roughly 3-to-1, and assigns a subjective probability above 50% to a positive outcome materialising. This represents analytical opinion, not financial advice. The competitive auction price range of $70-$100 is original source analysis and is not sourced to wire reports.

That 3-to-1 ratio sounds attractive, but it is only meaningful if your own probability estimate for at least one higher bid exceeds the implied breakeven. That depends entirely on your assessment of the competing bidder field covered above.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The scenario pricing and probability estimates referenced are analytical opinion and subject to change based on market developments.

Key risks that could derail the deal entirely

Four specific risk categories could cause this entire process to unwind rather than progress toward a transaction:

- Board rejection without a market check. PayPal’s board has every incentive to run a robust process rather than accept an unsolicited first bid. If the board concludes that standalone intrinsic value materially exceeds $60.50 and declines to engage, the process ends before it starts. Even in a scenario where a deal ultimately occurs, this introduces timeline uncertainty.

- Debt market deterioration. The approximately $50 billion in committed bank financing creates material exposure to credit spread widening or rate changes. If risk appetite shifts before terms are finalised, the debt could reprice, potentially lowering what Stripe and Advent can afford to pay or discouraging them from proceeding.

Leveraged financing conditions in mid-2026 carry their own macro tail risk independent of any single transaction; record margin debt levels and corroborating signals across leveraged instruments mean that a broad shift in credit appetite could reprice the approximately $50 billion debt package underpinning this proposal before terms are finalised.

- Multi-jurisdiction regulatory scrutiny. A Stripe-PayPal combination would create one of the largest merchant-acquiring and checkout ecosystems globally by volume, attracting antitrust review across multiple jurisdictions. Technology platform bidders would face substantially higher hurdles, but Stripe’s own combination would not be exempt from review.

Governance and capital constraints

- Stripe’s private-company limitations. This is the least-discussed but potentially most binding constraint on how far Stripe can go in a competitive process. A public strategic acquirer can issue shares to fund a higher bid. Stripe, as a privately held company, must rely on equity capital that is harder to mobilise quickly. If a competing bidder forces the price above $60.50, Stripe’s ability to stretch depends on its own investor base and governance structure in ways that a public company simply would not face.

Understanding these failure modes allows you to monitor real-time indicators, including credit spread movements and regulatory filing timelines, rather than treating deal risk as a binary unknown.

The next major ASX story will hit our subscribers first

What to watch as this situation unfolds over the next several months

The deal process, if it proceeds, will follow a reasonably predictable sequence. Each stage produces observable signals that tell you whether the situation is escalating toward a competitive auction or cooling toward withdrawal.

- Board evaluation: PayPal appoints external advisors and benchmarks the $60.50 bid against standalone value

- Market check: The board conducts a quiet or overt process to determine whether competing interest exists

- Term negotiation: If PayPal is receptive, price, termination fees, and financing covenants are refined, potentially yielding a revised offer above $60.50

- Regulatory filing: Multi-jurisdiction antitrust and financial-services approvals follow any agreed transaction, extending the timeline by many months

- Credit and market evolution: Debt markets and technology valuations shift throughout, raising or lowering the effective ceiling on what leveraged buyers can pay

Deal resolution, if any transaction occurs, is expected within approximately one year from July 2026, but significant developments could emerge in the coming weeks as the board responds.

Signals that the process is escalating toward a bidding war:

- PayPal formally engaging external advisors and inviting competing interest

- Reports of additional parties conducting due diligence

- Credit markets remaining accommodative for large-scale LBO financing

Signals the process may be cooling:

- Extended board silence without advisor engagement

- Credit spread widening that reprices the debt package

- Stripe or Advent publicly moderating language about the transaction

The board’s first formal response, including whether it appoints external advisors and invites competing interest, will be the most informative single data point about whether this process is heading toward a transaction or a breakdown.

Whether $60.50 holds or the process forces a higher number

Two variables will determine the outcome more than anything else. First, the board’s assessment of PayPal’s standalone intrinsic value relative to $60.50. Michael Burry’s position that intrinsic value exceeds the offer price by a meaningful margin is not an isolated view. If the board shares that conviction, the opening bid is a starting point, not a finish line. Second, whether the process draws in at least one credible additional bidder. The arrival of even a single competing party, including from the private equity universe, would materially shift the negotiating dynamics and push the probable clearing price higher.

PayPal’s own asset composition, spanning a consumer wallet, Venmo’s peer-to-peer network, and Braintree’s enterprise gateway, lends itself to a sum-of-parts valuation approach where each unit is assessed independently before deriving a consolidated intrinsic value, a methodology that frequently produces a materially different number than a single earnings multiple applied to consolidated results.

The analytical competitive auction range of approximately $70-$100 per share, which represents original source analysis rather than wire-reported figures, gives you a sense of the gap between what has been offered and what might be achievable in a contested process.

Nothing is agreed. The $60.50 bid is non-binding and unsolicited. PayPal has not formally responded as of 15 July 2026. Both parties retain full optionality.

The specific thing to watch first: PayPal’s formal board response and whether it publicly invites competing interest. Everything else, the price, the timeline, the competitive dynamics, flows from that decision.

Past performance does not guarantee future results. These forward-looking statements are speculative and subject to change based on market developments and company performance.