Hormuz Shipping Collapses 52% as US-Iran Clash Sends Oil Surging

1 hr ago

Bernstein issued fresh ratings across the four dominant memory chip companies on 13 July 2026, and the firm’s verdict draws a sharp line: three are buys on pullbacks, and one is a structural risk even as the sector rallies.

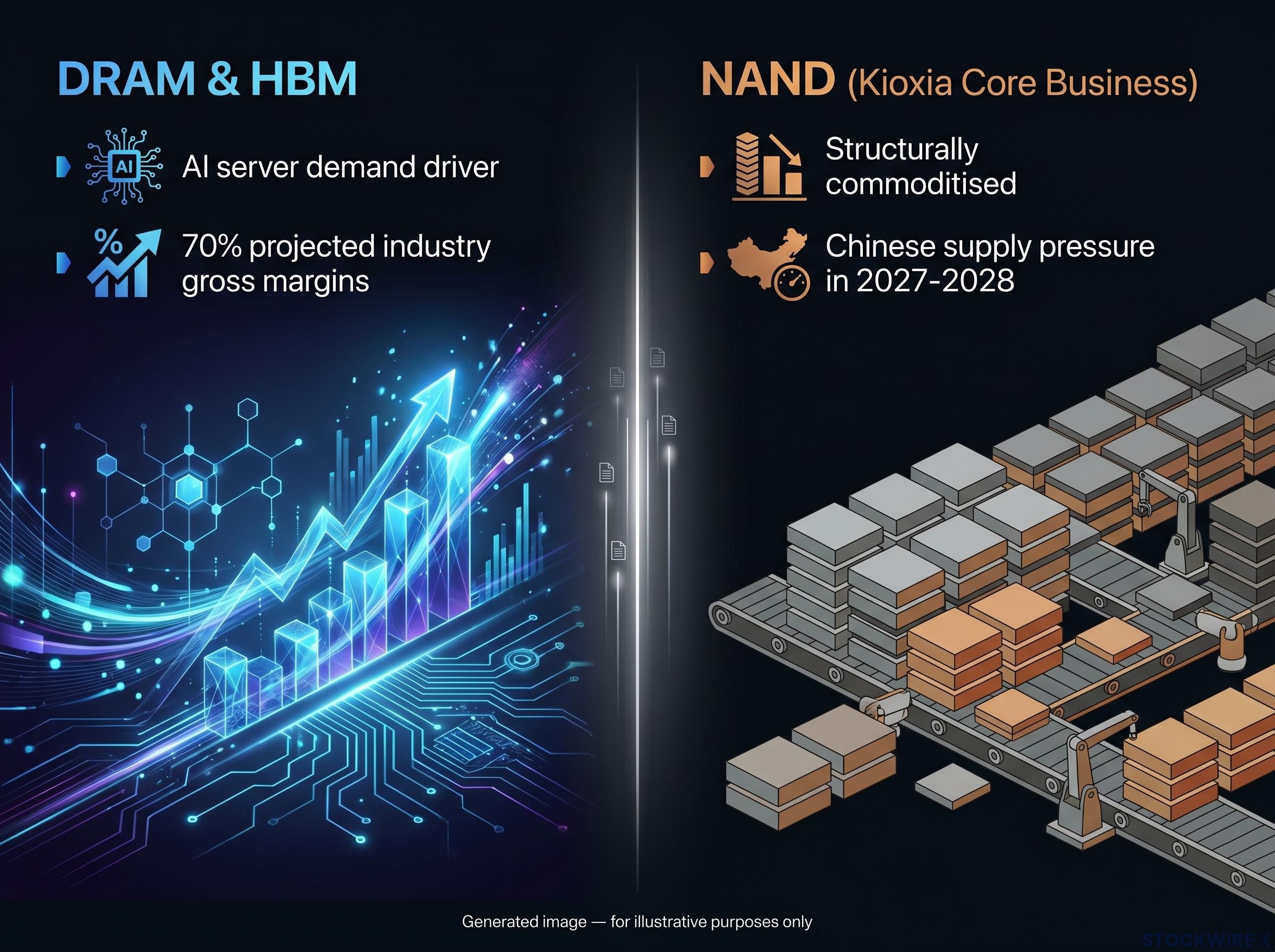

The ratings arrive at a moment of tension. AI-driven server demand is sustaining an unusually durable pricing upcycle in DRAM and HBM (high bandwidth memory, the specialised chips that power GPUs and AI accelerators), while NAND-heavy businesses face a different competitive reality shaped by rising Chinese supply capacity. Bernstein’s framework separates these two worlds cleanly, and the distinction matters for how you think about exposure across the sector.

Here is exactly where Bernstein sees opportunity and risk across Samsung, SK Hynix, Micron, and Kioxia, what the reasoning behind each rating tells you about the memory cycle right now, and where the thesis still depends on execution.

Bernstein maintained Outperform ratings on three of the four major memory chip stocks despite recent share price pullbacks. That is a specific signal: the firm is treating the dip as entry context, not a deteriorating thesis. The fourth name, Kioxia, received an Underperform, and the dividing line is product mix. DRAM and HBM exposure separates the favoured three from the cautioned one.

| Company | Rating | Cited price target | Currency |

|---|---|---|---|

| Samsung Electronics | Outperform | 440,000 | KRW |

| SK Hynix | Outperform | 3,300,000 | KRW |

| Micron Technology | Outperform | 1,300 | USD |

| Kioxia | Underperform | N/A | N/A |

Price targets are drawn from analyst research summaries and are subject to independent verification. All ratings current as of 13 July 2026.

Maintaining three Outperform ratings through a pullback is not routine coverage. It signals that Bernstein views the recent weakness as cycle-consistent, not thesis-breaking.

The bull case starts with pricing. DRAM and NAND contract prices rose sharply into Q2 2026, with the pace of increases exceeding earlier projections and showing no sign of peaking in near-term data. That pricing environment is the foundation of all three Outperform ratings.

AI server demand is the structural driver. HBM and high-performance DRAM are the chips that go into GPUs and accelerators, the hardware powering data centre AI infrastructure. That infrastructure is expanding rapidly, and the memory required per server is growing with it. The result is a demand profile that looks different from prior memory cycles, which were driven more heavily by smartphones and PCs.

The memory supercycle dynamics driving this cycle differ structurally from prior DRAM upcycles: hyperscaler capex is projected to reach $725 billion in 2026 with AI data centre operators accounting for an estimated 70% of total memory shipment volumes, a demand composition that previous cycle models were never calibrated to handle.

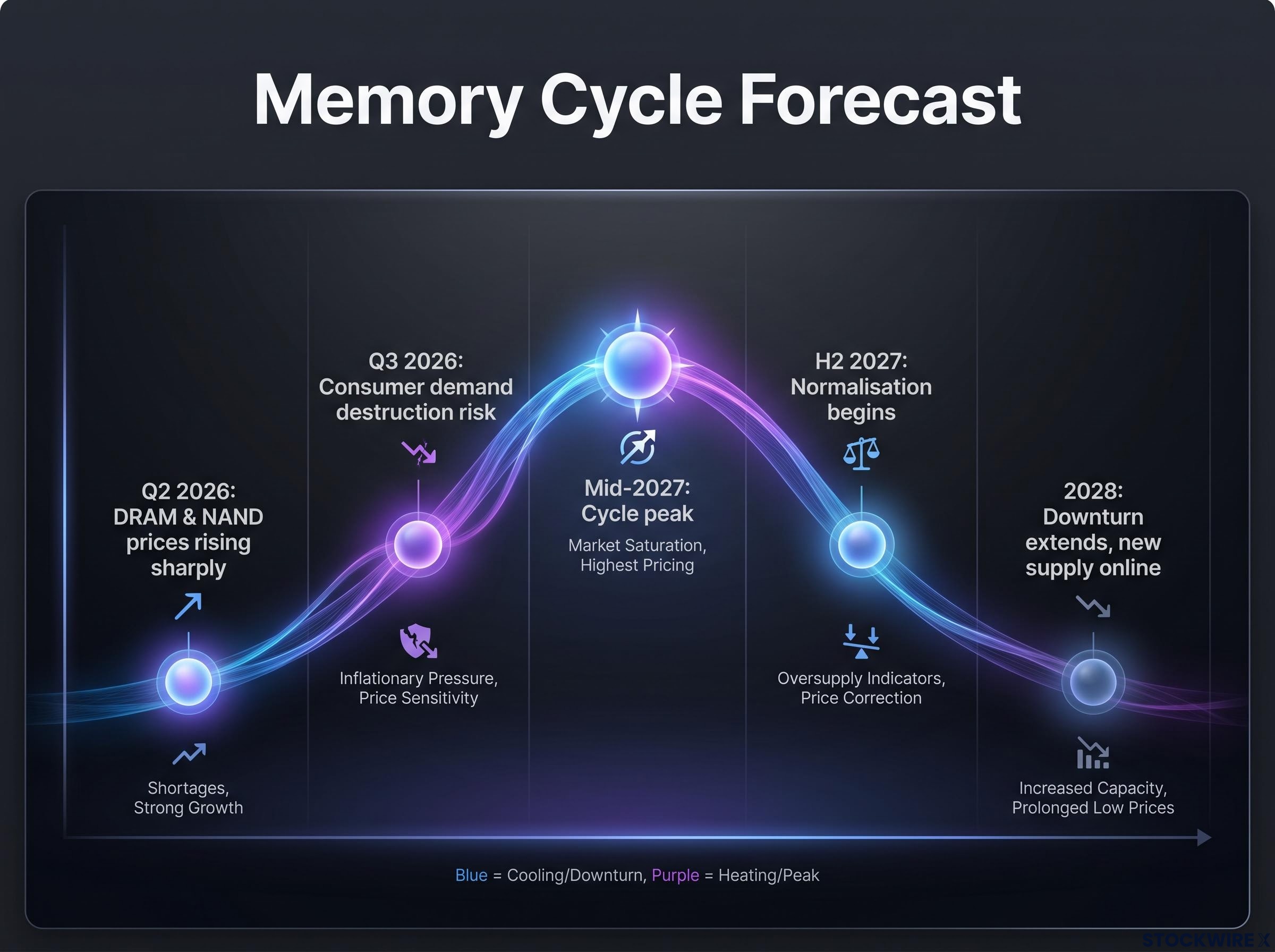

The key cycle timing data points:

Bernstein projects that even after the cycle normalises, DRAM industry gross margins could remain near 70%, above prior-cycle peaks. If that holds, it tells you the firm does not expect this cycle to end with the kind of margin collapse that has historically punished memory stocks, and that is the foundation of its willingness to maintain elevated price targets.

Three Outperform ratings from the same firm can look identical on a headline screen. They are not. Bernstein’s conviction varies by company, and the HBM leadership hierarchy is the single most relevant differentiator: SK Hynix first, Micron ramping, Samsung closing the gap.

The HBM4 supplier qualification picture reinforces the hierarchy Bernstein outlines: SK Hynix secured the earliest certification and the largest estimated volume allocation for Nvidia’s Vera Rubin platform, with Samsung and Micron qualifying subsequently and holding smaller initial shares.

For a reader weighing how to distribute exposure across these three names, the product mix is what changes the conviction level behind each rating. HBM leadership is where Bernstein sees the widest margins and the most durable pricing power.

The shift from three Outperform ratings to one Underperform is not arbitrary. It follows directly from the same framework Bernstein applies to the favoured names, just inverted.

Kioxia’s core business is NAND flash, not DRAM or HBM. That distinction is the root of Bernstein’s concern rather than any company-specific execution failure. NAND economics are structurally more commoditised, with less durable pricing power, and the competitive dynamics are tougher, particularly as Chinese capacity comes online over 2027-2028.

The three core risk factors Bernstein identifies:

Bernstein judges Kioxia’s current valuation as too rich relative to its structural risk profile. In the firm’s view, the price does not adequately discount the competitive and structural challenges ahead.

The Chinese capacity risk is not a cyclical threat that resolves with the next pricing upturn. Bernstein frames it as a structural pressure on NAND margins, which is why the Underperform is expected to persist beyond the current cycle.

Chinese memory capacity expansion by producers including CXMT and YMTC is expected to add substantial NAND and DRAM output over 2027-2028, a supply dynamic that sits at the centre of Bernstein’s structural case against Kioxia and its more cautious view on NAND-centric businesses generally.

Even the Outperform names are not immune to the eventual cycle turn. Bernstein’s thesis is about capturing the remaining upcycle, not an indefinite hold. The firm’s cycle map, in sequence:

Bernstein warns that consumer segments, specifically smartphones and PCs, are likely to see demand destruction as memory prices rise. That could slow the pace of price increases from Q3 2026 onward, even as server and AI demand remains strong.

This is the nearest-term caveat Bernstein attaches to its bull case. If you are evaluating near-term price momentum in memory stocks, the consumer slowdown should be weighed against continued strength in server and AI segments rather than treating the cycle as uniformly positive across all end markets.

Late-cycle warning signals are already visible alongside the bull case: SK Hynix’s planned 60% capacity expansion by 2030 and Samsung’s single-session decline after reporting decelerating price increases in Q2 2026 both follow the textbook pattern of supply responses that have historically ended memory upcycles.

Bernstein’s framework extends beyond individual stock ratings. The firm’s positive view on wafer fabrication equipment stocks follows directly from the capital expenditure commitments of DRAM and HBM leaders, reinforcing that the AI-driven investment cycle is expected to be multi-year, not a single-quarter phenomenon.

The three pillars of the Bernstein framework, summarised:

That extension to wafer fabrication equipment tells you the firm sees the AI-driven memory capex cycle as durable enough to lift the entire supply chain, not just the chip makers themselves. That is a materially broader claim than a standard stock rating.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These are Bernstein’s analyst views as of 13 July 2026 and do not constitute guarantees of future performance.

The clarity in Bernstein’s framework is real: the DRAM and HBM versus NAND divide is the cleanest structural call in the research, grounded in both product economics and AI demand trajectories. That part of the thesis stands on its own logic.

The conditional elements are equally clear. The bull case on Samsung, SK Hynix, and Micron depends on the upcycle extending as modelled, Chinese supply arriving on the timeline Bernstein projects, and AI server demand remaining the dominant end-market driver. If any of those variables shift meaningfully, the ratings change with them.

Three variables to watch from here:

The thesis is coherent but time-bounded. Treat the Outperform ratings as cycle-phase positions, not indefinite holds, and let the data from these three variables tell you whether the cycle is tracking as modelled or deviating.

For investors wanting to act on Bernstein’s cycle-phase framing rather than treat the Outperform ratings as indefinite holds, our dedicated guide to semiconductor cycle positioning covers the five-indicator framework and graduated de-risking sequence for capturing peak-cycle gains before the 2027-2029 supply wave arrives.

HBM, or high bandwidth memory, is the specialised chip type that powers GPUs and AI accelerators inside data centres; because AI server demand is expanding rapidly and HBM is supply-constrained, companies with leading HBM positions like SK Hynix command significantly higher margins and pricing power than NAND-focused competitors.

Kioxia's business is concentrated in NAND flash rather than DRAM or HBM, leaving it exposed to more commoditised pricing, rising Chinese supply capacity from producers including CXMT and YMTC, and with no meaningful HBM business to capture AI-driven demand; Bernstein judged its current valuation too rich relative to that structural risk profile.

Bernstein projects strong DRAM and NAND pricing through 2027, a cycle peak around mid-2027, normalisation beginning in H2 2027, and a downturn extending into 2028 as new supply including Chinese capacity comes online.

Bernstein's three key watchpoints are Q3 2026 DRAM contract price data (to gauge whether consumer demand destruction is slowing overall pricing), Samsung's HBM ramp progress (to assess whether its gap with SK Hynix is closing), and Chinese NAND capacity timing (to determine whether structural pressure on Kioxia arrives ahead of schedule).

Bernstein also holds a positive view on wafer fabrication equipment stocks, arguing that multi-year capex commitments from DRAM and HBM leaders, anchored by SK Hynix's KRW 100 trillion Cheongju facility, will drive upward EPS revisions across the broader semiconductor supply chain through 2028.