June US Inflation Report Hits as Fed Sits 9-9 on Rate Hikes

2 hrs ago

While the ASX 200 spent most of last week in retreat, three financial sector stocks quietly reached prices not seen in over a year. That kind of divergence does not happen by accident.

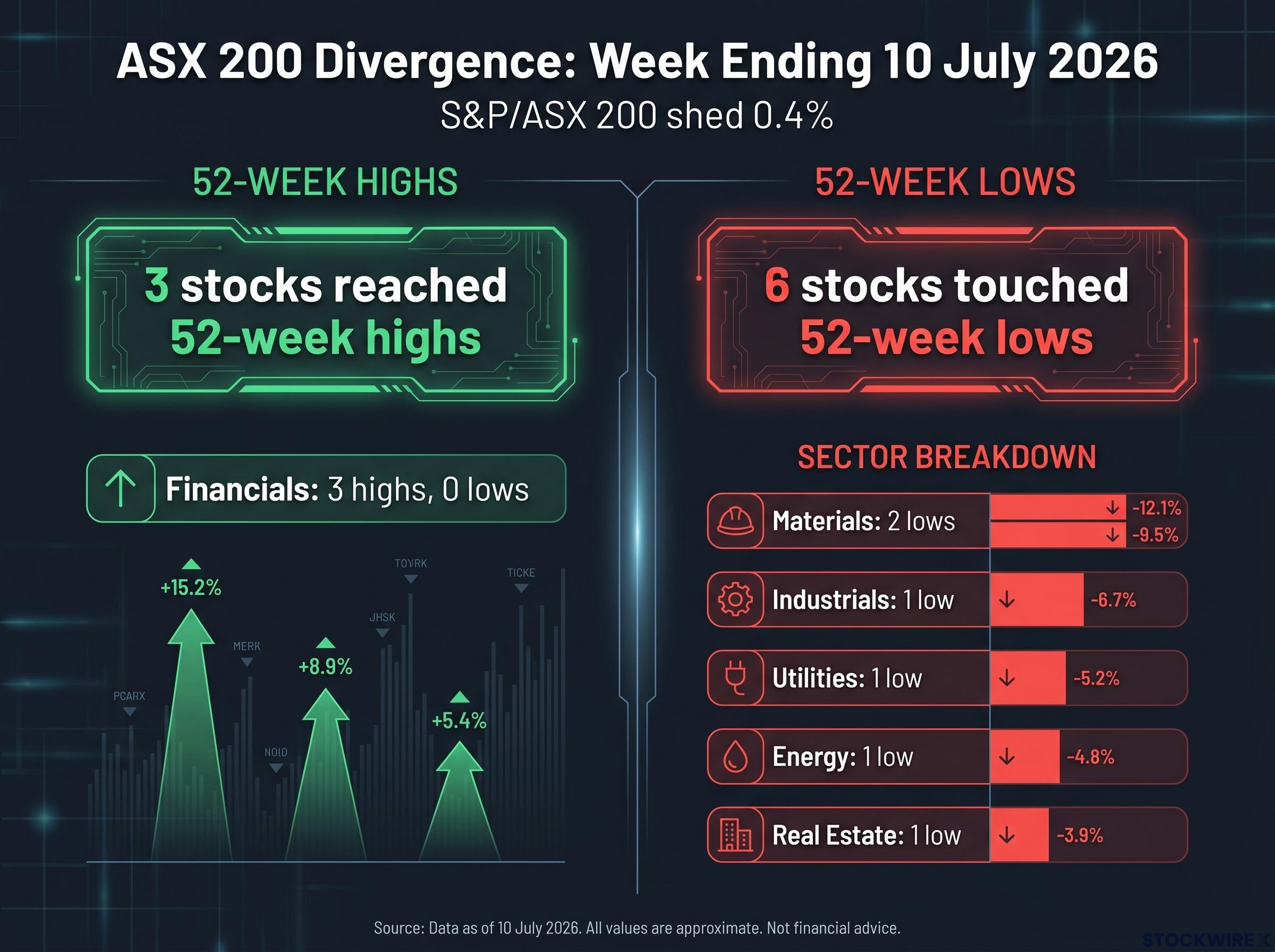

During the week ending 10 July 2026, only three stocks across the entire ASX 200 recorded 52-week highs. All three were financials: Challenger Ltd, Macquarie Group, and QBE Insurance. The index posted a net weekly loss of 0.4%, with selling pressure across four straight sessions only partially relieved by a 0.5% bounce on Friday. Materials and energy were still nursing heavy losses from recent rotations. Yet this corner of the financials sector moved against the grain.

Here is the specific catalyst behind each stock’s move, why these three stories are more different from each other than the shared sector label suggests, and what investors already holding these names should be watching now.

Only three stocks out of 200 hitting annual highs in a week the index was falling tells you something immediately: this outperformance is selective and deliberate, not a rising tide lifting financials broadly.

Institutional capital rotation out of domestic bank dividends and rate-sensitive defensives and into globally exposed names was already visible on 2 June 2026, when market breadth showed 184 decliners against 99 advancers beneath a near-flat index close, establishing the rotational pattern that carried into the financials outperformance recorded this week.

Key stat: Just 3 ASX 200 stocks reached 52-week highs during the week ending 10 July 2026, while 6 touched 52-week lows.

The S&P/ASX 200 shed 0.4% over the course of four losing sessions, with a 0.5% Friday rebound trimming but not eliminating the week’s damage. The sector breakdown of those highs and lows tells the story of where capital was rotating:

The S&P/ASX 200 Materials Index had reached a year-to-date gain of roughly 22% by 17 June 2026, only to give back most of that ground and sit at approximately 6% as of 9 July 2026. All three highs came from the same sector, but the drivers were stock-specific rather than a blanket financials re-rating.

Macquarie Group closed at $254.49 on 10 July 2026, up 1.1% for the week and 13.4% year-on-year. A measured, double-digit gain from a business this size in a volatile year is not luck. It is a function of having four separate earnings engines firing at different times.

Those four divisions, and what each contributed during this period:

| Division | Primary earnings driver | Current condition |

|---|---|---|

| Commodities and Global Markets | Trading revenue from market volatility | Elevated volatility supportive |

| Asset Management | Infrastructure and real asset capital flows | Institutional demand steady |

| Banking and Financial Services | Conventional lending margins | Stable earnings base |

| Capital Markets and Advisory | Energy transition and infrastructure deal flow | Active deal pipeline |

Macquarie’s global earnings base means it is not a pure play on Australian macro conditions. For investors comparing it to domestic banks, the question is not the share price level but whether divisional conditions (volatility, infrastructure flows, deal activity) that drove this result are durable or already priced.

Macquarie’s FY26 earnings result, which showed a 30% profit surge to $4.85 billion with Commodities and Global Markets alone up 49%, provides the quantitative foundation for why divisional conditions rather than index-level exposure drove the share price to current levels.

QBE Insurance closed at $25.47 on 10 July 2026, up 2.6% for the week and 11.0% year-on-year. Market commentary describes the move as reaching multi-year highs, not just a 52-week milestone. That distinction matters.

Multi-year highs, not just a 52-week high. QBE’s price action is consistent with comparable insurers reaching levels not seen in several years, adding further significance beyond the annual framing.

The first engine is yield sensitivity. Insurers collect premiums before they pay claims. That pool of capital (known as the float) gets invested predominantly in fixed income. When bond yields rise, the reinvestment rate on that portfolio lifts, directly increasing investment income. For a globally diversified insurer with a fixed income book as large as QBE’s, even incremental yield moves materially affect forward earnings expectations.

The second engine is the commercial insurance hard market, a period where premiums rise, underwriting standards tighten, and insurers can be more selective about the risks they take on. This cycle has been running for several years, driven by elevated catastrophe experience and claims costs. The pace of rate increases has moderated, but underwriting discipline has been maintained and conditions remain materially more constructive than five years ago.

The distinction between one engine and two is directly relevant if you hold QBE. A yield reversal or a softening pricing environment would each independently pressure earnings. Both turning negative simultaneously would be materially more damaging than either alone.

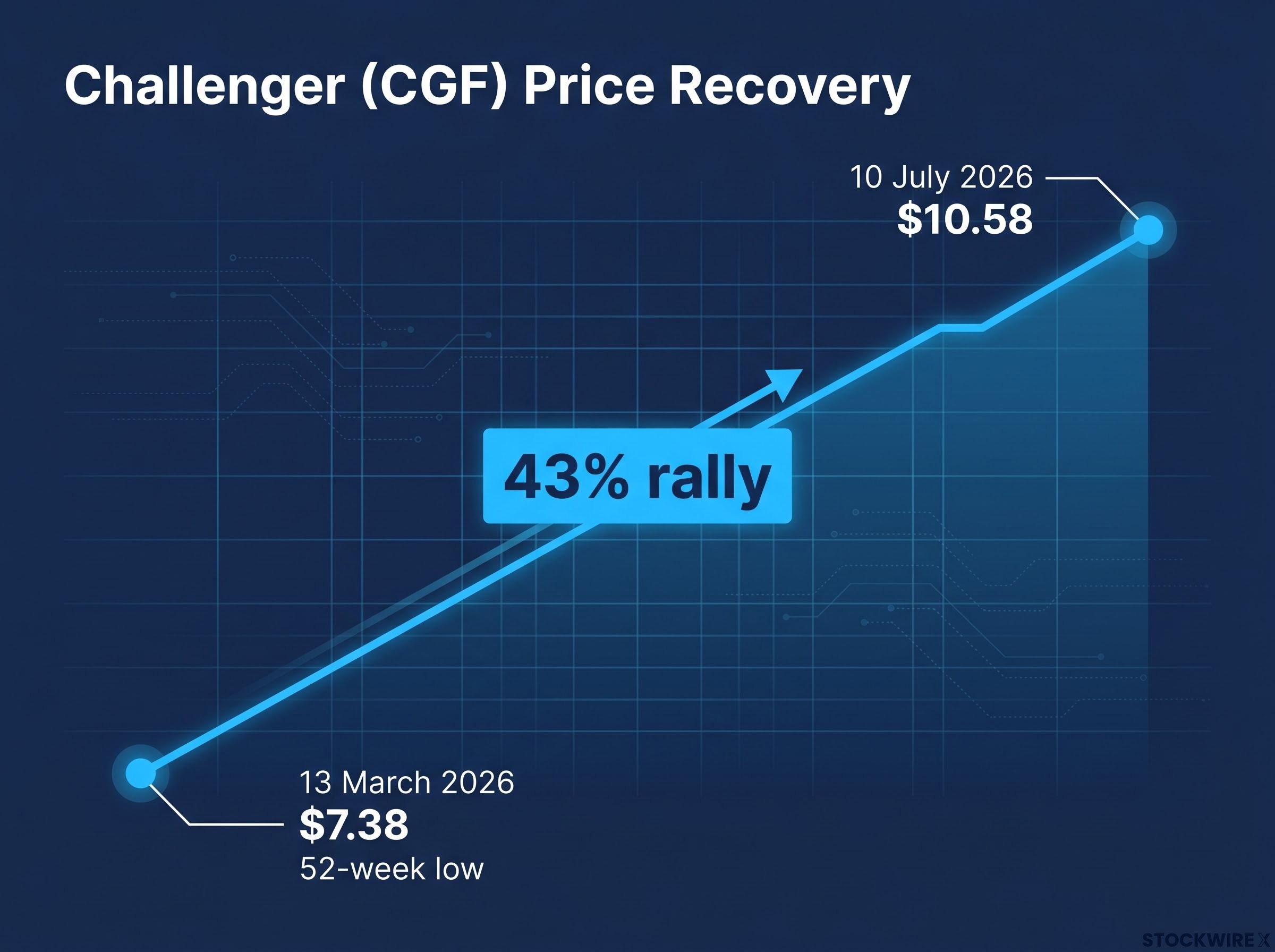

Challenger closed at $10.58 on 10 July 2026, up 2.4% for the week and 28.9% year-on-year. The stock hit a 52-week low of $7.38 on 13 March 2026, meaning it has rallied approximately 43% from trough to current levels.

43% from the March low. Challenger’s recovery from its 13 March 2026 trough represents one of the sharpest four-month moves in the ASX financials sector this year.

The stock trades above both its 50-day and 200-day moving averages, confirming a sustained uptrend rather than a single-day spike. But the price action is only the door; the structural architecture behind it is what matters.

Challenger operates as a retirement income and annuity-focused business. Higher risk-free yields allow incoming premiums to be deployed at more attractive reinvestment rates, widening spreads on new business and supporting margins on in-force annuities.

Three converging structural forces underpin the thesis beyond rates. An ageing population is increasing demand for reliable retirement income. The expanding superannuation pool requires drawdown strategies as members retire. And the Retirement Income Covenant, legislation requiring superannuation trustees to consider retirement income strategies for members, is structurally directing attention toward providers like Challenger.

The APRA capital framework changes finalised for longevity product providers, effective 1 July 2026, add a fourth structural tailwind to Challenger’s thesis: lower required capital levels reduce the cyclical drag on the balance sheet during market stress, supporting the business model precisely when annuity demand tends to spike.

APRA’s Retirement Income Covenant review, published in late 2025, found that many superannuation trustees still needed to accelerate progress on developing credible retirement income strategies for members, reinforcing the regulatory pressure that is channelling attention toward specialist providers like Challenger.

For existing holders, the 43% move from the March low is not a short-term momentum trade. It is a thesis that needs earnings results to keep validating it at the current multiple.

The coincidence of all three names hitting highs in the same week does not constitute a sector-wide signal. Treating them as interchangeable “financials exposure” means carrying three distinct and largely uncorrelated risk profiles without realising it, which has direct implications for how a portfolio behaves when one thesis breaks down.

| Company | Primary driver | Secondary driver | Key risk to watch |

|---|---|---|---|

| Challenger (CGF) | Structural retirement income demand | Rate-supportive annuity economics | Earnings delivery vs. elevated expectations |

| Macquarie (MQG) | Diversified global earnings | Energy transition deal flow | Divisional conditions (volatility, capital flows, activity) |

| QBE Insurance (QBE) | Yield-driven investment income | Hard commercial pricing cycle | Bond yield direction; pricing competition |

Before entering any of these names at or near 52-week or multi-year highs, two questions matter:

Only 3 highs across a 200-stock index during a down week. Stock selection, not sector exposure, is what this rotation is rewarding.

The forward-looking conditions for each stock are not generic macro risks but specific business-model sensitivities. Knowing which variable to track for each position is the practical takeaway from this week’s unusual concentration of highs.

Narrow breadth plus idiosyncratic drivers means sector ETF exposure does not capture this story. Each name carries a distinct thesis and a distinct set of conditions that would challenge it. Understanding which condition to monitor for each position is what separates rational position management from reacting to price action alone.

ASX 200 concentration risk means that sector ETF exposure to financials is itself dominated by the major banks, which held no position among this week’s three 52-week high achievers, illustrating precisely why a broad financials allocation would have missed the selective moves in Challenger, Macquarie, and QBE entirely.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

—

A 52-week high is the highest price a stock has traded at over the past year, and when it occurs during a broader market decline it signals selective institutional conviction rather than a rising tide lifting all stocks.

Challenger Ltd, Macquarie Group, and QBE Insurance were the only three ASX 200 stocks to record 52-week highs during the week ending 10 July 2026, while the index itself fell 0.4%.

Challenger rallied approximately 43% from its 13 March 2026 low of $7.38 to $10.58 by 10 July 2026, driven by higher reinvestment rates on annuity premiums, structural demand from an ageing population, the expanding superannuation drawdown phase, and APRA capital framework changes effective 1 July 2026 that reduced required capital for longevity product providers.

QBE's earnings are driven by two engines: investment income from its large fixed income float, which improves when bond yields rise, and commercial insurance premium pricing, which has remained elevated through a multi-year hard market driven by high catastrophe experience.

No. ASX 200 financials ETFs are dominated by the major banks, which recorded no 52-week highs this week, meaning broad financials exposure would have missed the selective moves in Challenger, Macquarie, and QBE entirely.