SK Hynix’s $26.5B Nasdaq Listing Shatters ADR Demand Records

32 mins ago

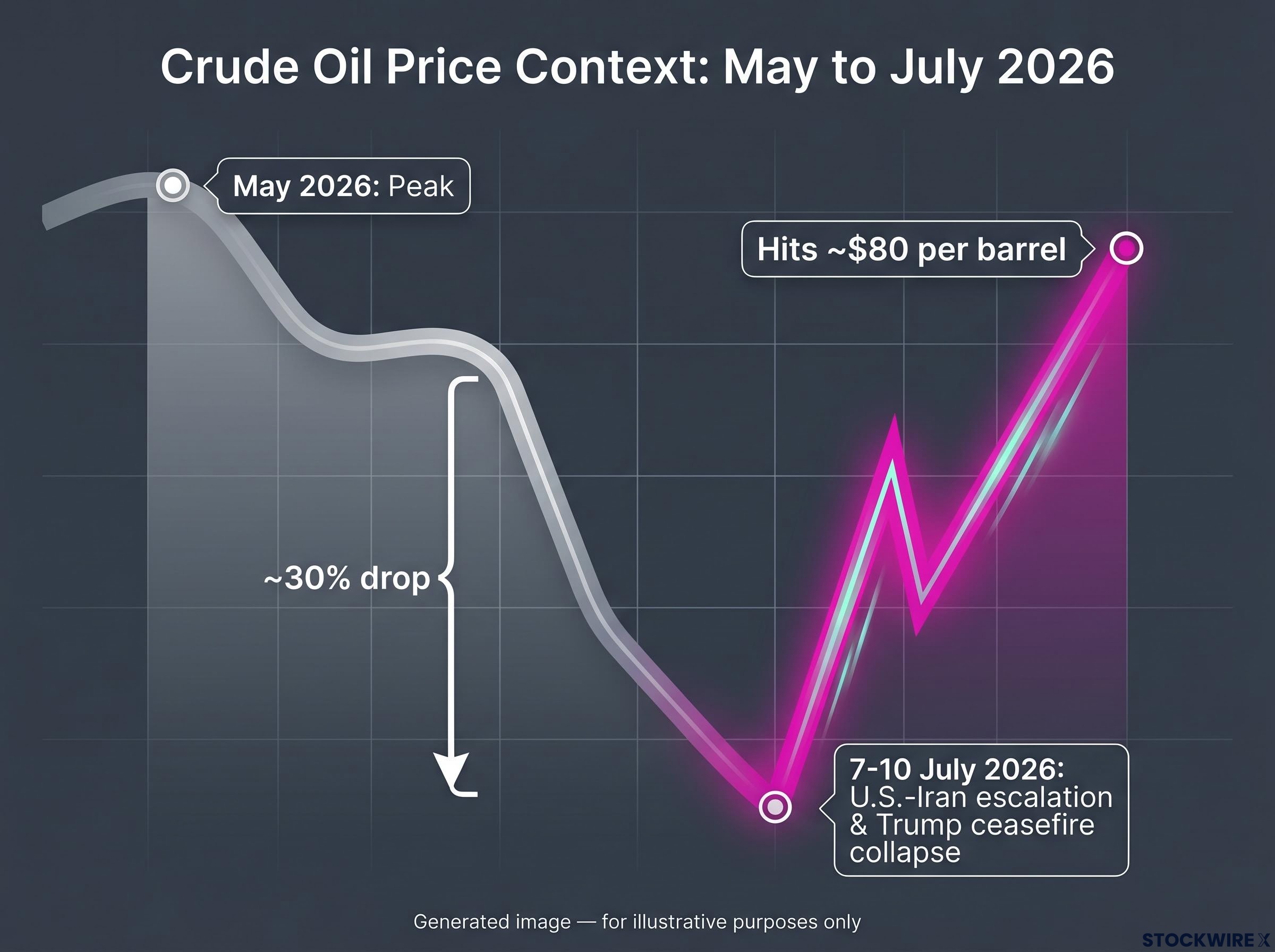

Oil prices climbed to around $80 a barrel this week as the standoff between the United States and Iran intensified sharply, with President Trump announcing that any existing ceasefire arrangement had broken down. Equity and bond markets moved in tandem, and the headlines turned alarming fast.

The instinct to treat every Middle East escalation as the beginning of something worse is understandable. But Barclays’ strategists, led by Emmanuel Cau, are pushing back. Their read is that the geopolitical panic embedded in current prices is likely larger than the probability of worst-case outcomes actually justifies.

Here is the specific reasoning behind that call, the data shaping it, and what investors watching energy markets actually need to weigh right now. The gap between Barclays’ base case and its tail-risk modelling tells you something concrete about how much protection is worth buying at these levels, and what would need to change before the alarm is warranted.

The period around 7-10 July 2026 saw a rapid and significant worsening of the U.S.-Iran situation. Events unfolded in quick succession:

The speed of the repricing was striking. Crude moved from a multi-month low to $80 in a matter of sessions, and the concurrent equity and bond selloffs signalled that markets were not treating this as a contained regional event. They were pricing in the possibility of something broader.

That reflexive severity is where Barclays’ analysis begins. The question the bank’s strategists are asking is not whether the escalation is real, but whether the market’s response to it is proportionate to the most likely outcomes.

The reflexive severity of recent market moves has a clear precedent: oil price volatility near Hormuz has repeatedly produced intraday swings of several dollars per barrel on single diplomatic signals, with Brent settling well below intraday peaks as the initial shock is absorbed and competing supply-side responses begin to register.

The $80 level looks very different once you know where oil had been. Before the geopolitical flare-up, crude had shed around 30% of its value in an almost uninterrupted slide from the peaks it reached in May 2026. That is not a gentle pullback. That is a market that had already priced in significant demand-side weakness.

Barclays’ view: The prior decline “may have been excessive relative to fundamentals,” suggesting the rebound toward $80 contains two distinct components: a genuine geopolitical risk premium and a partial correction of oversold conditions.

Barclays was not blindly bullish before the escalation. The bank had already cut its global oil demand growth estimates and lowered near-term price forecasts, citing soft high-frequency indicators. So the 30% decline was not entirely unfounded. But the scale of the move appears to have overshot what the demand data alone warranted.

For investors holding energy equities or watching commodity exposure, this distinction is practical, not academic. If part of the $80 rebound reflects a correction of prior overselling rather than purely geopolitical panic, it changes how you should interpret the current price level. It also changes what might happen if tensions ease: a full retracement back to pre-escalation lows becomes less likely if the market was already too cheap.

Barclays’ price outlook has moved materially as the situation developed, and the direction of those revisions tells you something about how the bank is processing evidence.

Earlier in 2026, when the Strait of Hormuz disruption was at its most severe, Barclays raised its 2026 Brent forecast to approximately $100 per barrel, citing a supply deficit of roughly 6.6 million barrels per day (a figure not independently confirmed in available research, and one investors should treat with appropriate caution). The bank warned that if disruptions persisted, prices could push toward $110.

Then the supply picture improved. More tankers began exiting the Strait of Hormuz. Crude shipments rose back toward pre-war levels. Barclays responded by cutting its forecasts: $96 for 2026 Brent (down from $100) and $85 for 2027 (down from $88).

| Forecast Period | Initial Forecast | Revised Forecast | Key Driver |

|---|---|---|---|

| 2026 Brent | ~$100/barrel | $96/barrel | Hormuz tanker flow recovery |

| 2027 Brent | $88/barrel | $85/barrel | Normalising supply, softer demand |

The fact that Barclays has already revised forecasts downward once in response to improving Hormuz data is itself a signal. It tells you the bank’s $96 call is conditional on supply flows remaining open, not a static view. Hormuz shipping data is the leading indicator to watch.

The breadth of institutional oil price forecasts across the crisis period illustrates how wide the scenario distribution remained even as Barclays moved toward a revised central case: the EIA, Goldman Sachs, and JPMorgan have assigned materially different probability weights to reopening and prolonged-closure outcomes, producing a forecast range spanning more than $60 per barrel.

Even after cutting forecasts, Barclays remains neutral rather than outright bearish. Still-low inventories and producer caution about expanding supply into uncertainty explain why the bank is not calling for a collapse.

The intellectual core of Barclays’ position sits in a single phrase from Emmanuel Cau:

“Fragile but probably durable equilibrium” — Barclays’ characterisation of the current geopolitical situation, attributed to strategist Emmanuel Cau

That framing is doing specific analytical work. It acknowledges the fragility (the conflict is real, the risks are live) while arguing that structural incentives make a sustained, uncontrolled escalation the less probable path.

The broader macro context reinforces this. In its Q2 2026 Global Outlook, Barclays characterised the environment as:

“Cracks, but not a crater” — surging energy prices are adding to volatility but are not breaking the global economic cycle.

The pillars supporting the equilibrium thesis include:

For investors trying to decide whether to act on the headline or hold steady, this framework provides a specific analytical reason to avoid panic-driven repositioning. It does not eliminate the risk. It argues that the probability-weighted outcome favours containment over collapse.

Barclays’ relative calm is not naivety. The bank explicitly models scenarios where the situation deteriorates far beyond its base case.

Barclays describes these conflict-scenario risks as “bigger than the Russia-Ukraine conflict” in its tail-risk framing, stronger language than a contained geopolitical moment would warrant.

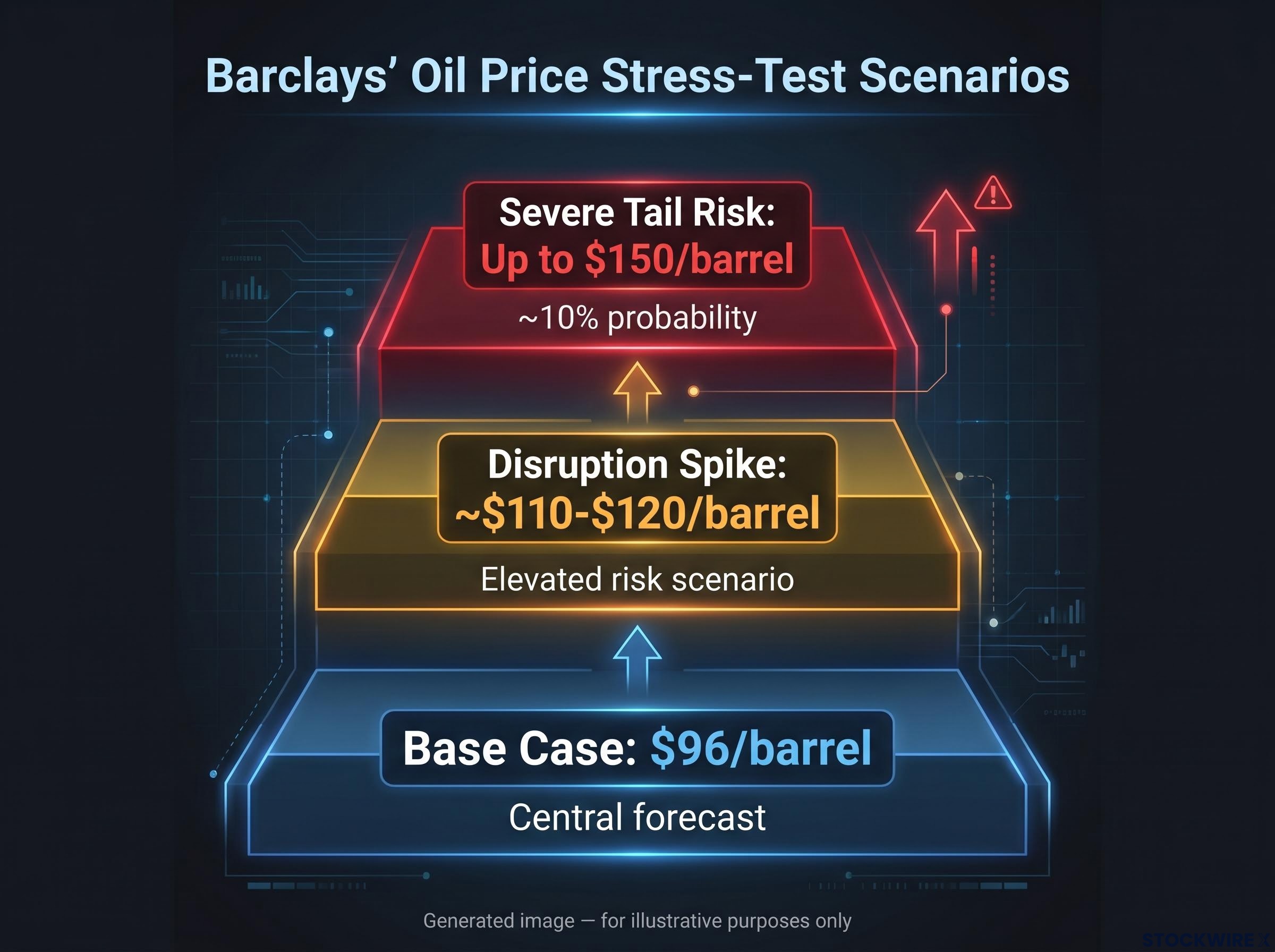

The stress-test scenarios are severe. Brent testing $120 if Middle East tensions persist and production shut-ins spread. In a 10% probability scenario, prices could potentially reach $150.

| Scenario | Brent Price Range | Probability Framing | Key Trigger |

|---|---|---|---|

| Base case | $96/barrel | Central forecast | Hormuz flows normalise, inventories draw modestly |

| Disruption spike | ~$110-$120/barrel | Elevated risk scenario | Tensions persist, production shut-ins begin |

| Severe tail risk | Up to $150/barrel | ~10% probability | Prolonged Hormuz closure, widespread shut-ins |

The 10% probability framing is doing real work. It tells you Barclays is not dismissing the extreme scenario but is treating it as a one-in-ten outcome. That has direct implications for how much portfolio protection is worth buying at current prices. Hedging against a 10% probability event carries meaningful cost if the base case holds, and Barclays is betting the base case holds.

The analytical framework is only useful if it translates into something you can monitor. Here are the specific variables that will determine whether Barclays’ base case holds or the tail risks begin closing in:

The inventory drawdown pace underpinning Barclays’ floor thesis is severe enough that emergency reserve releases have proven structurally insufficient: global inventories drawing at 8.5 million barrels per day in Q2 2026, with usable buffer estimated at around 800 million barrels, means the low-inventory price floor is not a temporary condition that resolves with improved diplomatic signals.

One important caveat: the supply deficit figure of approximately 6.6 million barrels per day attributed to Barclays was not independently confirmed in available research. Investors should verify this figure before incorporating it into any direct positioning decisions.

Investors who treat every Iran headline as a signal to act will be whipsawed by exactly the kind of episodic volatility Barclays is explicitly expecting. The more durable strategic posture is to track the underlying flow and inventory data that will confirm or challenge the equilibrium thesis over the coming weeks.

Barclays is not dismissing the geopolitical risk and it is not forecasting uncontrolled escalation. The call is for a high-but-rangebound oil market with episodic volatility driven by headlines, anchored around a revised 2026 Brent forecast of $96 per barrel.

The bank’s willingness to cut that forecast from $100 as Hormuz flows improved is itself evidence of a data-responsive analytical stance, not a static bullish position. The tail risks are real and severe, with $120-$150 Brent modelled at roughly 10% probability. But the base case, a fragile but probably durable equilibrium, remains intact.

The tension Barclays is holding is the tension every investor watching crude oil prices faces right now. The equilibrium is fragile. The worst-case scenarios are genuinely alarming. But panic-driven repositioning carries meaningful reversal risk if the more probable path, containment and episodic volatility, plays out.

For investors wanting to model what a base-case containment scenario actually means for long-term crude price levels, our full explainer on crude oil’s structural price floor examines why war-risk insurance timelines, SPR replenishment demand, and physical flow lags keep Brent well above $70 even after ceasefire announcements.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including price forecasts and scenario projections, are subject to market conditions and various risk factors. Past performance does not guarantee future results.

Barclays revised its 2026 Brent crude oil forecast down to $96 per barrel from $100, cutting its 2027 forecast to $85 from $88, after tanker flows through the Strait of Hormuz began recovering toward pre-war levels.

Crude oil prices surged toward $80 per barrel around 10 July 2026 after President Trump announced that any ceasefire with Iran had collapsed, triggering concurrent selloffs in equity and bond markets as investors repriced the risk of a broader conflict.

The Strait of Hormuz is a critical maritime chokepoint through which a significant share of global crude oil shipments pass; any disruption to tanker flows there directly tightens global supply and pushes prices higher, which is why Barclays treats Hormuz shipping data as the single most important leading indicator for its oil price forecasts.

Barclays models Brent reaching up to $150 per barrel in a severe tail-risk scenario involving a prolonged Hormuz closure and widespread production shut-ins, assigning this outcome roughly a 10% probability, with an intermediate disruption scenario placing Brent in the $110-$120 range.

The four variables Barclays' framework depends on are Hormuz tanker flow data, the pace of global inventory drawdowns, White House statements on the conflict's direction, and producer decisions on supply expansion into the current uncertainty.