Where Gold Is Headed in H2 2026 After a US$1,500 Crash

1 hr ago

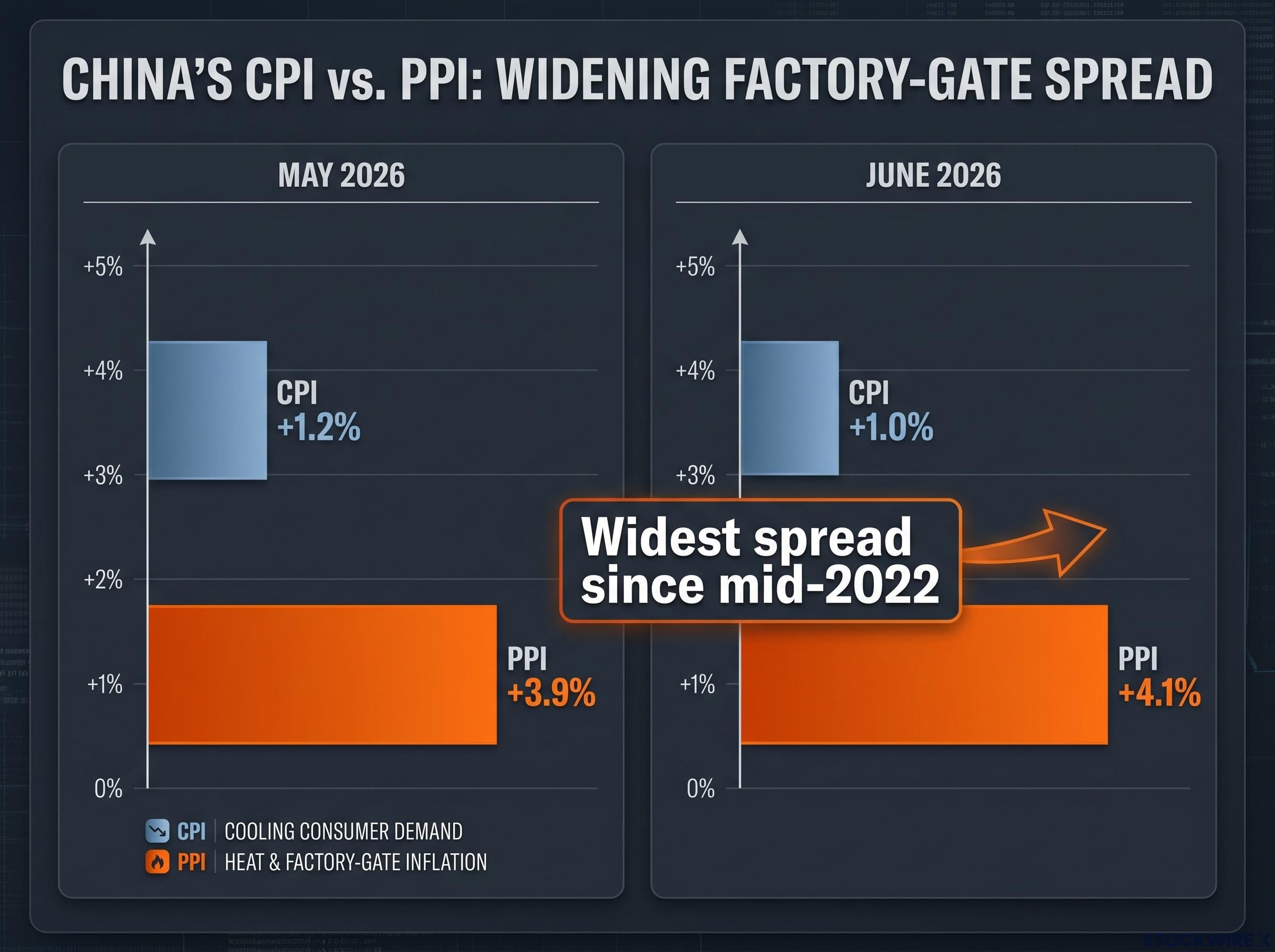

China’s consumer price index rose 1.0% year-on-year in June, missing forecasts. Its producer price index rose 4.1%, the fastest pace since July 2022. One number says households are barely spending more. The other says factories are paying sharply more. The gap between them is the story.

This is not a single-month anomaly. May’s data showed the same split: CPI at 1.2%, PPI at 3.9%. Two consecutive months of widening divergence, with the factory-gate acceleration driven partly by something most inflation frameworks do not account for: AI-driven semiconductor demand pushing up hardware input costs across Chinese manufacturing.

Here is what that divergence actually tells you. The cost pressure building inside China’s manufacturing base has not yet surfaced in consumer prices, either domestically or in the goods that Chinese factories export globally. This piece maps where that pressure is accumulating, what is driving it, how it transmits into global supply chains, and what it means for anyone with exposure to technology hardware, Chinese equities, or multinational sourcing costs.

The National Bureau of Statistics (NBS) released both figures on 9 July 2026, and the paired reading is more instructive than either number alone.

| Indicator | May 2026 | June 2026 | Context |

|---|---|---|---|

| CPI (YoY) | +1.2% | +1.0% | Below consensus forecast of +1.1% |

| CPI (MoM) | -0.1% | -0.3% | Worse than projected -0.2% decline |

| PPI (YoY) | +3.9% | +4.1% | Highest annual reading since July 2022 |

The monthly CPI reading came in at -0.3%, undershooting the anticipated -0.2% fall and deepening the picture of consumer retrenchment rather than offering any reassurance. Consumers are not absorbing higher prices. They are pulling back.

Meanwhile, factory-gate inflation has now strengthened for two successive months, with PPI climbing from 3.9% to 4.1% and reaching its highest annual rate in close to four years. The spread between what producers pay and what consumers spend is widening, and that gap defines where margins are being compressed and where pricing risk has yet to surface.

China’s two-speed economy had already surfaced in May 2026 trade data, with semiconductor exports surging 111% year-on-year to approximately $36 billion while domestic consumer spending contracted 0.6%, confirming that the CPI-PPI divergence visible in price data reflects a broader structural split rather than a single-month pricing anomaly.

CPI tracks what households pay for a basket of goods and services, from groceries to rent to transport. It is a downstream price signal: it captures the final price the consumer sees.

PPI tracks what factories pay for inputs and receive for their output at the production stage. It is an upstream price signal: it captures cost pressure before it reaches a shop shelf or a consumer invoice.

The key distinctions:

That spread is now at its widest since mid-2022. The companies assembling goods in China are caught between input costs that are accelerating and a consumer base that cannot, or will not, absorb higher prices. That squeeze has persisted across two months and shows no sign of closing on its own.

NBER research on PPI-CPI transmission establishes that the lag between producer and consumer price adjustment is highly sensitive to demand conditions, with weak final demand causing firms to absorb upstream costs rather than pass them through, exactly the dynamic compressing margins across China’s manufacturing base now.

Three forces are pushing PPI higher, and they are worth understanding in ascending order of how unusual they are.

The third driver is the one that changes the character of this inflation story.

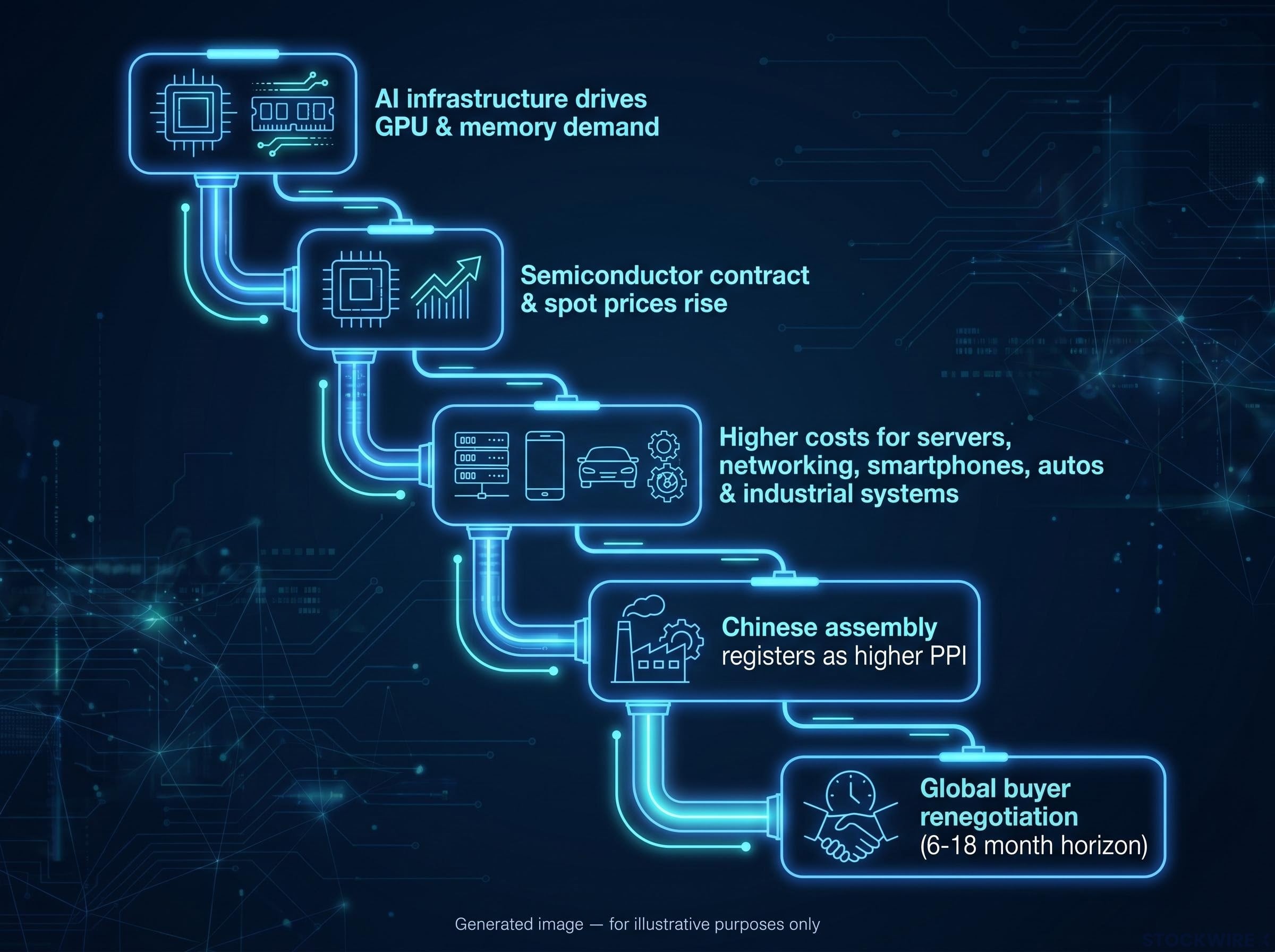

The NBS chief statistician explicitly linked part of the wholesale price surge to the “swift transition to electrification, intensified AI integration, and soaring demand for computing power,” which have raised costs across non-ferrous, electrical, and computer hardware categories.

S&P Global Ratings has extended memory chip price forecasts through at least 2028, with Samsung, SK Hynix, and Micron collectively redirecting capacity toward high-bandwidth memory for AI customers and structurally tightening commodity memory availability across the electronics supply chain.

CNBC’s reporting corroborates the linkage, noting that AI computing demand is contributing to higher prices for technology equipment and semiconductors alongside the commodity shock. This is not a conventional cost-push cycle driven purely by energy markets. It is a structural cost increase rooted in the global buildout of AI infrastructure, and it is showing up in the factory-gate data of the world’s largest manufacturing economy.

The distinction matters: cost-push inflation, which is what China’s upstream economy is experiencing, behaves differently from demand-pull inflation. It does not respond to interest rate adjustments in the same way, and it does not resolve simply because consumer demand stays weak. It persists as long as the forces feeding it, AI capital expenditure, energy costs, industrial policy, remain in place.

The transmission path from a Chinese PPI print to a cost problem in a boardroom in Munich, Seoul, or San Jose follows a specific sequence:

The current transmission is likely gradual and partial. Chinese exporters are absorbing a portion of the cost shock to defend market share, which tempers the direct inflation spillover into US and European consumer prices in the near term. But persistent upstream pressure at these levels raises the risk of stepwise price adjustments in goods categories over a 6-18 month horizon, an analytical inference based on the typical lag between PPI and CPI transmission.

The highest-exposure segments are energy-intensive and tech-heavy goods: server components, consumer electronics, power equipment, and industrial machinery.

Higher Chinese production costs do narrow the cost differential with alternative manufacturing locations in Vietnam, India, and Mexico for certain categories. But the energy and AI-linked component costs driving PPI higher are not unique to China. Semiconductor prices are a global phenomenon. Energy costs are a global phenomenon.

Production footprint decisions are driven by scale, lead times, and supplier ecosystems as much as unit cost. China’s depth across all three means that PPI acceleration reshapes the manufacturing calculus without reversing it. The result is incremental fine-tuning of supply chains rather than wholesale shifts, particularly for high-value or time-sensitive production that depends on China’s supplier density.

The CPI-PPI spread is not a single signal. It carries different implications depending on where your exposure sits.

Corporate margin compression operates differently depending on where a firm sits in the value chain: US nonfinancial after-tax margins reached a record 14.4% in Q1 2026, but that aggregate conceals wide dispersion between companies with hardware pricing power and those absorbing upstream cost increases without the ability to pass them through.

CNBC analysts note that “until domestic demand rebounds, the pressure on factory margins will only increase.”

That assessment captures the core tension. The margin squeeze is not self-correcting while the forces driving it, AI chip demand, energy costs, and industrial policy, remain intact.

The divergence has two plausible resolution paths, and which one materialises determines whether the cost pressure currently bottled up in Chinese factories eventually becomes a consumer inflation event in importing economies.

If China’s property sector stabilises, consumer confidence improves, and services spending grows, domestic demand would begin pulling CPI upward toward PPI. The margin squeeze on manufacturers eases. But the trade-off is that the cost pressure currently absorbed at the factory level would start transmitting into consumer prices, both domestically and in export markets. The gap closes, but the closing mechanism introduces a different risk: broad consumer inflation in the world’s second-largest economy.

If domestic demand remains soft while energy, semiconductor, and industrial input costs stay elevated, the margin compression deepens. Factory profitability deteriorates. Eventually, exporters who have been absorbing costs to defend market share reach the limit of that absorption, and export prices adjust upward. The cost pressure that has been contained domestically begins to migrate into global goods prices, with a lag.

The persistence of the divergence across May and June, with CPI decelerating from 1.2% to 1.0% while PPI accelerated from 3.9% to 4.1%, suggests resolution is not imminent. The structural forces sustaining it, AI chip demand, energy costs, and policy-driven industrial upgrading, are not dissipating quickly. And the trajectory of global AI capital expenditure, in particular, sustains upstream hardware price pressure regardless of what Chinese household consumption does.

The variables that distinguish which scenario emerges are specific and trackable: Chinese household consumption data, property sector stabilisation signals, and the pace of global AI infrastructure investment.

The CPI-PPI divergence is not primarily a story about weak Chinese household demand, although that is part of it. It is a window into where global cost pressure is accumulating: in AI hardware, in energy inputs, and in the manufacturing infrastructure that the world’s technology and industrial supply chains still depend on.

The AI mechanism is what distinguishes this episode from prior PPI spikes. Previous divergences were largely commodity-cycle driven. This one has a structural technology layer that will persist as long as AI infrastructure investment continues to accelerate, and every major cloud and semiconductor company’s capital expenditure guidance suggests it will.

Whether you are a supply chain strategist, an equity investor, or a macro analyst, the monthly CPI-PPI spread from China’s NBS is now a more consequential data release than it was three years ago.

PPI at 4.1% in a manufacturing economy of China’s scale is not background noise. It is a leading signal for procurement costs, margin pressure, and hardware inflation across the most consequential supply ecosystem in the world. Tracking it is no longer optional for anyone with exposure to global technology hardware, manufacturing costs, or AI infrastructure investment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements and analytical inferences regarding supply chain transmission timelines and scenario outcomes are subject to change based on market developments and policy decisions.

China's CPI measures what households pay for a basket of goods and services, capturing downstream consumer prices, while PPI measures what factories pay for inputs and receive at the production stage, capturing upstream cost pressure before it reaches consumers.

Three forces are driving China's PPI higher: elevated global energy and commodity costs linked to supply disruptions, Beijing's industrial policy reducing excess capacity, and AI-driven semiconductor demand pushing up memory chip and electronics hardware input prices, with the NBS chief statistician explicitly citing AI integration and computing power demand as a contributor.

The gap signals that cost pressure is accumulating inside Chinese factories without yet surfacing in consumer or export prices; over a 6-18 month horizon, persistent upstream pressure raises the risk of stepwise price adjustments in technology hardware, consumer electronics, and industrial goods for global buyers.

Companies sourcing from China face contract renegotiation pressure as suppliers attempt to protect shrinking margins; firms with pricing power in AI servers and high-end networking equipment can pass costs through, while mass-market consumer electronics brands must choose between compressing margins or risking volume loss by raising retail prices.

Either domestic demand recovers and CPI catches up to PPI, easing factory margin pressure but introducing consumer inflation risk in China and export markets, or demand stays weak and exporters who have been absorbing costs eventually reach their limit, pushing export prices upward and migrating the cost pressure into global goods prices with a lag.