How ASX’s CHESS Overhaul Became a $250M Governance Failure

Jul 6, 2026

You have probably done this before. You found a company you genuinely admired, one with accelerating revenue, expanding margins, and a product you used every day. You bought the stock. Then you watched it drift sideways for years while the business kept posting record numbers. The frustration was real, and the confusion was worse.

The problem was never the company. The company was fine. The problem was the price you paid for it. This is the most common and least-discussed mistake in retail investing: confusing admiration for a business with a sound investment thesis. Netflix is the perfect case study precisely because it scores exceptionally well on almost every fundamental quality metric. It is, by most measures, a genuinely great business, and that is exactly what makes it such a useful illustration of where the trap sits.

Here is a reusable process for separating business quality from investment quality, grounded in Netflix’s real numbers so the distinction stays concrete. You will leave with a framework you can apply to any stock in your portfolio this week, not just a view on one streaming company.

This is not a failure of intelligence. It is a structural pattern, and it catches investors at every experience level. The distinction sits in three definitions that most people conflate:

Warren Buffett has emphasised for decades that earnings power and pricing power matter enormously, but only if you do not overpay for them. Peter Lynch framed the flip side: when a company’s fundamentals improve while its share price falls, the market is offering you a better deal, not sending a warning signal. A declining price alongside improving business quality is an attractive setup for disciplined investors, not a reason for alarm.

The LSV contrarian investment research by Lakonishok, Shleifer, and Vishny established that investors systematically overpay for high-growth companies by extrapolating past performance into the future, precisely the behavioural pattern that turns a genuinely great business into a poor entry point.

Microsoft and Cisco after 2000, and several large-cap growth names after 2021, illustrate exactly what happens when admiration overrides price discipline. In each case, the businesses eventually performed well. The investors who overpaid did not, at least not for many years.

The historical record on price vs value investing is unambiguous: investors in the Nifty Fifty lost roughly 90% of their portfolio value between 1968 and 1973 despite holding world-class businesses like Coca-Cola and IBM, because they paid 80-90 times forward earnings for companies whose quality was never in question.

If you have ever held a stock that went nowhere while the company kept growing, this is the mechanism that caused your frustration. It was always price. It was never business quality.

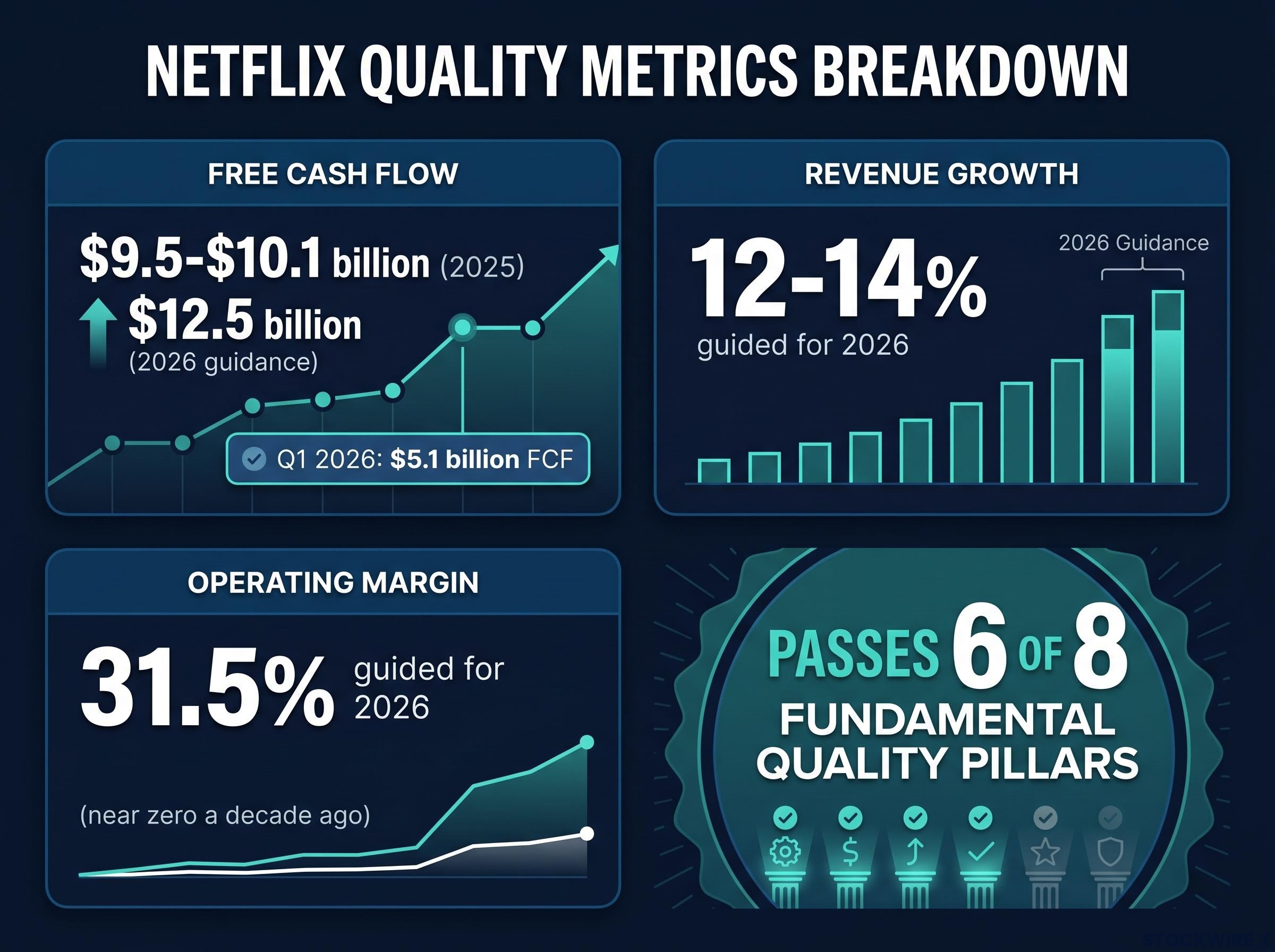

Before any discussion of price, you need to see the quality case clearly. If you skip this step and jump straight to valuation, you risk misreading everything that follows as a bearish call on Netflix. It is not. This is a business that passes six of eight fundamental quality pillars. The two that fail are valuation-specific, not quality-specific, and that distinction is the entire point of the article.

| Metric | Recent figure | Direction | What it signals |

|---|---|---|---|

| Free cash flow | $9.5-$10.1 billion (2025); $12.5 billion guided for 2026 | Accelerating | Genuine cash generation, not just accounting profit |

| Revenue growth | 12-14% guided for 2026 | Sustained above average | Pricing power and subscriber base still expanding |

| Operating margin | 31.5% guided for 2026 | Expanding (near zero a decade ago) | Structural profitability shift, not a cyclical blip |

| Return on invested capital | Strong across recent and five-year periods | Stable to improving | Management is allocating capital productively |

Add active share repurchases and a reasonable debt load relative to earnings, and the picture is clear. Q1 2026 alone delivered $5.1 billion in free cash flow.

Scorecard verdict: On six of eight fundamental quality pillars, Netflix earns a positive result. The remaining two are valuation measures rather than indicators of operational health. What warrants attention here is not the underlying business, but the price the market is currently charging to own it.

Any concern raised from this point forward is a concern about what the market is charging to own Netflix, not about the company itself. Those are categorically different concerns, and they require categorically different responses from you as an investor.

The following scenarios are not forecasts. They are structured estimates designed to test what would need to be true to justify Netflix’s current valuation. Even with disciplined assumptions, any intrinsic value estimate could be off by 20-30% in either direction. That is not a hedge; it is an honest statement about the limits of any valuation model, and acknowledging it actually makes the exercise more credible.

The model uses a 10-year forward projection period with a 9% required return applied across three scenario sets:

The discipline of intrinsic value estimation requires stress-testing the terminal value assumption above all else: that single input typically drives 60-80% of a DCF model’s total implied price, meaning small changes in assumed long-run growth or exit multiple produce enormous swings in what the model says a business is worth.

| Scenario | Revenue growth | FCF margin | Exit multiple | Implied intrinsic value |

|---|---|---|---|---|

| Conservative | 6% | 20% | 20x | ~$50 per share |

| Base | 8% | 23% | 23x | ~$74 per share |

| Optimistic | 10% | 26% | 26x | ~$107 per share |

Independent valuation estimates using similar assumptions often cluster around $70-$72 per share, corroborating the base case.

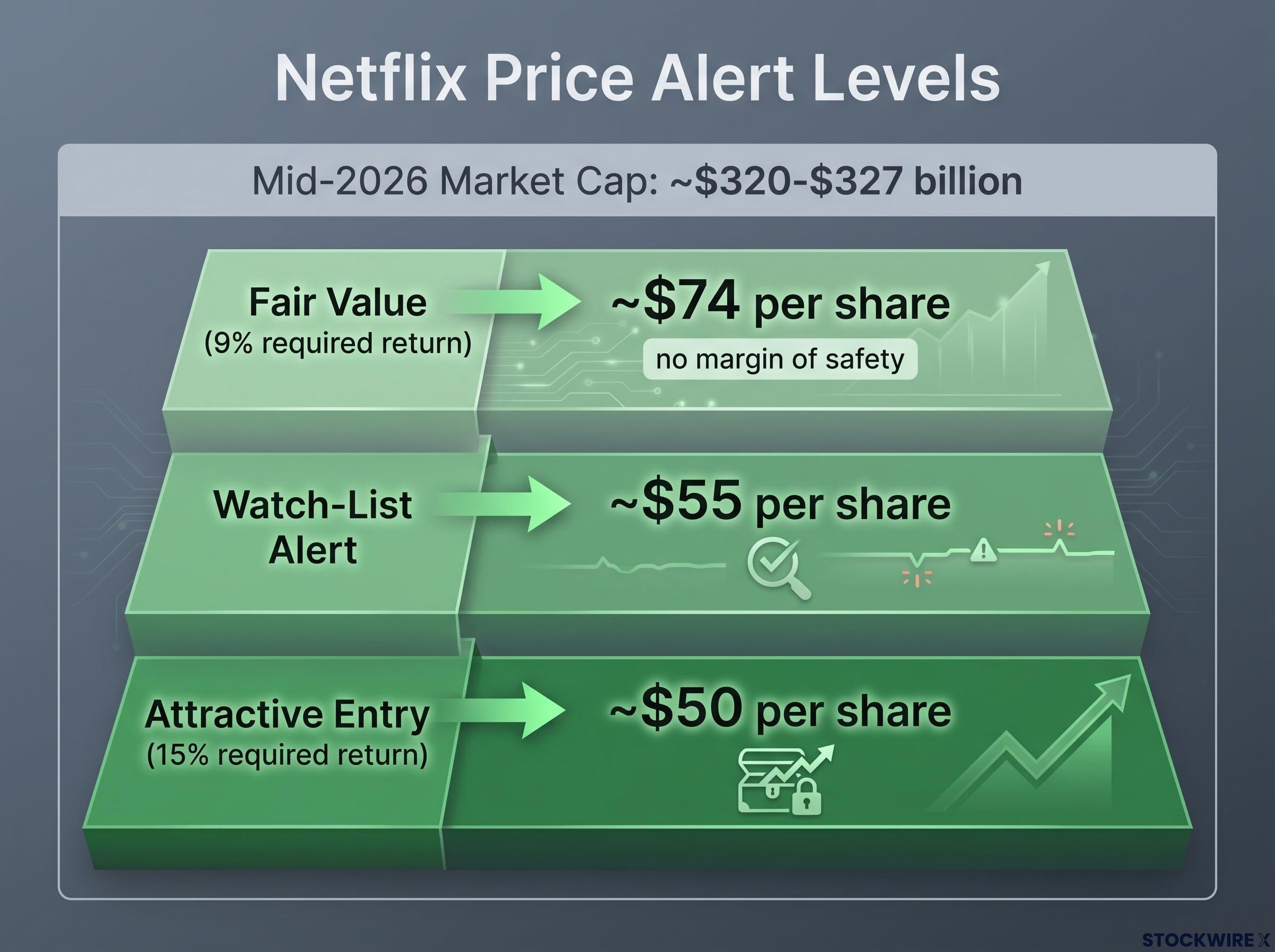

Netflix’s market capitalisation sits at approximately $320-$327 billion as of mid-2026. The long-run average price-to-earnings multiple for the broad market is approximately 15-16x. Even with a premium 20-26x multiple applied to reflect above-average business quality, the current market price sits well above every scenario in the range.

What today’s price requires: the current valuation leaves no tolerance for shortfall. For the share price to be justified, revenue growth, margin expansion, and exit multiples would all need to land at or near the top of their plausible ranges across the entire decade. Buying at this level means paying not for a high-quality business, but for a flawless one.

The valuation gap does not predict Netflix’s next price move. The stock could rise further from here. What the gap tells you is more useful than a direction call: it tells you the expected long-term return from today’s entry price, and that expected return is not especially attractive relative to the risk you are accepting.

The law of large numbers makes this pressure structural. As Netflix’s revenue base grows beyond $40 billion, sustaining 10% annual growth requires adding progressively larger absolute revenue each year. That is a mathematical reality, not a management critique. Your valuation model needs to reflect realistic deceleration, not an indefinite extrapolation of peak growth.

Margin of safety is the discount you demand from intrinsic value to protect against two things simultaneously: the possibility that your estimate is wrong, and the opportunity to earn attractive returns if your estimate is roughly right. It is not timidity. It is the rational response to uncertainty.

Value investors define risk as the probability of permanent capital loss rather than short-term price volatility, a distinction that reshapes how margin of safety is calibrated: a business with high earnings predictability warrants a smaller discount to intrinsic value than a speculative one, because the range of plausible outcomes is meaningfully narrower.

The specific buy thresholds derived from the model above give you concrete numbers to work with:

| Return requirement | Implied buy level | Interpretation |

|---|---|---|

| 9% required return (no buffer) | ~$74 per share | Fair value, no margin of safety |

| 15% required return (selective) | ~$50 per share | Attractive entry with meaningful downside protection |

| Watch-list alert level | ~$55 per share | Stock entering a range worth active monitoring |

With Netflix valued above $320 billion, the implied share price sits far above every one of these thresholds.

Consider two investors holding the same stock after a 20% decline:

The business is identical in both cases. The emotional and financial experience is not. What separates them is entry price.

Set a specific price alert for Netflix right now, not a vague intention to “keep an eye on it.” Ground that alert in your own required return, not in what you expect the stock to do next week.

This is the framework that converts everything above into a repeatable process you can run on any position you currently hold or are considering. The sequence matters:

Running Netflix through step one produces a clear result: six of eight quality pillars come back positive, placing the business firmly in the “high quality” category. Step four, however, rules out a purchase at current prices: the buy level sits around $50-$55 per share based on a 15% required return. The correct output is a watch-list entry with a specific trigger, not a trade.

Run this process on any stock in your portfolio this week. You will almost certainly find at least one position where you have never explicitly set a required return threshold.

Investors who overpaid for Microsoft and Cisco after 2000, and for several large-cap growth names after 2021, eventually saw the businesses perform well, but waited years just to break even themselves.

The Netflix repricing since its June 2025 peak involved four compounding forces beyond valuation: subscriber growth deceleration, a governance transition as Reed Hastings stepped back from the board, a failed acquisition attempt that raised capital allocation concerns, and sector rotation away from steady compounders toward AI-linked names.

Netflix may be a wonderful buy at some future price. The framework you have built here tells you what that price is: a watch-list alert at approximately $55 per share and a buy level at approximately $50 per share. Until the market offers the stock in that range, the disciplined output of the process is inaction, and inaction is not a failure to act. It is the specific, informed result of a framework that has simply not yet produced a buy signal. Recognising that distinction is what separates investors from speculators.

A declining price alongside stable or improving fundamentals is an attractive setup, not a reason for alarm. If Netflix’s business quality remains intact and the share price eventually corrects, the framework tells you exactly when to act and why.

“Business quality and investment quality are separated by price.”

You now have the tools to tell the difference. The job is not to chase a great story at any price. It is to know roughly what a business is worth, set your threshold, and wait for the market to offer it at a discount.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. The valuation scenarios presented are illustrative and subject to market conditions and various risk factors.

—

A great company has strong fundamentals, durable competitive advantages, and expanding margins; a great investment adds one more requirement: a favourable price relative to the future cash flows the business will generate. Paying too much for even an exceptional business destroys returns.

Margin of safety is the discount you demand below a company's estimated intrinsic value before buying, designed to protect against estimation errors and to generate attractive returns if your estimate is roughly correct. For Netflix, the article places the margin-of-safety buy level at approximately $50 per share, far below its current market price.

Using a 10-year projection with a 9% required return, the base case produces an intrinsic value of approximately $74 per share, with the conservative scenario at $50 and the optimistic scenario at $107; all three sit well below Netflix's current market price of around $320-$327 billion in total market capitalisation.

The five-step process starts by assessing business quality in isolation before looking at the price, then builds conservative, base, and optimistic valuation scenarios, sets a personal required return, applies a margin of safety calibrated to business predictability, and finally sets specific price alerts rather than acting on vague intentions.

The framework in the article places a watch-list alert at approximately $55 per share and a buy level at approximately $50 per share, based on a 15% required annual return; until the market offers the stock in that range, the disciplined output is inaction.