Samsung Posts Record AI Chip Profit, Then Its Stock Falls 6%

4 hrs ago

The New Mexico jury that returned a $375 million verdict against Meta in March 2026 did more than set a dollar figure. It answered a question the market had been treating as unresolved: will American juries accept the argument that social media platforms were engineered to addict children, and punish the companies accordingly?

The answer is now on the record. And the verdict is not an isolated event.

It sits at the front of a litigation wave that includes 29 states in federal court, a federal trial scheduled for August 2026, a second federal proceeding set for February, and thousands of individual cases still working through state and federal dockets. Meta, Snap, Alphabet, and TikTok are all named. The core legal theories are the same. The financial exposure is sector-wide.

Here is what the verdict actually established, how each company’s exposure profile differs, which upcoming legal milestones should trigger a reassessment of position sizing, and why the risk that standard valuation models are missing is not the penalty dollars but the court-ordered product changes that follow them. The $375 million headline is the entry point, not the ceiling.

The number matters, but what the jury found matters more. New Mexico jurors concluded that Meta willfully violated the state’s Unfair Practices Act (a consumer protection statute that penalises deceptive business conduct) by misleading the public about the safety of Facebook, Instagram, and WhatsApp for children. The finding was intentional misconduct, not mere negligence. That distinction reshapes how subsequent juries and settlement negotiations will be calibrated.

The penalty came to $375 million in civil fines, calculated at $5,000 per violation across thousands of individual violations. New Mexico’s attorney general had sought up to $2 billion, so the award landed well below the maximum ask, but it still represents the first state-led child-safety verdict of this magnitude against a major social media company.

New Mexico Attorney General’s public statement: “Meta executives were aware that their products were harmful to children, ignored warnings from their own staff, and misled the public.”

That language is significant for investors. “Aware,” “ignored,” and “misled” are the words that convert this from a negligence story into a concealment story, and concealment stories raise both jury sympathy and potential damage floors across every pending case that shares the same theory.

Meta has stated its intent to appeal. The appeal does not pause what comes next.

A second, non-jury phase of the New Mexico proceedings is currently underway before a state judge. This phase addresses whether Meta created a public nuisance and should be required to implement court-ordered changes to its platforms. The remedies New Mexico is seeking include:

These are not financial penalties. They are structural product mandates. Whatever changes the New Mexico court ultimately orders will likely serve as a template for demands by other states, which means the phase-two outcome could set the design standard for how these platforms are required to treat users under 18 across the country.

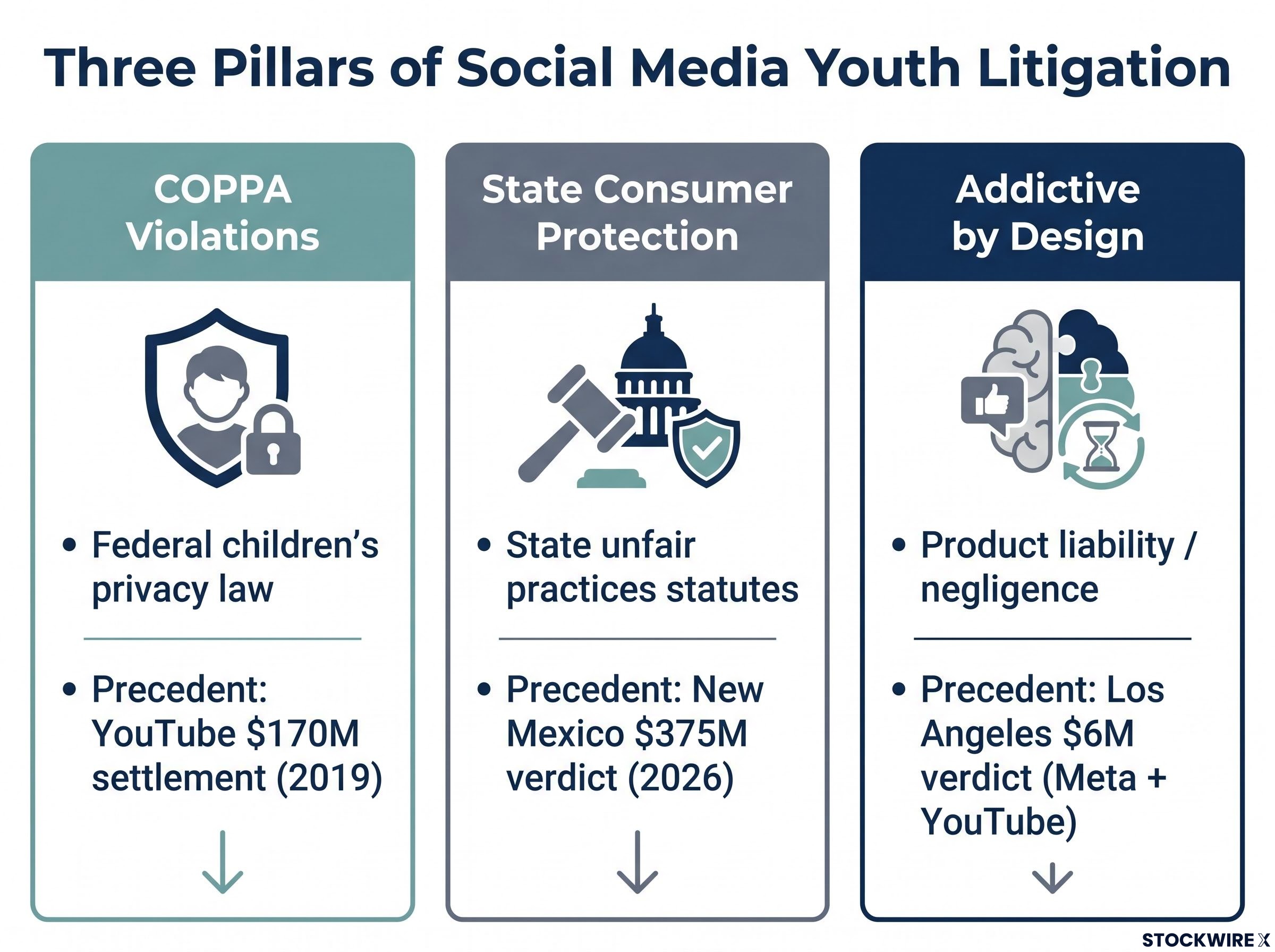

Three distinct legal theories underpin this litigation wave, and they are often layered in the same case rather than filed as alternatives. That layering is what makes the exposure calculation so difficult to simplify.

COPPA violations (the Children’s Online Privacy Protection Act, a federal law that prohibits collecting personal data from children under 13 without verifiable parental consent) target data collection practices. The prior benchmark here is Alphabet’s $170 million settlement with the FTC and New York Attorney General in 2019 for alleged improper data collection from children via YouTube.

The FTC’s COPPA enforcement action against YouTube established that collecting data from child users without verifiable parental consent constitutes a federal violation, setting the notice standard that plaintiffs now use to argue Alphabet’s subsequent conduct was willful rather than inadvertent.

State consumer protection claims focus on deception and omission. New Mexico’s case is the live example: the attorney general argued that Meta publicly portrayed its platforms as safe for young users while internal research showed the opposite.

“Addictive by design” product liability claims argue that specific engagement features were designed in ways that foreseeably create compulsive use and psychological harm in minors. In a Los Angeles trial, a jury found Meta and YouTube negligent on this theory and awarded $6 million total ($3 million compensatory plus $3 million punitive).

| Claim Type | Legal Basis | Key Allegation | Prior Precedent |

|---|---|---|---|

| COPPA violation | Federal children’s privacy law | Collecting data from under-13 users without parental consent | YouTube $170M settlement (2019) |

| State consumer protection | State unfair practices statutes | Deception about platform safety for minors | New Mexico $375M verdict (2026) |

| Addictive by design | Product liability / negligence | Features engineered to create compulsive use in minors | Los Angeles $6M verdict (Meta + YouTube) |

The layering of all three theories in the same case means that even a company that prevails on one claim can still face full damages on the other two. Partial legal victories do not translate cleanly into reduced financial exposure.

Across all defendants and all three theories, the specific engagement features under scrutiny include infinite scroll, recommendation algorithms, push notifications, streaks, and disappearing messages. Plaintiffs frame these as intentional design choices with foreseeable harm to minors, not incidental product characteristics. That framing is what connects the product liability theory to the consumer protection theory: the argument is that companies knew these features were harmful and marketed them anyway.

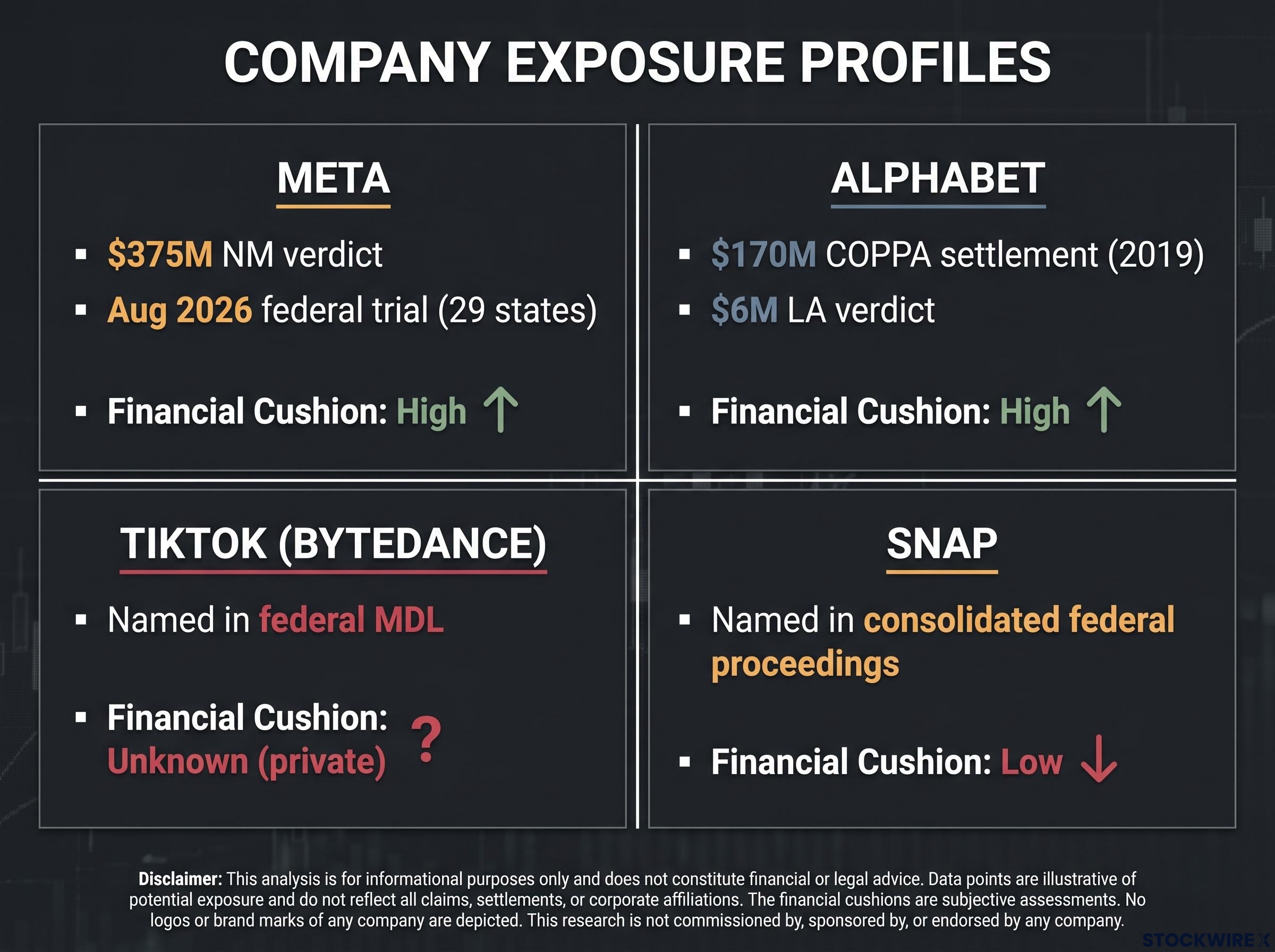

The four companies named in this litigation share the same legal theories but carry very different exposure profiles relative to their financial capacity to absorb them.

Meta is at the centre. It holds the $375 million New Mexico verdict, is named in the August 2026 federal trial covering COPPA claims from 29 states plus consumer protection claims from California, Colorado, Kentucky, and New Jersey, and faces the February proceeding. Its cash generation capacity is enormous, but the volume of cases and the precedent set by the intentional-misconduct finding create a compounding risk.

Alphabet carries YouTube’s prior $170 million COPPA settlement from 2019, which plaintiffs will use to argue ongoing violations were willful because the company had been put on notice. YouTube was a co-defendant in the $6 million Los Angeles verdict. Alphabet can absorb multi-hundred-million-dollar judgments more comfortably than most, but the larger threat is injunctive relief targeting its recommendation algorithm.

TikTok (ByteDance) is named in the federal multidistrict litigation (MDL, a process that consolidates similar federal lawsuits before one judge for pre-trial proceedings) in the Northern District of California. Its ForYou feed algorithm is central to claims. But ByteDance’s China-based corporate structure creates discovery, enforcement, and remedy complications that introduce a different category of uncertainty for investors.

Snap has not yet faced a headline verdict, but the same theories apply to Snapchat’s streaks, disappearing messages, and notification prompts. Here is the critical investor point:

Snap’s smaller market capitalisation and cash cushion mean that a verdict scaled to New Mexico’s $375 million level would represent a far higher share of enterprise value than the same verdict would for Meta or Alphabet. On a per-dollar-of-market-cap basis, Snap may carry the most financially dangerous exposure in this group.

| Company | Key Cases / Verdicts | Primary Legal Theory | Aggravating Factor | Financial Cushion |

|---|---|---|---|---|

| Meta | $375M NM verdict; Aug 2026 federal trial (29 states) | Consumer protection + COPPA + addictive design | Intentional misconduct finding on record | High |

| Alphabet | $170M COPPA settlement (2019); $6M LA verdict | COPPA + addictive design | Prior settlement demonstrates notice | High |

| TikTok (ByteDance) | Named in federal MDL | Addictive design + COPPA | China-based structure complicates discovery | Unknown (private) |

| Snap | Named in consolidated federal proceedings | Addictive design + consumer protection | Smallest financial cushion relative to exposure | Low |

Investors who have mentally assigned this as a “Meta problem” may be carrying unhedged exposure in Snap or Alphabet positions that face nearly identical legal theories with less financial capacity, or less legal distance from prior settlements, to absorb them.

Financial models handle one-time charges well. A $375 million penalty goes into a litigation reserve, hits one quarter’s earnings, and the market moves on. What they handle poorly is a court order that permanently constrains the product features driving engagement and advertising revenue.

That is what injunctive relief does, and it is the most consequential risk in this litigation cycle. The three categories, ranked by revenue impact severity:

Each of these strikes at the specific mechanisms that generate revenue: time-spent, ad load, and targeting precision. They do not appear as one-time charges. They appear as a structural cap on engagement metrics affecting every quarterly earnings report for years.

Litigation reserves in 10-K filings reflect expected cash settlement costs. They do not capture the ongoing revenue depression from court-mandated product constraints. Investors reading disclosure documents should look for qualitative risk factor language about “changes to product features” or “regulatory modifications to platform design” alongside quantitative reserve figures. The reserve number tells you what the company expects to write a cheque for. It does not tell you what the company expects to lose in ad revenue when a judge mandates algorithmic changes.

The litigation pipeline ahead is not a series of legal events. It is a series of information-release moments, each resolving a specific uncertainty currently priced ambiguously into these stocks.

| Proceeding | Timing | Jurisdiction | Companies Affected | Key Question Resolved |

|---|---|---|---|---|

| New Mexico phase-two orders | Ongoing (July 2026) | New Mexico state court | Meta | What structural product changes will courts mandate? |

| August 2026 federal trial | August 2026 | N.D. California (Judge Rogers) | Meta, Snap, Alphabet, TikTok | Will federal juries award at or above state-level benchmarks? |

| February trial | February 2027 | Federal court | Meta (14 additional states) | Do state consumer protection theories produce separate damage layers? |

Judicial signal: U.S. District Judge Yvonne Gonzalez Rogers denied Meta’s application to cancel the August trial, concluding that key factual questions about whether the platforms were addictive, whether Meta knowingly misrepresented that design, and whether the company had in practice oriented its platforms toward younger users all remained open for a jury to determine.

The August trial’s pre-trial rulings on the admissibility of internal Meta documents may be as consequential as the verdict itself. What the jury is allowed to see will anchor the public and media narrative for every subsequent case, including the February proceeding and remaining state-level suits. Treating earnings announcements as the primary price-moving event for these stocks misses this calendar entirely.

The comparison is not just media shorthand. It is being explicitly invoked in these cases because the legal structure mirrors tobacco litigation: corporate knowledge of harm, suppression of internal research, public statements contradicting known risks, and a pattern of regulatory avoidance preceding a wave of state-led enforcement.

The parallels that are legally relevant:

But the analogy has limits that matter for how you model the financial outcome:

The tobacco comparison is most useful not as a prediction of the dollar outcome but as a guide to the timeline. It suggests investors should plan for a decade-long liability cycle rather than expecting a single global settlement to clear the overhang quickly. Investors who watched prior tech regulatory cycles (GDPR, antitrust) resolve without lasting earnings impact may be applying the wrong mental model. The tobacco precedent suggests the more appropriate comparison is a multi-decade legal and regulatory constraint on a core business practice.

The litigation pipeline, 29 states in federal court, two federal trials, and ongoing New Mexico phase-two proceedings, extends well past a single news cycle. The framework for navigating it requires four specific adjustments:

Diversifying within “big tech” is not the same as diversifying away from this specific risk. Investors seeking genuine reduction should look toward enterprise-software or cloud-heavy names with limited consumer-social exposure, or platforms with predominantly adult or professional user demographics. The key filter is whether a company’s revenue depends on algorithmic engagement designed for younger cohorts.

Meta, Alphabet, and Snap remain powerful businesses with durable competitive positions. Nothing in this litigation changes the structural advantages of their ad platforms or the network effects that protect their user bases. The analysis loses meaning if it reads as a one-sided bear case.

But standard valuation models are missing three layers of risk simultaneously: one-time settlement cash across dozens of state and federal proceedings, ongoing product constraints from injunctive relief that depress engagement metrics quarter after quarter, and the chilling effect on future product initiatives targeting younger demographics. Each layer compounds the others.

The New Mexico verdict set a floor. The August 2026 federal trial will set the range. The injunctive relief phase will determine the ceiling on long-term earnings impact. Behind all of it sits a pipeline of 29 states in federal court, 14 more in February, and thousands of individual cases still active, with a tobacco-style timeline suggesting decades before resolution.

“The question is no longer whether the litigation is material. It is whether current valuations reflect a decade-long liability cycle.”

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding litigation outcomes, settlement sizes, and product changes are speculative and subject to change based on court rulings, jury decisions, and company actions.

Social media youth addiction lawsuits allege that platforms like Instagram, YouTube, and Snapchat were deliberately engineered to create compulsive use in minors. They typically layer three legal theories: COPPA violations for collecting data from children without parental consent, state consumer protection claims for deceptive safety assurances, and product liability claims arguing that specific features like infinite scroll and recommendation algorithms were designed to cause foreseeable psychological harm.

A New Mexico jury returned a $375 million verdict against Meta in March 2026, calculated at $5,000 per violation across thousands of individual violations. Critically, the jury found willful misconduct rather than mere negligence, concluding that Meta knowingly misled the public about the safety of Facebook, Instagram, and WhatsApp for children, a finding that raises damage floors in every subsequent case using the same theory.

Meta, Snap, Alphabet, and TikTok are all named in the litigation, but their exposure profiles differ significantly. Snap carries the most dangerous position on a market-cap-relative basis: a verdict scaled to New Mexico's $375 million level would consume a far larger share of Snap's enterprise value than it would for Meta or Alphabet, both of which have substantially greater financial cushions.

Litigation reserves reflect expected cash settlement costs but do not account for court-ordered product changes, such as algorithm modifications, notification restrictions, or stricter age verification. These injunctive remedies structurally depress engagement metrics and ad revenue across every subsequent quarter, creating an ongoing earnings impact that never appears as a one-time charge in financial disclosures.

The three most consequential upcoming events are the ongoing New Mexico phase-two proceedings (determining what structural product changes Meta must implement), the August 2026 federal trial in the Northern District of California covering COPPA and consumer protection claims from 29 states, and a February 2027 federal proceeding covering 14 additional states. Each resolves a specific uncertainty currently priced ambiguously into these stocks.