How ASX’s CHESS Overhaul Became a $250M Governance Failure

32 mins ago

One of the largest managers of Australian investor money operates on the premise that most professional stock-pickers cannot beat the market, yet it is not an index fund. Dimensional Fund Advisors (DFA) sits in a space most retail investors do not know exists, and it manages a significant portion of advised Australian wealth from that position.

The knowledge gap is striking. DFA is a dominant presence in Australian advisory networks, yet most retail investors have never heard the name. The framework it uses, factor investing, has quietly become one of the most widely adopted investment approaches in the world, but it rarely gets explained in plain language outside of academic circles.

Here is what you need to understand: what factor investing actually is, what DFA does with your money, and why it matters whether you are invested with them or evaluating whether you should be.

The assumption feels reasonable: paying a professional to pick stocks should deliver better results than buying the whole market. The evidence, however, tells a different story.

Shadforth, one of Australia’s largest wealth management firms, lived this problem first-hand. When it first engaged DFA in 1999, Shadforth’s model relied on blending active managers chosen on the strength of their recent track records. The fundamental difficulty was not poor manager quality; it was that predicting which managers would go on to outperform, rather than which had already done so, turned out to be far harder than the approach assumed.

DFA’s founding premise emerged directly from this kind of empirical observation rather than from a philosophical stance about how markets should work. The firm’s position is precise:

The pattern is not unique to the managers Shadforth encountered: active fund underperformance in Australia is structural and persistent, with SPIVA data showing 74% of Australian equity general fund managers failing to beat the S&P/ASX 200 even in 2025, a year described as unusually favourable for stock selection.

“DFA operates on the belief that prices incorporate information sufficiently well that the pursuit of traditional alpha through security selection is unlikely to be rewarded after costs.”

This is not an abstract claim about perfect market efficiency. It is a practical conclusion with a direct consequence for your money: if you cannot reliably identify which managers will outperform before they do it, paying for that selection process is likely to cost you over time. That structural difficulty is what led firms like Shadforth, under CEO Terry Dillon, to look for an entirely different approach.

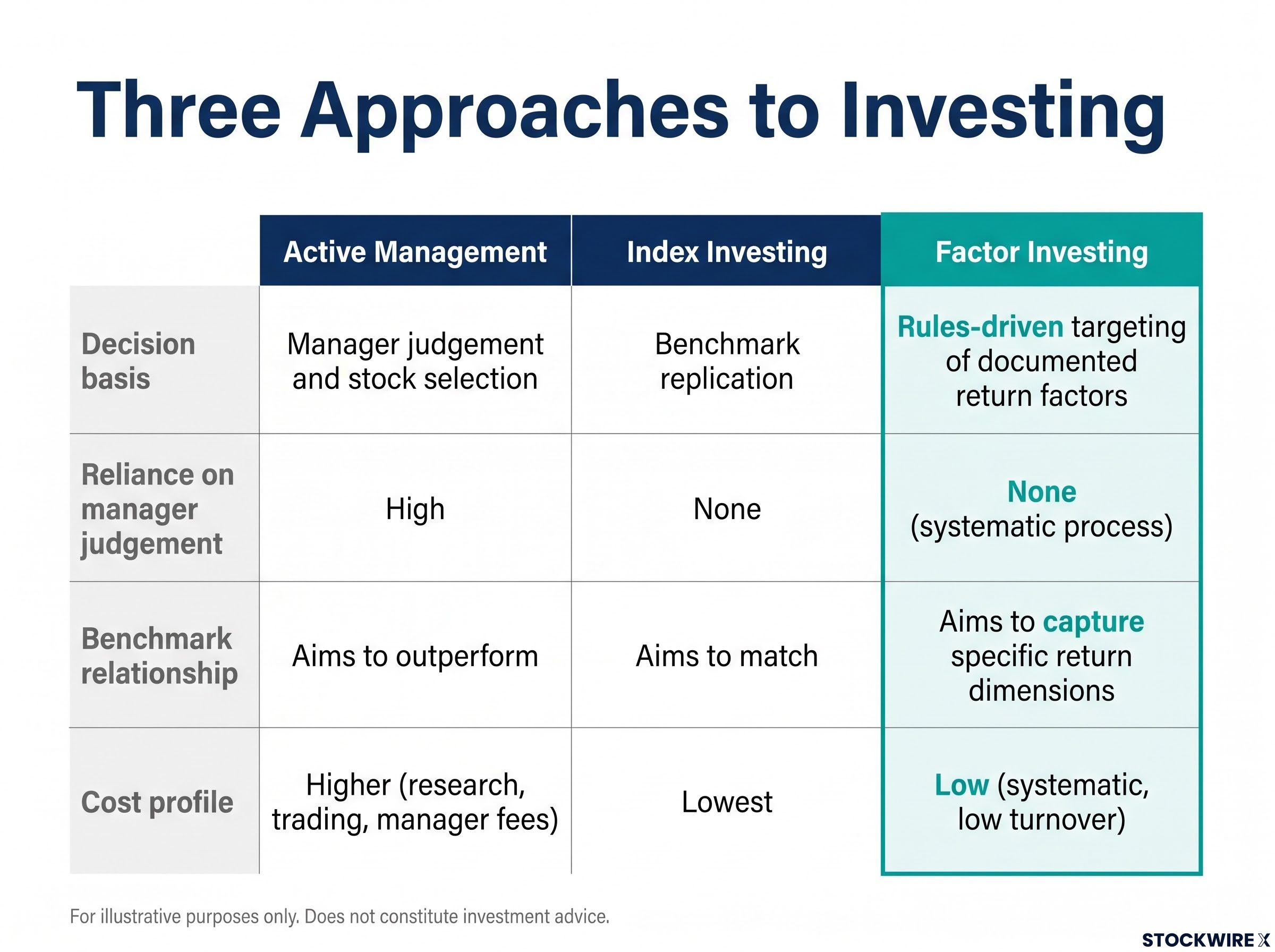

Most explanations of investing present you with a binary choice. On one side, you have active management: a professional stock-picker using judgement to select securities they believe the market has mispriced. On the other, you have index investing: a fund that simply replicates a benchmark like the ASX 200 or the S&P 500, making no attempt to beat it.

Factor investing occupies a third space you probably did not know existed.

Put simply, factor investing is a rules-driven approach that systematically seeks out measurable security characteristics which academic research has documented as being linked to stronger long-run returns. It does not rely on a fund manager’s judgement about which individual stocks are mispriced. Instead, it uses market data and a rules-driven process to tilt an entire portfolio toward certain measurable traits.

DFA itself draws the distinction clearly: traditional passive investing aims to “match the returns of an index,” while DFA’s approach aims to “use market data and a systematic approach to target higher expected returns.” The firm has been “translating academic research into practical investment solutions since 1981,” and its website points to five Nobel Laureates connected to the firm together with 29 staff members holding PhDs. That academic culture is not incidental to the product; it is the foundation.

| Active management | Index investing | Factor investing | |

|---|---|---|---|

| Decision basis | Manager judgement and stock selection | Benchmark replication | Rules-driven targeting of documented return factors |

| Reliance on manager judgement | High | None | None (systematic process) |

| Benchmark relationship | Aims to outperform | Aims to match | Aims to capture specific return dimensions |

| Cost profile | Higher (research, trading, manager fees) | Lowest | Low (systematic, low turnover) |

A factor premium is the additional return historically associated with exposure to a specific security characteristic. Think of it as compensation for bearing additional risk rather than a free lunch. Small companies, for instance, carry more risk than large ones, and the historical data shows they have delivered higher returns over long periods to compensate for that.

The critical caveat: these premiums are not guaranteed in any given year or even any given decade. That is precisely why a long investment horizon matters. If the premium were guaranteed, everyone would crowd into it and eliminate it.

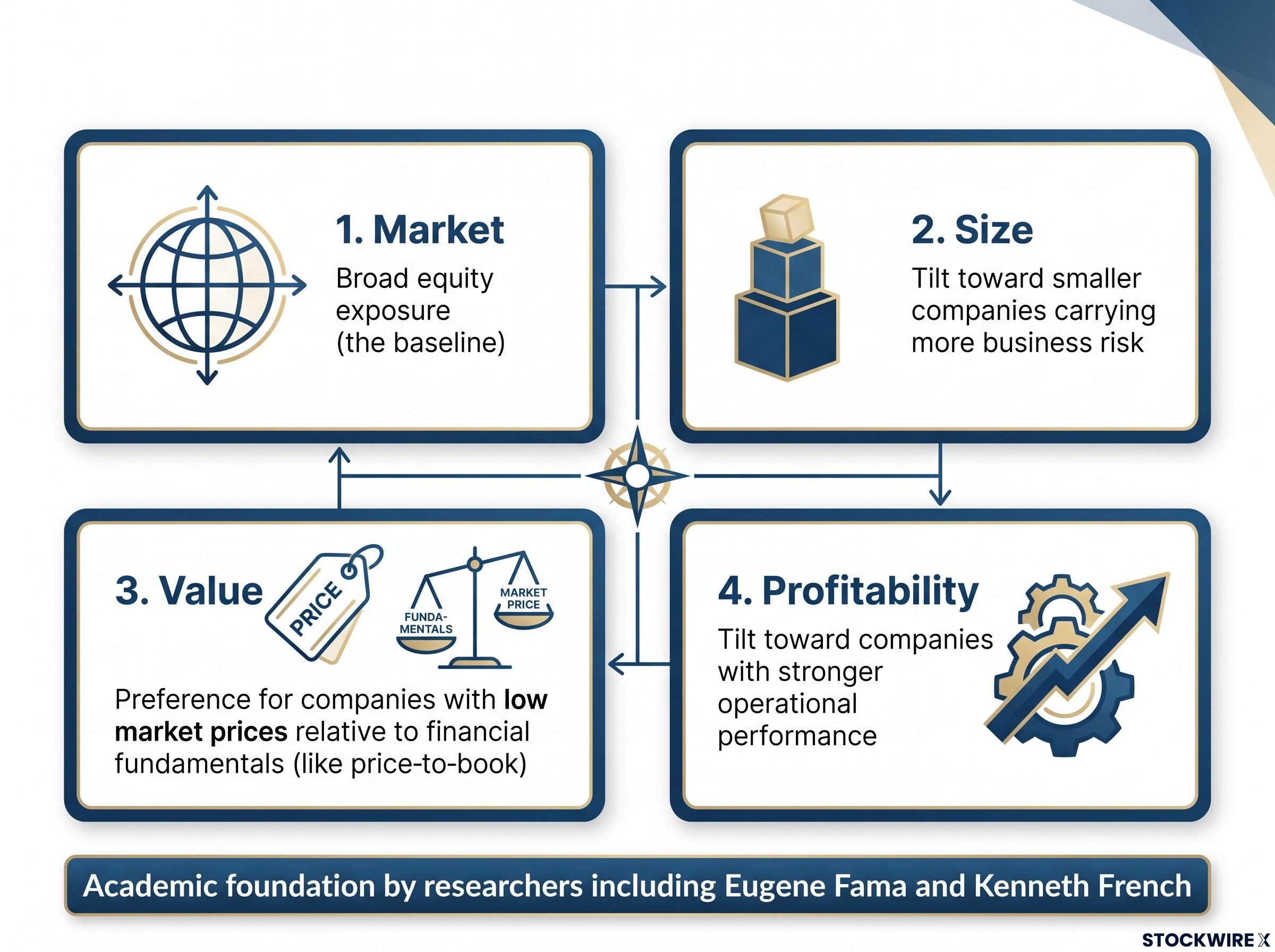

The academic foundation for DFA’s approach comes from Eugene Fama and Kenneth French, whose research documented that small-cap and value stocks have historically delivered higher returns than the broad market. Fama, a Nobel Laureate and Dimensional board member, co-developed the factor models that the firm’s entire strategy is built on. Subsequent research extended the framework to include profitability and investment characteristics.

DFA’s equity strategies are organised around four primary factors. Here is what each one means for you in plain language:

The small-cap premium is real but concentrated: AQR research shows the size premium resides primarily in higher-quality small-cap stocks, meaning broad passive small-cap exposure systematically dilutes it by including unprofitable and speculative names that drag on returns.

These factors were not discovered by DFA’s marketing department. They were documented by independent academic researchers, Fama and French among them, with no product to sell. That is precisely why DFA’s claim to be evidence-based carries weight.

DFA describes its mission as “translating academic research into practical investment solutions.”

DFA’s funds invest in thousands of companies and tilt toward these factors rather than concentrating in a small number of selected stocks. Your portfolio does not bet on ten “best ideas”; it captures the systematic return behaviour that decades of cross-market evidence has identified.

Understanding the factors is one thing. Understanding how DFA actually builds a portfolio around them is where the approach becomes concrete.

There is no star manager. No one at DFA is making concentrated bets based on personal conviction. Portfolio decisions are driven by a structured, repeatable process applied to market data and fundamental information. DFA uses “information in prices and fundamental data to systematically identify differences in expected returns among securities.” The firm sells process, not personality.

That systematic approach is applied at serious scale. As of 31 March 2026, DFA held $257 billion in ETF assets in the US market alone, making it the largest active ETF manager in that market across 42 active ETFs. Its funds hold thousands of stocks across developed and emerging markets globally, with systematic tilts toward target factors applied across the entire portfolio.

The absence of a named fund manager is not a gap in DFA’s model. It is the structural feature that makes the approach consistent, scalable, and robust to individual human error. For you, this means the strategy does not change when a portfolio manager retires, has a bad year, or leaves for a competitor.

The implementation operates through a set of specific disciplines:

Factor premiums are real, but they are not enormous. They are measured in percentage points, not multiples. That means transaction costs, taxes, and excessive portfolio turnover can easily erode a premium that the strategy is theoretically designed to capture.

Trading efficiency is the difference between a factor strategy working as designed and underperforming its own premise. This is why DFA’s emphasis on cost-effective execution is not a marketing point; it is structurally necessary for the approach to deliver.

DFA’s presence in the Australian market is well established. The firm holds an Australian Financial Services licence and operates offices in Sydney and Melbourne, with long-standing relationships across major Australian advisory networks.

The Shadforth relationship illustrates the pattern. Shadforth’s partnership with DFA commenced in 1999, making it one of the earliest and most significant Australian adopters. When advisers commit to DFA’s philosophy, they typically move heavily into the firm’s products across their client base, a pattern that speaks to deep conviction in the approach rather than routine product placement.

Industry observers have noted that DFA’s following among Australian financial advisers is unusually strong. Bhanu Singh, CEO of Dimensional Australia, serves as the firm’s primary spokesperson in the Australian market, while independent analysts like Shani Jayamanne, Director, Investment Specialist, Wealth at Morningstar Australia, have provided external perspective on the firm’s Australian positioning.

What matters most for you is this: DFA’s dominance in Australian advisory networks means this framework is already shaping the investment outcomes of a significant portion of advised Australians. If you use a financial adviser, there is a meaningful chance you are invested in DFA funds right now, whether or not you recognise the firm’s name or understand the philosophy behind your portfolio’s construction.

The academic evidence behind factor premiums is substantial. Size and value premiums have been documented across multiple developed and emerging markets over long periods. The Fama-French framework is not a fringe theory; it is foundational to mainstream academic finance.

That said, factor premiums are not guaranteed in any single year, any single decade, or any particular market cycle. Periods where a factor-tilted portfolio underperforms a simple index are entirely consistent with the long-run evidence. If your portfolio is tilted toward value and small-cap stocks, there will be stretches where a plain ASX 200 index fund looks like it was the better choice. That is expected, not a sign that the strategy has failed.

The deeper question is whether these premiums will persist in the future. The academic and practitioner consensus holds that the premiums reflect persistent risk exposures, meaning they represent compensation for taking on more risk, not anomalies that disappear once investors become aware of them. That debate has not been definitively settled, but the weight of evidence currently supports persistence.

For readers wanting to pressure-test the evidence before committing to a factor-tilted portfolio, our full explainer on factor investing premiums and their real limits covers how backtested returns overstate live investor outcomes and why two ETFs with the same factor label can behave very differently in practice.

A factor strategy works as intended when several conditions align:

Committing to a factor strategy requires patience and a longer time horizon than most investors are emotionally prepared for. That is why the adviser relationship DFA operates through matters as much as the strategy itself.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The core distinction is straightforward. DFA’s model is not about picking better stocks. It is about systematically capturing return premiums that academic research associates with specific security characteristics, implemented at global scale and at low cost. The firm was founded in 1981, grounded in Nobel Prize-linked academic research, counts five Nobel Laureates among those affiliated with the firm and employs 29 staff holding PhDs, and manages $257 billion in US ETF assets as of 31 March 2026.

If your adviser uses DFA, or if you are evaluating one who does, here are four questions worth asking:

Factor investing has moved from academic theory to the dominant investment framework for a large segment of the Australian advice industry. Understanding what it is, how it works, and what it demands of you as an investor is now a baseline for financial literacy among advised Australians. Whether you are already in a factor-tilted portfolio or deciding if you should be, the questions above are where the conversation with your adviser starts.

Investors ready to move beyond the conceptual framework and apply factor tilts directly will find our comprehensive walkthrough of building a factor portfolio useful, covering the dual-factor ETF overlap method, z-score normalisation of factor metrics, and the drift-based rebalancing triggers that improve after-cost outcomes.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Factor investing is a rules-driven approach that systematically tilts a portfolio toward measurable security characteristics, such as small size, low valuation, and high profitability, that academic research has documented as being linked to stronger long-run returns. It sits between traditional active management and plain index investing: it does not rely on a fund manager's stock-picking judgement, but it does aim to do better than simply matching a benchmark.

DFA's equity strategies target four primary factors: market exposure (owning equities rather than cash or bonds), size (a tilt toward smaller companies that carry more business risk and have historically delivered higher returns), value (a preference for companies whose prices are low relative to their financial fundamentals), and profitability (a tilt toward companies with stronger operational performance).

An index fund aims to match the returns of a benchmark like the ASX 200 or S&P 500, while DFA uses market data and a systematic, rules-driven process to tilt portfolios toward factors that academic research associates with higher expected returns. DFA itself draws this distinction explicitly: its goal is to target higher expected returns, not merely to replicate a benchmark.

SPIVA data shows that 74% of Australian equity general fund managers failed to beat the S&P/ASX 200 even in 2025, a year described as unusually favourable for stock selection. DFA's position is that prices incorporate information well enough that identifying which managers will outperform before they do it is far harder than identifying which have already done so, making the cost of active management difficult to justify over time.

Factor premiums are not guaranteed in any single year, decade, or market cycle, and periods where a factor-tilted portfolio underperforms a plain index are entirely consistent with the long-run evidence. The academic and practitioner consensus holds that these premiums reflect persistent risk exposures, meaning compensation for bearing more risk rather than anomalies that disappear once investors become aware of them, but the debate has not been definitively settled.