What JEPI Actually Is and Whether It Fits Your Portfolio

2 mins ago

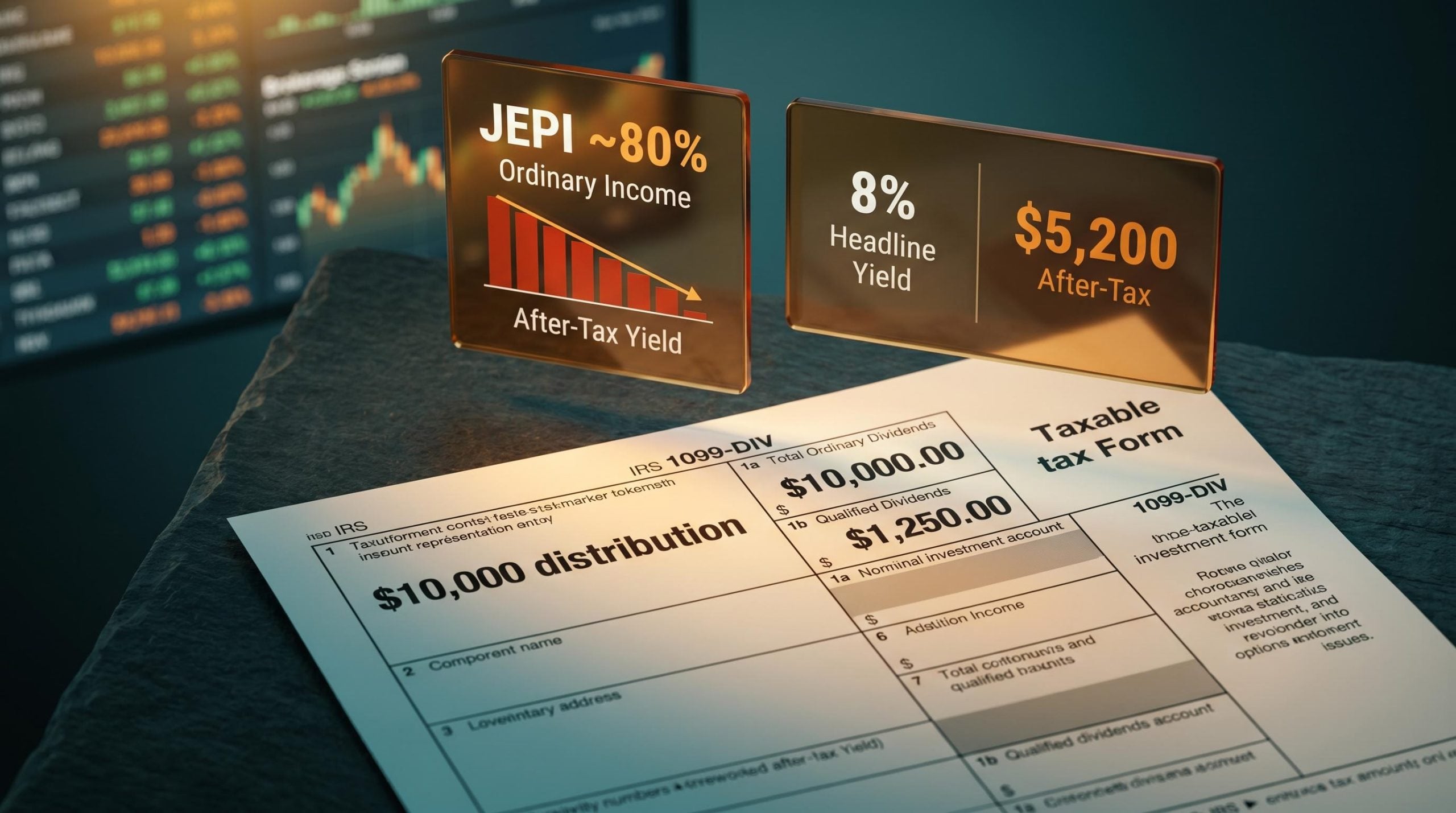

An investor in the 32% federal bracket earning $10,000 a year from JEPI distributions might assume they are keeping roughly $6,800 after tax. They are probably not. Once ordinary income rates, the 3.8% Net Investment Income Tax (NIIT), and state taxes layer on top of each other, the after-tax number can fall well below what the headline yield implied when they bought the fund.

That gap is not a quirk or a risk factor buried in the fine print. It is a structural feature of how JEPI generates its income, and it shows up on every 1099 the fund produces. Understanding it before tax season arrives is worth considerably more than understanding it after.

Here is exactly what your 1099 will show, why it shows that, and what it means for where you should be holding this fund. By the time you finish, you will have a clear framework for calculating your own after-tax yield and a short checklist of steps to take before your next distribution cycle begins.

JEPI (JPMorgan Equity Premium Income ETF) generates its high monthly income through a mechanism that looks different from what most dividend investors are used to. Instead of writing conventional covered calls on a listed exchange, the fund uses equity-linked notes (ELNs), which are structured financial instruments that embed short call positions on parts of the equity portfolio. ELNs are contracts between JEPI and a counterparty (typically a bank) that bundle stock exposure with an options component into a single instrument.

The result is an average distribution yield of approximately 8%, which sits well ahead of what broader market indices return to income investors: the S&P 500 yields just over 1%, while SPHD comes in at roughly 3.5%. The fund charges an expense ratio of 0.35% and has been operational for approximately six years.

The ELN structure is not a technicality to skim past. It is the precise mechanism that determines how the IRS classifies nearly every dollar JEPI sends to your brokerage account. The call premium embedded in ELNs is treated as interest-style ordinary income, not as a qualified dividend or a long-term capital gain. That single classification decision drives the entire tax profile of the fund.

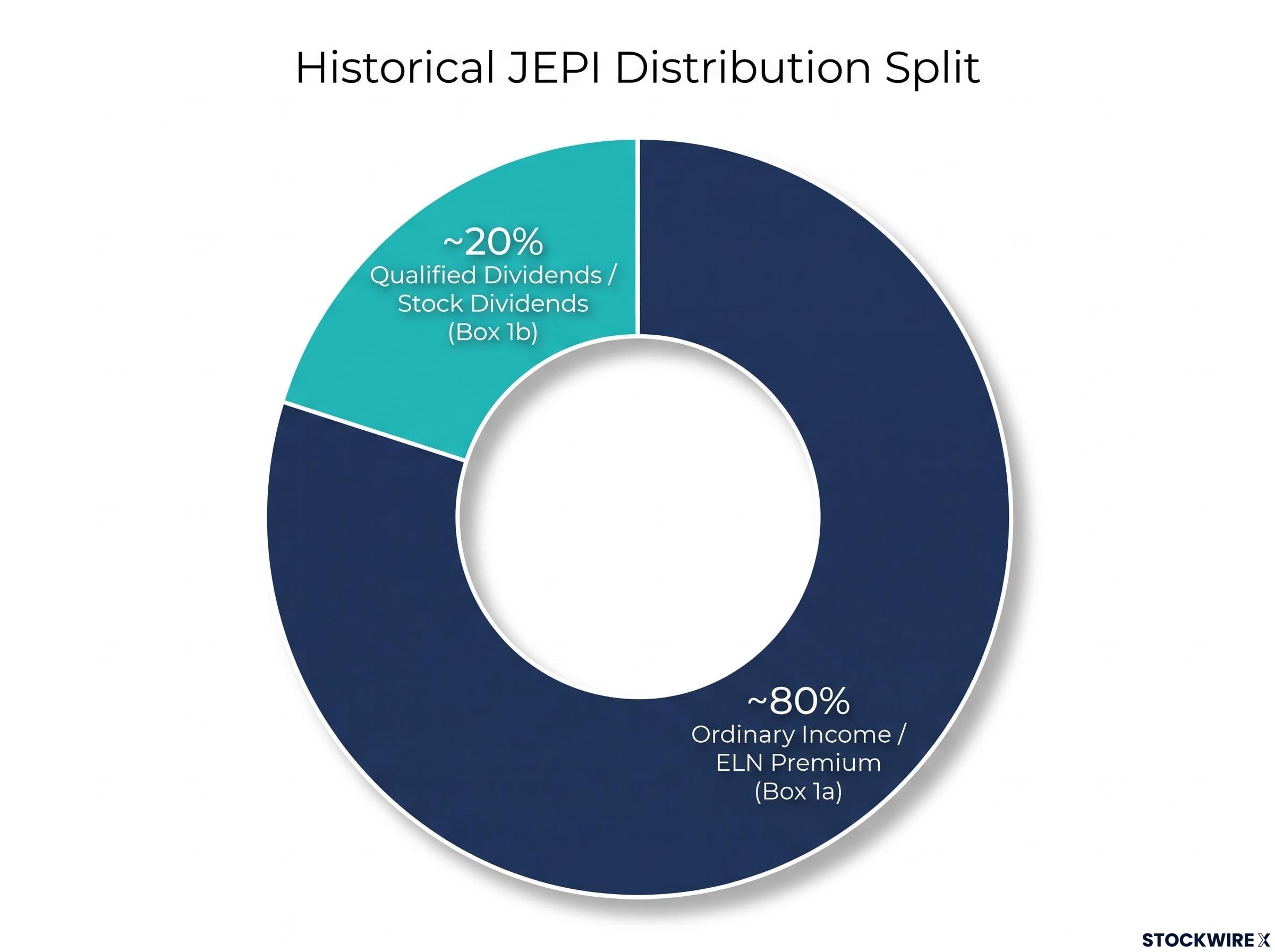

The ELN premium that powers JEPI’s yield is classified as ordinary income precisely because it is not a dividend at all; dividend mechanics govern only the portion of JEPI’s distributions that flows from the underlying stocks the fund holds directly, which historically represents just 20% of total payouts.

Inside JEPI, two distinct income streams coexist:

Understanding this split is the prerequisite for everything else in this article. Once you see that the ELN premium, the engine behind JEPI’s yield advantage, routes through the ordinary income door on your tax return, the rest of the tax story follows logically.

When the 1099-DIV for your JEPI position arrives, it will not tell you “here is your dividend income.” It will break your distributions into boxes, and the relative sizes of those boxes tell you exactly how much of your yield the IRS treats favourably and how much it does not.

Three boxes matter:

| 1099-DIV Box | What it captures | Typical JEPI characterisation |

|---|---|---|

| Box 1a | Total ordinary dividends (includes both non-qualified and qualified) | Large: the bulk of your JEPI distributions land here |

| Box 1b | Qualified dividends (eligible for preferential long-term capital gains rates) | Small: approximately 20% of total distributions historically |

| Box 3 | Return of capital (not currently taxable; reduces your cost basis) | Typically empty for JEPI |

The historical pattern, confirmed by multi-year tax documentation and consistent with broader practitioner estimates, is that approximately 80% of JEPI’s annual distributions have been classified as ordinary (non-qualified) income. The remaining 20% or so qualifies for the lower long-term capital gains rates. Multiple practitioners who track the fund place the ordinary income share in the 80-90% range across recent years, with the qualified slice at 10-20%.

When Box 1b is much smaller than Box 1a on your 1099, that gap translates directly into a higher tax bill than you would receive from a comparable fund paying mostly qualified dividends. Understanding that gap before the form arrives is what allows you to plan around it.

Planning note: The 80/20 ordinary-to-qualified split is a historical baseline, not a guarantee. The exact ratio varies year-to-year based on portfolio composition and the dividend behaviour of JEPI’s underlying holdings. Always verify the actual annual characterisation once official fund tax data is published before filing.

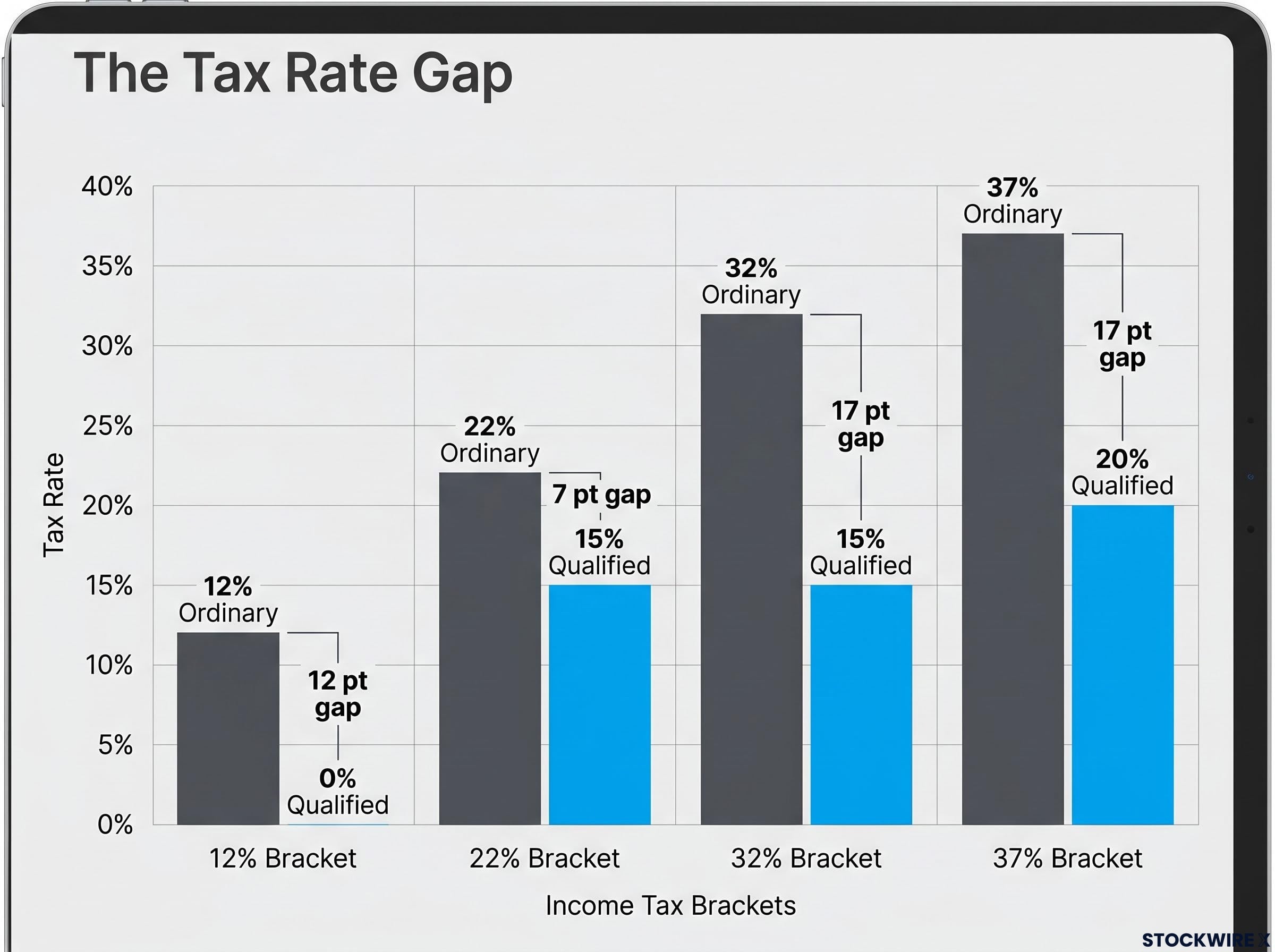

The difference between ordinary income and qualified dividend tax rates is not a minor technical footnote. It is the gap that determines whether JEPI’s 8% headline yield translates into a genuinely competitive after-tax income stream or one that converges toward what a much lower-yielding, more tax-efficient fund would have delivered.

Ordinary income is taxed at your marginal federal rate, which ranges from 10% to 37%. Qualified dividends are taxed at long-term capital gains rates: 0%, 15%, or 20%, depending on your taxable income. The rate gap between those two scales is where JEPI’s tax drag lives.

| Federal tax bracket | Ordinary income rate | Qualified dividend rate | Tax rate gap |

|---|---|---|---|

| 12% | 12% | 0% | 12 percentage points |

| 22% | 22% | 15% | 7 percentage points |

| 32% | 32% | 15% | 17 percentage points |

| 37% | 37% | 20% | 17 percentage points |

For investors above the applicable income thresholds, the 3.8% NIIT (Net Investment Income Tax, a surtax that applies to investment income for higher earners) stacks on top of both the ordinary and qualified rates, widening the effective gap further. State income taxes are additive on top of that.

IRS Topic 559 sets the specific income thresholds above which the NIIT applies: $250,000 for married filing jointly, $200,000 for single filers, and $125,000 for married filing separately, thresholds that many JEPI investors in the 32% and 37% brackets will exceed.

To model your own after-tax yield, work through this sequence:

A high-bracket investor running this calculation may find their effective after-tax yield from JEPI in a taxable account falls into a range that looks far closer to what a lower-headline-yield, qualified-dividend-heavy fund would have delivered. That convergence changes the comparison set entirely when you are choosing income investments for a taxable account.

Not all covered-call ETFs produce the same 1099. The fund structure, the type of options used, and the underlying stock mix all determine what kind of income reaches your brokerage account and how the IRS classifies it.

JEPQ (JPMorgan Nasdaq Equity Premium Income ETF) uses the same ELN-based structure as JEPI, but applied to Nasdaq-100 stocks. Because the Nasdaq-100 is dominated by growth and technology names that pay little or no dividends, the qualified dividend slice is even thinner. The estimated qualified income percentage for JEPQ is approximately 10% of total distributions, compared with JEPI’s approximately 20%. The underlying stock mix is the driver: fewer dividend-paying holdings means less income that qualifies for preferential rates.

In practical terms, JEPQ is even more tax-heavy in a taxable account than JEPI for most investors.

GPIQ (Goldman Sachs’ Nasdaq-focused premium income ETF) takes a structurally different approach. Instead of using ELNs, GPIQ writes exchange-traded listed covered call options directly. That listed-options structure can generate return-of-capital (ROC) distributions when the total cash paid out exceeds the fund’s net realised gains for the year.

ROC works differently from ordinary income. ROC distributions are not taxed as income when you receive them. Instead, they reduce your cost basis in the fund. That means you defer the tax liability until you sell your shares, at which point a lower cost basis may result in a larger taxable capital gain.

The distinction worth remembering: ROC is tax deferral, not tax elimination. Your current-year tax bill goes down, but your eventual capital gains tax at exit may go up. The long-term economics depend on when and at what price you sell.

| Fund | Options structure | Primary distribution character | ROC potential | Approx. ordinary income share |

|---|---|---|---|---|

| JEPI | ELNs (embedded options) | Ordinary income | Historically none | ~80% |

| JEPQ | ELNs (embedded options) | Ordinary income | Historically none | ~90% |

| GPIQ | Listed covered calls | ROC potential | Structurally possible | Varies; potentially much lower |

Choosing between these three funds in a taxable account is not just a yield decision. It is a decision about what kind of tax liability you are willing to accept and when you are willing to pay it.

The ELN versus FLEX options distinction extends across the broader covered call ETF category, where funds like SPYI and QQQI use FLEX options structures that can generate return-of-capital distributions rather than ordinary income, creating meaningfully different after-tax profiles even when headline yields look similar.

The ordinary-versus-qualified income distinction that drives JEPI’s tax profile largely disappears inside tax-advantaged wrappers. That makes account placement the single most powerful tool you have for managing the tax drag without selling the position.

A deliberate asset location strategy, placing high-income ordinary-income assets inside tax-advantaged wrappers while keeping tax-efficient holdings in taxable accounts, is the same structural logic that makes account placement the primary lever for JEPI holders rather than a secondary optimisation.

Your tax-advantaged options each handle JEPI’s ordinary income character differently:

In all four account types, the headline yield is much closer to the yield you actually keep, because the tax character of the distributions no longer matters inside the wrapper.

Holding JEPI in a taxable brokerage account is not inherently a mistake, but it requires explicit modelling rather than assumption.

If you are in the 10-12% federal bracket, the tax penalty is relatively modest. The ordinary income rate you pay on 80% of distributions is not dramatically higher than the 0% qualified dividend rate you would otherwise receive. For investors in these brackets who need current income, JEPI in a taxable account can still be a legitimate choice.

For investors in the 22-37% brackets, particularly in high-tax states, the calculus shifts materially. A substantial portion of each JEPI distribution dollar goes to federal income tax, NIIT, and state taxes. The threshold condition for holding JEPI in a taxable account at these brackets is not comfort with the fund’s strategy. It is having done explicit after-tax yield modelling and accepted the result, not assumed it.

One common misconception worth addressing: DRIP (dividend reinvestment) does not change or defer the tax obligation. When you reinvest distributions into additional JEPI shares, those distributions are taxed in the year they are paid, exactly as if you had received cash. Reinvestment is a capital allocation choice, not a tax planning tool.

Everything in this article points toward a small number of concrete steps you can take before the end of the tax year. Here they are, in order:

When your 1099-DIV arrives, verify it against expectations. Box 1a should be large (the bulk of your JEPI distributions). Box 1b should be small (approximately 20% of total, possibly less). Box 3 should typically be empty for JEPI. If any box looks materially different from the historical pattern, check the fund’s official annual tax characterisation before assuming an error.

Your holding period for JEPI shares affects your tax rate on any gain or loss when you sell, but it does not change how the distributions themselves are classified. Distribution character is driven by the nature of the income (ELN premium versus stock dividends), not by how long you have held the fund.

Timing reminder: Mid-year estimates using the 80-90% ordinary income historical baseline are reasonable planning tools, but always verify the final annual distribution character from the fund’s official tax reporting before filing your return.

The gap between what investors assume their JEPI income costs them in taxes and what it actually costs is almost always correctable with a single planning action. You have everything you need to take that action now.

JEPI’s headline yield and JEPI’s after-tax yield are two different numbers. The gap between them is driven by a structural feature, ELN-sourced ordinary income, that is baked into how the fund generates its returns. That feature is not going to change.

JEPQ faces the same structural issue with an even thinner qualified dividend slice. GPIQ creates a different current-year tax profile through return of capital, but the long-term tax obligation does not disappear; it defers to the point of sale.

The most actionable lever you have is account placement. The same fund, in the right account, produces a materially better after-tax outcome. For a high-bracket investor, moving JEPI from a taxable brokerage account into a Roth IRA is not a minor optimisation. It is the difference between keeping the yield the fund advertises and watching a meaningful share of it leave through the tax door every year.

After-tax yield is the number that funds your retirement, your income needs, and your compounding. Start there, not with the headline.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Tax situations vary; consult a qualified tax professional for advice specific to your circumstances.

JEPI generates the bulk of its distributions through equity-linked notes (ELNs), which embed call option premiums that the IRS classifies as ordinary income rather than qualified dividends. Historically, approximately 80% of JEPI's annual distributions have fallen into this ordinary income category, taxed at your full marginal federal rate up to 37%.

Approximately 20% of JEPI's total annual distributions have historically qualified for preferential long-term capital gains tax rates, with the remaining 80% treated as ordinary income. For JEPQ, the qualified slice is even thinner at roughly 10%, because the Nasdaq-100 holdings pay fewer dividends.

Yes, the NIIT applies to JEPI's ordinary income distributions for investors whose modified adjusted gross income exceeds $250,000 (married filing jointly), $200,000 (single), or $125,000 (married filing separately), stacking on top of the regular marginal rate and any applicable state income taxes.

Holding JEPI inside a Roth IRA, traditional IRA, 401(k), or HSA eliminates the ordinary-versus-qualified income distinction entirely, meaning the fund's high monthly income compounds without triggering annual tax on distributions. For high-bracket investors in taxable accounts, account placement is the single most effective lever for improving after-tax yield.

No. Reinvesting JEPI distributions through a dividend reinvestment plan (DRIP) does not defer or reduce the tax liability. The distributions are taxed in the year they are paid, exactly as if you had received cash, regardless of whether the proceeds are used to buy additional shares.