Goldman Sees Contrarian Buy Signal in KOSPI Foreign Selloff

8 mins ago

Bank of America lifted its year-end Stoxx 600 price target to 630 from 590 on 3 July 2026, a roughly 6.8% uplift that prices in a reformed Germany, easing energy costs, and a more cooperative monetary backdrop. The number looks constructive. The question is how much of it rests on policy promises that will not produce verifiable economic data until 2027 at the earliest.

The catalyst is Germany’s “Programme for Revival and Employment,” announced on 2 July 2026: the largest structural reform package from Europe’s anchor economy in years. BofA’s revision is not routine housekeeping. It reflects a changed view on the Eurozone’s medium-term earnings trajectory, with German reform optimism sitting at the centre of that recalibration.

Here is how to evaluate whether the upgrade changes anything about your European equity exposure, which sectors carry the clearest reform linkage, and what signals to track before treating 630 as a floor rather than a scenario.

The revision is straightforward on its face. BofA Global Research moved its year-end 2026 Stoxx 600 target from 590 to 630, reported on 3 July 2026, implying an uplift of approximately 6.8%.

| Prior Target | Revised Target | Implied Uplift | Target Horizon | Revision Date |

|---|---|---|---|---|

| 590 | 630 | ~6.8% | Year-end 2026 | 3 July 2026 |

Germany’s reform package is the headline driver, but it is not the only one. The euro-area energy shock has eased, reducing margin pressure on energy-intensive industries and supporting real incomes across the bloc. Improved visibility on monetary policy and resilient global growth expectations also feed into BofA’s higher fair-value estimate.

European market consolidation below February 2026 highs, while the S&P 500 climbed roughly 9% over the same period, established the underperformance baseline from which BofA’s revised target represents a meaningful directional shift in institutional conviction.

What matters more than the number itself is the framing around it. BofA’s analysts were explicit: the revision prices the direction of policy rather than verified near-term GDP upside. Hard-data confirmation is not expected until 2027 and beyond.

BofA characterised current European equity valuations as “priced for perfection,” meaning the market already assumes reforms are implemented broadly as promised and macro shocks remain contained.

A 6.8% target uplift from a major institutional desk tells you the bar for disappointment has risen. If reforms stall or macro conditions deteriorate, the downside from current pricing is not trivially small. The number is a directional signal, not a precision forecast, and knowing the difference is where informed positioning starts.

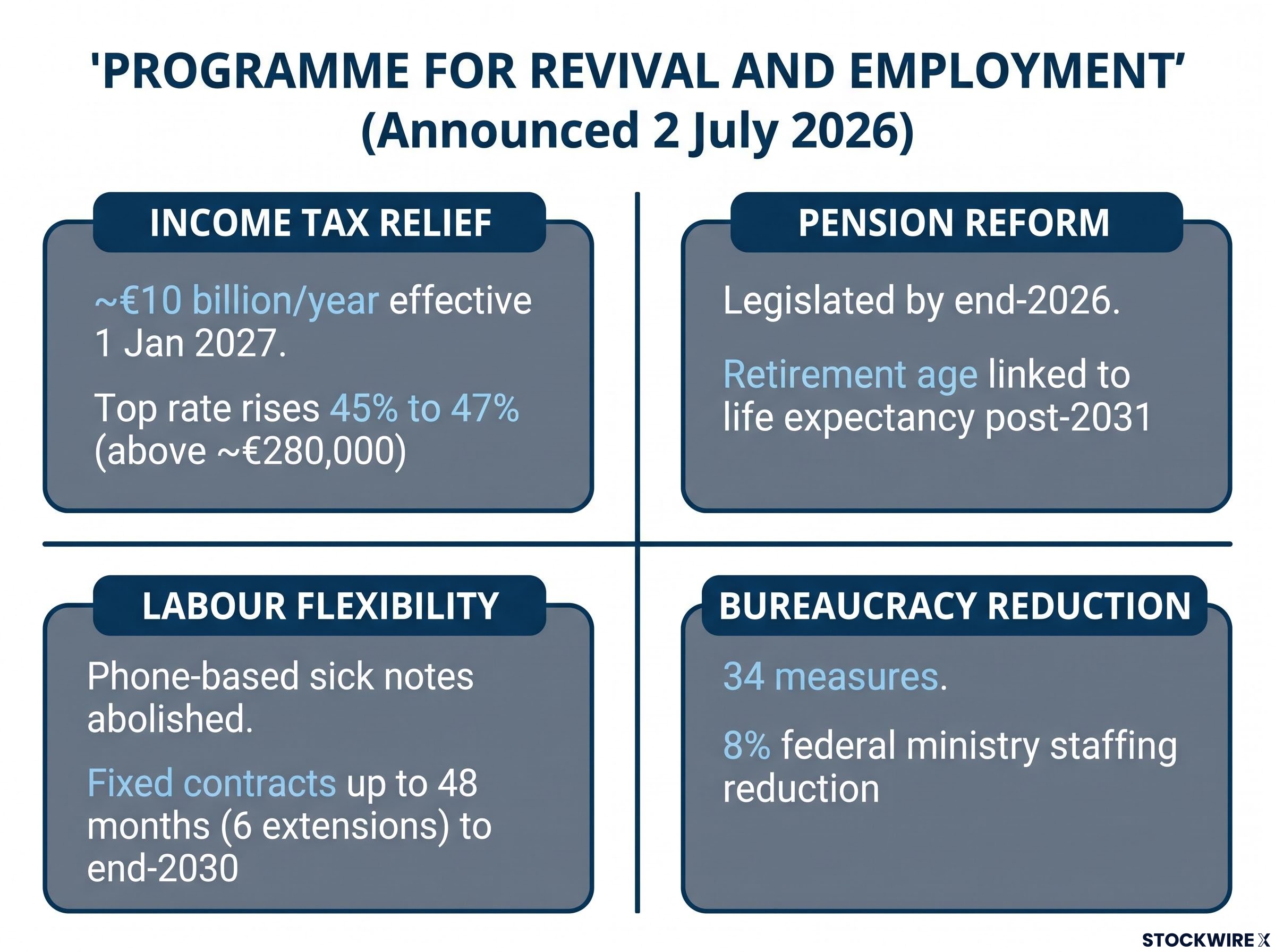

The “Programme for Revival and Employment,” announced on 2 July 2026, is built on four substantive pillars. Each operates through a different economic lever, and the market-relevant implication of each is distinct.

The tax relief quantum is the most immediately quantifiable lever. Approximately €10 billion flowing annually into lower- and middle-income households from 2027 supports retail, hospitality, and consumer services spending. The financing mechanism (a 2 percentage point top-rate increase) means the net fiscal impulse is redistributive rather than deficit-financed, which affects how markets price sustainability.

The retirement-age linkage to life expectancy does not take effect until after 2031, making it a multi-decade structural measure. Its impact on labour-force size, wage dynamics, and pension sustainability will not appear in hard data within the current BofA target horizon. Equity markets may begin pricing the credibility of the commitment earlier, but the verification window stretches years beyond year-end 2026.

Housing construction support and benefit-fraud countermeasures sit as second-order factors: relevant to social stability and labour mobility, not immediate Stoxx 600 catalysts. They shape Germany’s long-run growth profile without moving quarterly earnings in the near term.

The package’s design, weighted toward consumption support and labour supply rather than direct corporate subsidies, means the primary Stoxx 600 beneficiary is the domestically oriented German consumer and services economy, not the export-heavy industrial names investors might instinctively reach for.

The reform package does not lift European equities uniformly. Each policy lever connects to a specific part of the index, and the strength of that connection varies considerably.

| Sector | Reform Lever | Expected Benefit | Key Caveat |

|---|---|---|---|

| Consumer & Services | €10B annual tax relief | Stronger domestic demand from 2027 | Consumption effect is a 2027 story, not 2026 |

| Industrials & Autos | Bureaucracy reduction, labour flexibility | Lower compliance costs, faster hiring | Chinese EV competition remains a structural headwind for autos |

| Financials | Improved growth visibility, pension sustainability | Stronger credit demand, reduced uncertainty | Benefits are indirect; dependent on broader macro follow-through |

| Non-German intra-EU names | German demand amplification | Intra-EU exporters and supply-chain partners gain | FX translation matters for non-euro investors |

Consumer and services names with German revenue exposure are the most direct beneficiaries. The €10 billion annual tax relief enters household budgets from 2027, meaning the consumption tailwind has a defined start date and a quantifiable scale. For industrials, the 34 bureaucracy measures and expanded fixed-term contracting reduce operating friction, but the automotive segment faces persistent competitive pressure from Chinese EV makers that the reform package does not address.

Chinese EV competition in the automotive sector has moved well beyond pricing pressure into structural market-share erosion, a dynamic the Volkswagen restructuring plan, targeting up to 100,000 job cuts and four German plant closures, illustrates at operational scale.

Financials benefit from improved growth visibility and more sustainable pension frameworks. Banks and insurers with significant German exposure are positioned where reduced structural uncertainty supports credit growth and product demand. Non-German Stoxx 600 constituents with intra-EU supply-chain links to Germany benefit indirectly as German demand effects amplify across the broader European economy; for non-euro investors, an improved German growth profile also supports the euro’s structural backdrop, relevant through FX translation.

The clearest fundamental rationale sits in German-linked consumer, industrial (ex-auto), and financial names. Investors chasing a generic “European equity” allocation without sector specificity risk holding the parts of the index where the reform tailwind is weakest.

The gap between legislative action and verifiable economic impact is where the BofA upgrade is most vulnerable to over-interpretation. Understanding the phasing prevents two common errors: treating the target as already validated by a market move, and dismissing the thesis entirely because hard data has not arrived yet.

BofA framed the upgrade explicitly as pricing “policy direction rather than near-term GDP upside,” acknowledging that verification is a 2027-and-beyond proposition.

This timeline means that 2026 Stoxx 600 performance linked to this package is driven by sentiment and valuation re-rating, not underlying earnings growth. If the index runs toward 630 before year-end on sentiment alone, investors face a valuation-versus-verification gap: whether reform delivery credibility is strong enough to justify holding through the lag.

Naming these risks is not a caveat afterthought. It is what makes the bull case usable, because knowing the guardrails is what separates a positioned investor from an exposed one.

Structural underownership across European equities, amplified by extreme hedge fund short positioning documented by Barclays strategists, creates a mechanical snap-back dynamic that is independent of the reform thesis and can accelerate any sentiment-driven re-rating toward BofA’s 630 target.

For investors already holding European equities, these are the specific triggers that would signal the reform thesis is breaking down and a position review is warranted. A renewed energy disruption, a stalled pension bill, or a material deterioration in PMI readings through late 2026 would each weaken the assumptions behind the 630 figure.

The revised target is a scenario, not a floor. It becomes a useful input only when you understand the conditions under which it holds and the conditions under which it fails.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including BofA’s price target and reform impact projections, are subject to change based on market developments and policy outcomes.

BofA’s 630 target warrants constructive positioning in European equities, particularly in sectors with clear reform linkage, rather than either dismissal or unconditional bullishness. The question for most investors is not binary (in or out) but directional: calibration and sector tilt.

Four monitoring conditions will either validate or challenge the thesis through late 2026 and into 2027:

The sectors with the clearest reform linkage remain consumer and services, industrials (ex-auto), and financials with German exposure. Investors already holding European equities face a calibration decision; those with no exposure face a timing question best answered by the signals above rather than the headline number alone.

For investors wanting to understand the full scope of the positioning gap, our full explainer on European institutional positioning covers the Barclays upgrade from the same date, Germany’s fiscal disbursement schedule, and why the June 2026 BofA Fund Manager Survey shows institutional underweight at levels not seen since December 2024.

Investors with a 12-18 month view are better positioned to absorb the verification lag than those seeking near-term catalysts. The most actionable takeaway from the BofA upgrade is not 630 itself, but knowing which sectors carry the reform dividend and which monitoring conditions tell you whether the thesis is holding.

Bank of America raised its year-end 2026 Stoxx 600 price target from 590 to 630 on 3 July 2026, implying an uplift of approximately 6.8% and reflecting improved expectations driven by Germany's structural reform package, easing energy costs, and a more cooperative monetary backdrop.

Announced on 2 July 2026, Germany's Programme for Revival and Employment is a structural reform package built on four pillars: roughly 10 billion euros per year in income tax relief, pension reform, labour-market flexibility, and 34 bureaucracy-reduction measures. It sits at the centre of BofA's revised Stoxx 600 thesis because it changes the Eurozone's medium-term earnings trajectory, particularly for consumer, industrial, and financial stocks with German exposure.

Consumer and services names with German revenue exposure are the most direct beneficiaries, as the 10 billion euro annual tax relief enters household budgets from 2027. Industrials (excluding autos) gain from reduced bureaucratic friction, and financials benefit from improved growth visibility, while the automotive segment faces persistent Chinese EV competition that the reform package does not address.

The earliest window for verifiable data is 2027, when the income tax relief takes effect on 1 January 2027 and retail sales, services activity, and labour-market statistics begin reflecting the consumption response. BofA explicitly framed its upgrade as pricing policy direction rather than near-term GDP upside, with pension-linked retirement age effects not materialising until after 2031.

BofA described current European equity valuations as priced for perfection, meaning any legislative dilution of the reform package, failure to pass pension legislation by end-2026, a renewed energy shock, or a macro surprise could push outcomes below 630. The 630 figure is a scenario built on intact reform delivery and contained macro conditions, not a floor.