Why BTK Inhibitor Resistance Opens a Door for Off-the-Shelf CAR-T

41 mins ago

One hundred thousand jobs. That is the number attached to Volkswagen’s reported restructuring plan, surfaced by Germany’s Manager Magazin and relayed by Reuters and CNN ahead of the Monday 29 June 2026 trading week. It represents roughly 15% of the company’s entire global workforce, and it is not a labour headline. It is the clearest signal yet that the economics underpinning how legacy automakers make money are being formally abandoned.

VW has not confirmed the full plan. A spokesperson declined to comment on “internal, confidential documents,” acknowledging only that the matter would be discussed in company committees. But the spokesperson also confirmed the premise behind it: producing in Europe for global export “no longer works” for all brands.

Here is the framework for deciding whether this is a Volkswagen-specific crisis or the opening phase of a sector-wide repricing event, what the reported plan actually contains, where the execution friction lives, and which parts of your portfolio carry exposure you may not have mapped yet.

The sourcing chain matters. Manager Magazin published the original report. Reuters and CNN relayed it. VW’s spokesperson declined to confirm but did not dispute the substance, a response pattern that, for a report of this magnitude, amounts to high-credibility guidance rather than speculation.

The Reuters reporting on the VW restructuring, relayed across international outlets on 26 June 2026, confirmed the four-plant closure list and the scale of the investment reduction, lending the Manager Magazin figures a credibility level that moves them from leak to actionable market information.

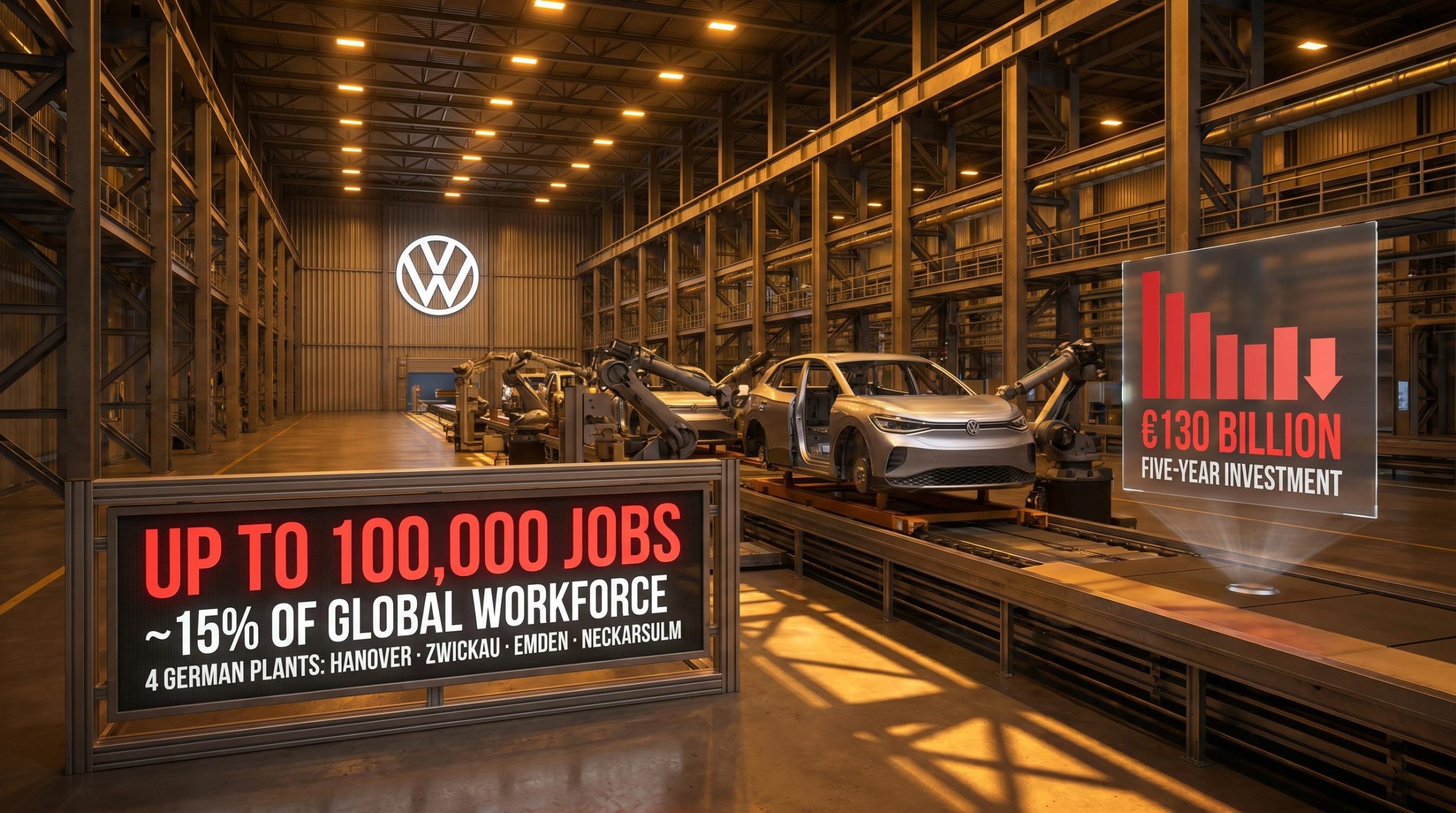

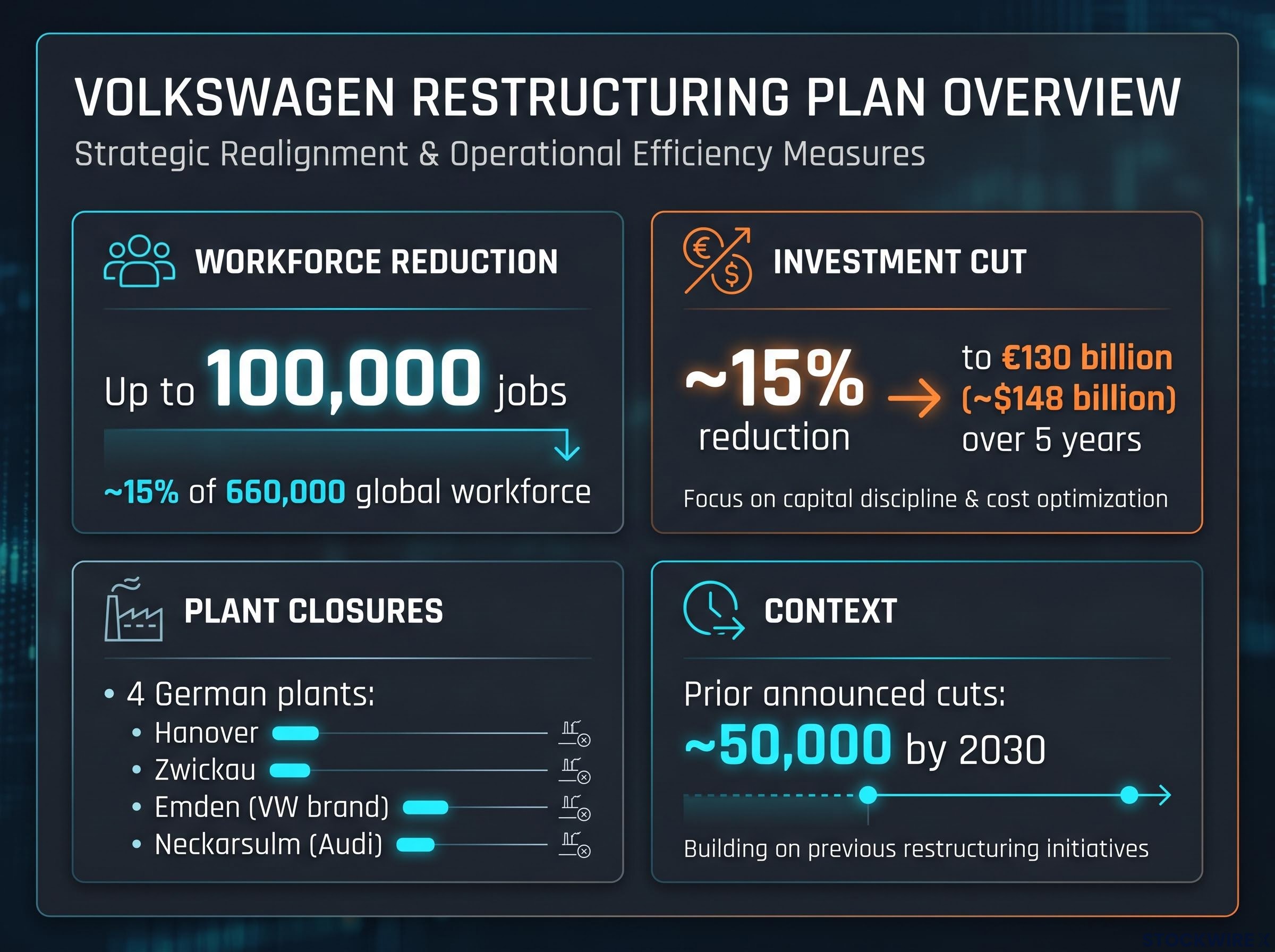

The reported plan has four components: job cuts of up to 100,000 positions worldwide (approximately 15% of the 660,000-person global workforce), closure of four German plants, a reduction of roughly 15% in five-year investment spending to just over €130 billion (approximately $148 billion), and consideration of spinning off the core VW passenger-car brand and the parts and components division. The plan goes well beyond the already-announced 50,000 German job cuts targeted by 2030.

| Metric | Reported figure |

|---|---|

| Worldwide job cuts | Up to 100,000 |

| Share of global workforce | ~15% |

| German plants targeted | Hanover, Zwickau, Emden (VW brand); Neckarsulm (Audi) |

| Five-year investment cut | ~15%, to just over €130 billion (~$148 billion) |

| Prior announced German cuts | ~50,000 by 2030 |

| Job-security agreements | In force through 2030/2033 |

The reported consideration of spinning off the core VW passenger-car brand and the components division into separate entities, potentially with separate stock listings, would represent a strategic break with the integrated group model. That model has historically been positioned as a source of scale advantage: shared platforms, centralised procurement, cross-brand component supply. If management is seriously evaluating dismantling it, the implication is that the scale benefits no longer outweigh the cost and complexity drag. For investors, this is the most structurally significant component of the entire report.

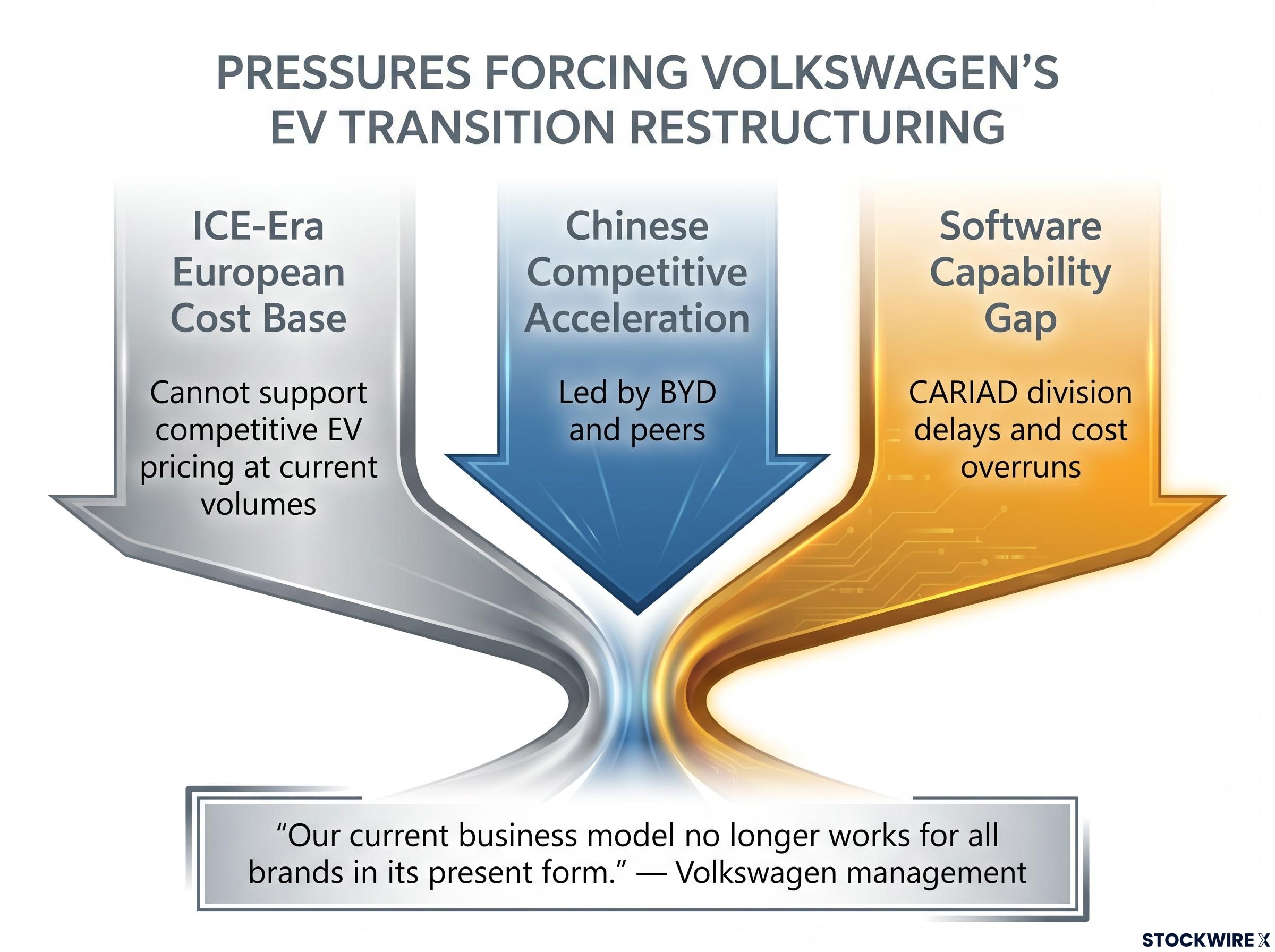

The headline is 100,000 jobs. The underlying story is arithmetic. VW’s cost structure was built for internal combustion engine manufacturing at scale, in high-cost European locations, at a time when that model generated reliable margins. That model is no longer viable under current EV pricing and competitive dynamics.

Three pressures are compounding simultaneously:

Chinese EV pricing is structurally insulated from the US market by a three-layer barrier combining a 100% tariff, a connected vehicle software ban, and federal tax credit exclusion, which means the margin pressure that BYD and peers are exerting on European incumbents like VW has no equivalent relief valve on the US side of the competitive equation.

“Our current business model no longer works for all brands in its present form.” — Volkswagen management

This is not a VW-specific admission. Ford has acknowledged heavy per-vehicle losses on EVs. GM and Stellantis have both revised EV rollout plans and margin expectations. VW’s reported plan puts a hard operational number on what that margin compression means in practice. The combination of external pricing pressure and internal software failures tells you that VW is not cutting costs to fund a clear transition plan. It is cutting costs because the transition is already more expensive and slower than planned.

The tension between brand preservation and luxury EV economics is playing out in parallel across the premium segment, with Porsche and Lamborghini having already retreated from full-EV commitments while Ferrari pressed ahead with the Luce launch and absorbed an immediate 8% single-session share selloff for doing so.

The assumption that legacy automakers are slow-moving cyclicals with durable, if modest, return profiles has rested on two pillars: brand and distribution scale as lasting advantages, and predictable cash generation through the cycle. The VW restructuring challenges both.

When scale itself becomes a liability, as it does when high fixed-cost manufacturing footprints face pricing pressure from leaner competitors, the low-but-stable multiple framework stops reflecting reality. The analytical shift required is significant:

If you still hold legacy auto positions under old-paradigm assumptions, this restructuring is the clearest possible signal that those assumptions need revisiting before the next earnings cycle.

Repositioning away from legacy auto exposure raises the question of where redirected capital finds structural growth; battery metals supply is facing a projected 50% demand increase by 2040 against a supply pipeline constrained by falling ore grades and decade-long greenfield project timelines, making it one of the cleaner ways to gain exposure to EV transition volumes without carrying OEM execution risk.

The remaining €130 billion investment envelope is still substantial. What matters now is its composition. If freed-up capital flows primarily toward deleveraging, buybacks, or dividends, that signals a defensive posture and limited confidence in long-term competitive positioning. If it is redirected toward EV architectures, battery supply, and digital platforms, it supports a thesis that VW is willing to absorb short-term pain to compete in the next phase. The mix, not the total, will be the clearest forward signal investors can monitor.

The ambition is 100,000 jobs. The legal reality is that binding job-security and no-plant-closure agreements are in force in Germany through 2030 and 2033, creating a hard constraint on the pace of any restructuring.

“We will resist with all our might.” — IG Metall and works council representatives

That is not rhetoric. German codetermination law gives works councils genuine blocking power over plant closures and large-scale redundancies. The practical path is likely to involve negotiated voluntary programmes, early retirement packages, and extended timelines, all of which cost more and deliver savings later than the reported plan implies. For investors, the gap between announced ambition and realised savings is a timing and execution risk that belongs in every valuation model covering VW or broader European auto exposure.

Watch these signals in the weeks ahead:

The investment risk here extends well beyond a single ticker. A restructuring of this magnitude will reduce order volumes for Tier-1 and Tier-2 suppliers, particularly those with high VW concentration and Germany-based production. The four plants targeted (Hanover, Zwickau, Emden, Neckarsulm) represent a geographic concentration point for supplier exposure, and plant closures or model programme terminations translate directly into reduced component orders, often with limited notice.

The relevant fault line for supplier equity risk is not simply “auto exposure.” It is the distinction between two categories:

If you hold diversified industrial or European equity positions, mapping your indirect VW supply chain exposure now is the practical step, because the restructuring timeline means order-book risk will materialise before it appears in supplier earnings.

Three near-term signals will determine whether this repricing stays contained to VW or spreads across the sector. First, peer OEM commentary from Ford, GM, Stellantis, and Renault on whether their own restructuring timelines are accelerating. Second, sell-side earnings model revisions incorporating restructuring charges and revised margin trajectories. Third, any formal VW confirmation or committee announcement that moves this from reported plan to binding programme. The difference between reacting to the headline and repricing structural risk across the auto complex sits in those signals.

Whether VW ultimately cuts 70,000 or 100,000 jobs, the structural signal is already unambiguous. The EV and software transition is more disruptive and cost-intensive than incumbents planned for. European manufacturing overcapacity, Chinese competitive pressure, software transition costs, and ICE margin erosion are not future risks. They are current conditions.

The legacy auto sector is being repriced from slow-moving cyclical to fast-moving structural turnaround. Portfolios built on old assumptions carry more hidden risk than historical volatility would suggest. Three watchlist items will clarify the direction over the next 6-12 months:

The question to carry forward is not whether VW will cut enough jobs. It is whether the capital being freed up is being deployed toward a competitive future, or toward a managed decline. The answer to that question will determine whether this restructuring creates long-term value or simply slows the erosion.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

The reported plan targets up to 100,000 jobs worldwide, approximately 15% of Volkswagen's 660,000-person global workforce, going well beyond the previously announced 50,000 German job cuts targeted by 2030.

Four German plants are on the reported closure list: Hanover, Zwickau, and Emden under the core VW brand, and Neckarsulm under Audi.

Three pressures are compounding simultaneously: an ICE-era European cost base that cannot support competitive EV pricing, accelerating Chinese competition from BYD and peers eroding incumbent margins, and costly delays at VW's CARIAD software division that have made the digital transition slower and more expensive than planned.

Binding job-security and no-plant-closure agreements are in force in Germany through 2030 and 2033, and German codetermination law gives works councils genuine blocking power over large-scale redundancies, meaning the practical path involves costly voluntary programmes and extended timelines that will delay and reduce realised savings.

Suppliers with high VW revenue concentration, Germany-based production, and an ICE-focused component mix face the most direct order-book risk; investors holding diversified industrial or European equity positions should map indirect VW supply chain exposure now, because order cancellations will show up before they appear in supplier earnings reports.