Why the Mid-Cap Rotation Beat Mega-Cap Tech in June 2026

2 mins ago

European equities are hitting fresh highs in early July 2026, and the institutional investors best positioned to ride the move have largely stayed out. That gap between price action and positioning is the tension at the centre of this market.

This is not a short-covering bounce. Barclays formally upgraded its outlook on the European region in a strategy note dated 3 July 2026, citing improving earnings revision trends, broadening sector participation, and a narrowing performance gap with the United States. Underneath that upgrade sits a German reform package with real fiscal architecture: a functioning €500 billion infrastructure fund, a multi-year borrowing expansion, and economic surprise indices that have turned upward across the continent.

Here is the case for European equities broken down layer by layer: the macro backdrop, the reform architecture, the EU funding that reinforces it, the sectors and names most exposed, the structural reasons institutions remain cautious, and the specific signals worth monitoring before making a portfolio decision.

European equities have advanced to fresh highs as of early July 2026, and the composition of the move matters as much as the direction. While U.S. market gains have been driven by a handful of dominant mega-cap technology names, the European advance has spread broadly across multiple sectors. Financials, industrials, and materials have all contributed to the advance.

European equity markets are not a single investable category: Switzerland, Spain, and Italy serve materially different portfolio roles as a defensive anchor, an income sleeve, and a cyclical growth position respectively, which means the index product you use to access Europe shapes your reform exposure as much as the reform story itself.

Barclays European Equity Strategy analysts, in their 3 July 2026 note, pointed to three reinforcing signals:

According to Barclays, institutional flows into Germany have returned to the levels that prevailed before the early 2025 elections, but the data does not yet show the scale of reallocation that would accompany a genuine re-rating of the region. Major long-only investors, including the pension funds and endowments that oversee the largest pools of allocatable capital, have yet to meaningfully increase their European positions.

That positioning gap tells you something important about timing. If the market were in the late stages of a re-rating, institutional capital would already be in. The fact that it is not suggests the move may still be closer to its beginning than its end, and the conditions for institutional re-engagement are measurable.

Germany’s reform agenda is often summarised in headlines as “spending more.” The architecture underneath that summary is worth understanding, because it signals a multi-year fiscal commitment rather than a one-cycle stimulus.

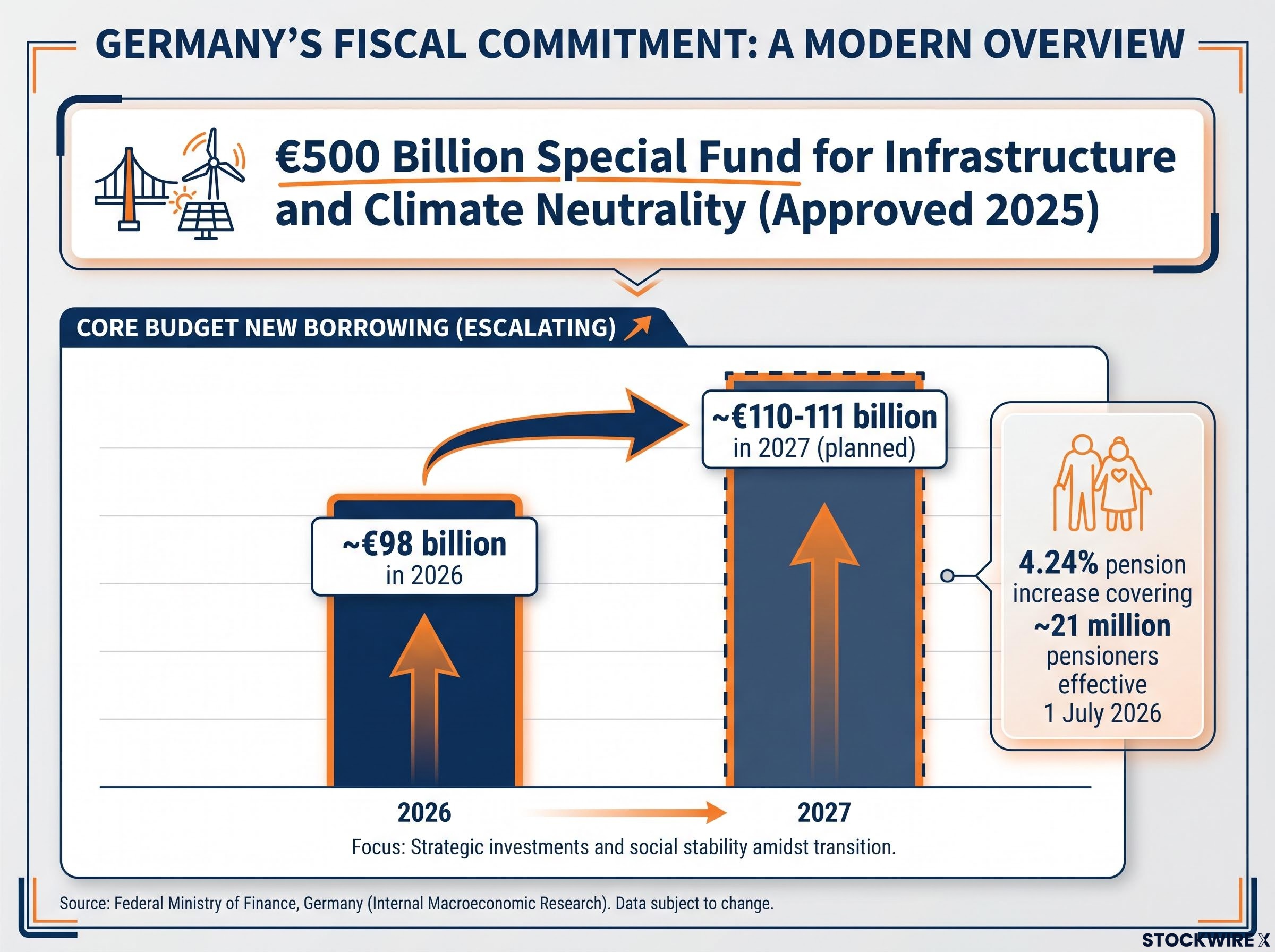

The centrepiece is the €500 billion Special Fund for Infrastructure and Climate Neutrality, approved in 2025 with disbursements now operational. The fund is designed to run over approximately a decade, with annual allocations in the tens of billions directed at modernising infrastructure and investing in public goods.

The German finance ministry has explicitly framed the agenda as “not an austerity programme but a sovereignty project,” a deliberate break from Germany’s historically conservative fiscal stance. Chancellor Friedrich Merz, elected on 6 May 2025 to lead a CDU/CSU-SPD coalition following the 23 February 2025 federal election, has overseen a legislative package that extends well beyond infrastructure:

The borrowing trajectory confirms the intent is structural. Planned new borrowing for 2027 sits at approximately €110-111 billion in the core budget, up from approximately €98 billion in 2026.

| Metric | 2026 | 2027 (planned) |

|---|---|---|

| New borrowing (core budget) | ~€98 billion | ~€110-111 billion |

That escalation from 2026 to 2027 is the detail that separates this from temporary fiscal loosening. Germany is committing to a rising borrowing path across multiple budget years, which means the fiscal impulse is designed to compound rather than fade.

Germany’s national reform agenda does not operate in isolation. The Recovery and Resilience Framework (RRF), the EU-level programme that allocates grants to member states for recovery and structural reform, adds a second committed capital stream that converges on many of the same sectors.

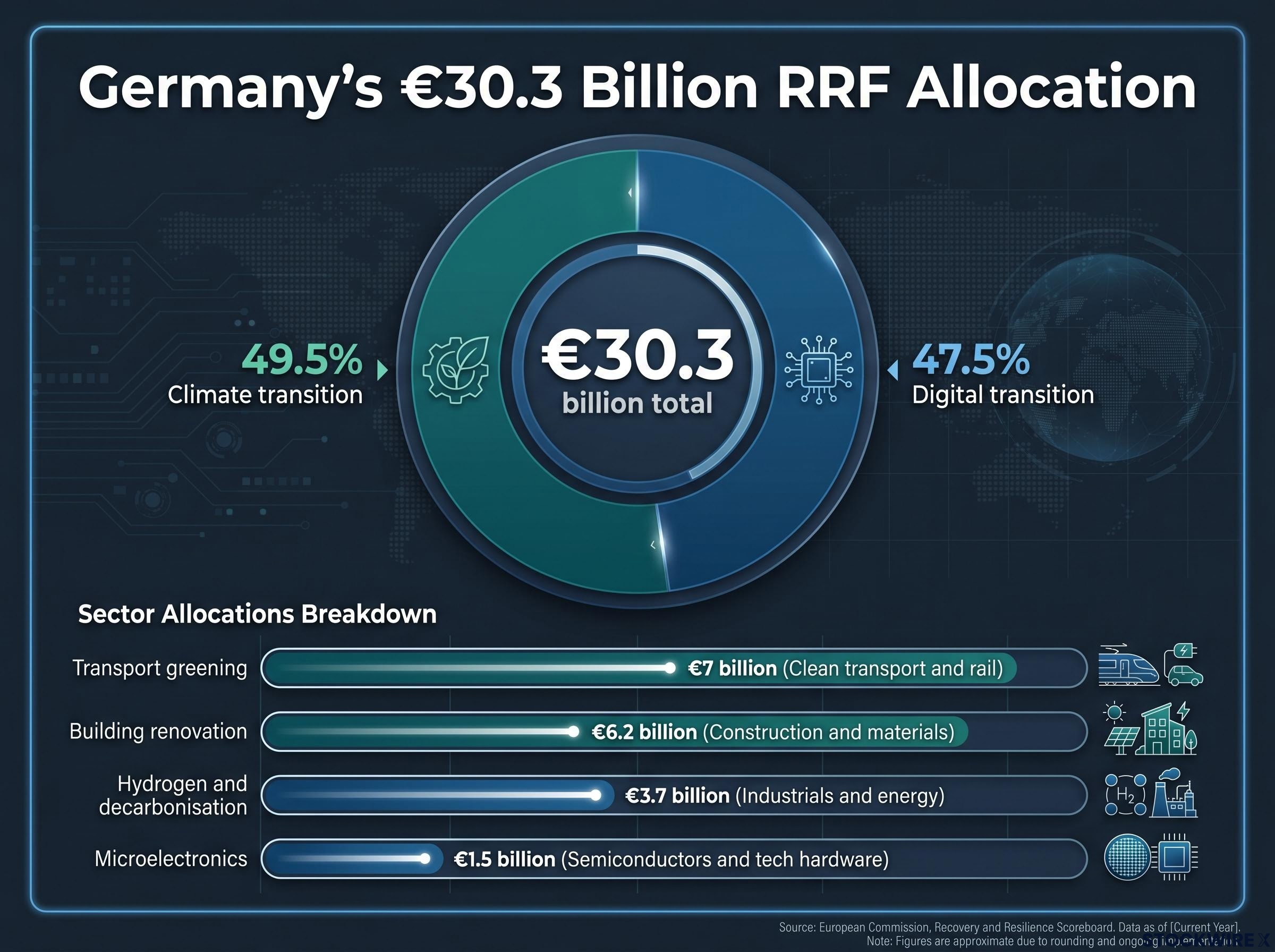

Germany’s RRF allocation totals approximately €30.3 billion in grants, heavily weighted toward two priorities: climate transition (approximately 49.5% of the total) and digital transition (approximately 47.5%). The specific allocations create visible multi-year demand in defined sectors.

The EU Council’s approval of Germany’s amended RRF plan confirmed the €30.3 billion total grant allocation, with the requirement that all implementation measures be completed by end-2026, giving the milestone calendar a hard regulatory deadline rather than a soft policy target.

| RRF allocation category | Amount | Primary equity sector exposed |

|---|---|---|

| Transport greening | €7 billion | Clean transport and rail |

| Building renovation | €6.2 billion | Construction and materials |

| Hydrogen and decarbonisation | €3.7 billion | Industrials and energy |

| Microelectronics | €1.5 billion | Semiconductors and tech hardware |

Most RRF milestones are scheduled for completion by August 2026, giving equity analysts near-term visibility on committed spending timelines.

Multi-year committed spending with milestone deadlines gives analysts something they rarely get in macroeconomic analysis: a forward order book for entire sectors. That directly supports earnings visibility for construction, renewables, and digital infrastructure companies. And because the EU funding layer is structurally independent of German coalition politics, it provides a floor of sector demand that persists even if domestic reform implementation slows.

The reform and funding architecture maps onto specific layers of the European equity market, and the distinction between those layers matters for how you access the story.

Germany’s export-oriented DAX names, the autos, global industrials, and chemicals firms, are the traditional way global investors access the German market. But the reform story’s primary beneficiaries sit below that headline index level. Domestically oriented mid-caps and small-caps carry greater exposure to construction activity, consumer spending, housing, and local services. Reforms to pensions, housing, social security, and labour supply, combined with the infrastructure spending programme, all support their earnings outlook more directly.

For an investor who has primarily accessed Europe through DAX-heavy index products, this matters. Standard index exposure may underweight the most reform-sensitive names.

Barclays explicitly named the banking sector among the likely beneficiaries in its 3 July 2026 note. Higher public borrowing, infrastructure investment, and EU-funded green and digital projects typically drive credit demand, capital-markets activity, and insurance coverage.

The banking sector’s reform-era earnings uplift carries a counterweight that the fiscal narrative does not resolve: the ECB has mapped approximately €425 billion in private credit spillover risk across European insurers, banks, and pension funds, with second-round losses through equity portfolio revaluations potentially exceeding direct credit losses in a severe scenario.

The broader beneficiary categories include:

Europe’s overall sector composition, heavier in financials, industrials, staples, and energy than U.S. indices, provides genuine differentiation that is independent of the reform narrative. The reform story adds a catalyst layer on top of that structural difference.

The rally has happened without the participation of the institutions whose re-engagement would deepen it most. That absence is not irrational. It is structural, and understanding its specific causes also defines the conditions for upside.

Global capital flows in 2026 have compounded the structural underweight, with a self-reinforcing dollar feedback loop amplifying returns on U.S. semiconductor positions and directing institutional allocation toward AI-linked U.S. equities rather than European markets, even as aggregate European fund flows at the headline level have remained technically positive.

Barclays identified four named deterrents keeping long-only institutional investors out:

The obstacles run deeper than perception. The CDU/CSU-SPD coalition faces low approval ratings and significant internal splits over pension and welfare reform. Many key measures still require Bundestag and Bundesrat approval, and Barclays specifically flagged doubts about whether the infrastructure programme’s capital will be deployed effectively.

The 2027 borrowing expansion, while a signal of fiscal commitment, raises ongoing questions about Germany’s constitutional debt brake and the sustainability of the expansion. And despite policy efforts to lower energy costs, Europe’s energy prices remain above pre-2022 levels relative to the United States, which continues to influence where multinationals deploy capital.

For investment committees that have spent years reducing European exposure, a structural re-weighting typically requires several quarters of consistent data and policy delivery. One strong year or one reform announcement is not enough.

The institutional hesitancy is, in that sense, measurable. The conditions for re-engagement are specific, which means they can be monitored rather than guessed at. And the structural underweight across pensions and endowments represents a large pool of latent demand that has not yet moved.

The June 2026 BofA Global Fund Manager Survey provides the most recent institutional positioning data on European equities: fund managers had European equities at their most underweight since December 2024, while simultaneously recording record-high concentration in long global semiconductors, a configuration that frames the European structural underweight as the direct inverse of the AI crowding trade.

The question is not whether Europe’s reform story is real. The fiscal architecture, the committed EU funding, and the broadening market participation all point in the same direction. The question is whether institutional capital follows, and that depends on measurable confirmation signals.

Three categories of signal matter most:

Germany’s 2026 GDP growth forecasts highlight a live tension: the European Commission projects approximately 0.5-0.6%, while the German government’s own Annual Economic Report projects 1.0%. Both mark an improvement from 0.2% in 2025, but the gap between them means the incoming economic surprise data will function as a real-time verdict on whether the reform agenda is delivering.

| Signal category | Specific indicator | What it confirms |

|---|---|---|

| Macro data | Economic surprise indices for Europe and Germany | Whether reform is delivering above-forecast growth |

| Earnings | Revision trend direction for European indices | Whether sector earnings are following fiscal spending |

| Legislative progress | Bundestag and Bundesrat votes on pension and welfare measures | Whether reforms pass in current form |

| Flow data | Institutional allocation data beyond pre-election reversion | Whether structural re-weighting has begun |

| Spending effectiveness | Infrastructure deployment vs. committed timelines | Whether the €500 billion fund is translating to economic activity |

The RRF milestone deadline of August 2026 provides the nearest observable data point. Legislative passage of key reform measures is the next catalyst. And the earnings revision trend across European indices will tell you whether the fiscal spending is showing up where it matters most: in corporate results.

The European stock market has a more credible structural story than it has had in several years. The fiscal commitment is real, the EU funding layer is independently locked in, and the sector breadth of the rally distinguishes it from previous false starts. But the timing and scale of institutional re-engagement will depend on sustained policy delivery, legislative passage, and consistent macroeconomic confirmation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including growth forecasts and reform implementation timelines, are subject to change based on political developments, market conditions, and various risk factors.

The rally is driven by broadening sector participation across financials, industrials, and materials, improving economic surprise indices, and Germany's €500 billion infrastructure fund combined with €30.3 billion in EU Recovery and Resilience Framework grants, all reinforced by a formal Barclays upgrade on 3 July 2026.

The Special Fund for Infrastructure and Climate Neutrality is a multi-year fiscal commitment approved in 2025, with annual allocations in the tens of billions directed at modernising infrastructure; it creates sustained earnings visibility for construction, renewables, and digital infrastructure companies listed on European exchanges.

Barclays identified four specific deterrents: continued dollar strength favouring U.S. assets, competitiveness concerns about European industry, a widely held perception that structural reform has not advanced, and the dominance of the U.S. AI outperformance narrative across investment committees; the June 2026 BofA Fund Manager Survey confirmed European equities at their most underweight since December 2024.

Domestically oriented German mid-caps and small-caps in construction, housing, and consumer services carry the most direct exposure, alongside German and European banks, clean transport and rail, renewables and grid modernisation, and digital infrastructure companies receiving RRF-funded contracts.

The key indicators are European economic surprise indices, the earnings revision trend direction for European indices, legislative progress on pension and welfare reforms through the Bundestag and Bundesrat, institutional flow data beyond pre-election reversion levels, and infrastructure spending deployment against the €500 billion fund's committed timelines, with the RRF milestone deadline of August 2026 providing the nearest hard data point.