What Two ASX Broker Calls Reveal About the Rate Cycle Trade

21 mins ago

DroneShield rose 760% at its peak. Then it fell 60% from the high. The investors who made generational returns were not the ones who chased the narrative loudest; they were the ones who entered before the sector had a name and scaled out before the crowd arrived.

Boresight (ASX: BST) listed on 10 June 2026 at $0.20, hit $0.595 within three sessions, and has since pulled back to the mid-30 cent range. The ASX defence sector’s tailwinds remain real, but its easy-money phase has already passed. The question for anyone looking at Boresight now is whether this is the early chapter of a DroneShield-style story, or the late one.

Here is a structured way to answer that question: a framework for deciding whether Boresight warrants a position, at what price, and with what expectations. Not a buy or sell call. A set of tools for making your own.

DroneShield reached a market capitalisation of approximately $5.7 billion in October 2025, a period when the stock had gained roughly 760% over the year to that point. Since then, the share price has shed approximately 60%, placing the company’s market cap at around $2.2 billion as at 2 July 2026.

DroneShield has continued posting record quarterly results and maintained positive cash flow throughout, yet its share price sits roughly 60% below its all-time high. Strong sector fundamentals and solid company execution are not sufficient to hold a valuation once a speculative premium begins to unwind.

The investors who captured that move were positioned before the defence theme had broad retail recognition. By the time the narrative was consensus, the multiple had already expanded beyond what even strong earnings growth could sustain. That asymmetry is the defining feature of thematic investing: early capital is rewarded; late capital absorbs the de-rating.

The sector is not uniformly sold off. Electro Optic Systems and Elsight had both held within 10-15% of their respective all-time highs by early July 2026. The cohort is differentiated by execution, not dragged down by a single narrative shift.

Sector differentiation by execution rather than uniform narrative movement was visible in May 2026, when EOS, DroneShield, and Elsight posted intra-session gains of up to 11% against a falling ASX 200, with each company’s relevance to a specific geopolitical catalyst driving the divergence rather than any broad-based defence re-rating.

| Company | Approximate Peak Market Cap | Market Cap (Early July 2026) | Status |

|---|---|---|---|

| DroneShield | ~$5.7 billion | ~$2.2 billion | ~60% off peak; record earnings, cash flow positive |

| Electro Optic Systems | Near current levels | Within 10-15% of record high | Near all-time highs |

| Elsight | Near current levels | Within 10-15% of record high | Near all-time highs |

What this tells you about Boresight: it is entering a listed market where the speculative premium in the leading name has already unwound. The sector backdrop supports long-term demand, but the valuation tolerance that propelled DroneShield’s ascent is gone. Every new entrant now faces a market that wants evidence first.

Boresight produces low-cost drone targets engineered to be shot down during live counter-UAS training. These attritable platforms are purpose-designed for military exercises that require realistic, expendable aerial targets, allowing armed forces to train against drone threats without using costly operational assets. Counter-UAS refers to counter-uncrewed aerial system, the military discipline of detecting and neutralising hostile drones.

The commercial logic follows from the product design. Every training exercise that destroys a target drone generates a reorder. There is no new sales cycle, no capital expenditure approval process, no multi-year procurement review. If the platform is embedded in formal training doctrine, the consumption drives the revenue line automatically.

Beyond single-use target drones, the product ecosystem includes:

These extensions create switching costs and upsell pathways that deepen the commercial relationship beyond disposable consumables.

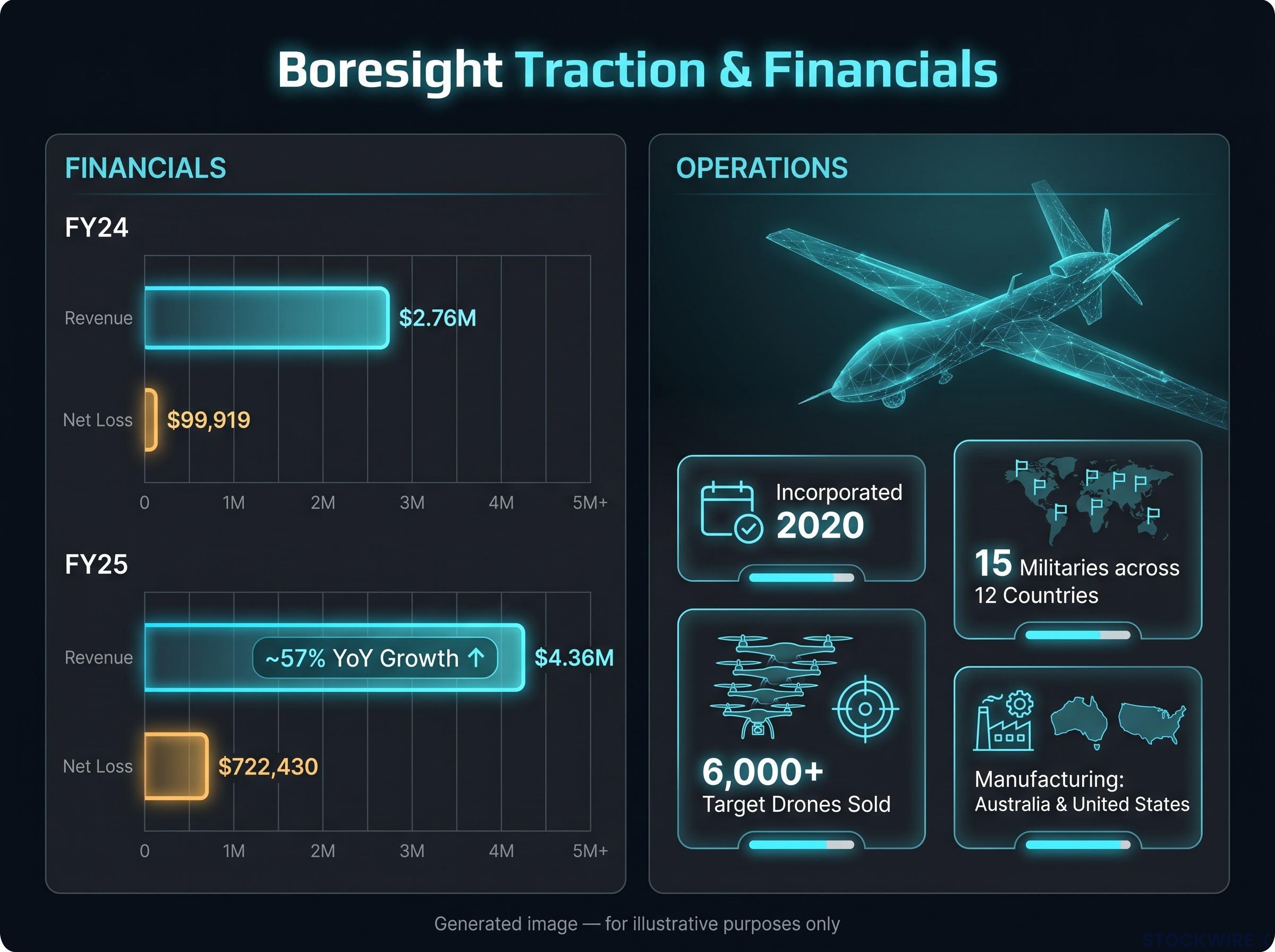

Since incorporation in 2020, Boresight has sold over 6,000 target drones to 15 militaries across 12 countries, with manufacturing in both Australia and the United States. That footprint represents early traction, not proof of scale. For the recurring-revenue thesis to hold, those relationships need to deepen into doctrine-level standardisation rather than remaining as trial-and-evaluation engagements.

DroneShield’s $1.3 billion Project LAND 156 panel selection illustrates the recurring revenue model Boresight’s consumables thesis is designed to replicate: a Capability as a Service structure shifts revenue toward high-margin software licensing and support streams once a supplier achieves doctrine-level standardisation across a network of defence bases.

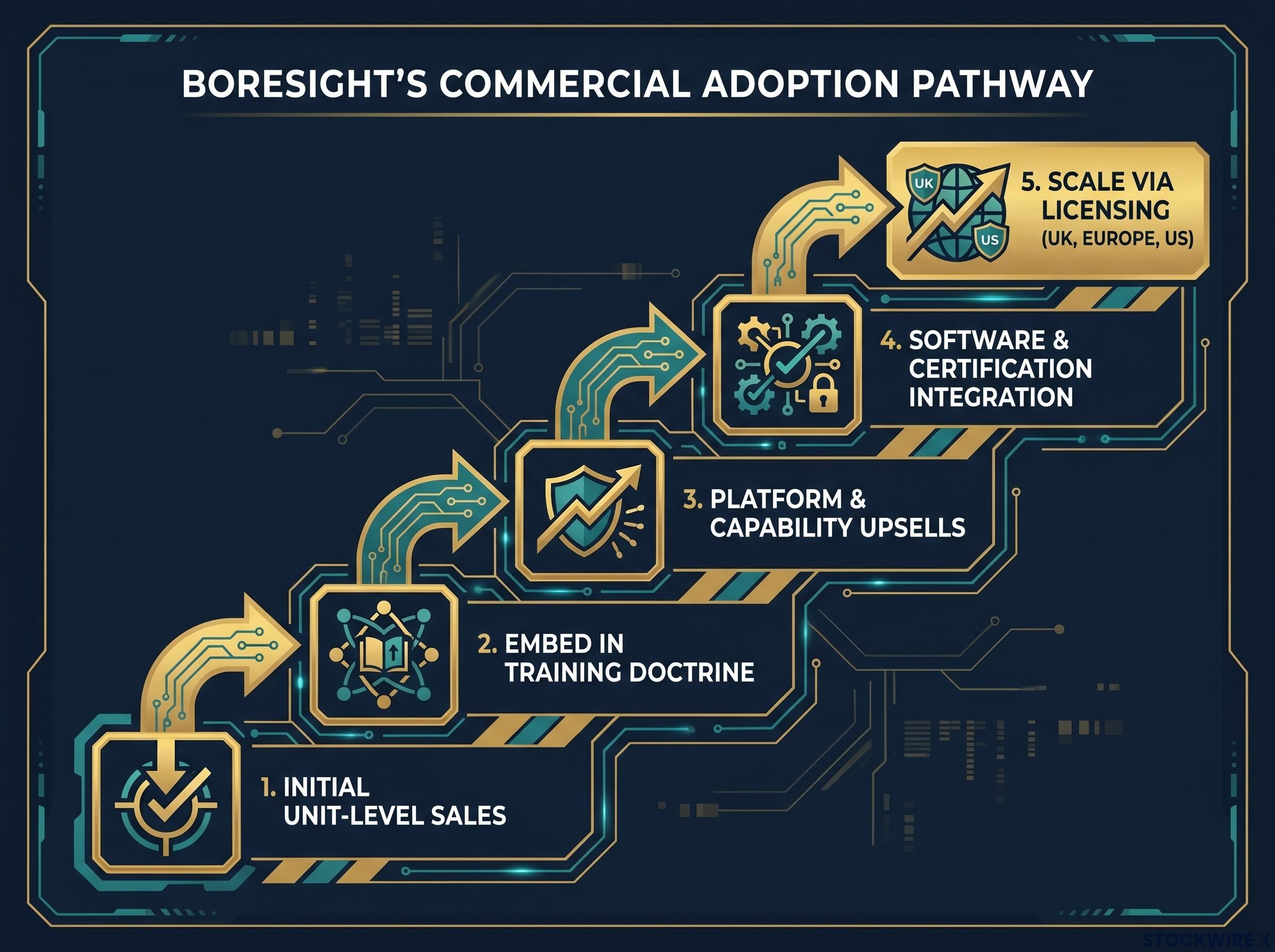

Boresight’s growth strategy follows a five-step commercial pathway: securing initial unit-level sales to gain a foot in the door with military customers, embedding products within established training doctrine so that reorders become automatic, expanding the relationship through higher-value platform and capability upsells, locking in customers through software and certification integration that raises switching costs, and ultimately scaling through a licensing model targeting allied markets including the UK, Europe, and the United States.

Stage transitions are where execution risk concentrates. Moving from trial orders to doctrine standardisation requires institutional buy-in from military procurement organisations that operate on multi-year timelines. Most early-stage defence companies stall between stages two and three, where the product works but the bureaucratic adoption process has not yet converted capability into committed spend.

According to its prospectus, Boresight grew FY25 revenue to $4.36 million, representing a 57% increase on the $2.76 million recorded in FY24. At this stage of the company’s development, that growth rate is a genuine positive signal, confirming that customer acquisition is accelerating rather than plateauing.

| Metric | FY24 | FY25 |

|---|---|---|

| Revenue | $2.76 million | $4.36 million |

| Net Loss | $99,919 | $722,430 |

| Revenue Growth (YoY) | — | ~57% |

Over the same period, the net loss expanded significantly, moving from $99,919 in FY24 to $722,430 in FY25. That is investment-phase spending: product development, manufacturing scale-up, and international market development. It is not evidence of a broken model, but it does require ongoing monitoring. If revenue growth slows while costs continue expanding, the investment-phase framing stops being credible.

Boresight raised $8 million at its IPO, listing with a post-raise market capitalisation of approximately $41.8 million. Less than a month later, the implied market cap sits at approximately $72-75 million. The valuation has nearly doubled before the first post-listing earnings report.

At a mid-30 cent share price and roughly $72-75 million market cap, Boresight trades at a mid-teens revenue multiple on a loss-making base. A mid-teens revenue multiple on a microcap with no near-term path to profitability means the market is already pricing in several years of strong growth. Any slowdown in doctrine adoption or export conversion will compress that multiple faster than the revenue line can compensate.

Defence spending tailwinds are real. That does not make every company within the theme a good buy at every price. Four distinct risk categories apply to Boresight at this stage:

The defence sector de-rating pattern is not unique to ASX names: Goldman Sachs, BofA, and Barclays each flagged overcrowding in April and May 2026, with Lockheed Martin and Raytheon trading at 25x forward multiples versus 18x pre-2022 levels, a valuation compression risk that travels across listed markets when speculative premiums unwind.

The price sequence tells a recognisable story. Boresight came to market at $0.20 and ended its first trading day at $0.32, a gain of 60%. The second session saw the stock finish at $0.545 before the third day produced a peak of $0.595, with buying pressure fading thereafter. The shares have since pulled back to the mid-30 cent range, sitting roughly 40-43% below that early high.

This is not commentary unique to Boresight. It is an observable pattern in ASX small-cap IPOs within high-momentum sectors: retail enthusiasm compresses into a waiting period for hard financial evidence. The investors who bought above $0.50 are now sitting on meaningful losses despite the company having done nothing wrong operationally.

That 40%-plus retracement is not a signal the thesis is broken. It is a signal that buying into IPO excitement, rather than business milestones, carries a real and rapidly materialising cost.

Rather than defaulting to sector conviction as a substitute for company-level analysis, investors can structure the decision around five testable questions:

The difference between a good sector and a good stock at a good price is where most retail investors lose money in thematic investing. The sector can be right and the entry can still be wrong.

Manufacturing in both Australia and the United States positions Boresight within allied-procurement frameworks, a structural advantage for Five Eyes and AUKUS-aligned contracts, but one that has not yet converted into disclosed programme wins.

Owning Boresight at the current price means holding a specific set of convictions. Making them explicit is the only way to manage the position over time.

The bull case requires you to believe:

The bear case requires equal precision:

The DroneShield experience provides the reference point. Early investors in an undiscovered name captured generational returns. Late-cycle buyers of peak narratives absorbed a 60% decline even as the company delivered record earnings. Boresight is entering a listed market after the speculative peak, not before it.

The investors most likely to succeed with Boresight are those who can articulate the specific milestones that would move the stock from thesis to evidence, and who have sized the position so a 40-50% further drawdown does not force an exit before those milestones arrive.

For investors wanting to stress-test the portfolio construction decisions around concentrated thematic exposure, our full explainer on thematic ETF sector rotation risk examines the behaviour gap between reported fund returns and actual investor returns, including why peak-conviction entry timing consistently destroys value in high-momentum themes.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Boresight produces low-cost attritable drone targets designed to be shot down during live counter-UAS military training, alongside ISR drones, mission planning software, and swarming ground control systems. The consumables model means every destroyed training drone generates a reorder without a new procurement cycle.

Once a drone target platform is embedded in formal military training doctrine, reorders become automatic because each exercise destroys the product. The thesis depends on converting trial-and-evaluation engagements into doctrine-level standardisation, which is where most early-stage defence companies stall.

At a mid-teens revenue multiple on a roughly $72-75 million market cap, the stock is already pricing in several years of strong growth from a loss-making base; doctrine adoption delays, export certification hurdles, or any slowdown from the 57% revenue growth rate would compress that multiple faster than the revenue line can compensate.

DroneShield fell roughly 60% from its October 2025 peak of approximately $5.7 billion market cap despite posting record earnings and maintaining positive cash flow, demonstrating that speculative premiums in ASX defence stocks can unwind independently of underlying business performance.

The key signals are doctrine standardisation announcements from existing military customers converting trial orders into committed programme spend, material export contract wins in the US or UK, and evidence that revenue concentration is diversifying across customer, geography, and product line.