Barclays Warns of Prolonged Market Volatility Under New Fed Reality

Jun 27, 2026

Bank of America has revised its EUR/USD outlook downward, setting fresh targets of 1.12 for end-Q3 and 1.15 for year-end 2026, pulling back from a prior projection of 1.20, while advising clients to hold long dollar positions against the single currency. The revision is not a tweak. It is a directional reversal from the bank’s late-2025 call for EUR/USD as high as 1.22 at this same horizon.

The shift carries weight because BofA is not acting alone. J.P. Morgan has independently moved to a near-identical 1.13-1.15 range, forming what amounts to a major-bank consensus around second-half dollar strength. Behind both calls sits a hawkish Federal Reserve forecast that few were pricing in at the start of the year: BofA now expects three rate hikes before December.

Here is what BofA’s revised call means for EUR/USD positioning, why the bank sees the Fed moving three times before year-end, and where the risks to this view actually sit.

The numbers tell the story. BofA’s updated projections place EUR/USD at 1.12 by end-Q3 2026 and 1.15 at the close of 2026, with the former year-end goal of 1.20 now deferred to end-2027. The directional trade is clear: buy USD, sell EUR.

| Horizon | Prior Target | Revised Target |

|---|---|---|

| Q3 2026 | — | 1.12 |

| Year-End 2026 | 1.20 | 1.15 |

| Year-End 2027 | — | 1.20 |

A bank that was projecting EUR/USD at 1.22 by end-2026 in late 2025 commentary now sees 1.15 at the same horizon. That gap tells you BofA’s fundamental outlook has shifted materially, not incrementally.

BofA’s strategists indicate that additional dollar gains remain on the table should U.S. economic performance continue to exceed expectations, meaning the 1.12 Q3 target could prove conservative if the data cooperates. For traders calibrated to the bank’s earlier, more euro-positive view, the repositioning required is significant.

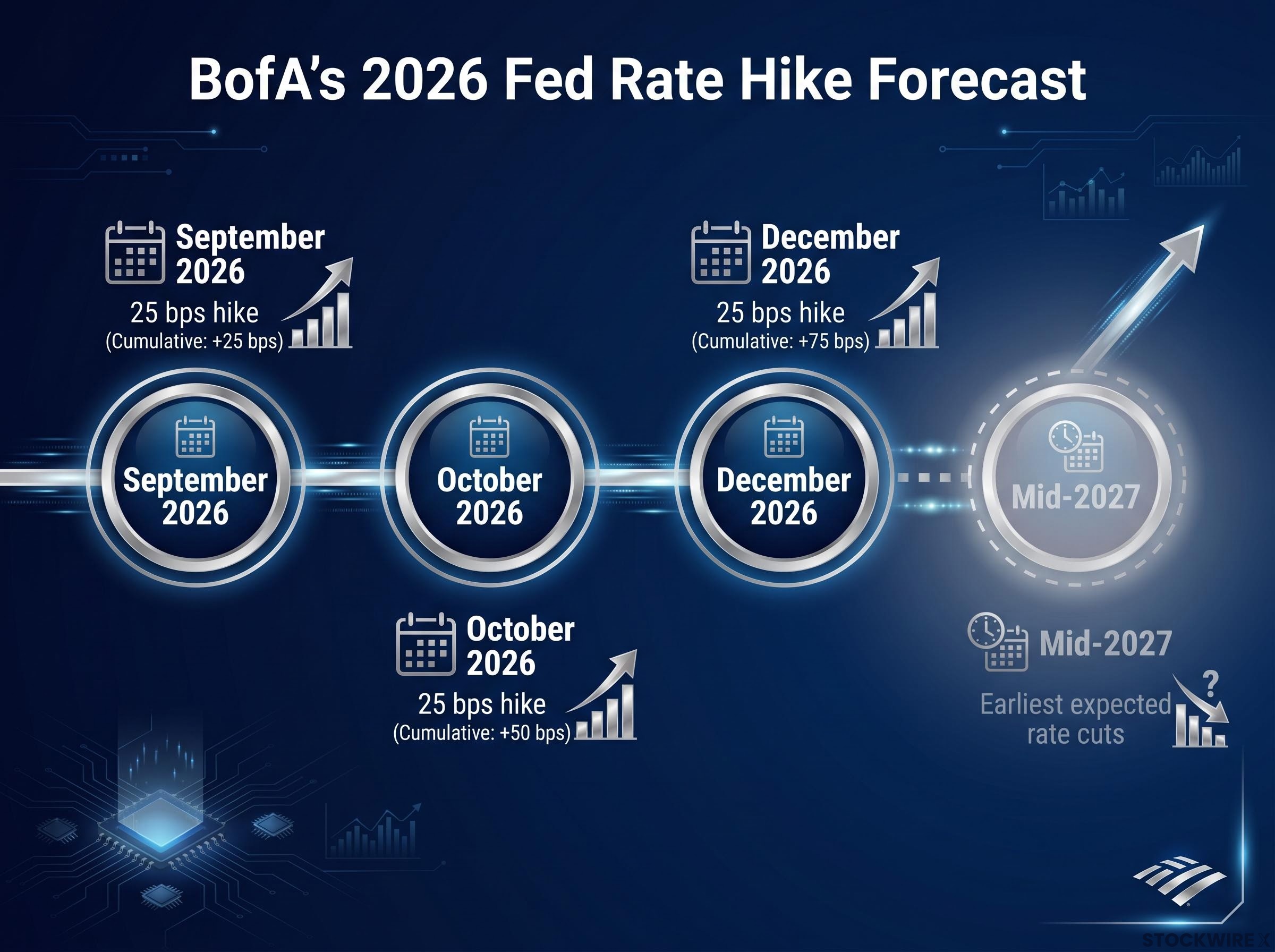

BofA Global Research now forecasts three 25 basis point Federal Reserve rate hikes in 2026, scheduled at the September, October, and December meetings, totalling 75 basis points of tightening.

That is an aggressive path. Earlier BofA commentary had flagged at most one possible hike; three hikes in four months represents a significant escalation. The bank does not expect any additional Fed cuts until mid-2027 at the earliest, reinforcing a higher-for-longer rate environment.

The June dot plot revision, which shifted the Fed’s own year-end rate median from 3.4% to 3.8%, provides the institutional foundation BofA is building on: the Fed itself has put at least one hike into its baseline, and BofA’s three-hike forecast extends that logic further than the committee has publicly signalled.

The mechanism is straightforward. Every hike drives a wider gap between U.S. and eurozone borrowing costs, with the European Central Bank (ECB) seen holding comparatively steady on policy. As that rate gap expands, dollar-denominated assets become more compelling to yield-seeking capital, redirecting flows into USD and out of EUR.

If BofA is right, USD borrowing costs will be rising through Q4 just as ECB policy remains comparatively flat. That divergence is the structural reason the bank sees EUR/USD trading lower through the rest of the year.

The dollar-bull thesis rests on a simple premise: the U.S. is growing faster than Europe, and its central bank is tightening policy. When that combination holds, capital tends to flow toward the higher-growth, higher-rate currency, pushing it higher.

The question for anyone assessing this trade is whether the growth gap is durable or temporary. BofA’s answer is that it is both, and the distinction between the two types of support matters.

The eurozone growth constraints running through BofA’s thesis are visible in the underlying data: eurozone Q1 2026 GDP expanded just 0.1% quarter-on-quarter while April inflation re-accelerated to 3.0% year-on-year, a stagflationary combination that limits the ECB’s room to stimulate and reinforces the relative-growth premium the dollar is currently pricing in.

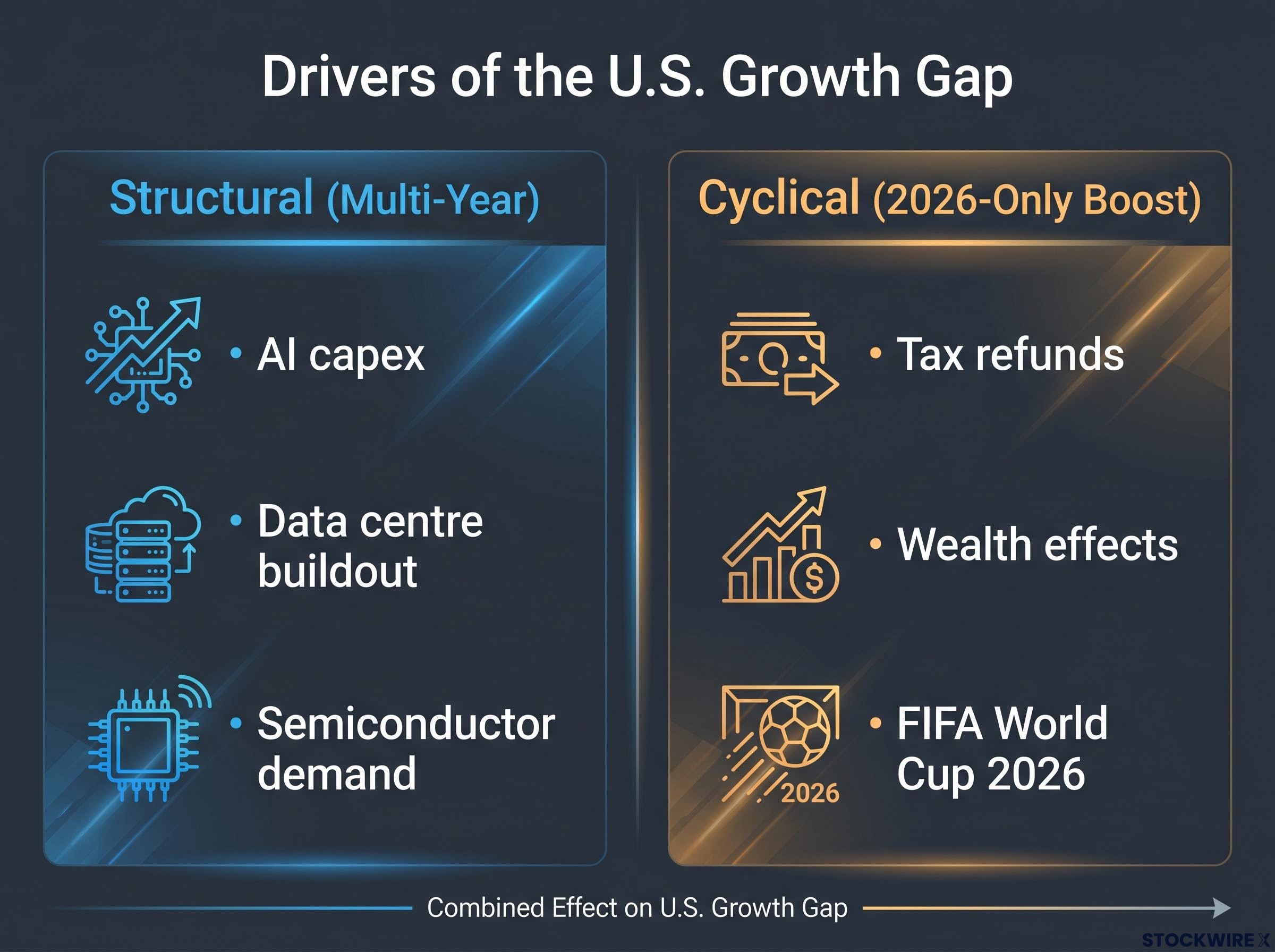

BofA frames AI-related capital expenditure as a multi-year structural driver with no defined endpoint. The causal chain runs from AI investment to data centre buildout and semiconductor demand, which supports U.S. corporate earnings and draws sustained capital inflows into dollar-denominated assets.

This is the part of the growth gap that does not fade with a calendar year. As long as AI capex continues scaling, the U.S. retains a structural investment advantage that translates directly into dollar demand.

Sitting atop the structural picture are short-term boosts that are particular to 2026:

These factors matter for the Q3 and year-end 2026 forecasts, but they are not reasons to expect dollar strength into 2027 and beyond.

According to BofA, the benefit to non-U.S. economies from declining energy costs is unlikely to show up in a meaningful way until 2027 rather than during the current year. That timing assessment keeps the growth gap substantially intact through the forecast horizon. For a reader trying to judge how long this trade works, the distinction is between the AI capex story (which persists) and the cyclical boosts (which do not).

J.P. Morgan Global Research has independently moved to a EUR/USD target of 1.13-1.15 over the next three quarters, converging closely with BofA’s 1.12-1.15 range. Two of the world’s largest banks arriving at the same directional call within weeks of each other shifts the dollar-bull view from a single-bank thesis to something closer to institutional consensus.

MUFG disagrees. The bank projects EUR/USD moving toward approximately 1.20 by Q1 2027, reflecting a more constructive view on eurozone growth recovery and a narrower future rate differential.

| Bank | EUR/USD Target | Key Driver |

|---|---|---|

| Bank of America | 1.12-1.15 (H2 2026) | Three Fed hikes, AI capex, U.S. growth premium |

| J.P. Morgan | 1.13-1.15 (next 3 quarters) | Widening rate differential, U.S. outperformance |

| MUFG | ~1.20 (Q1 2027) | Eurozone recovery, narrowing rate gap |

The specific variables driving the disagreement are identifiable: pace of Fed tightening, speed of European growth recovery aided by energy price relief, and durability of U.S. AI-driven investment. MUFG’s dissent is genuine, but it is currently the minority position among major banks.

For investors tracking how the Fed-ECB policy gap translates into cross-asset positioning beyond the EUR/USD pair, our dedicated guide to global central bank divergence examines the ECB’s stagflation bind, the Bank of Japan’s energy-driven tightening, and Deutsche Bank’s 10-year Treasury yield forecasts that frame the full rate-differential picture.

The BofA thesis has identifiable pressure points, and each one is something you can monitor in real time.

Current EUR/USD spot sits above the 1.12-1.15 zone, meaning meaningful euro depreciation is required for BofA’s call to be validated. The trade is not a confirmation of where the market already is. It is a bet on where it is going.

USD safe-haven demand is not confined to EUR/USD: across G10 pairs, the same structural dollar bid from rate differentials and geopolitical risk is compressing currencies where domestic fundamentals would normally provide a buffer, with AUD/USD near the 0.7000 level despite Australia’s elevated CPI maintaining a positive yield differential against the Fed’s current range.

The point is not that BofA is wrong. It is that the trade has tripwires, and you should know what they are before sizing any position.

BofA’s revised forecast draws a specific arc, not an open-ended dollar rally. Understanding that arc matters for how you think about positioning across different time horizons.

The 2027 target of 1.20 is the detail that qualifies the entire thesis. Even BofA does not see perpetual dollar dominance. The trade has a defined arc: dollar strength through H2 2026, followed by gradual euro recovery as convergence forces build through 2027.

For BofA to be right, the Fed delivers at least two hikes, U.S. growth data holds, and European energy relief does not arrive significantly ahead of schedule. Those are the conditions. Track them.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

Bank of America now targets EUR/USD at 1.12 by end-Q3 2026 and 1.15 by year-end 2026, a significant downward revision from its prior year-end target of 1.20, which has been pushed out to end-2027.

BofA's dollar-bull case rests on three Federal Reserve rate hikes totalling 75 basis points before December 2026, a widening US-eurozone rate differential, AI-driven capital expenditure sustaining US growth, and cyclical boosts including tax refunds and the FIFA World Cup.

BofA Global Research forecasts three 25 basis point hikes at the September, October, and December 2026 Fed meetings, with no additional cuts expected until mid-2027 at the earliest.

J.P. Morgan has independently converged on a 1.13-1.15 EUR/USD target over the next three quarters, aligning closely with BofA; MUFG is the main dissenter, projecting EUR/USD near 1.20 by Q1 2027 on expectations of a eurozone recovery and a narrowing rate gap.

The three main risks are the Fed delivering fewer than three hikes, a deterioration in US growth data that narrows the US-eurozone gap, and a faster-than-expected decline in European energy costs pulling the eurozone recovery forward from 2027 into late 2026.