How HBM’s Coming Price Surge Will Cascade Through AI Supply Chains

3 hrs ago

UBS is not telling investors where the market is going. It is telling them there are three places it might go, and that a portfolio needs to work in all of them.

The bank’s newly released Global Risk Radar, published on 27 June 2026, formalises that approach into a scenario framework with explicit probabilities: a 60% base case and two 20% tails. At the centre of the uncertainty sit four variables UBS considers effectively unforecastable with confidence: geopolitics, inflation, interest rate trajectories, and whether AI spending actually produces the earnings markets have already priced in.

Each scenario below breaks down in specific terms, including price targets and the portfolio moves UBS recommends under each, so you can assess where your own positioning stands before one of these paths becomes reality.

The core argument from UBS‘s Global Risk Radar is that the coming year cannot be responsibly reduced to a single number. Four structural uncertainties interact in ways that make any one-point forecast fragile:

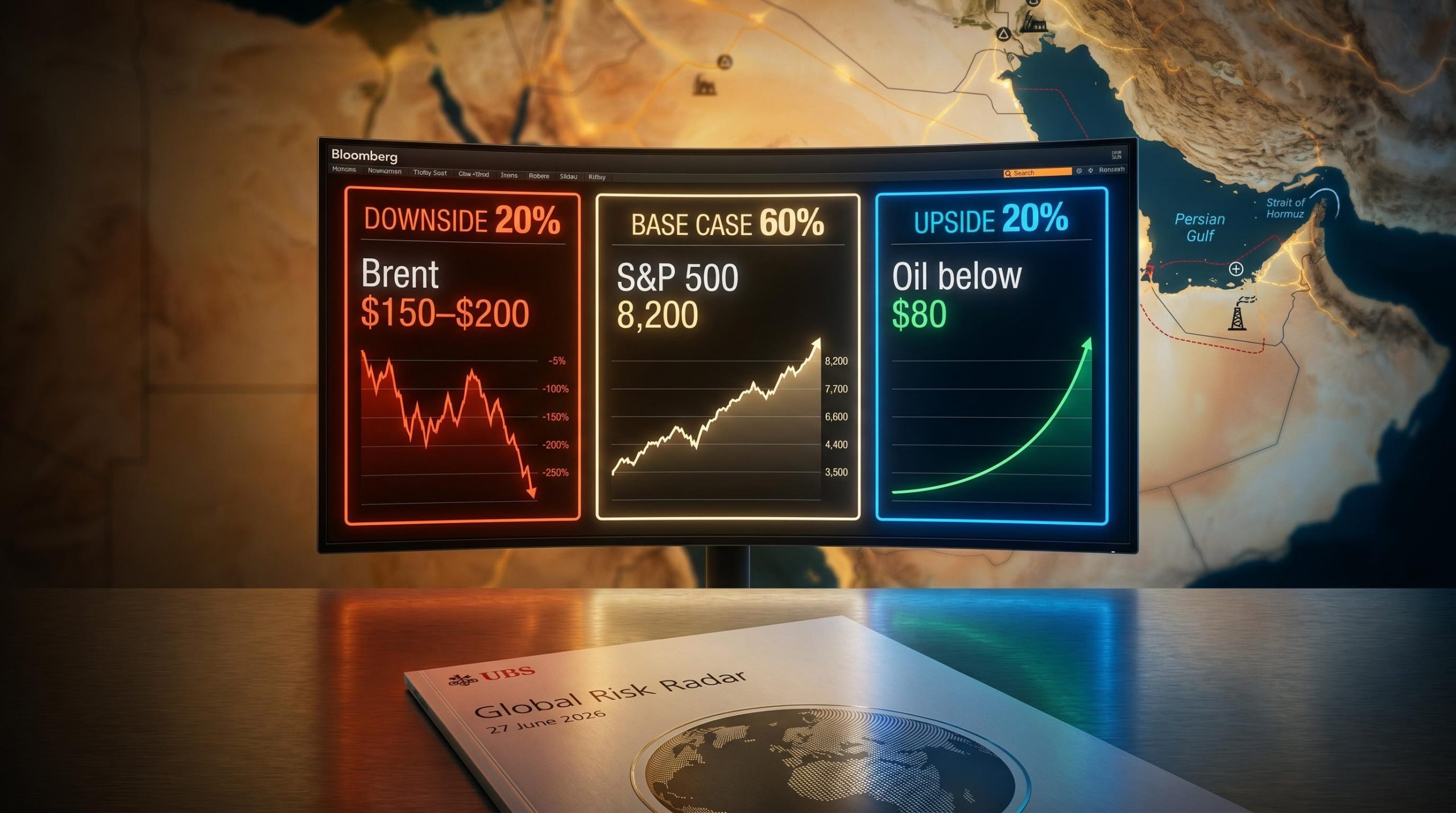

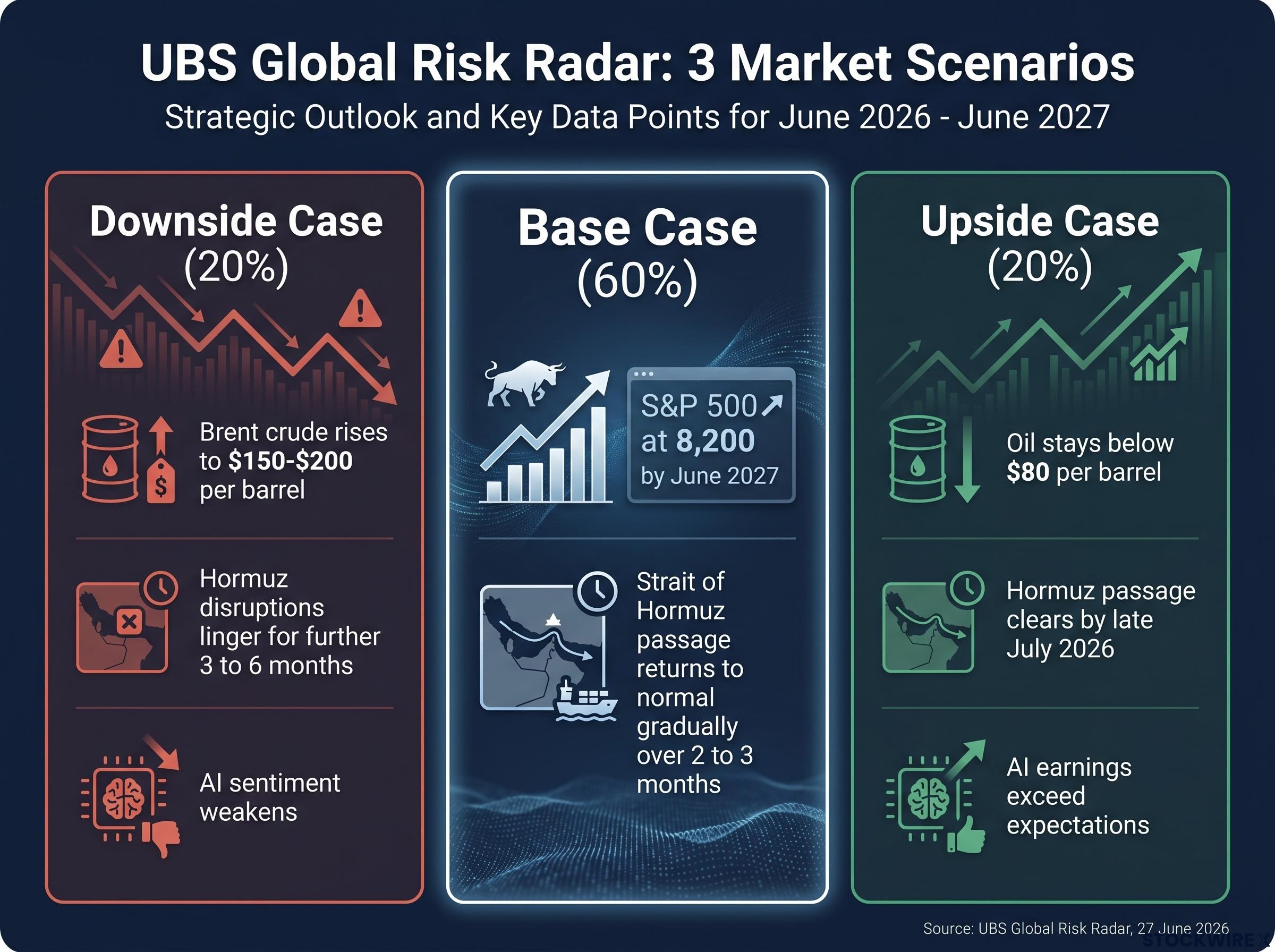

UBS assigns a 60% probability to its base case, 20% to the downside, and 20% to the upside.

The Strait of Hormuz is the specific geopolitical variable driving the divergence between all three scenarios. How quickly shipping through the strait normalises, or fails to, is the single factor that separates a contained recovery from an energy shock.

That 40% combined probability assigned to outcomes materially worse or better than the base case is the number worth sitting with. It means betting entirely on the central view carries real risk.

UBS projects the S&P 500 rising to 8,200 by June 2027 under the base case, the scenario it weights at 60% probability. That target represents meaningful upside from current levels. It is also contingent on a specific set of conditions all holding simultaneously.

Four things need to break in investors’ favour for the base case to materialise:

Under this scenario, oil prices stay contained and declining bond yields improve the investment case for fixed income. The base case is constructive, but the Strait normalisation timeline is the condition worth watching most closely. UBS itself assigns only moderate confidence to that specific geopolitical assumption, which means the scenario most investors will default to assuming is more conditional than it first appears.

The base case assumption of gradual Hormuz normalisation sits inside a broader pattern of geopolitical risk pricing that markets have applied consistently across recent conflict episodes, where forward earnings expectations, not headline severity, drive index direction.

The downside scenario activates on two conditions arriving together:

Under this scenario, Brent crude rises to $150-$200 per barrel.

The oil price is not abstract. At those levels, consumer spending compresses, transport costs cascade through supply chains, and central banks face a stagflationary bind where cutting rates to support growth risks fuelling the inflation an energy shock creates. UBS pairs this with a hard landing scenario in which deteriorating labour markets and trade tensions compound the energy shock, producing double-digit equity market declines.

At those price levels, the stagflationary bind UBS describes connects directly to the IEA’s characterisation of oil as a structural inflation risk rather than a transient spike, a framing that explains why central banks would face simultaneous pressure to tighten against energy-driven price rises and ease to offset demand destruction.

A 20% probability is not negligible. It is roughly the same odds as rolling a one or two on a six-sided die. If your portfolio has no defensive positioning for this outcome, you are implicitly treating it as impossible. UBS is telling you it is not.

The upside case rests on two specific triggers:

Under this scenario, oil stays below $80 per barrel, easing cost pressure for consumers and businesses and supporting broader equity valuations.

UBS is explicit, however, that the upside scenario is not an invitation to drop risk management. The bank warns that bubble risks in parts of AI and tech are real, and that chasing the upside without hedging is a structural error even if this outcome materialises. A 20% probability is the same weight as the downside case, which means the discipline required is identical in both directions.

The AI monetisation risks UBS flags as a downside trigger extend beyond sentiment: BCA Research’s Peter Berezin has identified structural airline-like economics in foundation model providers, where near-zero switching costs and commoditised output make the translation from capex to earnings structurally difficult regardless of technology adoption rates.

UBS identifies the sectors most likely to benefit under rapid normalisation: technology and the broader AI value chain, health care, selected cyclicals, banks, utilities, and broad commodities. The recommendation is to spread exposure across the AI value chain (infrastructure, software, semiconductors, industrials) rather than concentrating in a handful of megacap leaders.

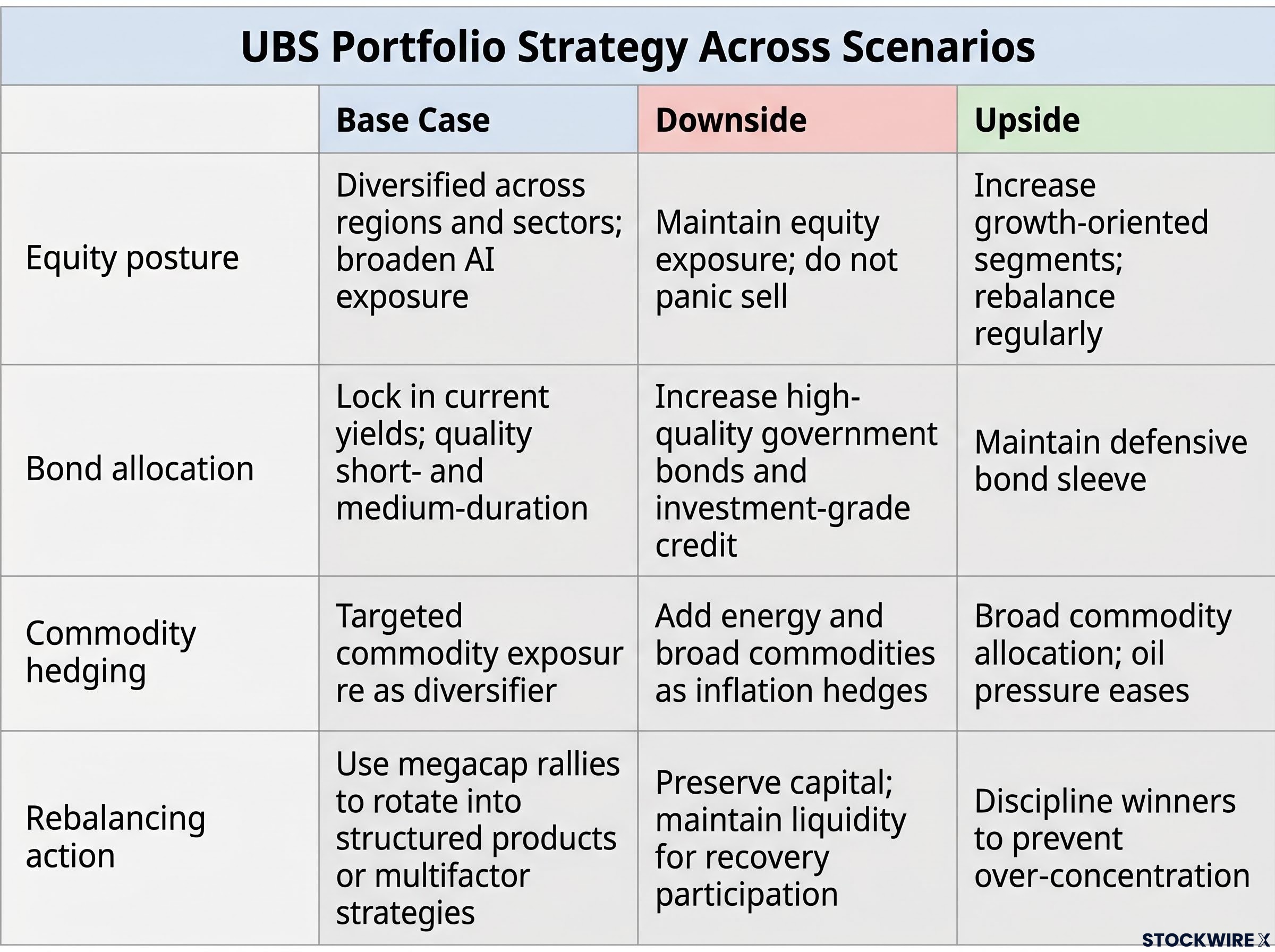

The most striking feature of the UBS framework is how little the portfolio prescription changes across the three scenarios. The degree of emphasis shifts; the structure does not.

| Portfolio Element | Base Case | Downside | Upside |

|---|---|---|---|

| Equity posture | Diversified across regions and sectors; broaden AI exposure | Maintain equity exposure; do not panic sell | Increase growth-oriented segments; rebalance regularly |

| Bond allocation | Lock in current yields; quality short- and medium-duration | Increase high-quality government bonds and investment-grade credit | Maintain defensive bond sleeve |

| Commodity hedging | Targeted commodity exposure as diversifier | Add energy and broad commodities as inflation hedges | Broad commodity allocation; oil pressure eases |

| Rebalancing action | Use megacap rallies to rotate into structured products or multifactor strategies | Preserve capital; maintain liquidity for recovery participation | Discipline winners to prevent over-concentration |

That convergence is the report’s most actionable signal. UBS is effectively saying the structure of a resilient portfolio does not change much depending on which scenario plays out.

The geographic diversification recommendations are specific: Japan, emerging markets, China (including tech), global health care, Switzerland, and European consumer discretionary, all positioned as alternatives to concentrated U.S. megacap tech exposure. Within AI, the recommendation is to broaden across infrastructure, software, semiconductors, and industrials rather than concentrating in a handful of leaders.

The practical question from the UBS framework is not whether the S&P 500 hits 8,200. It is whether your current asset mix would meaningfully underperform in the 40% of scenarios where the base case does not play out.

UBS identifies two time-sensitive portfolio actions under the base case:

The Strait of Hormuz timeline is the near-term variable to watch. The base case assumes normalisation within two to three months; the upside case prices it by late July 2026. If neither materialises, the downside scenario’s conditions start activating.

UBS’s core argument is that portfolio adaptability has more value than predictive accuracy in the current environment.

That framing is worth taking seriously. Diversification across equities, bonds, and currencies reduces risk across market conditions, and the bank’s scenario framework is designed as a stress-test tool rather than a market call. The question is not which path to bet on; it is whether your portfolio could survive the two you are not expecting.

For investors wanting a structured framework to operationalise the multi-scenario approach UBS recommends, our comprehensive walkthrough of the All Weather Portfolio explains how Ray Dalio’s four-quadrant risk balancing addresses rising and falling growth and inflation simultaneously, covering both the original weights and modern refinements for today’s higher real-yield environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

The UBS Global Risk Radar is a scenario framework published on 27 June 2026 that assigns explicit probabilities to three market outcomes: a 60% base case, a 20% downside, and a 20% upside, built around four unforecastable variables: geopolitics, inflation, interest rates, and AI monetisation.

UBS projects the S&P 500 reaching 8,200 by June 2027 under its base case scenario, contingent on resilient U.S. growth, sustained AI capital expenditure, solid corporate earnings, and a gradual normalisation of Strait of Hormuz shipping within two to three months of the report's publication.

In the downside scenario, which UBS weights at 20% probability, Brent crude rises to $150-$200 per barrel driven by prolonged Hormuz oil flow disruptions lasting three to six months, creating a stagflationary bind for central banks and double-digit equity market declines.

UBS's key finding is that the portfolio structure changes very little across all three scenarios: diversified equities across regions and sectors, quality bonds to lock in current yields, commodity exposure as an inflation hedge, and regular rebalancing to prevent over-concentration in megacap tech leaders.

The Strait of Hormuz is the single variable that separates all three UBS scenarios: rapid normalisation by late July 2026 triggers the upside case, gradual normalisation over two to three months supports the base case, and disruptions lingering three to six months activate the downside case with oil potentially reaching $200 per barrel.