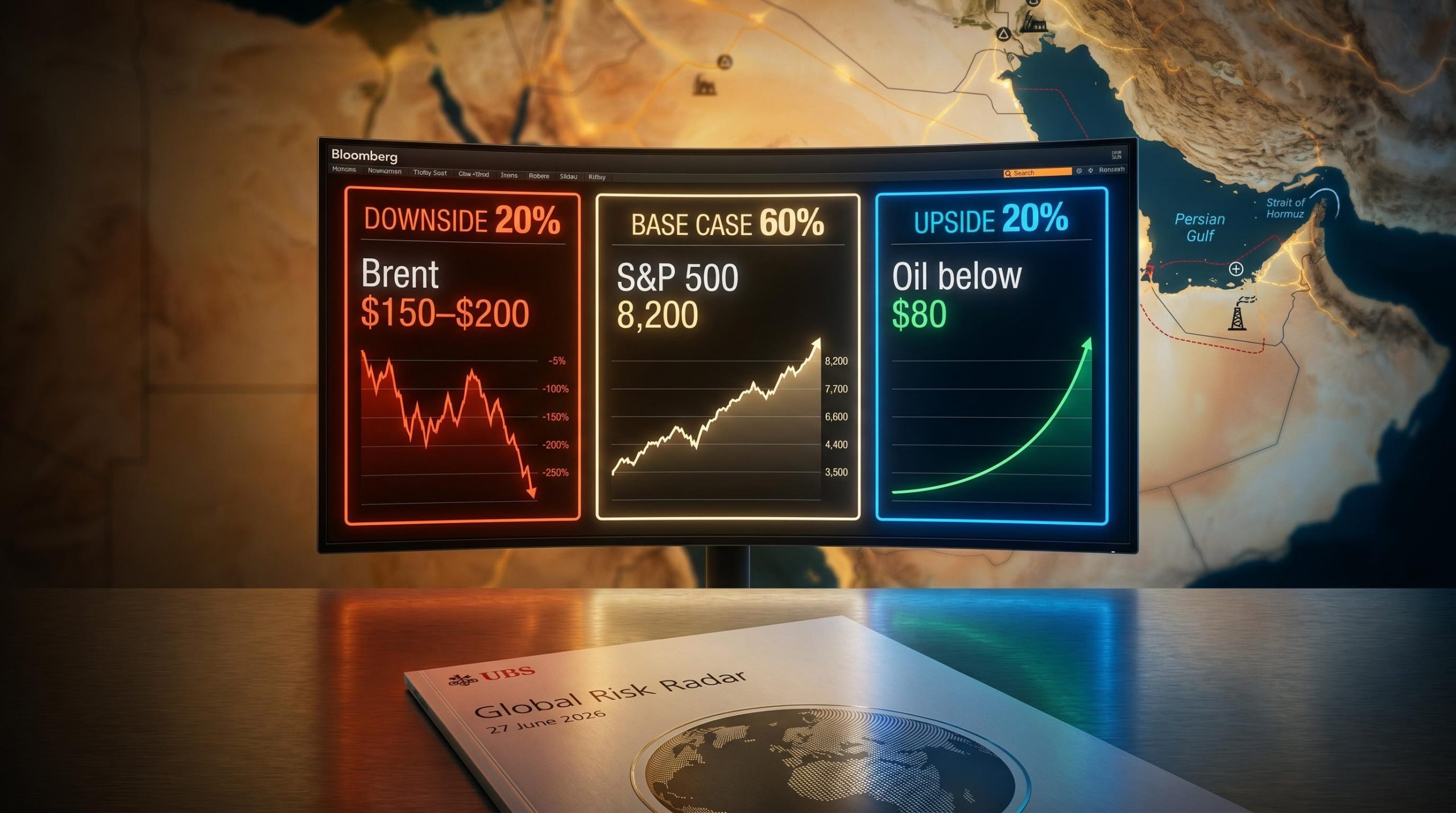

UBS Maps 3 Market Paths From $200 Oil to S&P 500 at 8,200

37 mins ago

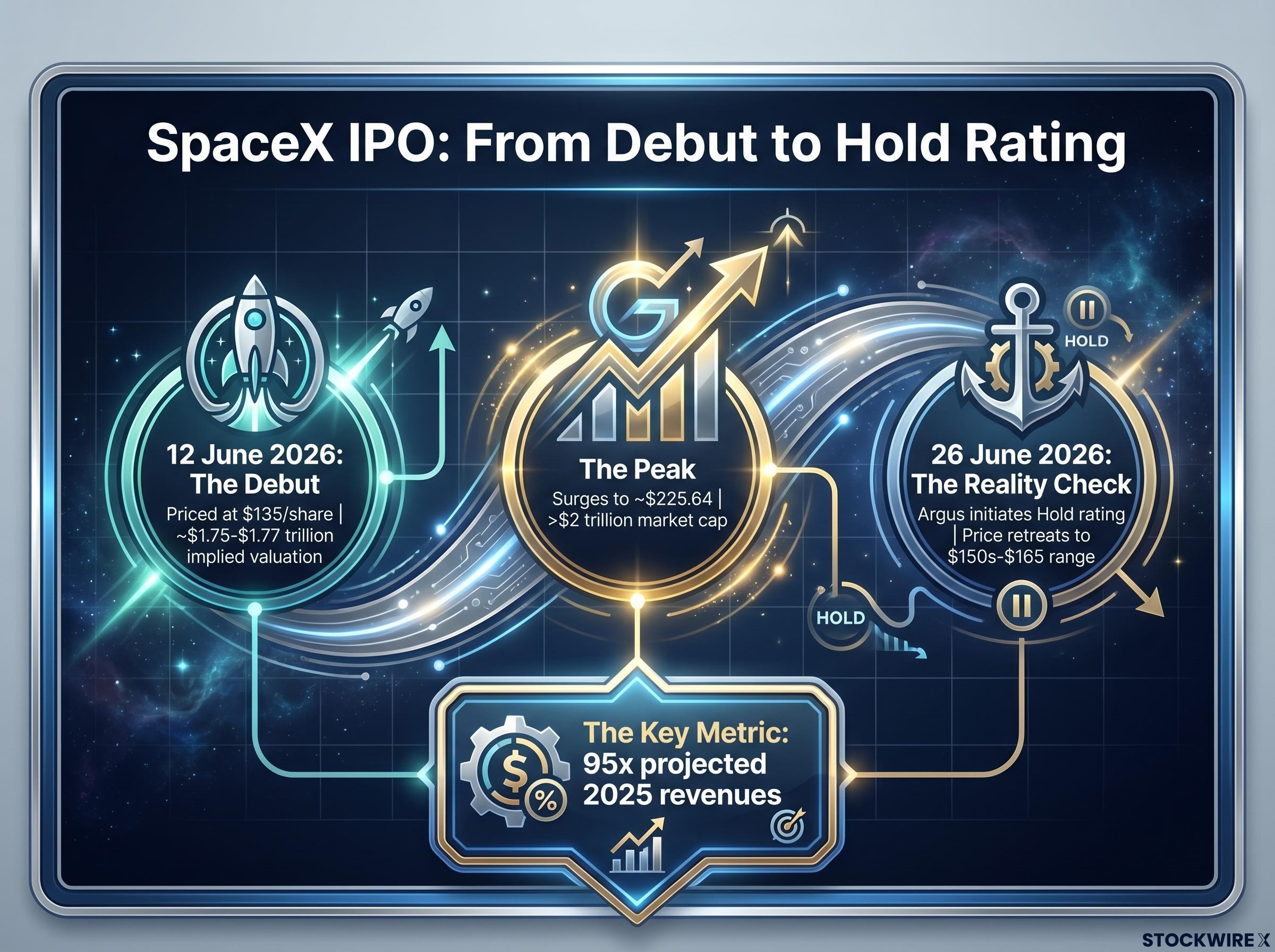

The largest IPO in history arrived on 12 June 2026, and the first major institutional verdict was not a buy. Fourteen days after SpaceX priced at $135 a share, Argus Research initiated coverage with a Hold rating. The number that explains everything: a price-to-sales multiple of roughly 95x projected 2025 revenues.

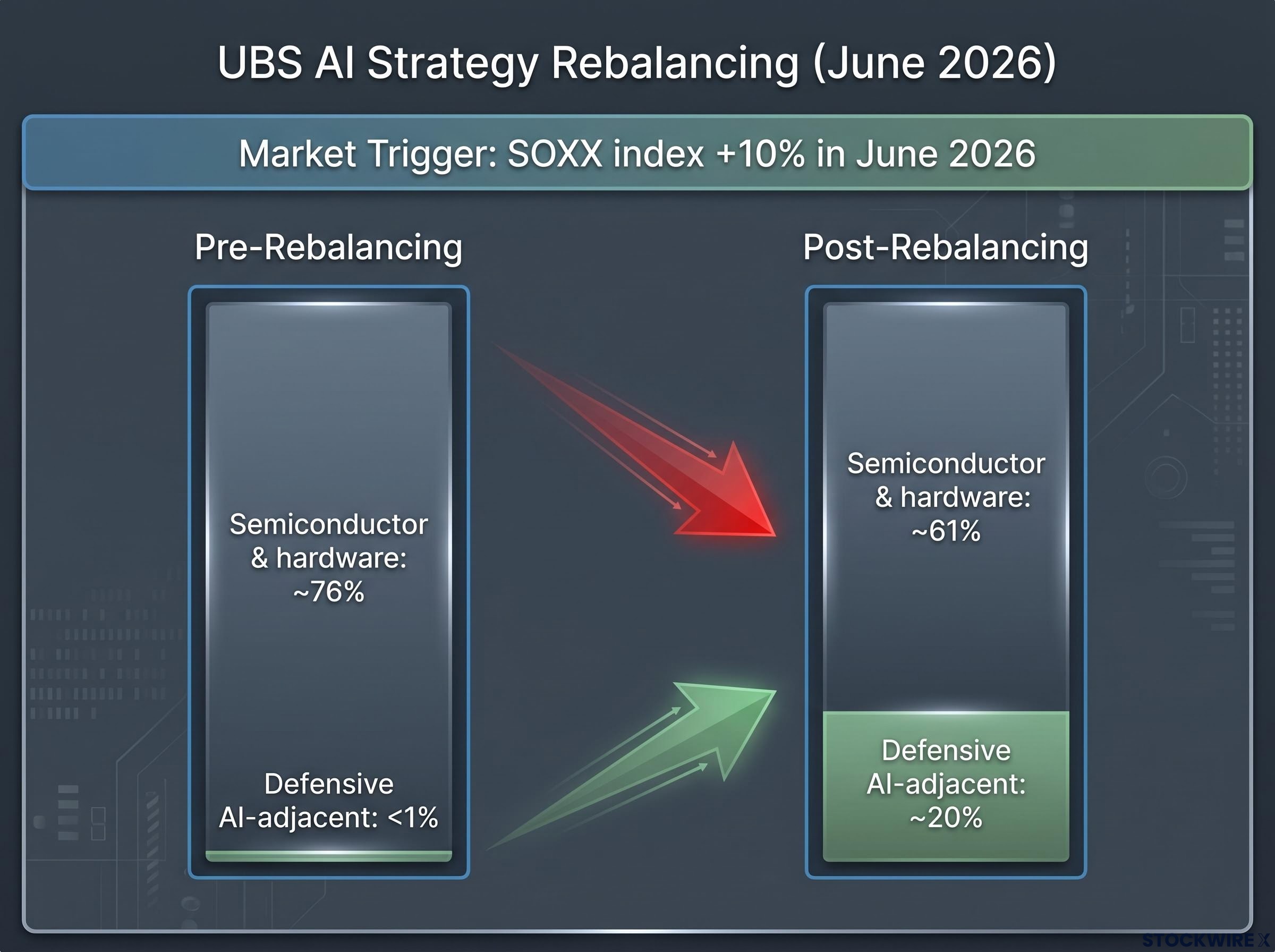

That caution was not confined to a single stock. The same AI-fuelled enthusiasm lifting space infrastructure valuations also pushed the SOXX semiconductor index up approximately 10% in a single month, prompting UBS to cut its hardware allocation by 15 percentage points in response. Two major institutions, two different asset classes, one shared discipline: price matters even when the business story is genuinely compelling.

Here is the analytical lens both moves share, with the specific numbers and named decisions behind them, so you can apply the same framework the next time a transformational story meets a stretched valuation.

SpaceX priced its IPO at $135 per share on 12 June 2026, selling approximately 555.6 million shares and raising roughly $75 billion in base proceeds. When the likely overallotment exercise is included, total proceeds reached around $85.7 billion, with the deal placing the company’s implied valuation somewhere in the region of $1.75-$1.77 trillion and securing its place as the biggest public listing ever recorded.

| Metric | Value |

|---|---|

| IPO price | $135 per share |

| Shares sold | ~555.6 million |

| Base proceeds | ~$75 billion |

| Implied valuation | ~$1.75-$1.77 trillion |

| Post-IPO peak price | ~$225.64 |

| Peak gain vs. IPO price | ~67% |

| Market cap at peak | >$2 trillion |

| Post-peak trading range | ~$150s-$165 |

The debut was explosive. The stock surged to around $225.64, representing a gain of approximately 67% over the offer price and carrying the market capitalisation above $2 trillion at its high. The retreat followed swiftly. When Argus initiated coverage on 26 June, the shares had pulled back into the $150s-$165 range, holding roughly 10% above the offering price yet sitting well over 25-30% below where they had peaked.

Two structural forces amplified that volatility. First, the free float was small relative to the total market capitalisation, meaning relatively modest trading volumes could move the stock sharply in either direction. Second, strong index-inclusion mechanics and elevated retail participation created buying pressure in the first days that was always likely to fade. With lockup expirations approaching, further supply is set to enter the market. The first weeks of a mega-IPO are often more noise than signal, and SpaceX has been no exception.

Argus Research analyst Steve Silver initiated coverage on 26 June 2026 with a Hold rating, and the core of his argument was arithmetic. At the time of his note, SpaceX traded at approximately 95x projected 2025 revenues. A price-to-sales multiple that high, on a company that is not yet consistently profitable and whose revenue base is smaller than many comparably valued peers, leaves almost no room for anything to go wrong.

Silver characterised SpaceX as a company that blends the characteristics of a mature infrastructure business with those of a venture-stage growth investment. That hybrid identity is part of the appeal, but it also means the valuation will likely take years to normalise even under optimistic assumptions.

Argus’s core characterisation: SpaceX operates with the profile of an established infrastructure provider grafted onto a high-growth venture investment. At approximately 95x forward sales, the gap between today’s valuation and what would be considered a more normalised multiple is likely to take several years to close, even under conditions of strong execution.

At 95x sales, the investor is not buying the current business. They are buying a very specific forecast of how much that business will grow, and whether that forecast proves right is the central risk embedded in the price.

Argus identified two circumstances that could warrant an upgrade:

Both conditions reinforce the same point. The Hold is about price, not about the company’s quality.

Price-to-sales is a valuation metric that compares a company’s market capitalisation (its total stock market value) to its annual revenue. It is most commonly used when a company has minimal or negative earnings, making traditional profit-based measures like price-to-earnings ratios unreliable.

The price-to-sales ratio is the single metric doing the most analytical work in the Argus note, yet it is also one of the most misread tools in retail investing: a discounted multiple is a starting signal for deeper investigation, not a standalone buy verdict, and a stretched multiple is an instruction to examine what growth rate the market has already priced in, not an automatic sell.

Here is how to read the ratio in three steps:

At approximately $1.75 trillion implied valuation on a revenue base that Argus described as smaller than many peers trading at comparable or lower multiples, SpaceX’s 95x forward sales multiple implies years of compounding revenue growth at rates few companies in history have sustained. The company is not yet consistently profitable, which means the path from current revenue to the earnings that would justify this valuation is long and uncertain.

This is not a dismissal of the business. It is a mathematical observation: at 95x, the market has already priced in an extraordinary amount of success. What the investor is paying for is not today’s revenue but a specific trajectory of future revenue, and the gap between “good” and “good enough to justify 95x” is narrower than most people assume.

After Micron earnings sparked a move of approximately 4% in the SOXX semiconductor index within a single session in June 2026, the index went on to add around 10% across the month as a whole. UBS responded by cutting its combined semiconductor and hardware weighting within its AI strategy from around 76% down to roughly 61%, a reduction of 15 percentage points, while simultaneously building its defensive AI-adjacent allocation from below 1% to around 20%.

That is a substantial repositioning in a single month. UBS did not exit the semiconductor trade; it managed the position risk within it.

The AI capex lag between infrastructure investment and verifiable revenue generation is the structural tension behind the UBS rebalancing: Morningstar analysts have identified an 18-24 month delay between hyperscaler spending commitments and the supplier-level revenues that would justify the multiples already priced into the SOXX.

| Allocation category | Pre-rebalancing weight | Post-rebalancing weight |

|---|---|---|

| Semiconductor and hardware | ~76% | ~61% |

| Defensive AI-adjacent | <1% | ~20% |

| Magnificent Seven weight | ~18% (substantial underweight) | |

The selling was focused on AI supply chain companies at the smaller and mid-cap end of the market, where valuations had stretched the furthest, spanning names across:

The defensive capital went into data centre operators, telecommunications companies, and select payments firms characterised by prudent balance sheets and stable dividends. These names provide exposure to the AI ecosystem without the full valuation risk of high-beta hardware stocks. Moving roughly 20% of a strategy into defensive names after a 10% sector rally in a single month is not a bearish call on AI. It is a disciplined acknowledgment that when prices run fast, valuation-adjusted risk changes, and position sizing should change with it.

Within its semiconductor book, UBS maintained concentrated positions in three names it continues to back with conviction:

The common logic is clear: these are established, supply-chain-critical companies with diversified customer bases, not speculative mid-cap niche suppliers riding a single product cycle. UBS’s broader House View continues to position AI and technology as key sources of equity market upside, with medium-term demand supported by cloud acceleration and agentic AI workload growth. However, tech valuations sit above long-term averages, requiring selectivity. UBS recommends diversifying across the enabling, intelligence, and application layers of the AI value chain rather than concentrating in any single segment.

Semiconductor valuation dispersion in 2026 is wider than at any point in the dot-com era: Micron trades below 9x forward earnings while Intel sits at approximately 101x, meaning a sector-level bubble verdict obscures a stock-by-stock reality where some names are historically cheap and others are historically expensive simultaneously.

The risk UBS named explicitly: a sharp fall in the share prices of major hyperscaler companies could lead management teams to scale back their capital expenditure programmes going forward. That capex reduction would propagate rapidly through the entire AI supply chain, hitting the most richly valued, least diversified names hardest.

This is the lever worth watching most closely. If Amazon, Microsoft, Google, or Meta signal reduced AI infrastructure investment in upcoming earnings, the effect is not limited to their own share prices. It compresses forward revenue expectations across every supplier in the chain simultaneously.

The Argus Hold on SpaceX and the UBS semiconductor trim look like unrelated moves. One is a single-stock valuation call on a space infrastructure company. The other is a portfolio rotation within AI hardware. But the discipline underneath is identical: both represent institutional capital separating long-term business quality from near-term valuation risk.

That distinction is the most portable tool in this analysis. Any time you evaluate a high-growth position, three questions do the heavy lifting:

Three leading indicators are worth monitoring as the AI and space infrastructure investment narratives evolve:

These are forward signal anchors, not predictions. The point is not to forecast what will happen, but to know which data points change the picture first.

Institutional crowding signals provide independent corroboration for the UBS trim: the June 2026 Bank of America Global Fund Manager Survey recorded 80% of managers naming long global semiconductors as the most crowded trade in the survey’s history, a concentration level that escalated from roughly 24% in April to 80% in June with no historical precedent.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding SpaceX’s revenue trajectory, AI sector performance, and institutional strategy positioning are speculative and subject to change based on market developments and company performance.

The price-to-sales ratio compares a company's total market value to its annual revenue, and at approximately 95x projected 2025 revenues, SpaceX's multiple signals that investors are paying a very high price for expected future growth rather than current earnings power, leaving almost no margin for the business to disappoint.

Argus analyst Steve Silver issued a Hold on 26 June 2026 because SpaceX was trading at roughly 95x forward sales on a company that is not yet consistently profitable, meaning the valuation already prices in years of exceptional revenue growth and offers little buffer if execution falls short of those projections.

SpaceX surged roughly 67% from its $135 offer price to a peak of approximately $225.64, briefly pushing its market cap above $2 trillion, before pulling back into the $150s-$165 range by the time Argus initiated coverage on 26 June 2026.

UBS reduced its combined semiconductor and hardware weighting by 15 percentage points, from roughly 76% to 61%, because the rapid price appreciation outpaced verifiable revenue generation, with Morningstar analysts estimating an 18-24 month lag between hyperscaler spending commitments and the supplier-level revenues that would justify stretched multiples.

The three key signals to watch are hyperscaler capex guidance from major cloud platforms (any downward revision hits the entire AI supply chain), SpaceX's revenue growth relative to its 95x multiple, and institutional AI strategy weightings from firms like UBS, where further trimming would signal broadening valuation concern rather than isolated caution.