May PCE Inflation Hits Target, Keeping Fed on Hold

54 mins ago

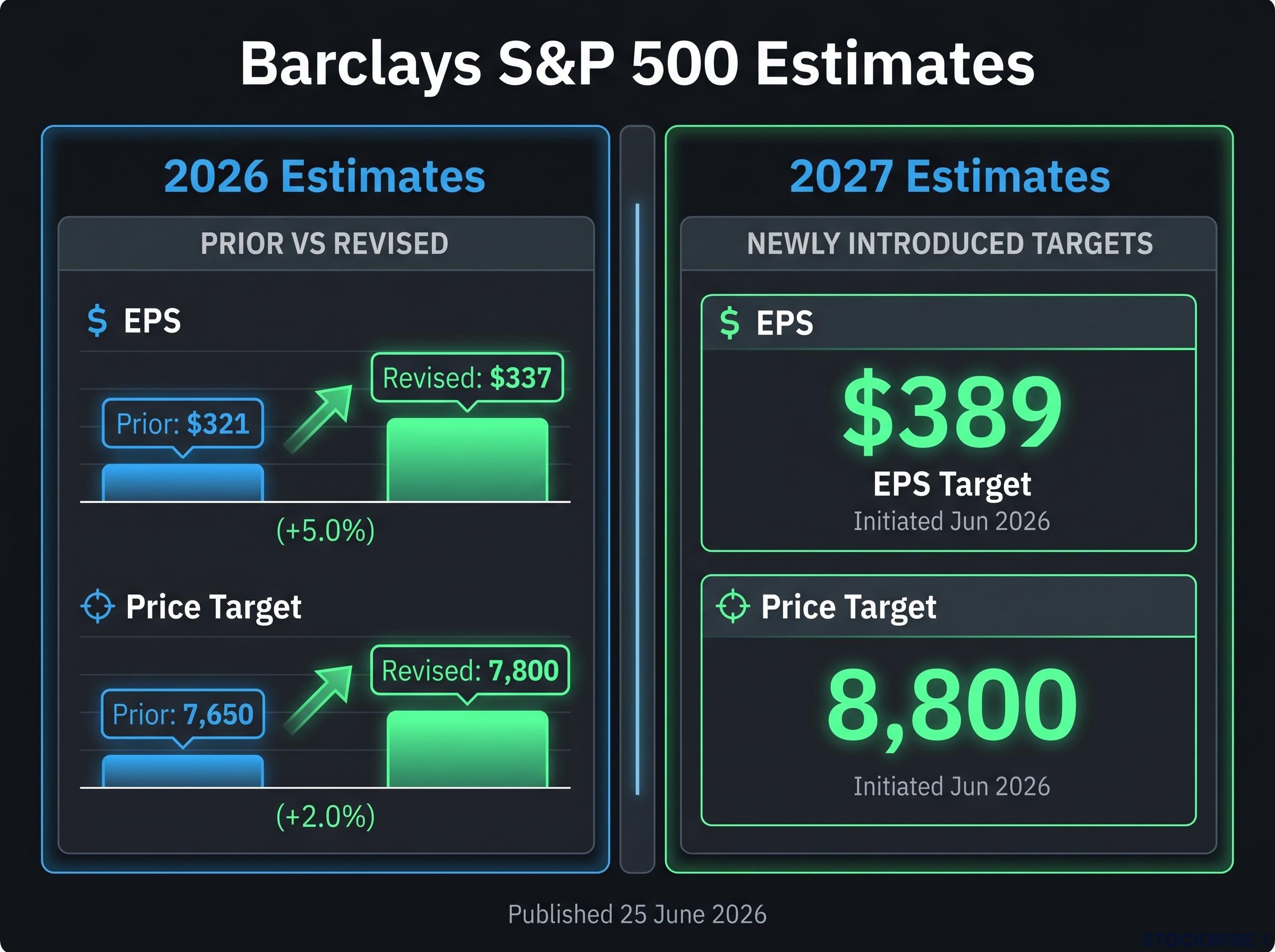

Barclays just raised its S&P 500 year-end target to 7,800 and lifted its 2026 earnings per share (EPS) estimate to $337, publishing its Q3 Global Outlook today, 25 June 2026. The revised figures, up from a prior target of 7,650 and an EPS forecast of $321, represent one of the more aggressive institutional calls heading into the second half of the year.

The timing matters. Investors entering Q3 are grappling with stretched valuations and a genuine question about whether the AI investment cycle is producing durable earnings or inflated expectations. A major global bank putting specific upward revisions on the table gives both sides of that debate a concrete number to argue against.

Here is what Barclays actually says, sector by sector and market by market, so you can assess whether the bank’s logic holds against your own portfolio assumptions heading into H2 2026.

Valuations are elevated. Barclays knows it. The bank’s Q3 outlook, authored by Ajay Rajadhyaksha, Global Chairman of Research, explicitly acknowledges that multiples are stretched. The bank’s continued preference for equities over bonds and cash does not ignore this reality; instead, it depends entirely on one condition holding true: that corporate earnings keep delivering above what analysts expect.

That condition is doing all the structural work. Barclays does not cite macro stability, geopolitical calm, or rate-cut timing as requirements for the bull case to hold. The bank names one exit trigger, and only one.

Barclays’ singular trigger to abandon the equity overweight: a confirmed collapse in earnings growth. Not valuation expansion, not macro volatility, and not geopolitical noise.

What that tells you is exactly which signal to monitor. If earnings momentum holds, the current multiples are sustainable in Barclays’ framing. If it breaks, the entire edifice shifts. Every other market wobble between now and year-end is, in the bank’s view, noise.

HSBC’s 7,650 target, set in early May 2026, identified the 10-year Treasury yield crossing 4.5% as the point at which AI capex rate sensitivity peaks, a rate-dependent framing that stands in contrast to Barclays’ singular focus on earnings delivery as the only exit trigger for the equity overweight.

Conviction is slightly lower than Q2 2026 because bargains are fewer, but the fundamental rationale remains intact. The revised numbers tell the story:

| Metric | Prior estimate | Revised estimate |

|---|---|---|

| 2026 EPS | $321 | $337 |

| 2026 price target | 7,650 | 7,800 |

| 2027 EPS | N/A | $389 |

| 2027 price target | N/A | 8,800 |

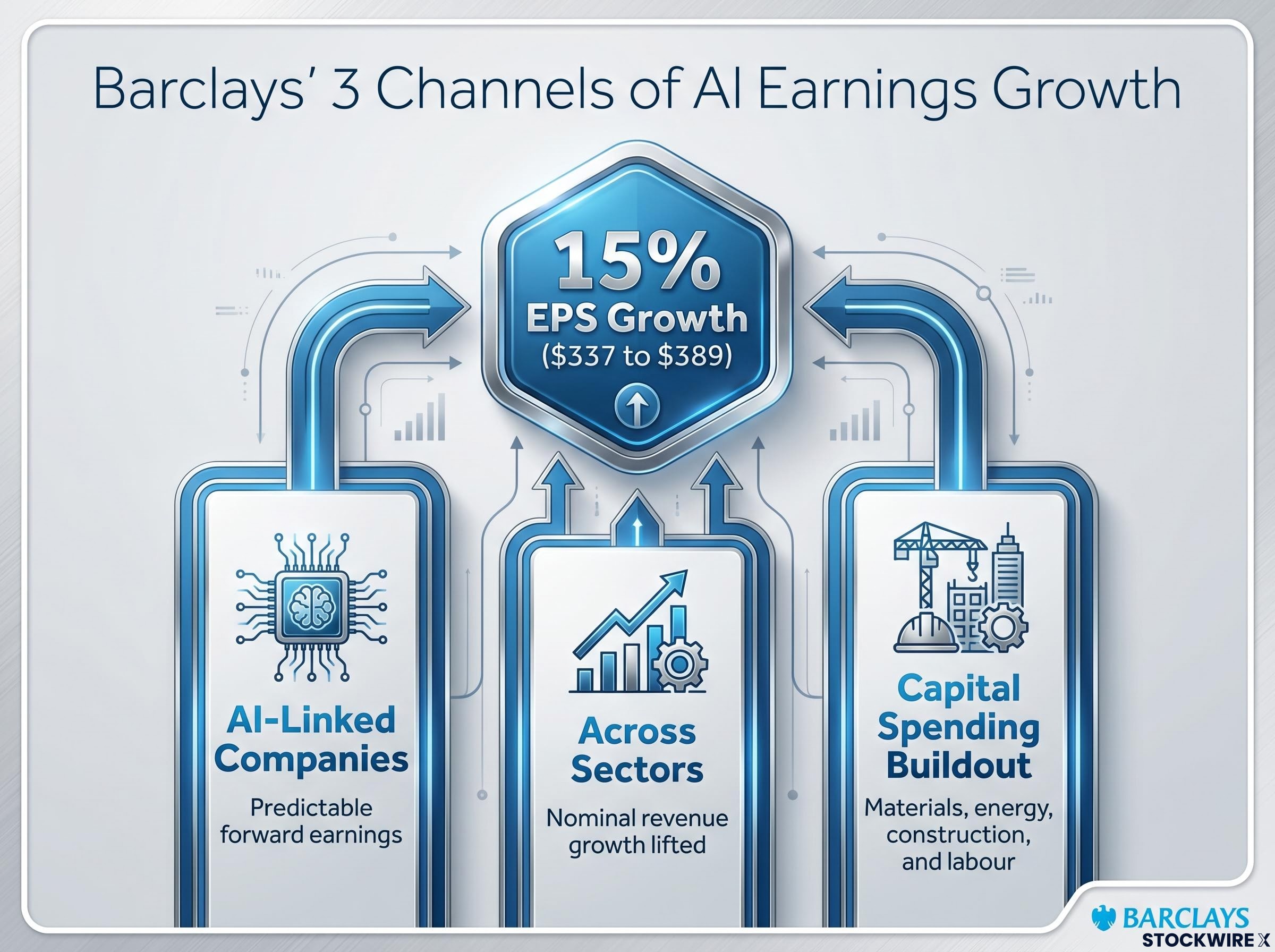

The 2027 EPS target of $389 sits approximately 15% above the 2026 estimate of $337. That is a large gap to close in twelve months, and Barclays does not hand-wave it. The bank identifies three specific channels through which AI is driving earnings growth across the market, not just within technology names:

The three-channel framework is the most important structural detail in the outlook. It tells you that Barclays is not making a concentrated tech bet. The bank is making a macro argument: AI is reflationary for broad corporate earnings. If that reading is correct, portfolio construction tilts toward diversified AI-adjacent exposure rather than a narrow allocation to semiconductor and software names.

AI hyperscaler capex projections were revised upward by $80 billion in a single quarter to $751 billion in Goldman Sachs’ Q1 2026 analysis, with Amazon, Alphabet, Meta, and Microsoft collectively delivering 61% profit growth, the foundational earnings data that major institutional strategists including Barclays are now extrapolating forward.

That distinction matters for how aggressively you weight pure tech versus the industrial and utility names that benefit from channel three.

Barclays’ sector positioning for H2 2026 reads as a unified AI-adjacency theme rather than a collection of unrelated calls. The four overweight sectors all connect, directly or indirectly, to the AI capital deployment cycle.

| Sector | Barclays rating | Key rationale |

|---|---|---|

| Technology | Overweight | Core beneficiary of AI-driven earnings visibility |

| Media and Telecoms | Overweight | AI-linked demand and infrastructure exposure |

| Industrials | Overweight | Capital spending tied to AI infrastructure buildout |

| Utilities | Overweight | Data-centre power demand growth |

| Financials | Neutral (downgraded) | Private credit risk; AI margin compression |

| Consumer | Underweight | Deteriorating household spending capacity in H2 |

| Healthcare | Neutral (upgraded) | Reduced concern; not a high-conviction overweight |

The two calls worth pausing on are the counterintuitive ones.

Healthcare’s upgrade to neutral from a previously more negative stance signals that whatever was worrying Barclays earlier has moderated. It is a reduced-concern signal, not a conviction buy.

The Financials downgrade is sharper and more actionable.

Why Barclays downgraded Financials to neutral: Mounting private credit exposure alongside AI-driven pressure on margins in trading, wealth management, and operations. The bank sees AI not as a tailwind for financial institutions but as a force that compresses their margins.

If that reading is correct, investors with heavy financial sector exposure may be holding a structural headwind rather than a cyclical dip. The consumer underweight, meanwhile, reflects Barclays’ view that accumulating pressures on household spending power are likely to intensify through the back half of 2026, making consumer-facing names the clearest sector to avoid.

In Barclays’ Q3 outlook, Japan emerges as its preferred destination for investors seeking international equity exposure beyond the U.S. The call rests on two independent pillars, which is what makes it structurally resilient rather than dependent on any single catalyst:

Two concrete mechanisms underpin the governance reform story: companies are returning more capital through dividends, and the long-standing practice of holding cross-stakes in peer companies is gradually being dismantled. Cross-shareholdings (where companies hold stakes in each other primarily for relationship purposes rather than return on capital) have historically suppressed return on equity across Japanese corporates. Their unwinding improves capital efficiency directly.

Barclays frames this as what distinguishes the Japan call from a momentum trade. Even if the AI investment cycle were to moderate, the governance reform story supports Japanese equities on its own terms.

For U.S.-based investors evaluating international allocation, the dual thesis changes the risk profile materially. The case for holding Japanese equities does not collapse if semiconductor stocks correct, a meaningfully different proposition than a pure Taiwan or South Korea play.

Japan’s equity performance in 2026 has run well ahead of the bearish narrative that dominated financial media earlier in the year, with Q1 GDP growth of 2.1% annualised driven by private consumption and business investment rather than government stimulus, providing independent macro support for Barclays’ preference for the Nikkei over other international developed markets.

Barclays’ Q3 outlook distils into four actionable positions for H2 2026, with a secondary horizon extending through 2027:

The variable to watch is singular.

The monitoring trigger: earnings growth, specifically whether AI-driven earnings momentum continues to print above consensus in coming quarters. If earnings growth collapses materially, that is the single development that would prompt a reassessment of the entire call.

The reduced conviction language deserves attention. Barclays is not reversing its equity overweight, but the bank is telling you that bargains are fewer than they were in Q2 2026. Investors who implement the call at maximum aggression without acknowledging that nuance are taking on more risk than the bank itself is underwriting.

The entire Barclays outlook, from the 7,800 index target to the sector overweights to the Japan call, is downstream of one variable: whether AI-driven earnings growth delivers. The 2026 EPS target of $337 and the 2027 target of $389 are the numerical stakes.

The near-term proving ground arrives next month. Q2 2026 earnings season begins in July 2026, and results from AI-exposed companies will be the first concrete test of whether the momentum underpinning this outlook is holding. If those numbers print above consensus, the path to 7,800 stays open. If they disappoint, the bank’s own framework suggests reassessment.

For investors who want to apply active scrutiny when Q2 2026 results arrive in July, our full explainer on reading earnings reports walks through a seven-step framework covering revenue quality, GAAP versus non-GAAP gaps, free cash flow alignment, and forward guidance signals to distinguish genuine momentum from manufactured beats.

Barclays has told you exactly what to watch. The question is whether the earnings show up.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Barclays raised its S&P 500 year-end target to 7,800 in its Q3 Global Outlook published on 25 June 2026, up from a prior target of 7,650, alongside a revised 2026 EPS estimate of $337.

Barclays lifted its target because AI-driven earnings growth is producing stronger and more predictable forward earnings across multiple sectors, not just technology, with the bank projecting EPS reaching $389 by 2027.

Barclays has named one specific exit trigger: a confirmed collapse in earnings growth. The bank explicitly excludes elevated valuations, macro volatility, and geopolitical noise as sufficient reasons to reduce its equity overweight.

Barclays is overweight Technology, Media and Telecoms, Industrials, and Utilities, all connected to the AI capital deployment cycle, while downgrading Financials to neutral and underweighting Consumer on deteriorating household spending capacity.

Barclays favours Japan because the Nikkei 225 offers broader sectoral AI exposure than semiconductor-heavy South Korean and Taiwanese benchmarks, and ongoing corporate governance reforms including increased dividends and the unwinding of cross-shareholdings provide an independent return driver.