Investors entered 2026 expecting the Reserve Bank of Australia to start cutting. Instead, the RBA cash rate climbed to 4.35% across three consecutive hikes in the first half of the year, and the easing cycle that was supposed to define the year never arrived.

The analytical interest now sits in the genuine ambiguity of what comes next. This is not a story of rates peaking and relief on the way. The RBA’s own revised forecasts describe a stagflationary configuration: growth slowing to 1.3% while inflation stays stuck well above the 2-3% target band, with no return to target expected before 2028. The central bank is caught between prices that refuse to behave and an economy visibly losing momentum.

Here is the read on the RBA’s actual decision logic, the specific conditions that could force another hike, and what this higher-for-longer environment means for every Australian holding rate-sensitive assets.

How three hikes reshaped Australia’s rate landscape in 2026

The consensus at the start of the year was confident, and not without reason. Global central banks were edging toward easing, Australian inflation had moderated from its peak, and futures pricing pointed firmly toward cuts. The logic was straightforward: the tightening cycle had done its work, and the next move was down.

Then the data arrived, and it kept arriving in the wrong direction. Three categories of incoming evidence repeatedly overrode the expected pivot:

- Services inflation remained sticky, refusing to moderate at the pace the RBA’s models projected

- Wages growth stayed firm, sustained by a labour market that loosened far more slowly than anticipated

- Domestic demand proved more resilient than rate-sensitive forecasts implied, with household spending absorbing higher rates without the sharp pullback that would have justified easing

Each time a cut appeared imminent, one or more of these data inputs forced the RBA to act in the opposite direction. The result was not a single abrupt shift but a pattern: three separate hikes across H1 2026, each one a response to the same stubborn reality that inflation was not falling fast enough.

The third consecutive hike carried a specific signal beyond the rate level itself: an 8-1 board vote that revealed the threshold between hiking and holding was narrower than the headline margin implied, with forward guidance language that preserved full optionality on a fourth move.

That sequence matters. The RBA did not arrive at 4.35% by accident. It got there by hiking three times into an environment where markets expected it to ease, which means another move higher carries not just economic weight but reputational stakes the Board cannot ignore.

When big ASX news breaks, our subscribers know first

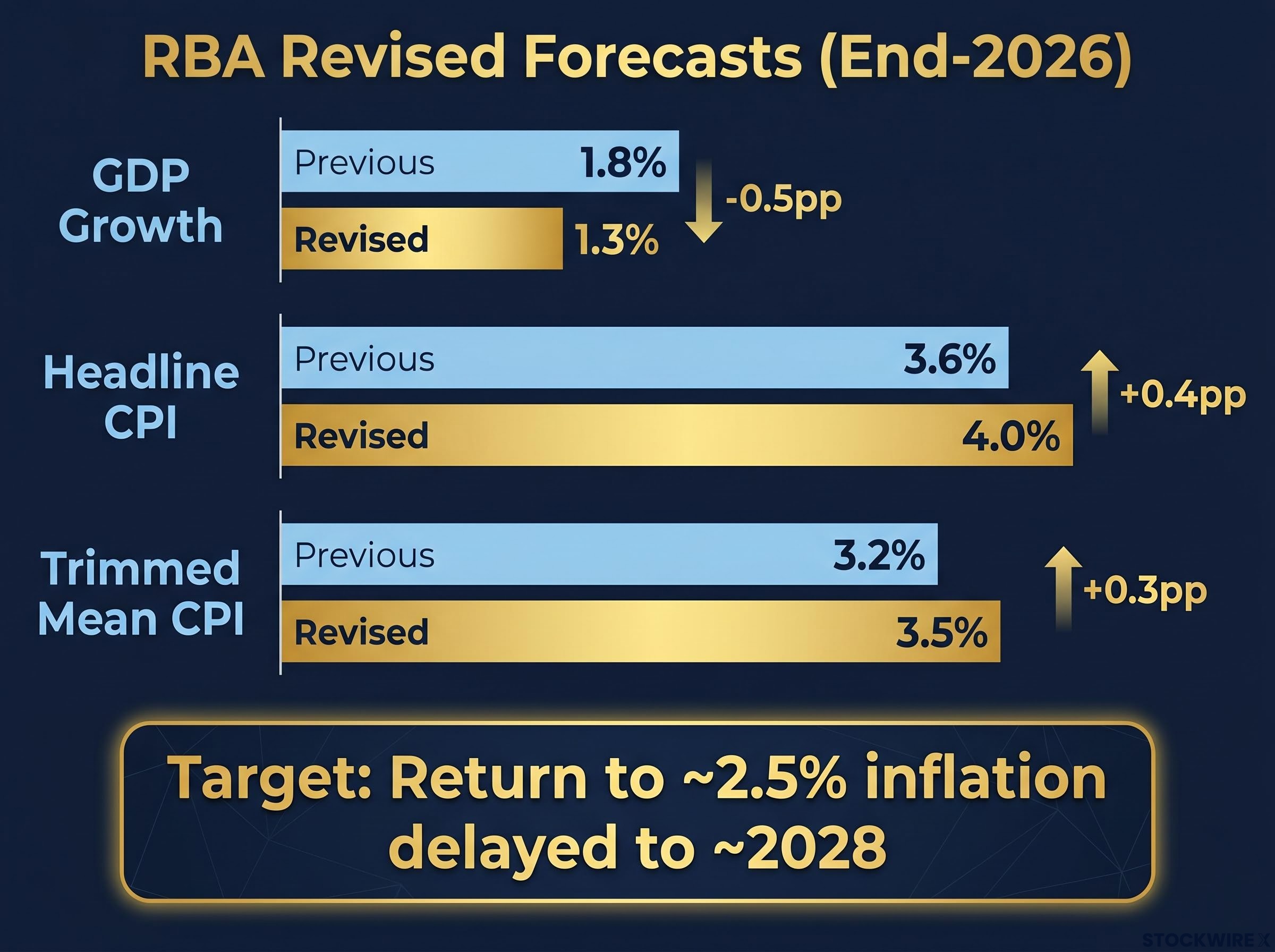

What the RBA’s revised forecasts actually say about the economy

The numbers the RBA published in its May 2026 Statement on Monetary Policy tell a story that is uncomfortable in a specific way. Read the growth forecast in isolation and it looks like an economy absorbing the cost of tight policy. Read the inflation forecast in isolation and it looks like a central bank that still has work to do. Read them together and the picture sharpens into something harder to manage.

| Indicator | Previous Forecast | Revised Forecast | Horizon |

|---|---|---|---|

| GDP growth | 1.8% | 1.3% | December 2026 |

| Headline CPI | 3.6% | 4.0% | End-2026 |

| Trimmed mean CPI | 3.2% | 3.5% | End-2026 |

| Unemployment | — | 4.3% | End-2026 |

| Inflation return to ~2.5% | — | ~2028 | — |

Growth downgraded by half a percentage point. Headline CPI revised 0.4 points higher. Trimmed mean revised 0.3 points higher. The economy is absorbing the costs of tightening without yet delivering the price stability those costs are meant to buy.

Trimmed mean inflation is the RBA’s actual policy signal, not the headline CPI figure that absorbs volatile fuel and administered price swings; the distinction explains why the Board kept hiking through 2026 even as headline numbers told a more complicated story.

The labour market trajectory is central to the policy maths. Unemployment is expected to rise only gradually, reaching 4.3% by end-2026 and 4.7% by June 2028. That slow loosening removes the hard-landing scenario that might otherwise force an emergency pivot. The RBA has no unemployment crisis to justify cutting while inflation runs above band.

The number that anchors everything else: On the RBA’s own published timeline, a sustainable return of inflation to around 2.5%, the midpoint of the target band, is a 2028 outcome at the earliest. For investors holding rate-sensitive positions on the assumption that cuts are imminent, that is a two-year wait on the RBA’s own published timeline.

Why cutting rates now would be a credibility problem, not just an economic one

The data case against cutting is clear enough. But the constraint on the RBA runs deeper than the latest inflation print. It is institutional.

Having already surprised markets with three hikes that nobody expected at the start of the year, a premature pivot to easing would invite a specific and damaging question: does the Board actually mean it when it says it is committed to the 2-3% target band? Credibility, once questioned, reprices how markets interpret every subsequent piece of forward guidance.

Three factors keep a cut firmly off the table:

- Transmission lags are still working. The full contractionary effect of three H1 2026 hikes has not yet flowed through to household spending, business investment, and credit. Holding rates elevated allows existing tightening to do its job without requiring further action.

- Inflation remains above the target band. Trimmed mean inflation at 3.5% is still outside the 2-3% range. Cutting while above band would amount to accepting a longer inflation overshoot by choice.

- Credibility constraints are binding. A central bank that surprises in one direction and then reverses before the data justify it becomes a central bank whose guidance markets discount. The RBA cannot afford that after the year it has had.

The absence of a sharp employment deterioration removes the one scenario that might override all three. If unemployment were spiking, the Board could justify an emergency cut despite above-target inflation. At 4.3% by year-end, that rationale does not exist. The hold is not passivity. It is active policy, and reading it correctly matters for how you interpret any hold decision over the coming quarters.

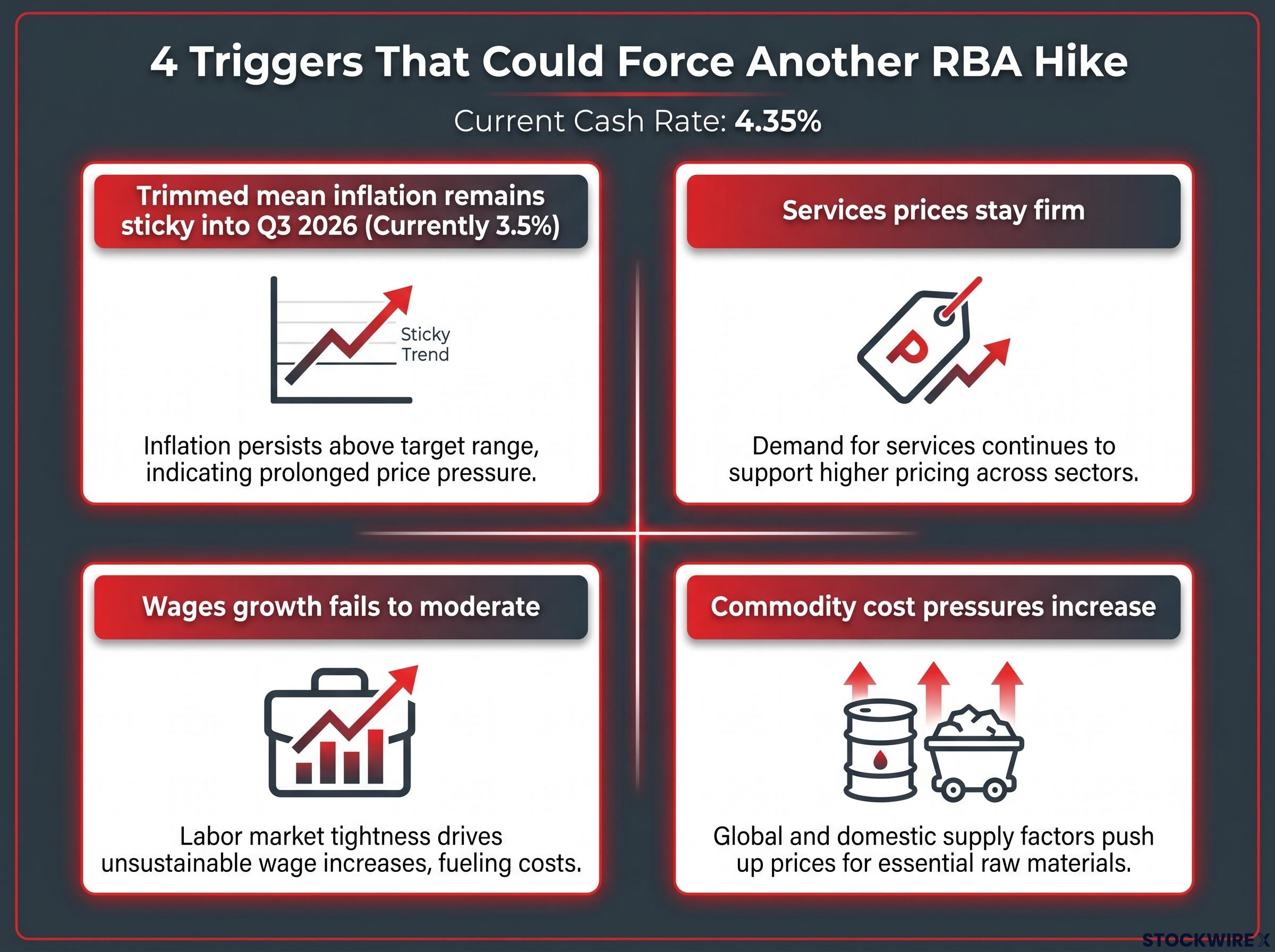

The conditions that could force another hike

Markets appear to be treating 4.35% as a ceiling. The RBA’s own forecasts suggest it may be a staging point.

The distinction matters. When the Board opts to hold, it is pausing to evaluate how prior tightening is working through the system, not announcing that the rate cycle has peaked. Should Q3 2026 data reveal that disinflation has lost momentum, the RBA would be left with an uncomfortable set of options: accept an extended period of above-target inflation, or lift rates once more.

Major bank rate forecasts entering the June decision ranged from a hold-through-2026 base case to a Westpac scenario projecting two further hikes to 4.85% by August, a dispersion that itself captures how much genuine uncertainty existed about whether 4.35% was a ceiling or a waypoint.

Four specific conditions would force the Board’s hand:

- Trimmed mean inflation remains sticky into Q3 2026, showing no meaningful deceleration from the current 3.5% trajectory

- Services prices stay firm, with the sector continuing to resist the downward pressure that rate hikes typically deliver

- Wages growth fails to moderate, keeping unit labour costs elevated and feeding through into consumer prices

- Commodity cost pressures increase, pushing input costs higher and adding an external inflation impulse to the domestic picture

A hold at 4.35% is a tactical pause, not a signal that the hiking cycle is definitively over.

The risk here is asymmetric. If the RBA holds, not much changes for rate-sensitive pricing. If the RBA hikes again, duration reprices sharply. Treating 4.35% as a ceiling rather than a possible way station means taking a position on Australian inflation data that may not be fully stress-tested.

What higher-for-longer means across Australian asset classes

The stagflationary configuration the RBA’s forecasts describe does not hit every asset class the same way. The usual portfolio hedge logic breaks down when bonds cannot provide a clean safe haven (because rate risk is upward) and equities do not get a growth tailwind (because GDP is at 1.3%). Position-by-position thinking replaces asset-class-level generalisations.

| Asset Class | Directional Pressure | Key Risk Factor |

|---|---|---|

| Long-duration bonds | Negative | Duration risk extends to 2028 if higher-for-longer holds |

| Equities (leveraged / consumer discretionary) | Negative | Compressed margins from weak demand (1.3% GDP) and high funding costs |

| AUD | Mixed | Yield-differential support offset by growth weakness |

| Property / variable-rate borrowers | Negative | Compounding mortgage stress from three H1 2026 hikes, with a fourth possible |

Long-duration bonds carry the most direct exposure. If markets continue to underprice the probability of another hike, or bring forward cut expectations relative to the RBA’s slow disinflation path, bondholders face sustained repricing risk that could extend for two years. For Australian equities, the pressure comes from both sides of the stagflationary squeeze: weak real GDP suppresses demand while persistently high funding costs compress margins. Highly leveraged firms and consumer-discretionary names sit in the sharpest part of that vice.

ASX home bias concentrates portfolio exposure precisely in the sectors most exposed to the stagflationary squeeze: a domestically weighted index that is structurally underweight global growth assets compounds the earnings pressure from weak GDP with the discount rate pressure from elevated rates.

AUD under a stagflationary rate scenario

Higher relative Australian rates versus easing global peers would normally support the currency through yield differentials. Under stagflation, the growth component complicates that logic. Weak domestic demand and a 1.3% GDP trajectory may limit or offset the yield support. The honest read is mixed signals, and that ambiguity is itself the investor-relevant insight: the AUD is not a clean yield play right now.

Property and household cash flow

Housing is the primary transmission channel. Variable-rate mortgage borrowers have already absorbed three hikes in H1 2026. A fourth would not simply add incremental pressure; it would compound existing stress on household cash flows at the point where discretionary spending is already contracting. This is not just a housing market event. It flows directly into consumer spending, retail earnings, and broader domestic demand.

Where Australian rate policy sits in mid-2026 and what to watch next

The RBA’s near-term menu is narrow: hold, hike, or hold-then-hike. A genuine easing cycle, on current projections, is a 2028 story at the earliest.

Three plausible scenarios describe the next six to twelve months. The Board holds through end-2026 while transmission effects work through the economy. Or Q3 data confirm stalled disinflation and force another hike. Or the decision is deferred into a prolonged hold-then-hike path that pushes any resolution into late 2026 or early 2027. All three scenarios sit within a structural frame where sustained rate relief is years, not quarters, away.

Three specific data series will resolve the uncertainty:

- Trimmed mean CPI: The single most important input for the RBA’s inflation assessment. Any reading above 3.5% in Q3 keeps the hike option live.

- Services inflation: The category most resistant to rate-driven disinflation. Persistence here signals that policy is not transmitting where it needs to.

- Wages growth: Sustained elevated wages feed unit labour costs and make the return to 2-3% inflation arithmetically harder without further tightening.

Positioning for a 2026 or even early 2027 rate-cut cycle in Australian assets requires betting against the RBA’s own published forecasts. That is a position that needs to be held deliberately, with clearly defined exit conditions, rather than as a passive assumption inherited from the start of the year.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced are subject to market conditions and various risk factors. Past performance does not guarantee future results.