China Is Paying Double for Nvidia AI Hardware It Cannot Buy

1 hr ago

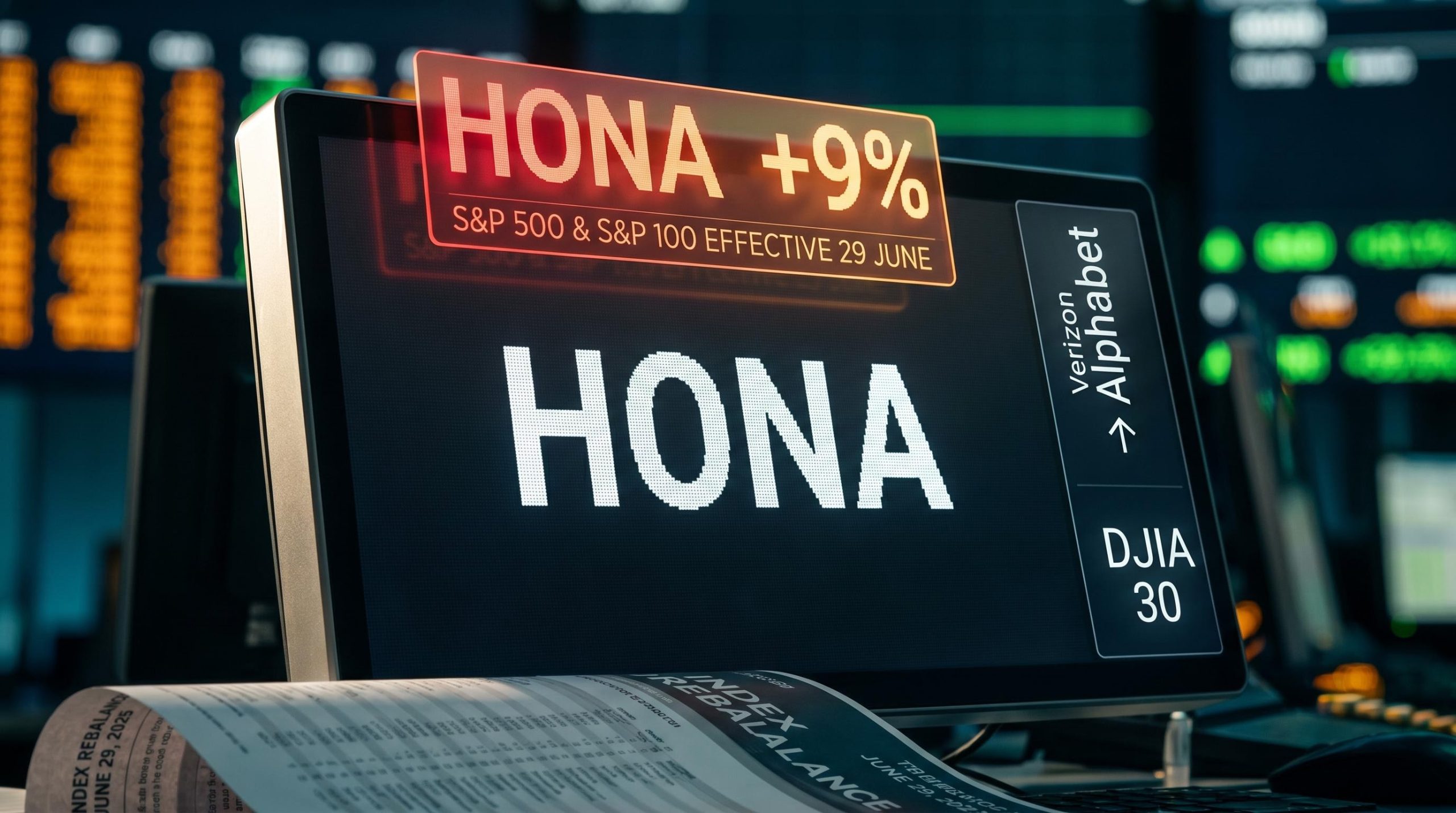

Two major U.S. index reshuffles land simultaneously on 29 June, and the price tag on one of them is already visible: Honeywell Aerospace’s when-issued shares climbed over 9% in after-hours trading once the news broke, with markets moving before the company has even begun operating as a standalone business.

Index composition changes are often treated as administrative footnotes. These two are not. One involves a spinoff entering the S&P 500 and S&P 100 at the same moment, creating a forced-buying dynamic with constrained float. The other is the Dow Jones Industrial Average adding its second consecutive AI-era technology giant, cementing a structural tilt in America’s most-cited equity benchmark.

Here is a clear framework for reading stock index changes as a market catalyst: which one carries real flow implications, which one carries a signal, and where the edge disappears once the rebalancing window closes.

Both changes take effect on 29 June 2026, per S&P Dow Jones Indices. Both involve blue-chip names entering major benchmarks. The similarities end there.

Honeywell Aerospace (ticker: HONA, Nasdaq) joins the S&P 500 and S&P 100 simultaneously, replacing Conagra Brands. Trillions of dollars benchmark to the S&P 500, and a further layer of derivatives and structured products track the S&P 100. Passive funds benchmarked to those indices are obligated to hold HONA at its index weight, and they must acquire that position by the effective date. The 9% after-hours move in when-issued shares reflects that desks have already begun pricing in the anticipated buying pressure, rather than any new view on the underlying aerospace franchise. Understanding that distinction matters before deciding what to do with it.

Alphabet Class A, meanwhile, replaces Verizon in the 30-stock, price-weighted Dow. Verizon represented approximately half of one percentage point of the DJIA. The Dow carries a fraction of the passive assets linked to the S&P 500, meaning the obligatory dollar rebalancing is far smaller. Treating both events as a single “index reshuffle” would cause you to overestimate the demand impact on Alphabet and underestimate the short-term volatility risk around Honeywell Aerospace.

| Dimension | Honeywell Aerospace | Alphabet Class A |

|---|---|---|

| Index joined | S&P 500 and S&P 100 | Dow Jones Industrial Average |

| Replacing | Conagra Brands | Verizon |

| Effective date | 29 June 2026 | 29 June 2026 (before open) |

| Benchmarked assets (scale) | Trillions (S&P 500 + S&P 100) | Significantly smaller (Dow-tracking products) |

| Immediate market reaction | When-issued shares up 9%+ after hours | No material after-hours move |

S&P 500 inclusion means that every benchmarked passive vehicle must carry the new constituent at its index weight, generating non-discretionary demand that has nothing to do with whether any buyer considers the stock cheap or expensive. That creates non-discretionary demand, the kind of buying that happens regardless of whether the buyer thinks the stock is cheap or expensive. The scale of that demand is a function of how much money benchmarks to the index, and for the S&P 500, the figure runs into the trillions.

Now layer in the spinoff. Honeywell’s board approved the aerospace spinoff with a record date of 15 June 2026 and a distribution effective at 12:01 a.m. New York time on 29 June 2026. The index entry lands on the same date. Here is the sequence:

Because HONA starts life as a newly independent company, its freely tradable float is potentially constrained relative to a seasoned large-cap. The same volume of passive demand is chasing fewer available shares. That is the spinoff amplifier.

The when-issued shares of Honeywell Aerospace jumped more than 9% after hours once the index inclusion was confirmed, a move driven by anticipated passive fund flows rather than any fundamental reappraisal of the aerospace business.

Dual inclusion in the S&P 500 and S&P 100 simultaneously adds another layer. The S&P 100 underlies a range of derivatives and structured products that carry their own mandatory rebalancing obligations. Research on the “index effect” shows additions tend to experience abnormal returns and elevated trading volume around effective dates, though the magnitude has declined over recent decades. What makes the HONA setup unusual is the combination: spinoff float constraints plus dual-index entry compress greater buying pressure into a narrower window than a standard addition would produce. That is worth factoring into any near-term position sizing decision. Honeywell International, to be known as Honeywell Technologies post-spin, remains in the Dow and other indices.

The Dow is a 30-stock, price-weighted index. Fewer passive products track it directly, and Verizon’s prior weight of roughly 0.5% means the dollar value of obligatory selling and buying is modest. Alphabet is already a massive S&P 500 constituent and a core holding across global equity portfolios, so Dow membership adds visibility but not a new wall of forced buying.

The structural contrast matters:

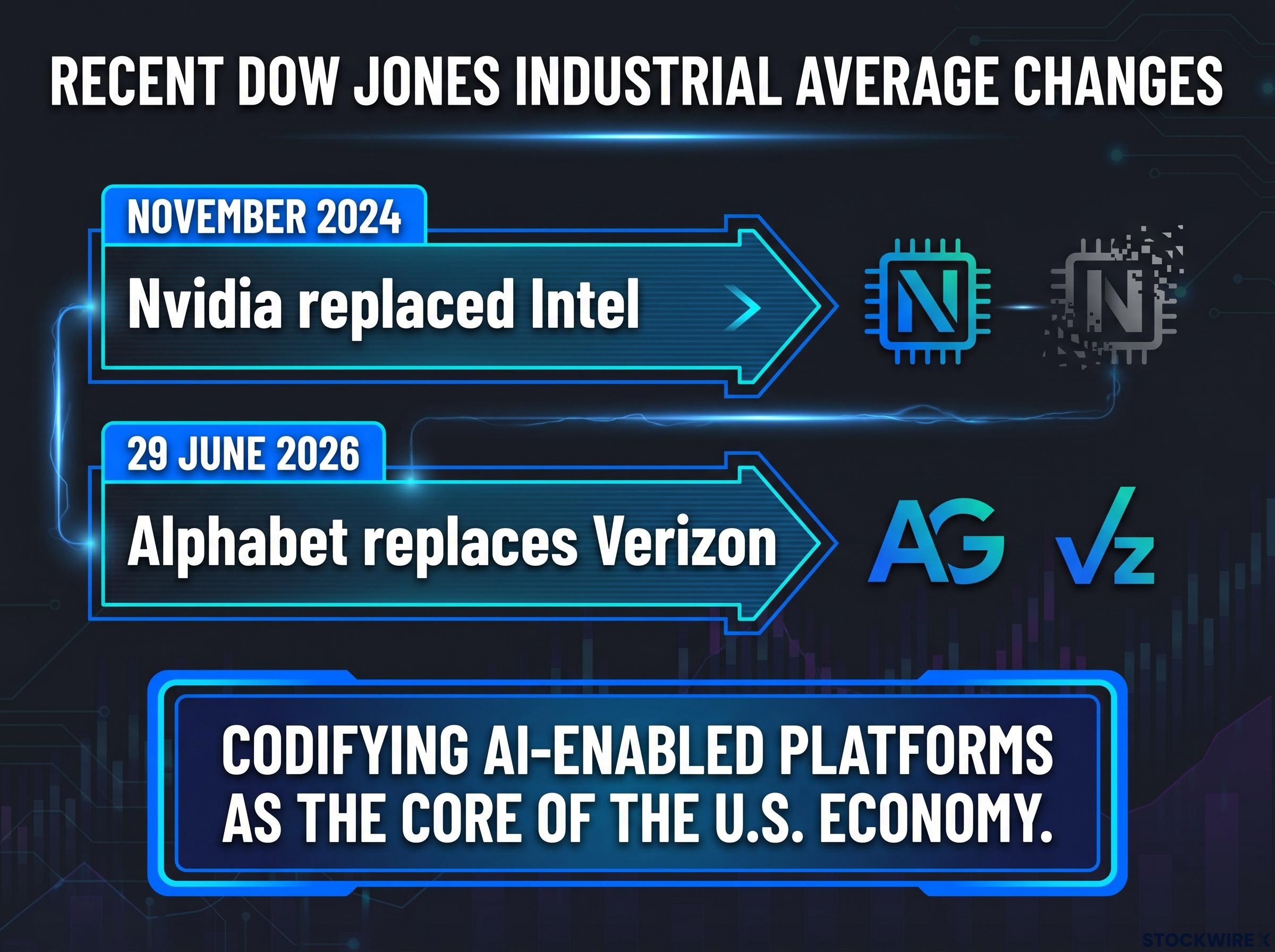

The more durable read is what the change signals about benchmark composition itself. Nvidia replaced Intel in the Dow in November 2024, the last prior modification. Now Alphabet replaces Verizon. Two consecutive Dow additions from the AI-era technology wave mean that America’s most-cited 30-stock benchmark is formally codifying AI-enabled platforms as the core of the U.S. economy.

Verizon retains its S&P 500 membership, so the removal is a prestige reduction rather than a fundamental status change.

For investors who hold broad U.S. equity index products, this is a reminder that “the market” increasingly means a concentrated bet on a small number of AI-platform companies. The flow impact on Alphabet is modest, but the question it raises is durable: whether the passive holdings you already own carry more technology concentration than you realise.

Three variables determine how much a given index change matters as a price event:

Academic and industry research finds that abnormal returns on index additions cluster between the announcement date and the effective date. Once passive rebalancing is largely complete, the mechanical tailwind dissipates.

The timing dynamic matters. Passive orders tend to execute at or near the close on the effective date, creating a predictable but crowded window that arbitrage desks and quantitative strategies already target. That crowding compresses the available edge.

Once you understand that the index effect’s edge is front-loaded between announcement and effective date, you can apply that logic to every future index addition event rather than reacting to each one as unprecedented. The framework is the reusable asset. The specific trade is not.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The permanent changes are structural: benchmark composition, index weight allocation, and investor-profile visibility for both companies. The temporary changes are mechanical: the elevated volatility, the forced buying pressure, and the compressed rebalancing window around the effective date.

For Honeywell Aerospace, the question after 29 June is no longer about index flows. It is about whether the aerospace and defence cycle, combined with standalone execution, justifies the valuation at which the passive buying wave delivered the shares. Three factors to watch:

For Alphabet, Dow inclusion does not alter the risk profile. Three factors that continue to matter:

Honeywell Technologies (formerly Honeywell International) remains in the Dow and other indices post-spin, so the industrial conglomerate lineage persists in the benchmark universe. The broader pattern, two consecutive Dow additions from AI-adjacent categories, tells you that major benchmarks are evolving toward technology concentration. If you hold passive products that track these indices, it is worth periodically auditing whether the concentration you are implicitly accepting reflects your actual risk appetite.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The index effect refers to the abnormal returns and elevated trading volume that stocks experience around the time they are added to a major index, driven by non-discretionary buying from passive funds obligated to hold every constituent at its index weight. Research shows these abnormal returns cluster between the announcement date and the effective date, then fade once passive rebalancing is largely complete.

The move reflected anticipated passive fund flows, not a new view on the aerospace business. Because trillions of dollars benchmark to the S&P 500 and S&P 100, passive vehicles are obligated to hold HONA at its index weight by 29 June 2026, and desks began pricing in that forced buying as soon as the dual index inclusion was confirmed.

An S&P 500 addition triggers non-discretionary buying across trillions of dollars in benchmarked assets, while a Dow Jones addition involves far fewer passive tracking products and a much smaller dollar value of obligatory rebalancing. Alphabet's Dow entry generates incremental demand; Honeywell Aerospace's S&P 500 entry generates a materially larger forced-buying wave.

HONA enters the S&P 500 and S&P 100 simultaneously on the same date it begins life as a newly independent spinoff, meaning its freely tradable float is potentially constrained relative to a seasoned large-cap. That combination compresses greater passive buying pressure into a narrower window than a standard index addition would produce.

Alphabet's addition follows Nvidia replacing Intel in November 2024, making two consecutive Dow inclusions from the AI-era technology wave and signalling that America's most-cited 30-stock benchmark is formally codifying AI-enabled platforms as the core of the U.S. economy. For investors in passive products tracking broad U.S. indices, it is a reminder that the benchmark increasingly reflects concentrated exposure to a small number of AI-platform companies.