Westpac Poaches Macquarie’s CIO to Lead Core Banking Overhaul

12 hrs ago

Cerebras just posted 94% year-over-year revenue growth in its first public earnings report and watched its stock fall 7-9% after hours anyway.

The gap between that headline number and the market’s reaction is the entire story of this print. Investors entered 23 June with elevated expectations baked into a share price already 22% above the May 2026 IPO level. What they got was a revenue beat, an earnings-per-share miss, two landmark partnership announcements, and gross margin guidance that implied a 9-11 percentage point sequential decline in a single quarter. Each of those facts points in a different direction, which is why the after-hours reaction zeroed in on the negatives while the bull case for the stock remains structurally unchanged.

Here is the framework for separating signal from noise: what the numbers actually show, what the OpenAI and AWS deals do and do not mean for near-term financials, and what investors holding or considering CBRS should be watching before the September earnings report.

The top line came in hot. Cerebras reported $193.4 million in Q1 2026 revenue, beating the analyst consensus of $180.8 million and marking approximately 94% growth from $99.5 million in the prior-year period. Sequential growth clocked in at roughly 13% quarter on quarter.

Then the earnings line told a different story. The GAAP net loss landed at $14.0 million, or -$0.22 per share, missing the consensus expectation of -$0.16 per share. That miss is what sent shares lower after hours, and on its face, it looks like a company spending faster than it is growing.

But the non-GAAP adjusted net loss was just $2.5 million. The $11.5 million gap between the two figures is overwhelmingly non-cash stock-based compensation, the kind of expense that is standard for a growth-stage tech company fresh off a premium IPO. That distinction matters: it tells you the operating cash burn is far narrower than the headline loss suggests.

| Metric | Q1 2026 Reported | Consensus / Prior Year |

|---|---|---|

| Revenue | $193.4M | $180.8M (consensus) |

| YoY Revenue Growth | ~94% | $99.5M (Q1 2025) |

| GAAP EPS | -$0.22 | -$0.16 (consensus) |

| Core Gross Margin | 47% | N/A (first public quarter) |

| Cash & Short-Term Investments | $3.3B | N/A |

CEO Andrew Feldman characterised the quarter as a strong beginning to fiscal year 2026, emphasising the productivity advantages of Cerebras’ wafer-scale technology, where a single massive chip replaces the clusters of smaller GPUs that most AI workloads currently run on.

Start with the Q1 number: 47% core gross margin. For a hardware company still scaling production, that looked reasonable. Investors could live with it.

Then the Q2 guidance arrived.

Cerebras guided Q2 2026 core gross margin to 36% to 38%, a sequential decline of 9-11 percentage points in a single quarter.

That is the figure that drove the after-hours selloff more than anything else on the earnings release. A company growing revenue at 94% year over year can absorb a near-term EPS miss. A company whose margins are contracting that sharply while revenue scales raises a harder question: is this a temporary cost of landing huge customers, or is it the real economics of the business showing up?

Three plausible drivers could explain the compression:

Management has not provided granular detail on which of these factors is dominant. Until the Q2 actuals arrive and the leadership team offers a clear narrative that the compression is ramp-related rather than structural, the margin uncertainty will continue to weigh on the multiple investors assign the stock. Revenue growth alone cannot solve a unit economics question.

The company’s full-year 2026 core revenue guidance of $855 million to $865 million points to roughly 69% year-over-year growth at the midpoint, a figure that underpins the demand bull case even while the margin trajectory remains unresolved.

Both partnerships carry genuine strategic weight. The risk for investors is conflating long-term contract value with near-term earnings impact.

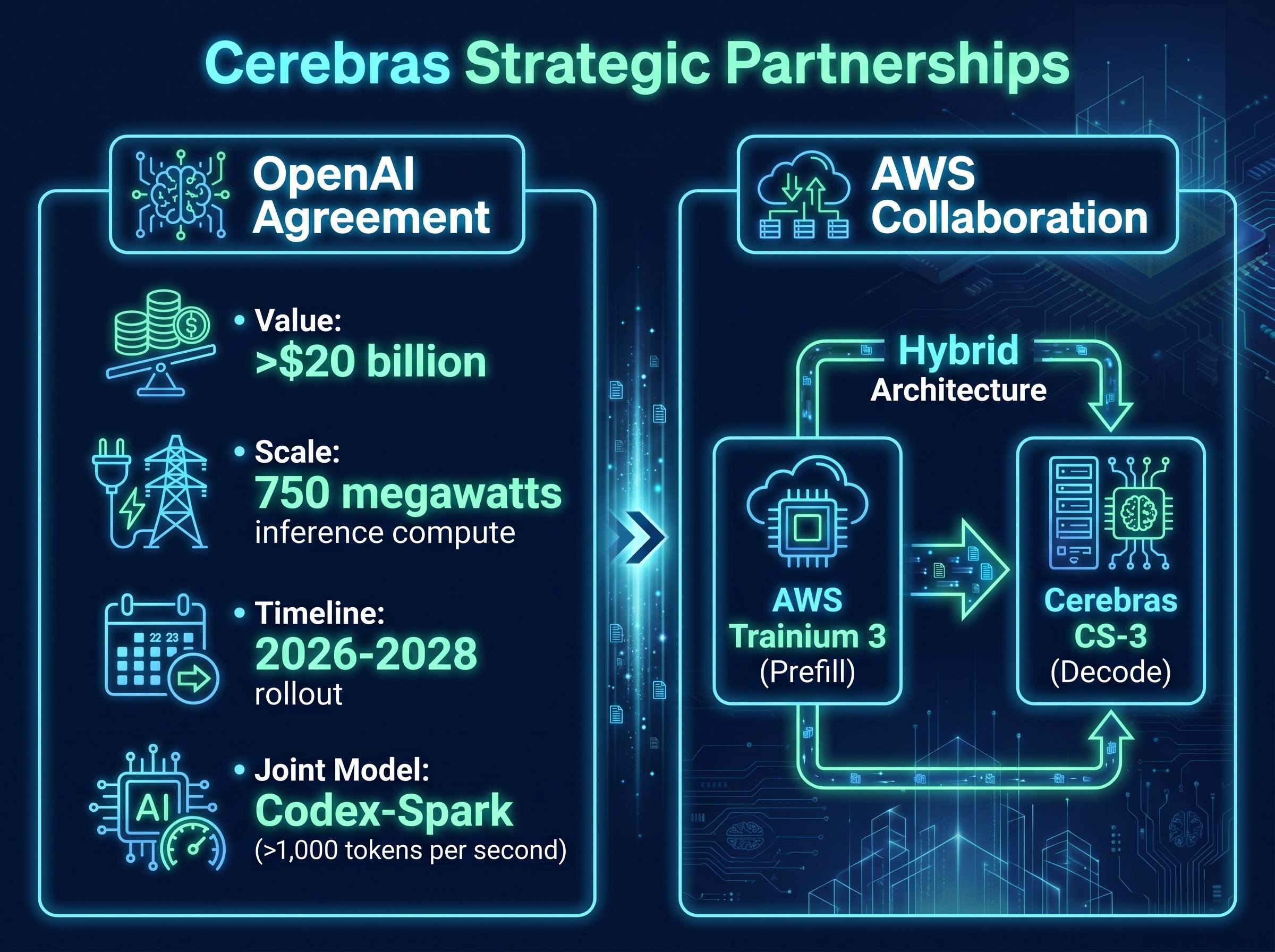

The contract terms are substantial: a multi-year arrangement with OpenAI worth more than $20 billion, covering 750 megawatts of inference compute capacity, with rollout scheduled across 2026 through 2028. Having the leading AI lab commit to wafer-scale inference at that scale is external validation that Cerebras’ architecture works for production workloads, not just benchmarks.

As part of the agreement, the two companies brought Codex-Spark to market together, a coding model that produces output at rates exceeding 1,000 tokens per second. That throughput figure plays directly to the speed advantage wafer-scale chips hold over GPU clusters for inference (the phase of AI where trained models generate outputs, as opposed to the training phase where models learn).

The financial caveat is straightforward: $20 billion in total contract value does not mean $20 billion in near-term revenue. Revenue recognition follows actual deployment and usage, and the staged rollout means the financial impact builds over years, not quarters. If the early phases are front-loaded with lower-margin infrastructure work, the deal may be contributing to the Q2 margin compression rather than offsetting it.

The AWS collaboration takes a different form. It routes the prefill stage of inference (where a model processes an input prompt) through AWS Trainium 3 chips, while Cerebras CS-3 systems handle the decode stage (where the model generates its response). That split reflects each chip family’s engineering strengths rather than a compromise.

From a go-to-market perspective, embedding Cerebras capabilities inside an AWS environment removes integration friction for enterprise customers and broadens the addressable market beyond a small number of direct-sale relationships. Over time, this reduces the customer concentration risk that comes with relying on a handful of massive contracts.

| Partner | Deal Structure | Financial Scale | Strategic Function |

|---|---|---|---|

| OpenAI | Multi-year inference compute supply | More than $20B, 750 MW | Validates wafer-scale inference at production scale |

| AWS | Hybrid prefill/decode architecture | Staged revenue, not yet quantified publicly | Broadens distribution, reduces customer concentration |

Both deals were announced concurrently with the Q1 earnings on 23 June 2026. Together, they reduce customer concentration risk and anchor multi-year demand, changing the risk profile of holding CBRS at any reasonable long-term horizon, even while near-term financials remain messy.

The post-earnings price drop did not occur in isolation. Semiconductor stocks broadly sold off on 23 June, with the Philadelphia Semiconductor Index losing approximately 7.6% across that session. During regular trading hours, CBRS had actually held up better than the sector, finishing at $226.72 (a gain of roughly 1%) before the results crossed after the close. That divergence tells you expectations were elevated heading into the print.

The Philadelphia Semiconductor Index’s 7.6% single-session drop on 23 June occurred against a sector where the AI capex-to-revenue lag has been a persistent concern: hyperscalers have committed an estimated $725 billion in 2026 capex, but independent analysts have identified an 18-24 month delay before that spending translates to recognisable chip vendor revenue, a dynamic that amplifies the volatility around any individual earnings print.

Key stock data points for context:

That last figure matters. With 17.15% short interest and a stock that entered the print at a 22% premium to its IPO price, even a modest negative surprise was always going to produce an outsized after-hours reaction. Short sellers had a concentrated bet against the name, and the EPS miss plus margin guidance gave them the catalyst they needed. That means the post-print price action is not a clean read on how the market assesses the long-term thesis; it is a sentiment-driven move amplified by positioning.

The stock’s 22% premium to IPO price heading into the print reflected the euphoria that surrounded the Cerebras IPO debut in May, when the deal priced at $185, surged 68% on its first trading day, and was 20 times oversubscribed, compressing the margin for disappointment on any first public earnings report.

Cerebras’ wafer-scale approach (building an entire processor on a single silicon wafer rather than connecting thousands of smaller chips) positions it as a differentiated alternative for inference workloads. The OpenAI and AWS deals suggest the architecture is proving its value in production environments. Whether that differentiation translates to sustainable premium pricing is exactly the question the margin guidance has re-opened.

The debate over wafer-scale versus GPU cluster inference economics centres on whether the latency and throughput advantages of a single large chip justify its per-unit cost structure relative to commodity GPU arrays that benefit from decades of supply chain maturity.

Analyst ratings heading into the print skewed firmly bullish, but every target was set before the EPS miss and margin guidance landed:

Those figures should be treated as inputs to update rather than current guidance. Analysts who set $300+ targets did so before the 36-38% Q2 margin guide. How those firms respond to the Q2 margin guidance and EPS miss in their research notes will set the tone for near-term sentiment around the stock.

For investors mapping Cerebras’ analyst target range against the broader valuation landscape, our full explainer on AI semiconductor sector forecasts covers Bank of America’s $2.7 trillion industry revenue projection through 2030, the sixfold expansion in AI data centre systems TAM, and the specific upgrade criteria that analysts applied to individual semiconductor names on the same day Cerebras reported its Q1 results.

Full-year 2026 core revenue guidance: $855 million to $865 million, pointing to roughly 69% year-over-year growth at the midpoint. That is the demand anchor for the bull case: even against margin headwinds, the revenue trajectory remains steep.

With Micron Technology due to publish its Q3 2026 results on 24 June, the day after Cerebras reported, the sector has an immediate near-term read on AI infrastructure momentum.

The Q2 2026 earnings release is scheduled for 2 September 2026. That report carries more weight than anything in the current print when it comes to settling the debate around margins and business quality.

Four specific questions investors should track heading into September:

The $3.3 billion cash position provides a meaningful buffer. This is not a company in distress during a margin compression period. But cash on hand does not answer the question that matters most: whether 36-38% gross margins are temporary onboarding noise or closer to the real steady-state economics of selling wafer-scale inference to hyperscalers at volume.

The margin compression question at the core of Cerebras’ Q2 guidance connects to a broader structural debate about inference cost economics: if generative AI applications remain fundamentally unprofitable at scale, the hyperscaler capex commitments underpinning multi-year wafer-scale infrastructure contracts could face pressure well before the 2028 deployment window closes.

For existing holders whose thesis rests on wafer-scale differentiation and multi-year AI demand, the Q1 print did not break that thesis. For prospective buyers, the after-hours dip improves entry versus pre-print levels but does not close the information gap. A conservative approach waits for Q2 confirmation; an aggressive one starts a small position on weakness and scales based on September’s evidence.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The Q1 print gave investors two competing narratives at once: a record revenue quarter with two landmark partnerships on one side, and an EPS miss plus a sharp margin compression warning on the other. Both can be simultaneously true for a company at this stage.

The central question this first public earnings report leaves open is whether the margin trajectory reflects a passing cost of ramping the largest AI infrastructure commitments in the industry, or whether it reveals something more durable about how Cerebras must price its technology to win business. September’s numbers will provide the first real answer.

The Q1 print has given investors a clearer picture of both what Cerebras is capable of and what questions still need answering. For a company’s first public earnings report, that is precisely the function it is supposed to serve.

Financial projections and forward-looking statements referenced in this article are subject to market conditions and various risk factors. Past performance does not guarantee future results.

Cerebras reported Q1 2026 revenue of $193.4 million, beating the analyst consensus of $180.8 million and representing approximately 94% year-over-year growth. The GAAP net loss came in at $0.22 per share, missing the consensus expectation of $0.16 per share.

The after-hours selloff was driven primarily by two negatives: an EPS miss ($0.22 loss versus the $0.16 consensus) and Q2 gross margin guidance of 36-38%, a sequential decline of 9-11 percentage points from the 47% reported in Q1. High short interest of 17.15% of float amplified the move.

Cerebras signed a multi-year inference compute agreement with OpenAI covering 750 megawatts of capacity and worth more than $20 billion, with rollout scheduled across 2026-2028. The two companies also jointly launched Codex-Spark, a coding model capable of generating output at more than 1,000 tokens per second.

Wafer-scale technology builds an entire processor on a single large silicon wafer rather than connecting thousands of smaller chips, delivering lower latency and higher throughput for AI inference workloads. Cerebras argues this architecture outperforms GPU clusters for the inference phase of AI, where trained models generate outputs in real time.

The four key questions heading into the 2 September 2026 earnings report are: whether gross margin lands at or above the 36-38% guidance range, whether management guides to re-expansion in H2 2026, whether the $855-$865 million full-year revenue guidance is reaffirmed or raised, and how much OpenAI and AWS revenue is being recognised versus sitting in deferred backlog.