In January 2002, the Federal Open Market Committee (FOMC) issued a post-meeting statement of roughly 130 words. By September 2014, that same document had swelled to nearly 900 words. Over the same period, the Federal Reserve’s balance sheet grew from approximately $0.7 trillion to $4.5 trillion. The parallel is not coincidental.

Federal Reserve forward guidance, the practice of signalling the likely future path of interest rates through public statements and projections, was designed to reduce uncertainty. If investors know where policy is headed, they can plan accordingly and volatility should fall. What actually happened across the Bernanke, Yellen, and Powell eras is more complicated: market panics triggered by the guidance itself, reversals that required investors to unlearn deeply embedded expectations, and growing questions about whether more communication reliably produces more stability.

What follows traces the full arc of forward guidance as a policy tool, from its original design through its most consequential failures, and explains why the return to brevity under new Fed Chair Kevin Warsh may reflect a more honest reckoning with the tool’s limits.

Two types of forward guidance, and why the difference matters more than most investors realise

The entire history of Fed communication rests on a distinction most market participants overlook. The Brookings Institution separates forward guidance into two categories: Delphic and Odyssean. The first is a forecast. The second is a promise. The gap between them explains nearly every episode where guidance went wrong.

Delphic guidance signals how policymakers believe rates may change without committing to that path. It is conditional by design. Odyssean guidance goes further, explicitly tying the hands of future policymakers by pledging a specific course of action. The mechanism depends entirely on the Fed honouring what it has promised; once broken, as a Purdue retrospective on guidance effectiveness argued, the tool’s credibility is irreparable by design.

| Dimension | Delphic guidance | Odyssean guidance |

|---|---|---|

| Definition | Conditional forecast of likely policy path | Explicit commitment that binds future action |

| Examples | Dot plot projections, qualitative phrases | Threshold-based pledges tied to unemployment or inflation |

| Market expectation risk | Misread as a promise when conditions shift | Markets price it as a guarantee |

| Consequence of deviation | Repricing, but framework intact | Credibility damage; tool may be permanently weakened |

Why the dot plot reads as a promise when it was never designed to be one

The dot plot, the quarterly Summary of Economic Projections chart showing each FOMC member’s rate expectations, is formally classified as Delphic guidance. It is a conditional forecast, not a commitment. Markets have repeatedly treated it otherwise.

When projections shift between meetings, the repricing can be sharp precisely because investors had positioned around the dots as though they were binding. Fed officials frequently deviate from their own published projections, and that deviation is a feature of data-dependent policy, not a failure of honesty. Recognising this distinction is the foundation for reading every subsequent FOMC statement and dot plot release with appropriate calibration.

When big ASX news breaks, our subscribers know first

How the Fed built, stretched, and occasionally broke its own guidance architecture from 2002 to 2022

Each phase of forward guidance tried to solve a problem the previous phase had created. The progression, tracked across three chairs and two decades, follows a pattern of escalating ambition:

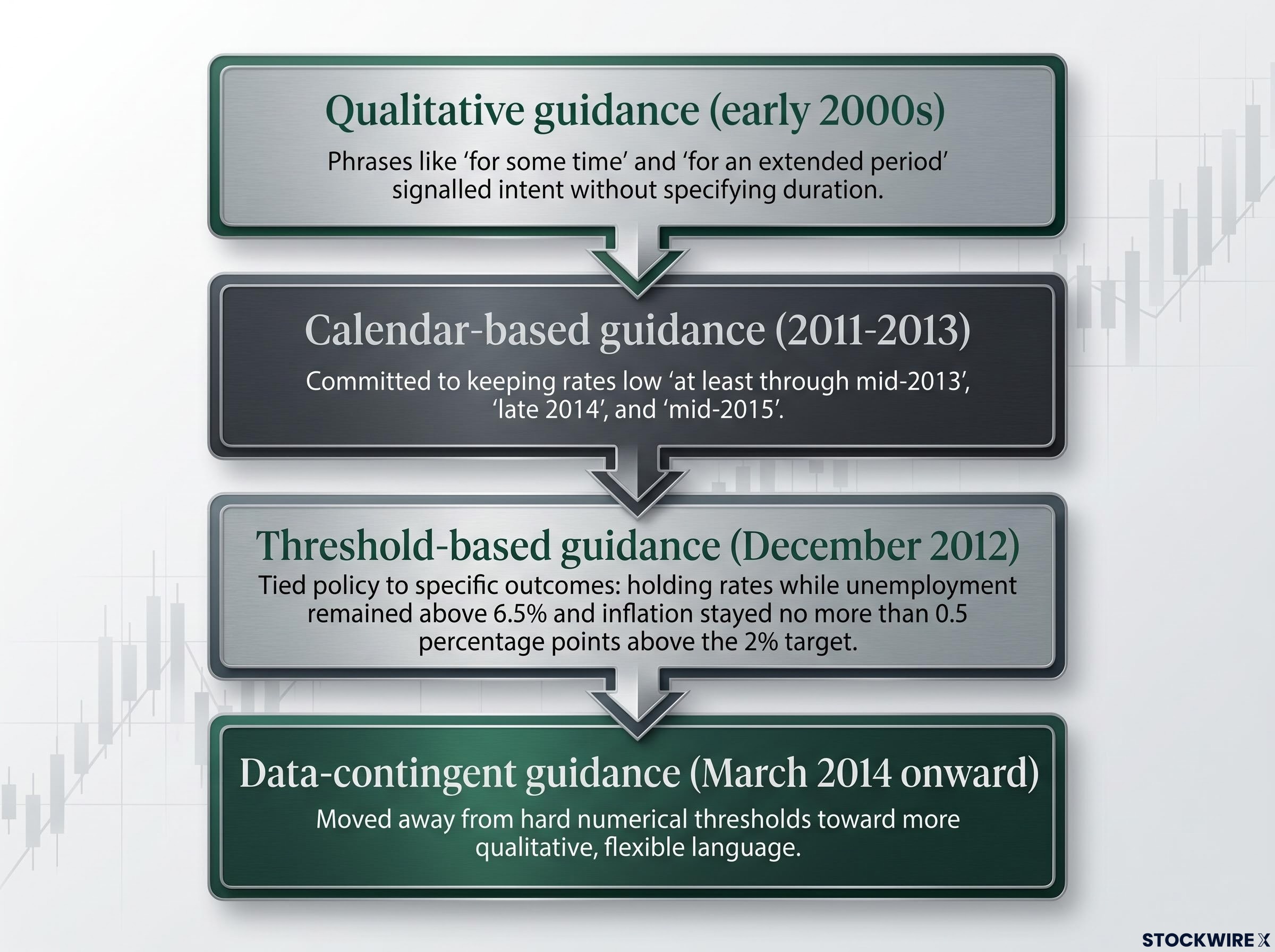

- Qualitative guidance (early 2000s): Phrases like “for some time” and “for an extended period” signalled intent without specifying duration, offering flexibility but little precision for markets to price.

- Calendar-based guidance (2011-2013): The FOMC committed to keeping rates low “at least through mid-2013,” later extended to “late 2014” and “mid-2015,” giving markets a concrete timeline but limiting the Fed’s ability to respond to changing conditions.

- Threshold-based guidance (December 2012): The committee tied policy to specific economic outcomes, pledging to hold rates while unemployment remained above 6.5% and inflation stayed no more than 0.5 percentage points above the 2% target, the clearest Odyssean commitment in the documented record.

- Data-contingent guidance (March 2014 onward): The FOMC moved away from hard numerical thresholds toward more qualitative, flexible language, acknowledging the limits of precision.

“The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored.” — FOMC Statement, December 2012

The pattern broke most visibly in two episodes. In May 2013, Ben Bernanke’s signalling about tapering quantitative easing triggered a sharp market selloff, the taper tantrum, followed by a reversal. The gap between prior guidance and subsequent action amplified the reaction. In 2021, Jerome Powell characterised inflation as transitory and used forward guidance to minimise rate hike expectations. The steep tightening cycle that followed in 2022 was an unexpected development for markets that had positioned around the prior framing. Each evolution in the guidance architecture was driven by the previous tool reaching its credibility limit.

What the word count data actually reveals about two decades of Fed communication

The numbers tell their own story before any interpretation is applied.

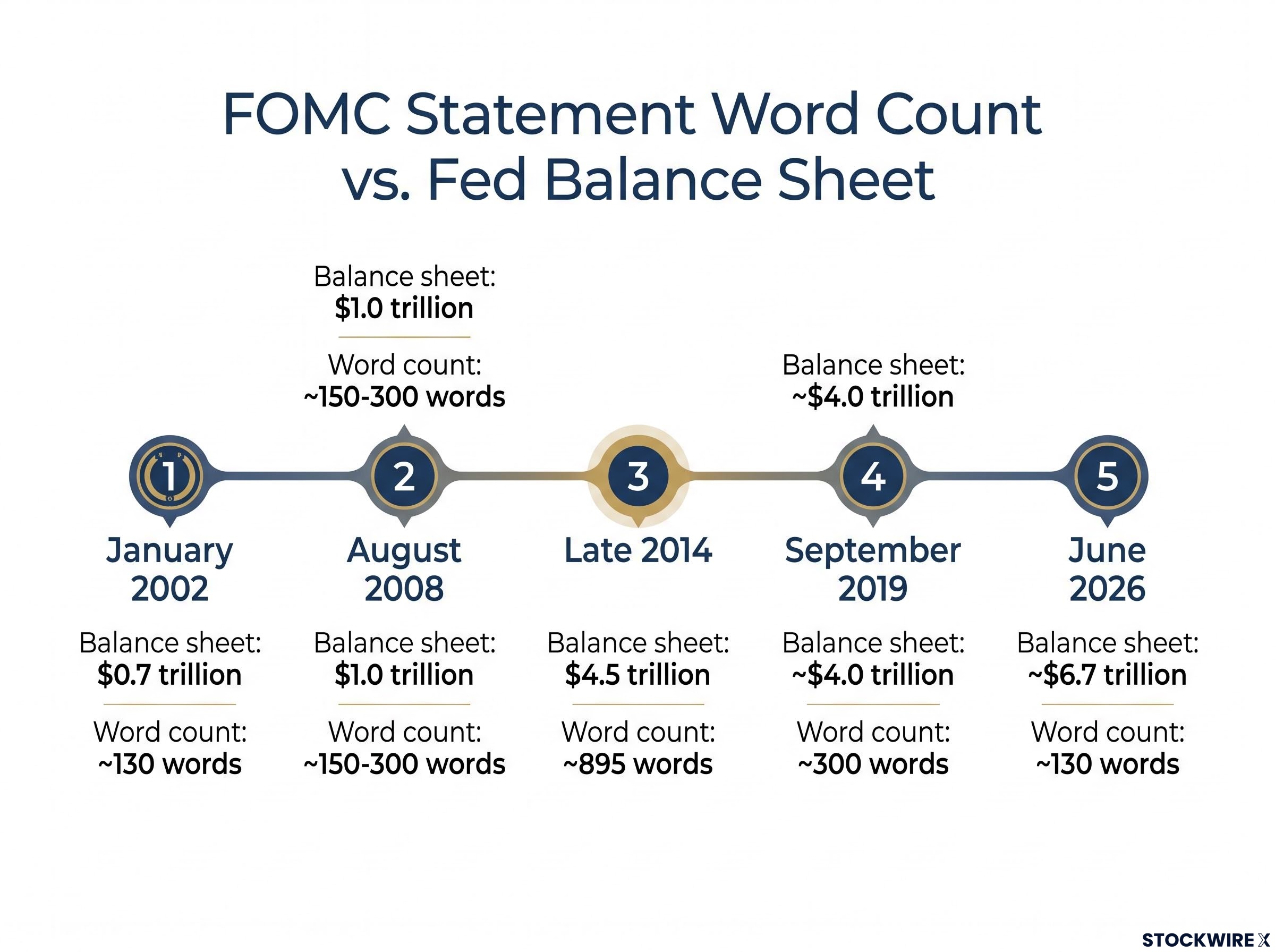

In January 2002, the FOMC statement ran approximately 130 words. Through the mid-2000s, statements expanded to roughly 150-300 words. Then the financial crisis arrived, unconventional tools multiplied, and explanatory language expanded with them. The peak came in September 2014: approximately 895 words. By September 2019, statements had contracted to around 300 words. By June 2026, under Kevin Warsh, they returned to approximately 130 words, matching the 2002 baseline.

Balance sheet and statement length: the parallel that explains the peak

The trajectory of the Fed’s balance sheet tracks alongside statement length with structural coherence. More unconventional policy generated more detailed explanatory language. When the tools became simpler, the statements contracted.

| Period | Balance sheet (approx.) | Statement word count (approx.) |

|---|---|---|

| January 2002 | $0.7 trillion | ~130 words |

| August 2008 | $1.0 trillion | ~150-300 words |

| Late 2014 | $4.5 trillion | ~895 words |

| September 2019 | ~$4.0 trillion | ~300 words |

| June 2026 | ~$6.7 trillion | ~130 words |

The word count and balance sheet data were reported by Fisher Investments Editorial Staff, drawing on Federal Reserve and FactSet data as of 17 June 2026. The figures represent the originating source’s measurement rather than an independently replicated calculation. The structural logic, however, is coherent: quantitative easing, threshold-based commitments, and calendar-based pledges all required extensive written justification. A simpler policy toolkit requires fewer words to explain.

The conditions under which guidance actually worked, and the conditions under which it made things worse

The evidence resists a clean verdict. Forward guidance is neither inherently stabilising nor inherently destabilising. Its track record depends on the conditions under which it was deployed.

When guidance works: the conditions

Research by Campbell et al. found that a purely rule-based policy would have produced better outcomes immediately after the 2008 crisis than the ad hoc guidance the Fed actually employed. From late 2011 onward, however, more explicit calendar-based guidance had measurable positive effects.

According to Campbell et al., well-designed calendar-based guidance from late 2011 onward “boosted real activity and moved inflation closer to target.”

The conditions that support effectiveness share common features:

- Guidance is clearly labelled as either a forecast (Delphic) or a commitment (Odyssean), so markets calibrate expectations accordingly

- Commitments are credibly honoured over time, reinforcing the tool’s mechanism

- Language remains explicitly conditional, reflecting genuine uncertainty rather than false precision

- Communication volume remains proportionate to the complexity of the policy being explained

When guidance backfires: the failure pattern

The two clearest failures, the 2013 taper tantrum and the 2021-2022 transitory inflation episode, share a common structure:

- The Fed encoded a forecast that later proved wrong, requiring abrupt reversal

- Markets had treated conditional guidance as a hard commitment, amplifying the repricing when the path shifted

- The volume and complexity of communication outstripped policymakers’ ability to maintain consistency across statements, projections, and actions

- The gap between prior guidance and subsequent action, rather than the action itself, was where the largest market surprise originated

Research confirms that surprises in the forward guidance components of FOMC announcements have sizable effects on asset prices and private sector forecasts. Moving markets is part of the tool’s design. The problem arises when the direction of the move reverses because the underlying forecast was wrong.

What Kevin Warsh’s return to brevity signals about the Fed’s relationship with markets

Kevin Warsh was sworn in as the 17th Fed Chair on 22 May 2026, beginning a term that runs through 2030. He previously served as a Fed governor from 2006 to 2011. By June 2026, the FOMC statement had returned to approximately 130 words, matching the January 2002 baseline.

The shift is less a stylistic preference than an institutional response to the credibility problem the previous two decades documented. Fisher Investments staff framed the argument directly: lengthy, complex FOMC statements did not produce lower market volatility during the period when they were in use. The S&P 500 experienced multiple corrections and two bear markets during the era of maximal statement complexity. Credibility, producing fewer but more reliable communications, is more likely to support investor confidence than transparency through volume.

Credibility, not transparency through sheer volume of communication, is the factor most likely to support investor confidence. Fewer but more reliable communications may produce better outcomes than more voluminous, less dependable guidance.

What investors should actually watch now that the statements are shorter

Brevity alone does not signal anything about the direction of policy. The communication format change under Warsh is separate from the substance of rate decisions; conflating style with substance is a common misreading.

What matters now is the language of conditionality. How the Fed describes uncertainty, how it characterises the data that would shift its reaction function, and whether its descriptions of current conditions match its subsequent actions are all more informative signals than statement length. Dot plot projections remain conditional forecasts, not commitments, and treating them otherwise creates vulnerability to repricing when projections shift.

The Fed has always been a work in progress, and the market knows it

The arc from 130 words in January 2002 to 895 words in September 2014 and back to 130 words by June 2026 is not a story of institutional failure. It is evidence that the Fed is capable of recognising when a tool has reached its limits and adjusting accordingly.

Forward guidance remains a powerful but fragile instrument. Its effectiveness depends entirely on the credibility of the institution using it, and credibility is earned through consistency between words and actions, not through the volume of words alone. The return to simpler communication under Warsh is less a break with tradition and more a return to an earlier and arguably more honest approach: explaining current conditions and acknowledging uncertainty, rather than attempting to lock in future paths the data may not support.

The practical framework for investors engaging with Fed communications going forward:

- Treat forward guidance as intent, not contract; the Fed should and will change course when data change

- Recognise that guidance reversals are themselves a source of investment risk, because the gap between prior guidance and subsequent action is where the largest surprises originate

- Monitor how the Fed describes uncertainty and conditionality, not just the level of rates; shifts in the reaction function description often appear in language before they appear in rate decisions

- Treat dot plot projections as conditional forecasts, not commitments

- Do not conflate communication brevity with hawkishness or dovishness; the format is separate from the substance

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements about Federal Reserve policy are subject to change based on economic conditions and data developments.