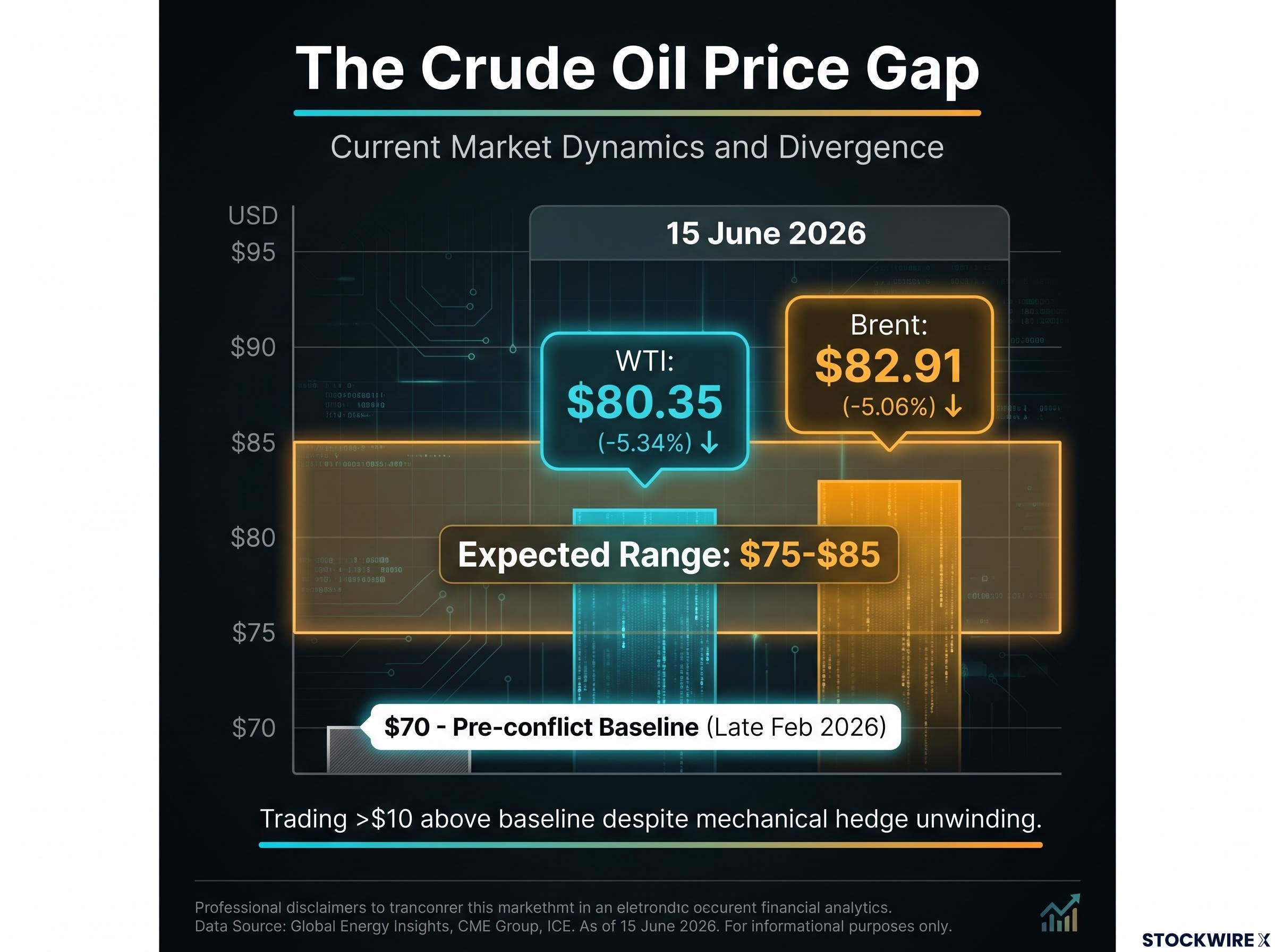

WTI crude fell 5.34% to $80.35 a barrel on 15 June 2026 as news of a preliminary U.S.-Iran ceasefire broke. Brent dropped 5.06% to $82.91. Global equities rallied. The instinct was to treat the session as the beginning of a clean return to normality. But before the conflict erupted in late February 2026, crude oil prices sat near $70 a barrel. Even after the sharpest single-day decline in months, both benchmarks are trading more than $10 above that baseline. The gap is not noise. It reflects at least five structural forces, from physical flow lags to depleted strategic reserves, that are likely to keep crude above pre-conflict levels for months, even under a durable ceasefire. What follows is a framework for understanding where the new price floor sits and which indicators will signal when, or whether, it begins to soften.

The June 15 price drop tells only half the story

15 June 2026: WTI crude settled at $80.35, down 5.34%. Brent crude settled at $82.91, down 5.06%.

A single-session drop of this magnitude following a geopolitical resolution is consistent with the mechanical unwinding of hedges accumulated during months of conflict. Traders who had built long positions or purchased call options as insurance against further escalation closed those positions rapidly once the ceasefire headline crossed. The move was a positioning event, not a fundamental reassessment of where supply and demand sit.

The distinction matters. Three reference points frame the gap:

- WTI at $80.35 on 15 June 2026

- Brent at $82.91 on the same session

- Pre-conflict baseline of approximately $70 per barrel before the late February 2026 outbreak

Global equities advancing on the same day reinforced the relief-driven nature of the repricing. Equity markets were responding to lower inflation expectations and reduced tail risk; crude was shedding geopolitical premium. Neither move addressed the structural supply questions that the next sections examine.

Investors who interpret the $80 print as a waypoint back to $70 risk misreading which forces are still at work.

The supply gap from the Hormuz closure reached a scale that existing pipeline alternatives, including Saudi Arabia’s East-West Pipeline and the UAE’s ADCOP Pipeline, could not collectively bridge, meaning the $10-plus premium above pre-conflict levels reflects a physical reality, not just sentiment.

When big ASX news breaks, our subscribers know first

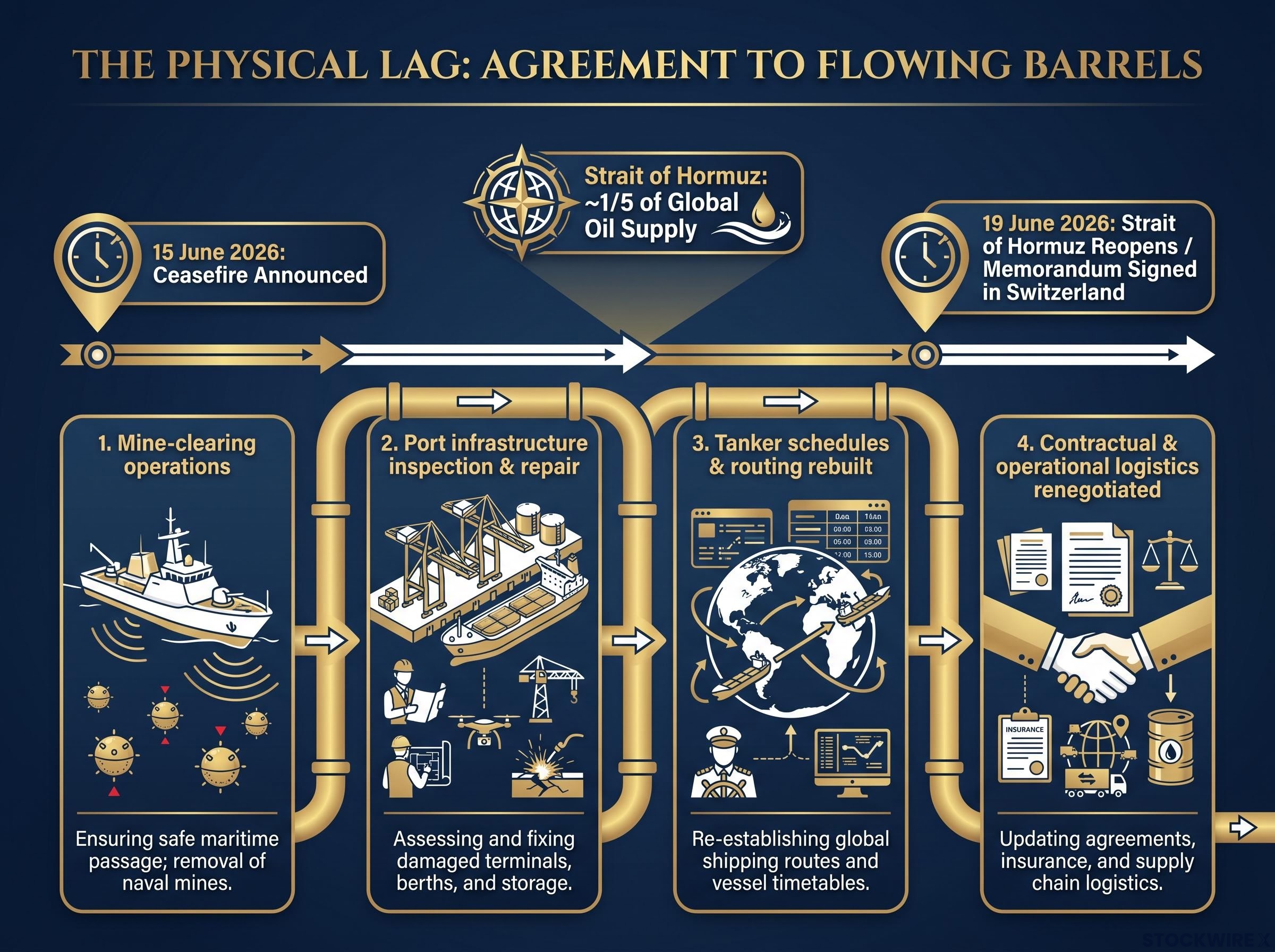

What actually reopens on June 19 and what does not

The Strait of Hormuz is the chokepoint through which approximately one-fifth of global oil supply passed before the conflict began. President Trump confirmed the waterway would reopen on 19 June 2026, with the delay from the 15 June ceasefire announcement attributed specifically to ongoing mine-clearing operations. Pakistani Prime Minister Shehbaz Sharif confirmed that the formal memorandum would be signed in Switzerland on that date, with both nations declaring a permanent halt to military operations across all fronts, including Lebanon.

The EIA Strait of Hormuz chokepoint data quantifies the waterway’s systemic importance: in the first half of 2025, approximately 20.9 million barrels per day transited the Strait, equivalent to roughly 20% of global petroleum liquids consumption, with limited alternative routing options available to producers and buyers alike.

Iranian officials, however, indicated that implementation would follow the signing, not precede it. The sequencing matters: a signed document does not equal restored barrels.

From signed agreement to flowing barrels: the physical lag

Even once the Strait is formally declared open, full supply restoration follows a sequential pipeline, not a simultaneous switch:

- Mine-clearing operations must be completed across shipping lanes (already underway but unfinished as of the ceasefire date)

- Port infrastructure requires inspection and repair after months of conflict

- Tanker schedules and routing must be rebuilt as operators assess safety and commercial viability

- Contractual and operational logistics must be renegotiated between producers, shippers, and buyers

ING analysts noted in published research that resuming infrastructure and logistics operations in the region would not be instantaneous. The timeline between a signed agreement and restored physical flows is measured in months, not days. Investors pricing crude as though 19 June marks a full supply reset are working from an incorrect premise.

Why shipping lanes heal slower than peace deals

War-risk insurance premiums are not set by diplomats. They are set by Protection and Indemnity (P&I) clubs and specialist underwriters who price risk based on demonstrated periods of stability, not announcements of intent. A ceasefire signed on Friday does not change a premium recalculated on Monday. Underwriters require sustained evidence that a waterway is safe before adjusting rates downward, and that evidence accumulates over weeks to months.

The war-risk insurance dynamics that kept the Strait effectively closed to standard commercial traffic even when physical passage was technically possible represent a market mechanism that moves on actuarial timescales, not diplomatic ones, with VLCC daily hire rates tracking around $110,000 per day as a real-time measure of residual disruption severity.

ING analysts confirmed that some shipping companies may remain hesitant to re-enter the Strait of Hormuz in the near term, even following the ceasefire announcement.

The hesitancy is rational. During the April 2026 ceasefire extension within this same conflict, the U.S. signalled de-escalation but kept naval forces in place and the blockade active. Conditions changed faster than the diplomatic language suggested they would. Shipowners who re-entered prematurely would have faced re-routing costs and potential losses.

Before owners commit vessels back through the Strait, multiple actors must all signal comfort simultaneously:

- Naval forces must confirm lane clearance and provide escort assurances

- P&I clubs must adjust war-risk zone designations

- War-risk underwriters must reduce or remove conflict-zone surcharges

Until all three align, elevated insurance and freight costs raise the effective delivered cost of every barrel transiting the Gulf. That cost premium flows directly into the crude price floor, holding it above pre-conflict levels regardless of what the spot market headline reads.

Depleted reserves create structural buy pressure at lower prices

Months of supply disruption have drawn down strategic petroleum reserves (SPRs) and commercial inventories globally. The conflict exceeded three months in duration, from late February 2026 through to the 15 June ceasefire. Over that period, consuming nations tapped reserves to manage domestic supply gaps and moderate price spikes. Those stocks now require replenishment.

ING analysts specifically identified inventory replenishment as providing a floor for crude oil prices even as flows gradually resume. The mechanism is straightforward: the very buyers who would normally allow prices to drift lower are instead structural purchasers the moment prices appear reasonable relative to crisis peaks.

The limits of emergency reserve releases became quantifiably clear during the conflict: the IEA’s coordinated release of approximately 280 million barrels failed to halt global inventory draws running at 8.5 million barrels per day, meaning the replenishment demand now facing consuming nations is compounding on top of stocks already drawn well below pre-conflict levels.

The 2022 SPR release offers the clearest precedent. The U.S. government released a record volume of strategic reserves to cool prices, then announced plans to buy back barrels once prices fell to target ranges. The stated buyback programme turned a public seller into a structural buyer, effectively placing a floor under the market. Other major consuming nations followed similar patterns.

The U.S. Department of Energy SPR replenishment data shows that nearly 200 million barrels were purchased or retained since 2022 at an average price under $76 per barrel, a buyback programme that transformed a major sovereign seller into a structural price-floor buyer and established the template that consuming nations are following in the current cycle.

Applied to the current scenario, the dynamic is the same. Replenishment demand is government-mandated and therefore predictable, not sentiment-driven. It limits how far prices can fall even as Hormuz flows normalise.

The table below summarises the five structural forces supporting the higher price floor, their mechanisms, and approximate time horizons:

| Force | Mechanism | Time Horizon |

|---|---|---|

| Physical flow lag | Mine-clearing, port repairs, tanker re-routing | Months to years |

| Shipping/insurance hesitancy | War-risk premia slow to normalise | Weeks to months |

| Strategic reserve replenishment | Structural buy demand from depleted stocks | Months |

| Residual geopolitical risk premium | Credible probability of resumed hostilities | Indefinite, decaying over time |

| OPEC+ quota response | Potential tightening to defend prices | Ongoing |

Investors waiting for a clean dip to $70 may be waiting for a price that structural buyers will not allow to materialise.

The new price floor: what to expect in the months ahead

Four forces are working in the same direction:

- Physical flow lag: Mine-clearing, port inspections, and tanker rescheduling keep barrels off the market for months

- Shipping and insurance hesitancy: Elevated war-risk premiums raise the effective delivered cost of Gulf crude

- SPR replenishment demand: Government buyers create structural bid at lower price levels

- Residual geopolitical risk premium: Markets price a non-trivial probability of re-escalation

Together, these support a crude price floor meaningfully above the pre-conflict $70 baseline, even under a scenario where the ceasefire holds.

The geopolitical premium deserves direct attention. Israeli strikes against Hezbollah in Lebanon over the weekend, conducted during the ceasefire transition period, drew sharp criticism from President Trump and demonstrated precisely the kind of third-party action that can reignite regional tensions independent of the bilateral U.S.-Iran deal. As long as that risk is credible, markets will maintain some premium.

OPEC+ adds a reinforcing variable. The group could respond to falling prices by tightening quotas, and the speed of Iranian export recovery (sanctions compliance, customer contract renegotiation, technical ramp-up) creates its own delays regardless of OPEC+ decisions.

Two scenarios frame the path forward:

- Floor holds: Global demand remains firm, structural buy-side forces (SPR replenishment, slow shipping normalisation) keep crude in the $75-$85 range for months, and the geopolitical premium decays gradually rather than disappearing

- Floor tested: A sharp global macro slowdown or recession destroys enough demand to overwhelm the structural forces, pushing crude toward or below the pre-conflict baseline

Demand destruction is the one force capable of overwhelming the buy-side dynamics described above. It is the primary downside risk to the thesis.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The ceasefire is a repricing process, not a reset

The 15 June price drop was the first stage of a multi-stage repricing. The hedge unwind is largely mechanical and largely complete within days. The structural recalibration, where shipping premiums, reserve stocks, and risk premia find their new levels, takes months.

Historical Hormuz episodes and the dynamics of this specific conflict both point to the same conclusion: geopolitical risk does not reprice as an on/off switch. Earlier ceasefire announcements during this conflict produced sharp single-session declines, yet both Brent and WTI remained well above pre-conflict levels, as geopolitical risk continued to be factored into prices. The new equilibrium sits above the pre-February 2026 baseline.

For investors reassessing energy exposure, three leading indicators will signal where the floor is actually settling:

For investors reassessing broader portfolio exposure beyond crude itself, our deep-dive into the cross-asset inflation transmission examines how a sustained $10-$20 per barrel crude increase feeds into US headline CPI, how 30-year Treasury yields and Japanese government bond yields responded simultaneously, and why all three major central banks adopted a conditional look-through posture that has kept rate cut timelines extended.

- War-risk insurance rate trends for vessels transiting the Strait of Hormuz

- Government SPR repurchase announcements from major consuming nations

- Iranian export volumes post-reopening, measured against pre-conflict baselines

Daily spot price moves will generate noise. These three indicators will generate signal.

The ceasefire changes the direction of crude prices, not the destination. The structural forces that built the higher floor remain in place, and they will take months, not days, to unwind.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.