BofA Double-Upgrades Intel to Buy With a $135 Street-High Target

2 mins ago

SpaceX priced its initial public offering at $135 per share on 11 June 2026, raised $75 billion in a single session, and closed its first day of trading at $160.95, a market capitalisation of approximately $2.1 trillion before the prospectus ink had dried. It is the largest U.S. IPO on record. Within hours of the debut, Wolfe Research analysts Myles Walton and Peter Supino initiated coverage with an Outperform rating and a $175 price target, projecting 70% top-line revenue growth and a near-doubling of EBITDA margins through 2030. What follows breaks down what Wolfe’s bull case actually argues, what each pillar of the thesis requires to be true, and how finance readers can structure an ongoing framework for evaluating SPCX as a publicly traded equity.

The numbers deserve a moment on their own before any analytical framework is applied to them.

The gap between the $1.77 trillion implied valuation at pricing and the $2.1 trillion close tells its own story: the market repriced SPCX above the offering level immediately, signalling that institutional demand was not satisfied at the IPO price.

Bloomberg’s SpaceX’s Nasdaq debut coverage confirmed the $1.77 trillion implied valuation at pricing and the immediate surge past $2 trillion on the first trading day, reflecting institutional demand that was not satisfied at the $135 IPO price.

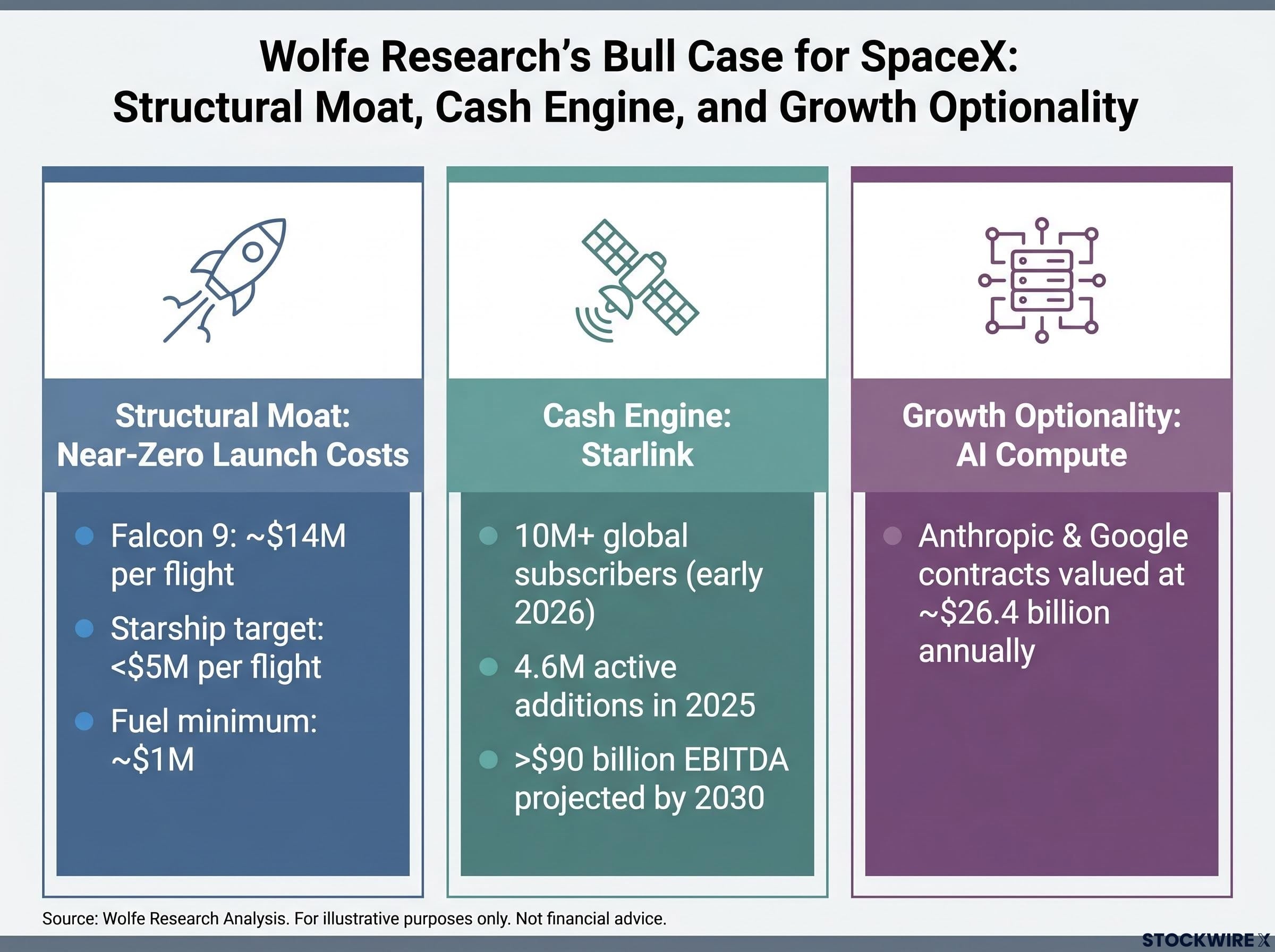

Wolfe Research initiation: Outperform rating, $175 price target, with projected 70% top-line revenue growth and a near-doubling of EBITDA margins through 2030.

Wolfe’s note, arriving within hours of the Nasdaq debut, represents the first serious public analytical framework applied to SPCX. Its value lies not only in the bullish conclusion but in how explicitly it quantifies what happens if the thesis fails.

The investment thesis has three load-bearing pillars. Compress them, and this is what Wolfe is asking investors to believe:

The bull case requires all three pillars to execute simultaneously. That requirement, which Wolfe’s own initiation acknowledges, is the central risk the valuation carries. Each new data point, whether a Starship test result, a Starlink subscriber report, or an AI contract announcement, should be evaluated against the specific pillar it advances or undermines.

A sum-of-parts valuation methodology applied with discipline about segment maturity is the analytical approach that most directly maps to how Wolfe structures its three-pillar thesis: each segment requires a separate framework because launch services, Starlink broadband, and AI compute each sit at a different point on the maturity curve and therefore warrant different confidence weights in any discounted model.

Starlink is the most conventional part of the thesis and, for now, the most proven. It reached more than 10 million global subscribers by early 2026, with approximately 2.7 million U.S. subscribers and 4.6 million active customer additions during 2025 alone. Wolfe characterised it as the most dependable near-term earnings contributor.

For the cash engine to function as projected, several conditions must hold: sustained subscriber growth, particularly in emerging markets and mobility applications; average revenue per user (ARPU) holding under competitive pressure; manageable churn; and continued regulatory approvals globally. Amazon’s Project Kuiper has been identified as the primary competitive threat to Starlink ARPU.

Q1 2026 segment profitability data anchors the cash engine claim in current financials rather than projection: Starlink contributed approximately 69% of quarterly revenue with an estimated 10.3 million subscribers while AI infrastructure remained cash-flow negative, producing a group net loss of $4.28 billion on $4.69 billion in revenue, a loss rate that puts near-term pressure on the thesis that Starlink alone can fund the capital requirements of the other two pillars.

Starship is where the thesis moves from operational evidence to projection. As of mid-2026, it has not achieved routine orbital operations or full rapid reusability. The risk is schedule, not physics. Even if the engineering works, a multi-year slip would materially reduce Starship’s contribution to the financial targets the valuation implicitly discounts.

Wolfe quantifies this starkly: without a successful Starship programme, 2030 financial targets would be reduced by 35% and 2035 targets by 50%. That figure is the most useful single data point in the initiation for risk-calibrated investors; it transforms an abstract timeline concern into a concrete valuation haircut.

| Attribute | Starlink | Starship |

|---|---|---|

| Current status | 10M+ subscribers, generating revenue | Testing phase; no routine orbital ops |

| Bull case requires | ARPU stability, subscriber growth, regulatory expansion | Full rapid reusability on schedule |

| Primary risk | Amazon Kuiper competition, ARPU compression | Schedule slip of 3-5 years |

| Wolfe’s downside if thesis fails | Cash engine underperforms, constraining other segments | 35% reduction to 2030 targets; 50% to 2035 |

The AI segment carries genuine growth credentials. Its three components are distinct and enumerable:

Wolfe’s analysts positioned the thesis carefully: they do not anticipate SpaceX surpassing Anthropic or OpenAI in AI model development. The argument is a cost advantage in compute infrastructure through vertical integration and, eventually, space-based data centres, not AI model leadership.

Two conditions determine whether that growth is structural or sentiment-driven. First, SpaceX must build and sustain a genuine cost advantage through vertical integration and space-based compute, infrastructure that does not yet exist at commercial scale. Second, today’s elevated AI capital expenditure must not prove cyclical.

The distinction between verified versus unverified AI infrastructure claims is sharpest in the xAI segment, where the S-1 filing confirms a gigawatt-scale ground-based GPU cluster as a balance-sheet asset but orbital data centres, a central component of the long-term compute cost advantage thesis, have no launched hardware and no announced deployment dates.

Wolfe Research explicitly acknowledged that the AI segment’s value could be diminished if broader AI market conditions prove to be a speculative bubble, making large compute contracts potentially non-sticky as enthusiasm cools.

The AI segment is the hardest to value precisely because its contribution depends on conditions entirely outside SpaceX’s control.

SPCX will trade as three different types of company depending on which segment is driving sentiment on any given day. Recognising which identity the market is assigning is the difference between reacting to headline noise and evaluating fundamental progress.

| Market identity | Metrics to watch | Comparable framework |

|---|---|---|

| Broadband utility (Starlink-driven) | ARPU, churn, subscriber adds, regulatory approvals | Subscription business multiples |

| Milestone hardware play (Starship-driven) | Test cadence, reusability achievements, timeline adherence | Milestone-driven probability discounting |

| AI infrastructure proxy (xAI/compute-driven) | Compute contract durability, Cursor option decision, xAI developments | AI sector multiples |

Several risks apply regardless of which narrative is driving the stock. Spectrum licensing outcomes in India, the EU, and developing economies carry material revenue implications for Starlink. Geopolitical friction from Starlink’s role in conflict zones could constrain operations or complicate government contracting.

Then there is the Musk-specific variable. Elon Musk’s parallel involvement in Tesla, X, xAI, and his DOGE advisory role creates a category of headline and reputational risk that does not attach to most comparable companies. Analysts have cited these interconnections as sources of regulatory and political friction that could affect any of the three segments unpredictably.

The IPO valuation, $135 per share at pricing, already repriced to $160.95 by the first-day close, asks investors to accept three propositions simultaneously:

Wolfe’s $175 price target and Outperform rating provide coherent scaffolding for the bull case. Notably, the initiation documents the downside cases rather than dismissing them, a feature that distinguishes it from promotional coverage.

The dual-class share structure SpaceX adopted gives founders and insiders majority voting control regardless of how much economic ownership public shareholders hold, meaning the governance constraints that would normally discipline capital allocation decisions across three simultaneous high-spend programmes do not apply here in the conventional sense.

The gap between a coherent argument and a realised return is filled by the simultaneous execution of three capital-intensive, timeline-sensitive, competitively contested business stories. The segment-aware monitoring framework outlined above is the practical tool for evaluating whether each pillar is proving out or breaking down as new information arrives.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced in this article are subject to market conditions and various risk factors.

SpaceX priced its IPO at $135 per share on 11 June 2026, raising $75 billion in a single session, the largest U.S. IPO on record. Shares closed at $160.95 on the first trading day, pushing the market capitalisation to approximately $2.1 trillion.

Wolfe Research analysts Myles Walton and Peter Supino initiated coverage with an Outperform rating and a $175 price target, projecting 70% top-line revenue growth and a near-doubling of EBITDA margins through 2030.

Starship must achieve full rapid reusability on schedule, which would reduce incremental launch costs from approximately $14 million per Falcon 9 flight to under $5 million. Without a successful Starship programme, Wolfe estimates 2030 financial targets would be reduced by 35% and 2035 targets by 50%.

Starlink surpassed 10 million global subscribers by early 2026, with approximately 4.6 million active customer additions during 2025 alone. Wolfe projects the Connectivity segment generating EBITDA exceeding $90 billion by 2030, making Starlink the most dependable near-term earnings contributor in the three-pillar thesis.

The three primary risks are: Starship schedule slips that would trigger material reductions to long-term financial targets, ARPU compression from Amazon Project Kuiper competition undermining Starlink's cash engine, and the AI capital expenditure cycle reversing before SpaceX builds a durable compute cost advantage. Elon Musk's parallel involvement in Tesla, X, xAI, and a DOGE advisory role also introduces reputational and regulatory risks that do not attach to most comparable companies.