Most Australians treat property as the default path to long-term wealth. The question of whether to buy an investment property or gain exposure through listed vehicles such as A-REITs receives far less scrutiny than the question of which suburb to target or which agent to use. Yet the structural form of property ownership, whether direct title or a position in a listed or unlisted vehicle, is itself a capital allocation decision with distinct implications for liquidity, cost, leverage, and risk. What follows is a framework for evaluating both pathways across the five dimensions that matter most to net outcomes, not a verdict on which is universally superior.

Two ways to own property without owning the same thing

Direct property ownership means holding title to a specific asset. The investor collects rent, manages or delegates tenant relationships, controls renovation and exit timing, and bears the full concentration of a single-asset position.

Indirect property exposure works differently. Three main structures are available to Australian investors:

- A-REITs (Australian Real Estate Investment Trusts): Listed on the ASX, these trade like shares and provide diversified exposure to commercial, industrial, retail, healthcare, and residential portfolios.

- Unlisted property trusts: Pooled vehicles that own direct property but are not exchange-traded. Redemptions are typically available through periodic windows, often quarterly or semi-annually.

- Hybrid structures: Vehicles that blend direct asset ownership with listed exposure, combining characteristics of both return profiles and offering diversification of income sources.

For most retail investors, the practical choice narrows to direct property, A-REITs, or unlisted trusts. The distinction matters because these are not interchangeable products with the same underlying mechanics.

The mechanics of ASX-listed investment structures matter for return outcomes beyond headline yield: units are held in a legally separate trust with an independent custodian, distributions carry different tax treatment depending on holding period, and execution practices such as using limit orders and avoiding the open and close reduce the implicit cost of each trade.

How institutional capital straddles both worlds

Entities like AEG build concurrent exposure to direct property assets and listed property vehicles within a single investment structure. This approach demonstrates that the two pathways are not mutually exclusive, even at institutional scale. Retail investors can replicate a version of this framework as their portfolios mature, provided they understand the structural tradeoffs each vehicle carries.

When big ASX news breaks, our subscribers know first

Liquidity is not just a convenience; it is a structural constraint

Liquidity determines how quickly and completely an investor can convert a position to cash. In direct property, that process is slow, binary, and market-dependent. In listed vehicles, it is fast, flexible, and incremental. The difference shapes every other decision in the comparison, including how long an investor can afford to hold a position that is underperforming.

Direct property settlement typically takes 4-6 weeks or longer in weak markets. There is no option to sell a quarter of a house. If capital is needed due to a job loss, a health event, or an unexpected opportunity, the choices are narrow: sell the entire asset, refinance, or wait.

A-REIT trades settle in T+2 on the ASX and can be executed in parcels as small as a few thousand dollars. An investor who needs to reduce exposure by 10% can do so during market hours without listing an asset, engaging an agent, or waiting for a buyer.

Unlisted trusts sit between the two. Redemption windows are commonly quarterly or semi-annual, but managers can and do restrict withdrawals during periods of market stress. For planning purposes, these should be treated as illiquid.

| Dimension | Direct property | A-REITs | Unlisted trusts |

|---|---|---|---|

| Typical exit timeline | 4-6 weeks minimum | T+2 settlement | Quarterly or semi-annual windows |

| Partial exit possible | No | Yes, in small parcels | Limited, subject to fund rules |

| Freeze risk in stressed markets | Slow sales, not formal freeze | None (exchange-traded) | Yes, managers may suspend redemptions |

An investor who may need access to capital within months, not years, faces a structural mismatch with direct property regardless of any other factor in the comparison.

Cost structures favour different capital bases

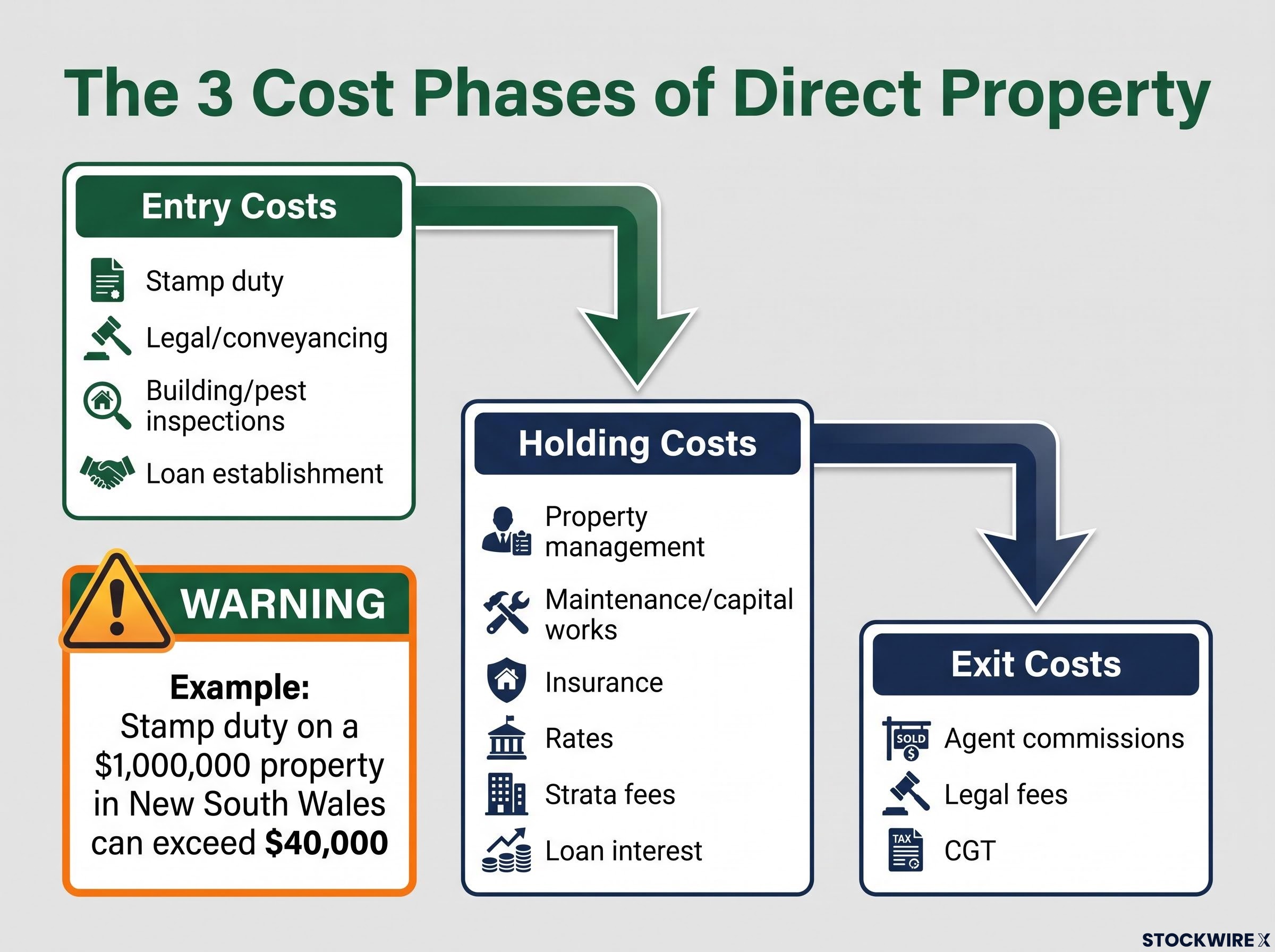

The true cost of each pathway extends well beyond the headline entry price. Direct property carries large, lumpy costs across three distinct phases, and failing to total them before committing capital is one of the most common errors in return forecasting.

The three cost phases of direct property:

- Entry costs: Stamp duty (significant and state-dependent), legal and conveyancing fees, building and pest inspections, and loan establishment fees.

- Holding costs: Property management fees (typically a percentage of gross rent), maintenance and capital works, insurance, council and water rates, body corporate or strata fees, and loan interest.

- Exit costs: Agent commissions, legal fees, and capital gains tax where applicable.

A-REITs carry a leaner structure. There is no stamp duty, no conveyancing, and no direct maintenance obligation. Management expense ratios for large diversified REITs tend to sit in the low single-digit percent per year range, absorbed before distributions are paid. Brokerage on ASX trades is typically small relative to position size.

Unlisted trusts often carry more complex and potentially higher fees, including entry fees, ongoing management and administration charges, and possible performance or exit fees.

For investors with smaller capital bases, avoiding stamp duty alone represents a meaningful structural advantage for listed property exposure. Stamp duty on a $1,000,000 investment property in New South Wales, for instance, can exceed $40,000, a cost that does not exist for an equivalent A-REIT position.

Net return, not gross yield, is what investors keep. A full cost accounting across all three phases often shifts the comparison materially compared to headline rental yield figures.

Understanding how each structure generates returns

Direct property and listed property vehicles generate returns through related but structurally different mechanisms. Treating them as equivalent because both involve “property” leads to expectation mismatches that catch investors off guard during rate cycles.

Direct property returns have two components. Rental income provides the cash flow, though gross yields in major Australian cities are often modest, and net yields fall further once management fees, repairs, insurance, rates, and vacancies are deducted. Capital growth has been strong over the long run nationally but remains highly uneven by city, suburb, and property type. Two properties bought in the same year in the same city can produce very different outcomes. Both components are heavily influenced by asset-specific factors: location, tenant quality, and management decisions.

Why listed property can feel like shares in a downturn

A-REIT returns combine distributions from pooled rental income (typically paid quarterly or semi-annually) with unit price movements. The distinction that catches many investors by surprise is that unit prices reflect market sentiment and interest rate expectations, not just underlying building values.

A-REIT unit prices can fall sharply even when the buildings in the portfolio have not been formally revalued. This occurs because investors reprice future cash flows when discount rates change, causing listed property to sell off before physical property markets move. This premium or discount to net tangible assets (NTA), where the traded price diverges from the assessed value of the underlying buildings, has no direct equivalent in physical property ownership.

During stress events, A-REITs often correlate more closely with the broader equity market than with direct property valuations. This is not a flaw in the structure; it is a feature of how listed markets incorporate information. But it means investors who expect listed property to track physical property values closely will be surprised by volatility that feels more like owning shares than owning buildings.

Leverage dynamics and the risk they concentrate

Leverage is the primary mechanism through which direct property has built wealth for Australian investors. But its structural form, whether personal and visible or embedded and pooled, determines how risk is distributed and who bears responsibility when conditions deteriorate.

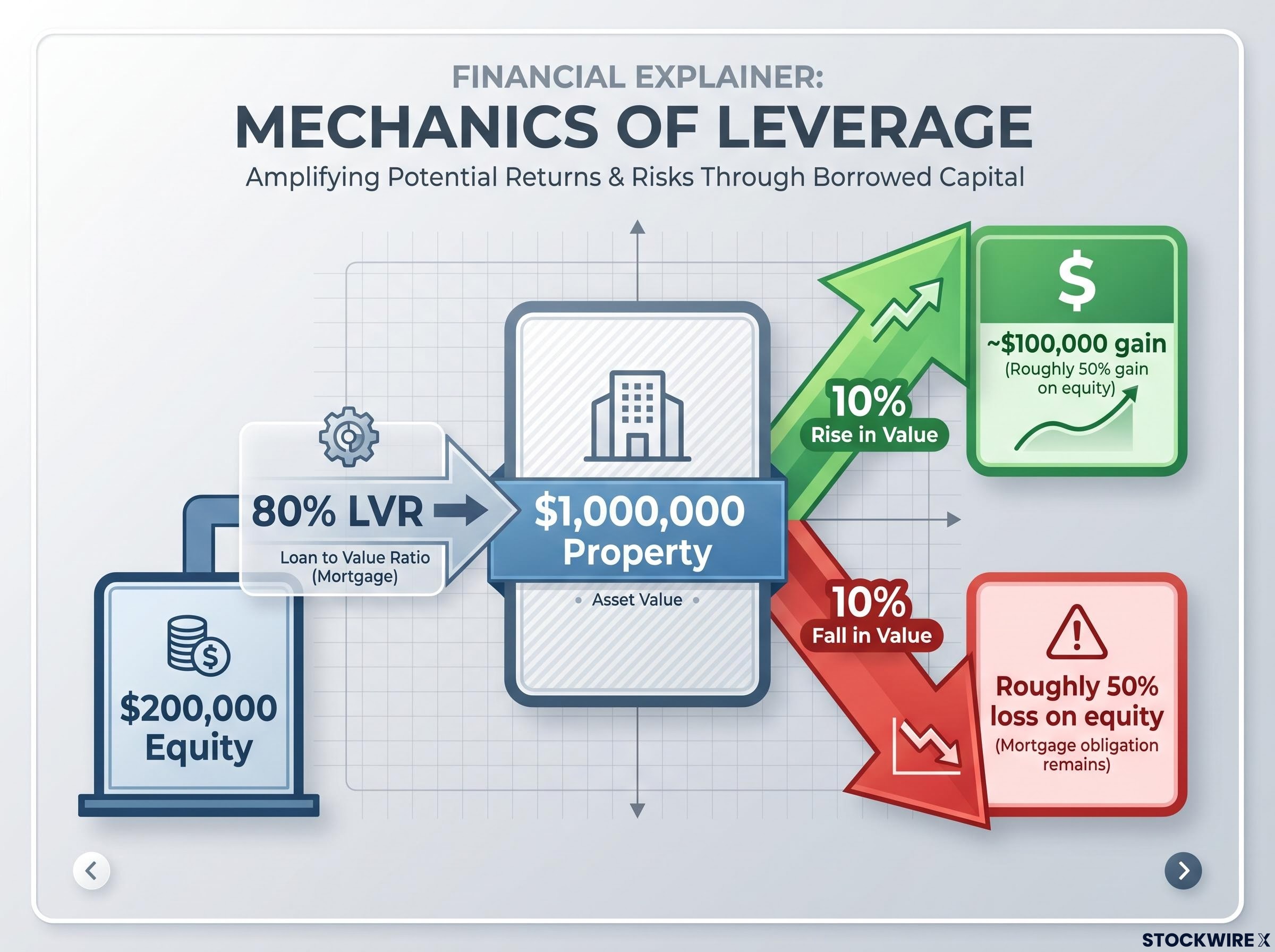

The mechanics of personal mortgage leverage in direct property:

- An investor commits $200,000 in equity.

- At 80% loan-to-value ratio (LVR), this equity controls a $1,000,000 property.

- A 10% rise in property value (approximately $100,000) represents roughly a 50% gain on the original equity.

- A 10% fall produces the same amplification in reverse, roughly a 50% loss on equity, and the obligation to service the mortgage remains regardless.

Negative gearing allows losses on a leveraged investment property to be offset against other income, which benefits investors on higher marginal tax rates. Combined with depreciation deductions, this tax treatment has made leveraged direct property particularly attractive to higher-income Australians.

Investment property tax changes announced in Australia’s 2026-27 Federal Budget, including the proposed removal of negative gearing on existing residential dwellings and replacement of the 50% CGT discount with cost base indexation, are already shifting the after-tax return calculus for leveraged direct property strategies before a single piece of legislation has been tabled, with the grandfathering cut-off date having already passed.

Embedded vs personal debt: a structural distinction most investors overlook

REITs borrow at the fund level. Investors gain exposure to leveraged property portfolios without personally servicing the debt. There is no personal margin call if asset values fall, but unit prices will reflect income or asset value pressure when rates rise or vacancies increase.

The absence of a personal debt obligation is a meaningful difference in risk profile, particularly for investors who could not comfortably service a mortgage through a prolonged vacancy period or a sustained rate increase. Layering personal margin loans over A-REIT positions is possible but concentrates risk significantly; this approach suits only sophisticated, risk-tolerant investors.

Which path fits your balance sheet, not just your temperament

The evaluative dimensions covered, liquidity, costs, return mechanics, leverage, and cycle behaviour, each point to a different weighting depending on the investor’s circumstances. The question is not which vehicle sounds more appealing but which one is structurally appropriate.

Conditions that favour direct property:

- Stable income capable of servicing debt through stress scenarios including higher rates and extended vacancies

- A time horizon of 7-plus years with no anticipated need for liquidity from that capital

- A higher marginal tax rate, where negative gearing and depreciation deductions provide meaningful after-tax benefits

- Comfort with concentrated, single-asset exposure and either the willingness to manage the property or the budget to delegate

Conditions that favour listed vehicles (A-REITs):

- A need for liquidity or flexibility within a shorter time horizon

- Preference for diversification across property sectors (industrial, retail, office, healthcare) and geographies

- No desire or capacity to take on personal mortgage debt

- Acceptance of market-driven price volatility in exchange for low-friction access and simple rebalancing

Unlisted trusts occupy a distinct position for investors seeking institutional-grade assets and income yields, provided they have genuine comfort with limited liquidity and complex fee structures.

How property exposure is owned can be as consequential to long-term outcomes as the underlying market the investor is exposed to. AEG’s concurrent deployment across direct and listed pathways reflects an institutional logic that many retail investors replicate at smaller scale as their portfolios mature.

Most experienced Australian investors will use both structures over a lifetime, with the balance shifting as capital base, income stability, and life stage evolve.

The structure decision deserves the same rigour as the asset decision

Property exposure is not a single investment category. It is a family of structurally distinct vehicles with meaningfully different risk, return, cost, and liquidity profiles. The five dimensions examined here, liquidity constraints, cost structures, return mechanics, leverage dynamics, and market cycle behaviour, each lead to a different weighting depending on the investor’s balance sheet, income, tax position, and time horizon.

As those inputs change over a career, the optimal blend of direct and listed exposure is likely to shift with them. Revisiting the structure decision periodically, with the same discipline applied to choosing the underlying assets, is itself a form of portfolio management that separates considered capital allocation from default assumptions.

For investors thinking beyond the direct versus listed property decision to the broader architecture of a wealth-building portfolio, our deep-dive into long-term wealth accumulation covers compounding mechanics, tax-sheltered structure selection, and the behavioural factors that cause most investors to underperform the strategies they have chosen, with worked illustrations across 10-20 year horizons.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.