Why Money Supply Growth Matters More Than Oil Prices

33 mins ago

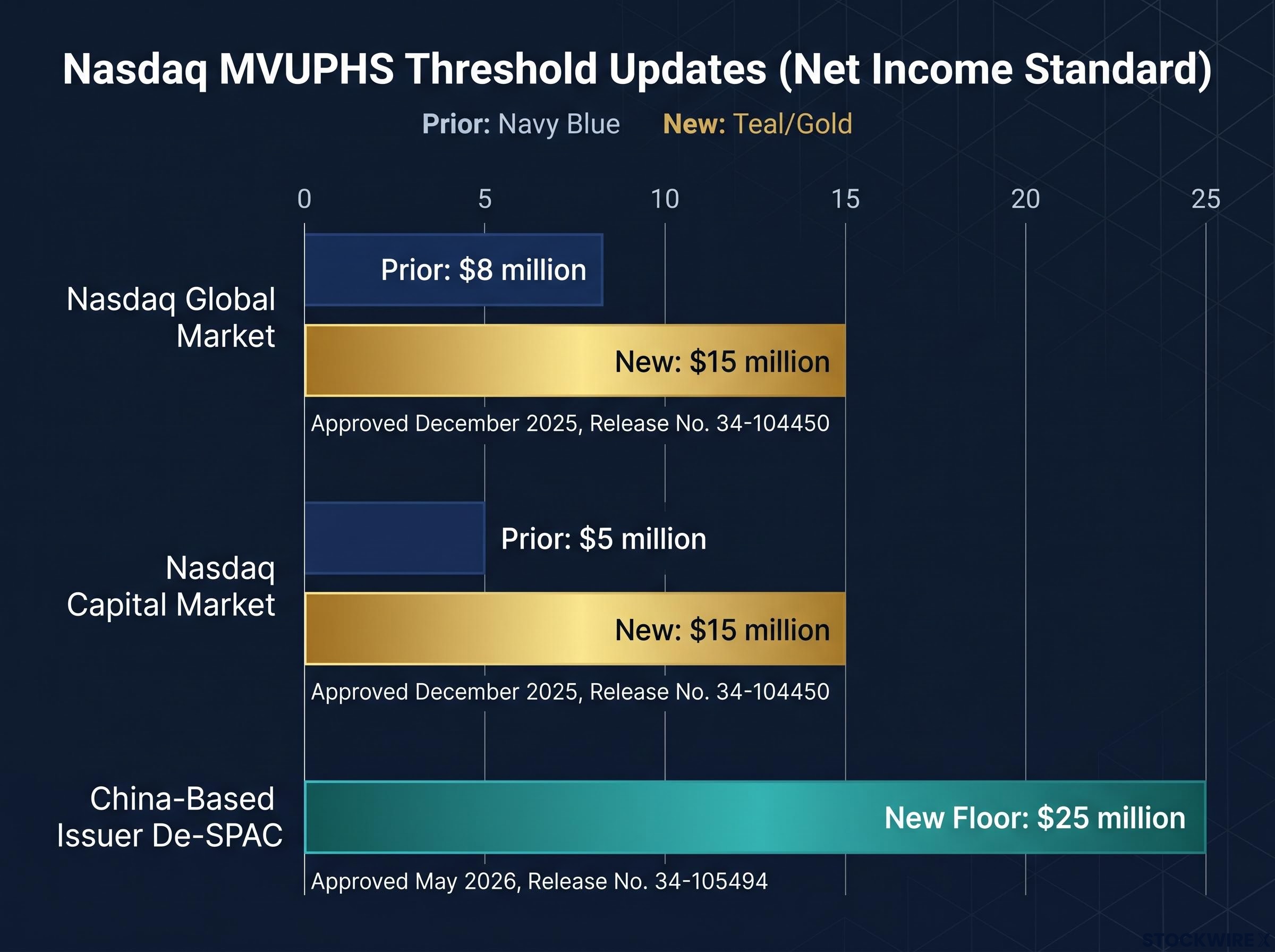

Nasdaq raised the float bar for companies listing under the Net Income Standard, and for mid-market issuers planning a De-SPAC transaction, the change lands directly in the deal structure. The revised threshold, approved by the SEC in December 2025 under Release No. 34-104450, requires at least $15 million in Market Value of Unrestricted Publicly Held Shares (MVUPHS), a measure of genuine day-one liquidity that was previously as low as $5 million on the Capital Market. This article explains exactly what changed, how Nasdaq calculates the threshold, why the SPAC structure creates specific complications and specific solutions, and what deal teams need to do differently from term sheet onward.

The amendment is narrow in scope but significant in consequence. Listing Rules 5405(b)(1)(C) and 5505(b)(3)(C) now require at least $15 million MVUPHS for companies applying the Net Income Standard on both the Nasdaq Global Market and the Nasdaq Capital Market. The prior thresholds were $8 million on the Global Market and $5 million on the Capital Market.

The table below summarises the shift.

| Market Tier | Prior MVUPHS Threshold | New MVUPHS Threshold |

|---|---|---|

| Nasdaq Global Market | $8 million | $15 million |

| Nasdaq Capital Market | $5 million | $15 million |

| Applicable to the Net Income Standard only. Market value, equity, and revenue/asset-based standards are unaffected. | ||

The SEC approved the change on an accelerated basis under File No. SR-NASDAQ-2025-068, and the rule became operative 30 days after approval, meaning its structuring implications have been live since early 2026.

Nasdaq listing rule changes in 2025-2026 have not been limited to the MVUPHS floor revision; the exchange’s fast-track rule, effective 1 May 2026, also accelerated the timeline for qualifying mega-cap companies to enter the Nasdaq-100 index, signalling a broader regulatory posture of adapting listing and index mechanics to the current IPO environment.

SEC Release No. 34-104450 granted accelerated approval to the Nasdaq rule amendment under File No. SR-NASDAQ-2025-068, setting out the regulatory basis for the revised MVUPHS thresholds and the 30-day operative timeline that brought the new structuring requirements into effect.

Nasdaq’s stated rationale: Companies meeting a $15 million MVUPHS floor are less likely to experience volatile trading and illiquidity than those listing with smaller floats.

Because only the Net Income Standard is affected, the first analytical step for any issuer is confirming which standard applies. Companies that qualify under a market value, equity, or revenue/asset standard face different thresholds and mechanics entirely.

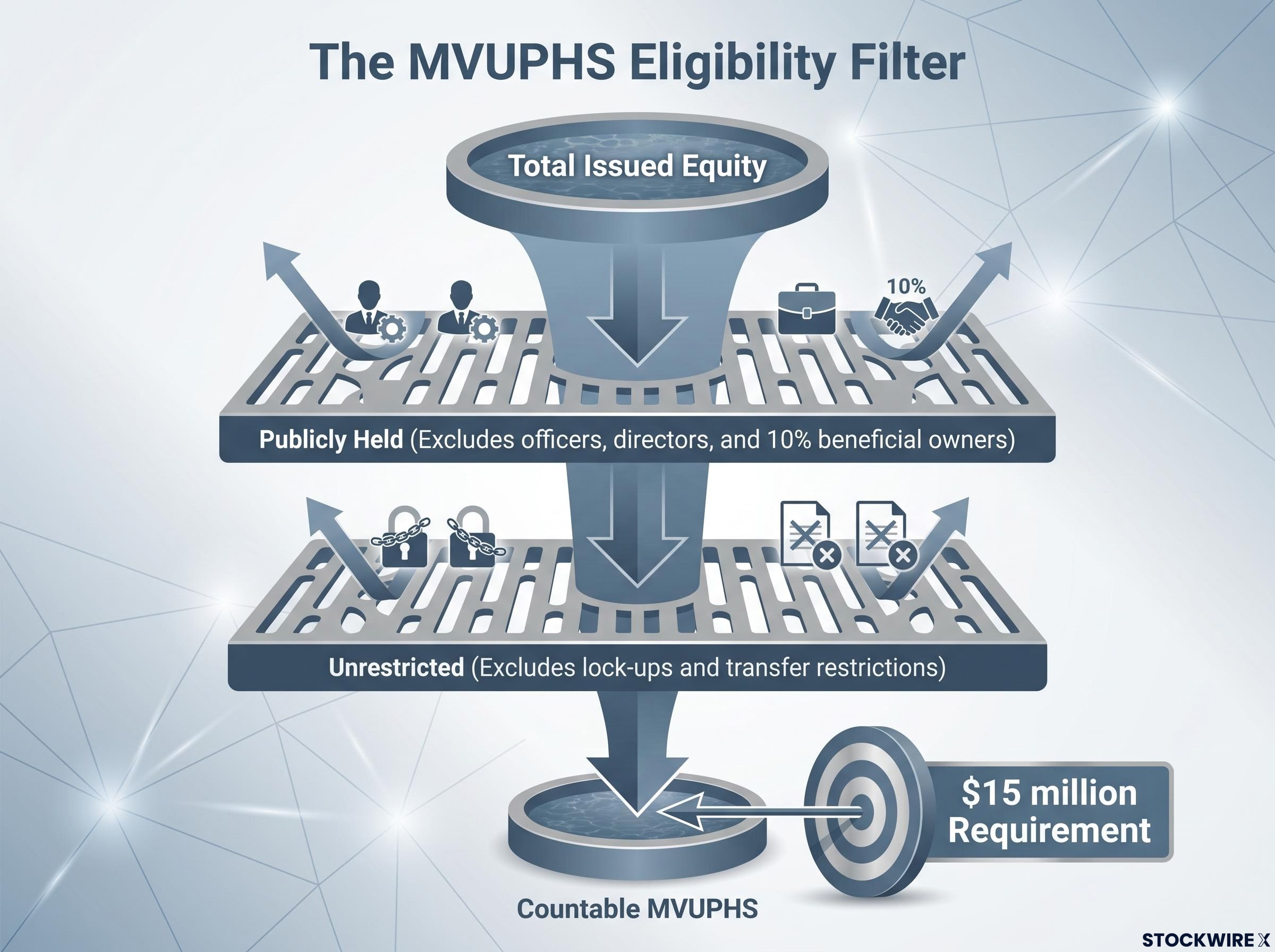

The number investors see most often, total market capitalisation, is not the number Nasdaq uses to assess float eligibility. MVUPHS applies a two-part filter that strips out equity that is technically issued but practically illiquid on day one. A share counts toward MVUPHS only if it satisfies both conditions simultaneously:

MVUPHS functions as a proxy for actual day-one liquidity. It measures the pool of free-trading stock that will genuinely be available to the market from the first moment of listing, not equity that exists on the cap table but cannot change hands.

IPO lock-up mechanics, including the standard period lengths, the insider categories subject to restriction, and the supply surge that follows expiry, form the same conceptual foundation that underlies the MVUPHS two-part eligibility filter, because both frameworks are ultimately measuring which shares are genuinely available to the market versus which are technically outstanding but practically frozen.

Nasdaq’s listing qualifications staff review the composition and calculation of MVUPHS as part of the initial listing application. What qualifies as unrestricted and publicly held in any specific structure is a question that benefits from early engagement rather than late-stage assumptions.

A company can have substantial total equity outstanding and still fall short of $15 million MVUPHS if insider ownership is concentrated and lock-ups are broad. This is not a hypothetical edge case; it is a common profile among mid-market De-SPAC candidates with enterprise values in the $100-$500 million range, where founder and sponsor holdings frequently account for a large share of outstanding equity.

Restricted shares, including unregistered PIPE shares without effective registration, are excluded until they become freely tradable. This creates a timing dimension to the float test that becomes directly relevant when structuring concurrent financings.

The De-SPAC format introduces a structural dynamic that both compresses and rebuilds the post-closing float. Understanding the sequence is the prerequisite for managing it.

Houlihan Capital SPAC redemption data for Q2 2025 recorded a median redemption rate of 99.6%, against a trailing three-year average of 96.6%, figures that illustrate how reliably high redemptions compress the post-closing float in transactions relying on legacy SPAC shares to meet the MVUPHS threshold.

The redemption dynamic is not a market accident. It is a structural feature of the SPAC format, and high redemption rates are a predictable float-compression force for any transaction relying on the Net Income Standard.

Float planning is a primary design constraint in a De-SPAC transaction, not a late-stage clean-up item.

The counter to this compression is the SPAC platform itself. A De-SPAC provides a pre-listed equity vehicle, a structured path through the public reporting regime (including the S-4 or F-4 registration process), and concurrent financing tools that give sponsors active levers to rebuild float. These tools do not exist in the same form on a conventional IPO timeline. The question is whether they are deployed early enough in the deal process to meet the $15 million floor under realistic, not optimistic, redemption assumptions.

De-SPAC deal termination can itself become a strategic tool when the original SPAC sponsor is not aligned with the target’s valuation expectations; Ovanti’s exit from the Miluna transaction in March 2026 and its subsequent pivot to larger Nasdaq-focused sponsors illustrates how float and valuation mismatches surface before closing and force structural reconsideration.

The most common tool for backstopping SPAC redemptions is a PIPE financing. The problem is that “we will do a PIPE” is not a complete answer to the float question. The structure of the PIPE determines whether it actually solves the problem.

PIPE investors at closing typically receive unregistered shares with registration rights. Until a resale registration statement covering those shares is filed and declared effective, the shares are restricted and do not count toward MVUPHS. If the transaction relies on PIPE shares to reach $15 million, the registration statement must be effective by the time Nasdaq tests MVUPHS for initial listing. Registration rights filing and effectiveness deadlines must therefore be drafted with the listing timeline in the room, not treated as a post-closing administrative item.

An affiliate exclusion compounds the issue. PIPE investors who are affiliates or who reach 10% beneficial ownership at closing are excluded from the publicly held calculation regardless of their registration status. Investor identity and sizing matter alongside timing.

Beyond PIPE shares, several additional instruments can contribute to MVUPHS, each subject to the same two-part test:

The registration rights timeline is where many De-SPAC float plans silently break down. The deal team commits to a structure that assumes PIPE shares will count, without confirming that registration effectiveness will precede the listing date. Understanding this dependency converts a hidden risk into a manageable scheduling constraint.

For companies with principal operations in China (including Hong Kong and Macau) going public via De-SPAC, the $15 million analysis is the floor of a more demanding standard, not the ceiling.

The post-combination company must have at least $25 million MVUPHS, explicitly excluding shares subject to resale restrictions.

This China-specific requirement was approved in May 2026 under SEC Release No. 34-105494 and is now in effect. The $25 million floor is 67% higher than the general $15 million Net Income Standard requirement.

The two China-specific thresholds sit side by side:

Every element of float structuring discipline described in the prior sections applies at this higher threshold. Deal teams advising on cross-border De-SPAC transactions involving China-based operating companies need to apply the $25 million standard from the outset. Discovering it mid-process after structuring around $15 million creates significant rework and potential deal timeline risk.

The starting point is listing standard selection. If the combined company can satisfy a market value, equity, or revenue/asset standard, the applicable MVUPHS threshold and mechanics may differ. If the Net Income Standard is the only viable path, the $15 million floor (or $25 million for China-based targets) is binding from term sheet.

Five structuring decisions, ordered by when each becomes live in the deal timeline, jointly determine whether a De-SPAC transaction meets the MVUPHS threshold:

Staggered lock-up structures, which release insider shares in tranches rather than all at once at a fixed post-listing date, have been adopted by a growing number of De-SPAC and conventional IPO issuers as a mechanism to reduce concentrated selling pressure, and their design directly affects how MVUPHS evolves in the months following listing as tranches unlock and previously restricted shares become freely tradable.

Deal teams should initiate dialogue with Nasdaq’s listing qualifications staff before deal terms are finalised. The specific question to resolve is how the staff will treat particular share classes, PIPE structures, and lock-up arrangements in the MVUPHS calculation for the specific transaction at hand.

Early engagement converts structuring assumptions into confirmed positions. It reduces the risk of MVUPHS shortfalls discovered during the listing application review, when the cost of structural adjustment is highest and the deal timeline is least forgiving.

The $15 million MVUPHS requirement under the Net Income Standard is a structuring constraint, not a prohibition. De-SPAC transactions remain viable for mid-market issuers, and the SPAC format’s concurrent financing tools are well-suited to meeting the higher float floor when deployed deliberately from the outset.

What shifts is the architecture of deal readiness. Float planning moves from a pre-closing compliance task to a front-end design objective, touching listing standard selection, SPAC sizing, PIPE structuring, registration rights drafting, and lock-up design simultaneously. For China-based targets, the $25 million floor compounds every element of that discipline.

The rule raises the bar for uncoordinated deal execution while leaving the path open for teams that address float requirements as a primary structural variable from term sheet onward. Deal professionals working through a De-SPAC process should treat the new thresholds as a prompt to revisit float modelling and PIPE registration timelines now, and to open Nasdaq engagement earlier than previously necessary.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Nasdaq now requires at least $15 million in Market Value of Unrestricted Publicly Held Shares (MVUPHS) for companies listing under the Net Income Standard on both the Nasdaq Global Market and the Nasdaq Capital Market, up from prior thresholds of $8 million and $5 million respectively.

MVUPHS stands for Market Value of Unrestricted Publicly Held Shares; it counts only shares that are both publicly held (not owned by officers, directors, or 10%-or-greater beneficial owners) and unrestricted (not subject to any lock-up or transfer restriction at the time of listing), making it a measure of genuine day-one liquidity rather than total market capitalisation.

When SPAC investors redeem their Class A shares before a De-SPAC deal closes, the post-closing non-redeemed share count shrinks significantly; with median redemption rates near 99.6% in Q2 2025, the legacy SPAC float alone frequently falls below the $15 million MVUPHS threshold, requiring additional float sources such as PIPE financing.

PIPE shares only count toward MVUPHS after the resale registration statement covering those shares has been filed and declared effective; unregistered PIPE shares with pending registration rights are treated as restricted and are excluded from the calculation until that registration is effective.

China-based issuers (including those with principal operations in Hong Kong and Macau) completing a De-SPAC transaction face a $25 million MVUPHS floor, approved in May 2026 under SEC Release No. 34-105494, which is 67% higher than the general $15 million Net Income Standard requirement.