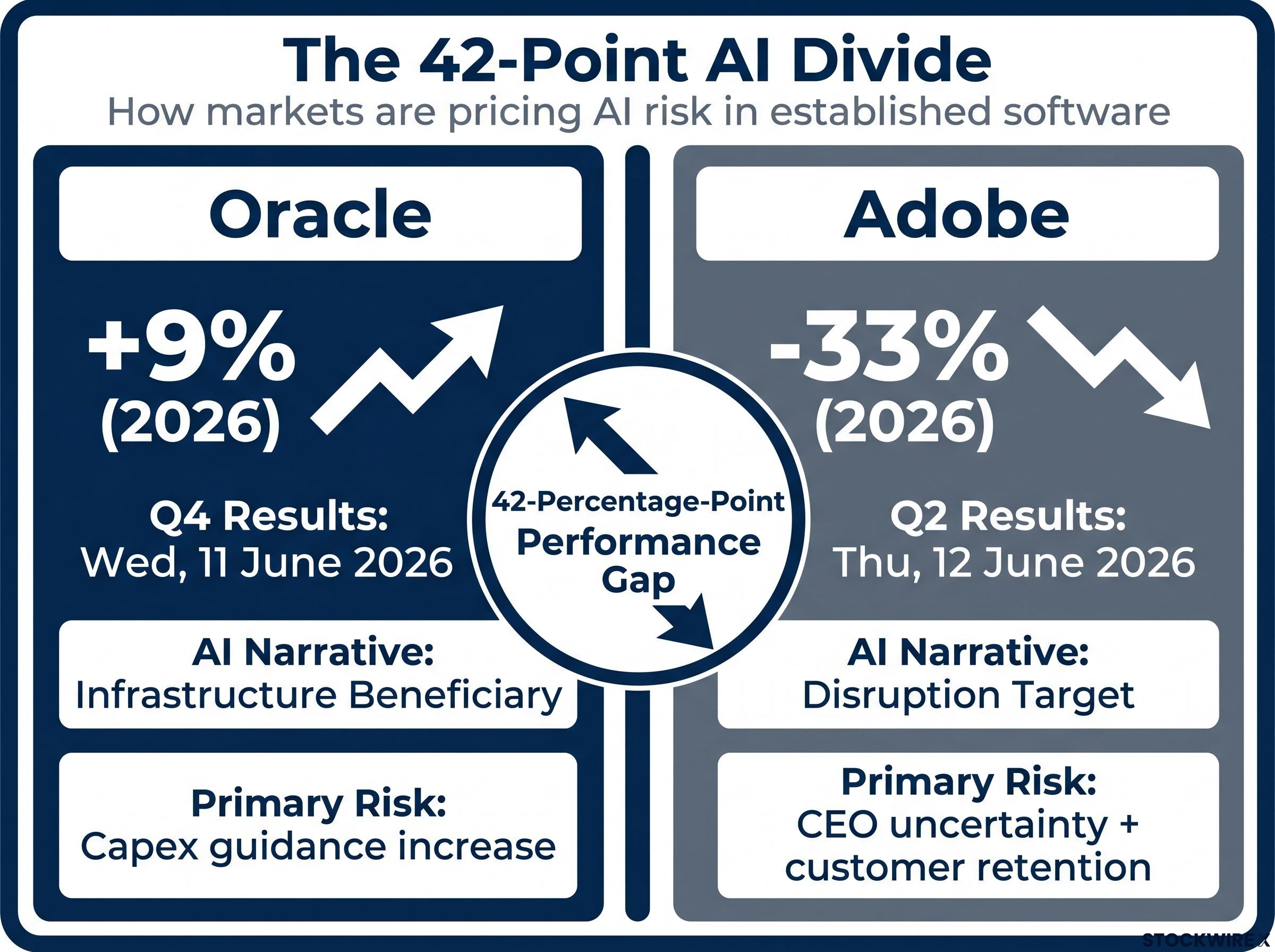

Within a 24-hour window this week, two of enterprise technology’s most watched names will report earnings on opposite sides of the AI trade. Oracle releases fourth fiscal quarter results after market close on Wednesday, 11 June 2026; Adobe follows with second fiscal quarter results after close on Thursday, 12 June 2026. The timing concentrates two divergent AI narratives into a single stress test, arriving just as Broadcom’s recent disappointing results and stronger-than-expected U.S. employment data have raised the probability of a Federal Reserve rate increase, putting fresh pressure on every AI-exposed equity. What follows is an assessment of what analysts are watching in each report, why two companies operating in the same era have landed on opposite sides of the AI investor narrative, and what a 42-percentage-point gap in their 2026 share price performance reveals about how markets are pricing AI risk in established software businesses.

Why this earnings window has become a referendum on AI software valuations

Neither stock enters this week on neutral ground. Three macro-level developments have elevated the stakes before either company says a word:

- Broadcom’s disappointing results shook confidence in the durability of AI-sector earnings momentum, prompting investors to reassess valuations across adjacent names.

- Strong U.S. employment data landed in the same window, pushing expectations for a Federal Reserve rate increase higher and compressing the multiple investors are willing to pay for growth-oriented technology stocks.

- Rate sensitivity and AI equity valuations are now colliding directly: higher-for-longer rate expectations raise the discount rate applied to future earnings, and AI infrastructure stories rely heavily on forward earnings visibility to justify current prices.

Fed rate hike probability forecasts shifted materially in the days leading into this earnings window, with major investment banks revising their FOMC expectations upward after the stronger-than-expected payrolls print, amplifying the discount rate pressure on growth-oriented technology valuations.

The concentration of two major AI-narrative reports within 24 hours is unusual. Oracle and Adobe sit at opposing poles of the same investment theme, meaning the two evenings will function as a back-to-back verdict on whether AI is creating or destroying value in enterprise software.

When big ASX news breaks, our subscribers know first

Oracle’s AI infrastructure bet and the one number that could unsettle it

Oracle shares have gained more than 9% in 2026, and the recent earnings trajectory supports the move. The company’s Q3 FY2026 results, reported on 10 March 2026, delivered earnings per share of $1.79 against a consensus estimate of $1.71, on revenue of $17.19 billion. Full-year FY2026 revenue guidance stands at approximately $67 billion, underpinned by cloud and AI-driven growth.

Analysts at Evercore ISI identify three conditions that could carry Oracle shares through the summer:

- Delivering clean quarterly results that extend the recent beat streak

- Reaffirming revenue growth acceleration projections for fiscal years 2027 and 2028

- Providing clarity on a previously announced equity raise

Each item reinforces the same thesis: that Oracle is positioned as an infrastructure beneficiary of the AI buildout, with demand for cloud, database, and compute capacity increasing as enterprise customers scale AI workloads.

The distinction between surface-level and infrastructure-level enterprise AI adoption matters here because Oracle’s cloud and database services benefit specifically from customers that have crossed the threshold into genuine workload integration, not merely pilot-stage experimentation that generates headlines but limited incremental compute demand.

What forward guidance language will mean more than the headline number

The quarterly earnings figure itself may matter less than what management says about FY2027 and FY2028 revenue acceleration. Investors are treating forward guidance as the real signal about whether AI infrastructure demand is durable or plateauing.

Evercore ISI analysts identify the primary downside risk as a potential increase in capital expenditure guidance, which could constrain upside by raising concerns about margin pressure and the pace of return on AI infrastructure investment.

A strong quarter paired with higher capex guidance would force investors to weigh near-term margin compression against long-term revenue acceleration. That tension, not the headline earnings number, is where the market’s reaction will be decided.

AI infrastructure suppliers across power and optical networking have posted 90-130% revenue growth in the first half of 2026, a rate that illustrates the scale of capital flowing into the buildout that Oracle is competing to serve with its cloud and database capacity.

What a 33% share price decline and a CEO departure say about AI disruption risk

Adobe shares have fallen more than 33% in 2026. The decline did not follow a missed quarter. Adobe’s Q1 FY2026 results, reported on 12 March 2026, showed earnings per share of $6.06, beating consensus, on revenue of $6.40 billion. The stock is down on something more structural.

Generative AI tools have proliferated rapidly across Adobe’s core product categories:

- Design software, where image generation tools offer direct substitution

- Video production, where AI-assisted editing and generation are accelerating

- Audio editing, where synthetic voice and sound tools are maturing

- Document management, where AI-powered automation reduces reliance on legacy workflows

Adobe has encountered difficulty attracting and retaining customers during the current AI adoption era, and the share price reflects a sustained reassessment of the business model rather than a single earnings miss.

The legacy software repricing that unfolded across early 2026 offers the structural context for why Adobe’s decline is not an isolated story: the $2 trillion in wealth destruction recorded across US software markets concentrated almost entirely in per-user licensing businesses where AI substitution risk is highest.

The departure of Shantanu Narayen, announced in March 2026 after 18 years as chief executive, compounded the pressure. The succession search, led by Frank Calderoni, is considering both internal and external candidates. Narayen has committed to remaining until a successor is named, after which he will transition to board chair. The market is not treating the leadership question and the AI strategy question as separate concerns; they are the same problem.

Adobe’s official CEO transition announcement confirmed that Frank Calderoni would lead the search for Narayen’s replacement, with Narayen committing to remain in post until a successor is named before transitioning to board chair.

What analysts actually expect from Adobe’s results, and why the CEO question matters more

Analysts at Jefferies expect few material surprises from the quarterly numbers. The baseline expectation is modest outperformance versus guidance and a reaffirmation of full-year 2026 targets. As an earnings event, the financial results alone are unlikely to move sentiment materially.

The CEO question is different. A naming of Narayen’s successor around the 12 June event is identified by analysts as the single development most likely to shift investor positioning.

Goldman Sachs has dated the AI software revenue thesis to 2027, with analyst Gabriela Borges identifying Microsoft and ServiceNow as the only companies currently producing quantified additive AI revenue evidence; by that standard, Adobe’s qualitative AI disclosures place it in the majority of software names still unable to separate AI-driven growth from the base business trajectory.

Jefferies analysts expect that a CEO announcement could carry more market weight than the financial results themselves, given that the leadership decision is inseparable from the question of whether Adobe will defend its existing model or reposition for the AI era.

Investors are not simply asking who leads Adobe next. They are asking whether the new leader will accelerate a strategic pivot or attempt to protect the subscription revenue model that generative AI is eroding. The income statement may confirm what is already known. The CEO answer, if it arrives, could reframe the entire investment thesis.

Oracle and Adobe as mirror images of where AI creates and destroys software value

The two companies have both beaten recent earnings consensus. The divergence in share price is not a fundamentals story. It is a narrative story.

| Dimension | Oracle | Adobe |

|---|---|---|

| 2026 share performance | +9% | -33% |

| AI narrative positioning | Infrastructure beneficiary | Disruption target |

| Primary analyst risk | Capex guidance increase | CEO uncertainty + customer retention |

| CEO / leadership status | Ellison active; no succession | Narayen departing; search underway |

| Key positive catalyst | Revenue acceleration guidance + equity raise clarity | CEO naming + full-year target reaffirmation |

Both companies face AI-related uncertainty, but the direction of that uncertainty runs opposite. Oracle is questioned on how much it will cost to win. Adobe is questioned on whether it can survive the disruption. That structural difference explains a 42-percentage-point performance gap between two companies that have both beaten earnings.

What the AI era means for established software businesses, and how to read this week’s results

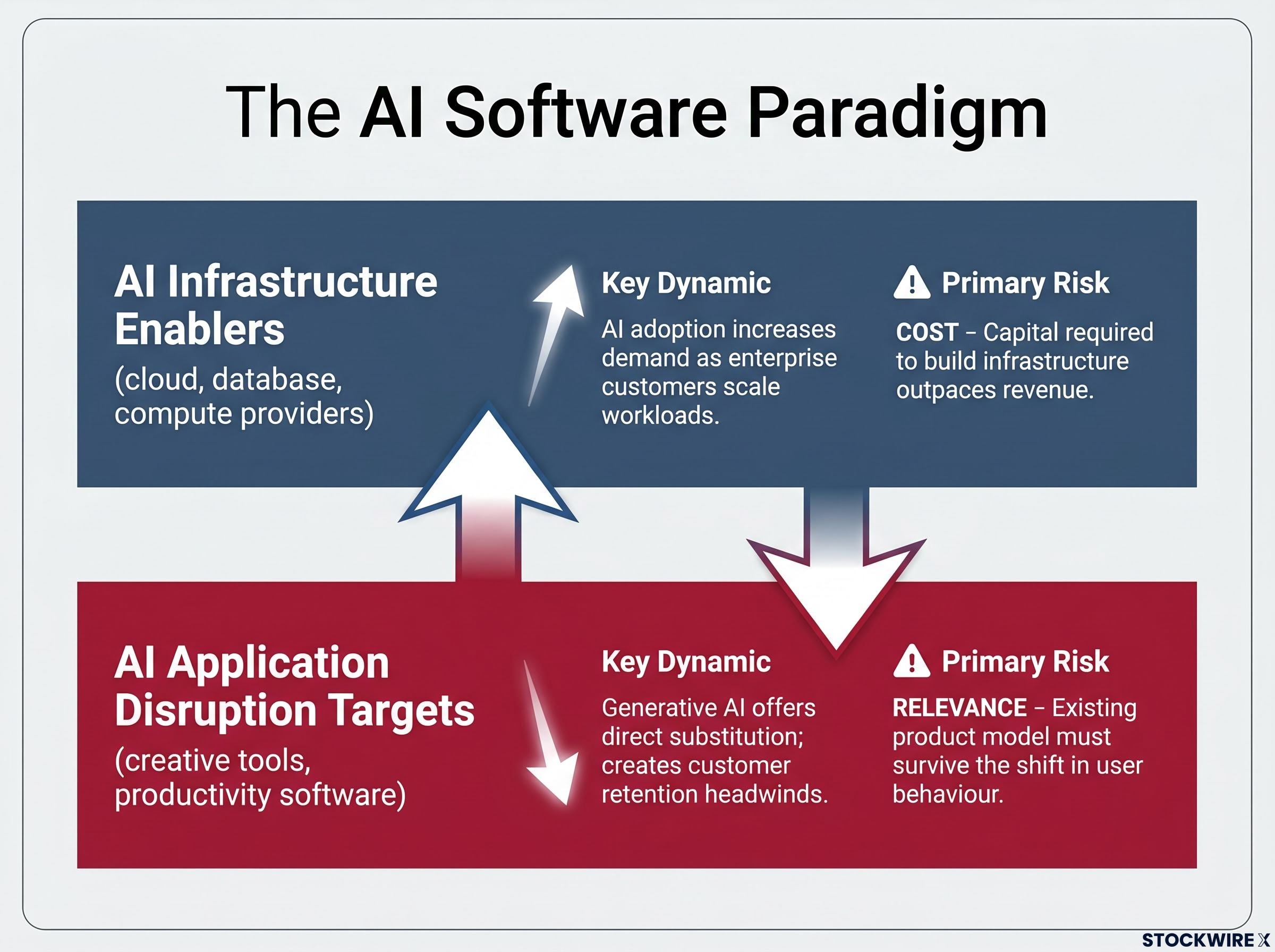

The same AI wave can simultaneously create new infrastructure demand and erode existing application demand. The distinction depends on where a company sits in the technology stack.

AI infrastructure enablers (cloud, database, compute providers):

- AI adoption increases demand for their core products

- Revenue growth accelerates as enterprise customers scale workloads

- Primary risk is cost, specifically whether the capital required to build infrastructure outpaces the revenue it generates

AI application disruption targets (creative tools, productivity software):

- Generative AI tools offer direct substitution for their core products

- Customer acquisition and retention face structural headwinds

- Primary risk is relevance, specifically whether the existing product model survives the shift in user behaviour

Applying the framework to Oracle and Adobe this week

Oracle sits squarely in the infrastructure layer. Its cloud and database services become more valuable as AI workloads grow. The investor question is about cost, not survival. Adobe sits in the application layer, where generative AI tools are replicating capabilities that customers previously purchased through subscriptions. The investor question is about whether the business model endures.

This framework extends beyond the two companies reporting this week. Any software business can be assessed by asking: does AI increase demand for what this company sells, or does AI replicate what this company sells?

The results arrive in a market that has already decided which story it believes

The market has priced Oracle as a winner and Adobe as a casualty. A 9% gain and a 33% decline represent a pre-results verdict that will take more than a single quarter to reverse.

Confirmation would look like Oracle clearing the capex concern, delivering FY2027 and FY2028 acceleration language, and providing equity raise clarity. For Adobe, confirmation would mean holding full-year targets and, more importantly, naming a successor to Narayen. Anything short of those conditions extends the existing narratives rather than disrupting them.

The broader context matters. Broadcom’s recent stumble and rising Fed rate expectations have tightened the margin for error across all AI-exposed equities. How Oracle and Adobe land this week will influence not just their own share prices but investor sentiment toward the wider AI software sector for the months ahead. The two-day window is concentrated, and the market is watching both reports as a single test of whether the AI investment thesis holds where it counts: in the earnings of the companies building and defending against it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.