When to Sell Winning Stocks: the Framework Investors Get Wrong

31 mins ago

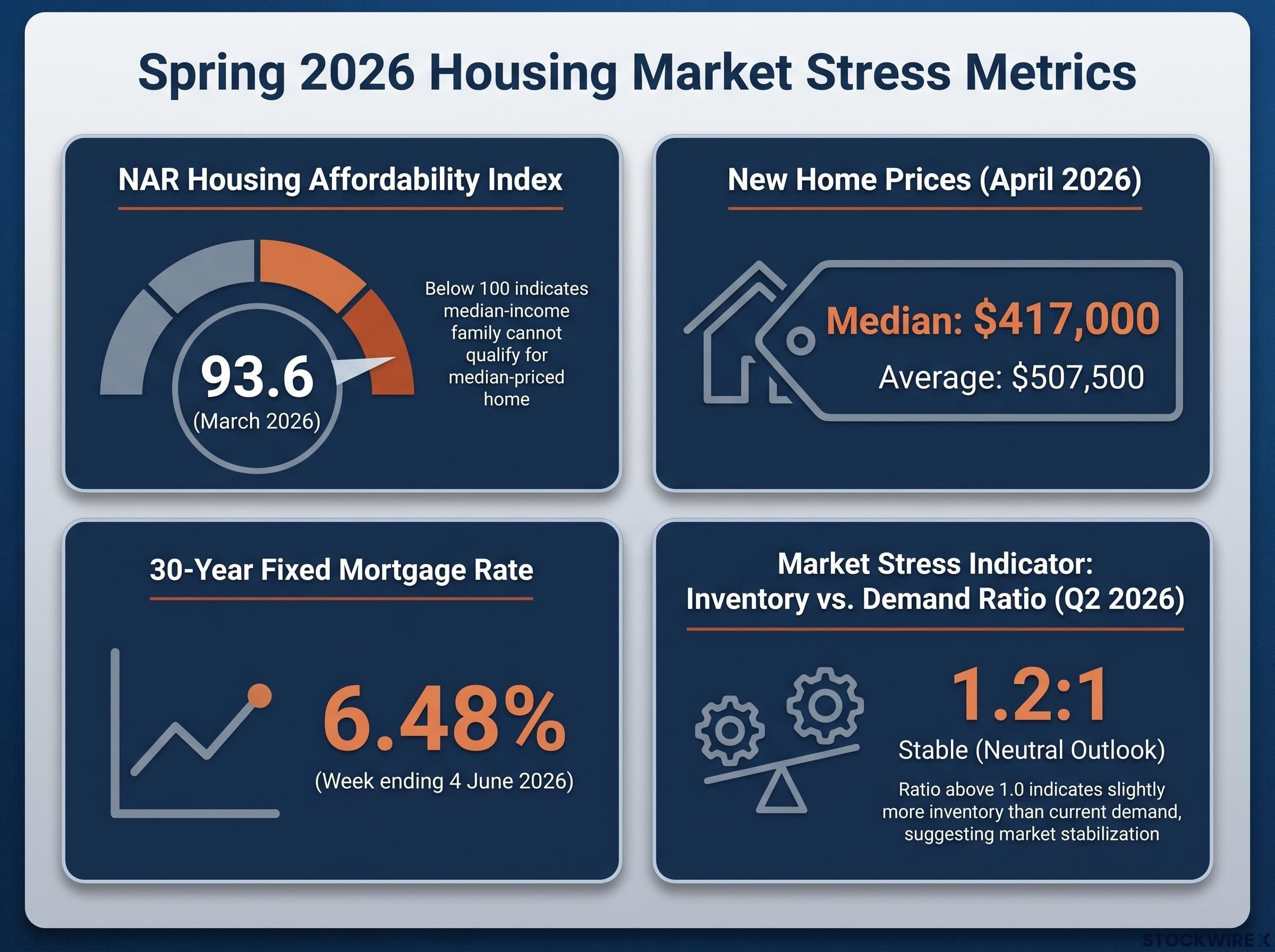

The NAR Housing Affordability Index fell to 93.6 in March 2026, meaning a median-income American family generally cannot qualify for a mortgage on a median-priced home. That single data point captures the demand side of the thesis Dan Loeb has built against US homebuilders. But demand is only one layer. The Third Point CEO has identified homebuilding as one of the last sectors still trapped in post-pandemic pricing and cost distortions, and his short thesis is not primarily a rate call or a demand call. It is a structural argument about how builders misrepresent their capital commitments and about the margin compression already visible in reported financials. What follows breaks down the Third Point thesis layer by layer, examines the accounting mechanics at its core, weighs the strongest counterarguments from Goldman Sachs and JPMorgan, and offers a framework for evaluating short theses in capital-intensive cyclical industries.

The problems Loeb identified are not emerging. They are already present in the financials.

Third Point began implementing its homebuilder short thesis roughly a year before Loeb discussed it publicly, framing the position as a reaction to observable structural impairment rather than a forecast of future decline. The thesis rests on three interconnected pillars:

The U.S. Census Bureau new residential sales data provides the primary official record of median and average new home prices, sales volumes, and months of supply, giving investors the benchmark figures against which builder guidance and sell-side estimates should be evaluated.

NAR Housing Affordability Index: 93.6 (March 2026) A reading below 100 indicates that a family earning the median income generally cannot qualify for a mortgage on the median-priced existing home. The index has remained below the qualification threshold, signalling persistent buyer affordability stress.

The structural framing matters because it changes the conditions for resolution. A cyclical short ends when rates fall or demand rebounds. A structural short persists until the underlying cost and capital misalignment works through the system, a process that typically takes longer and cuts deeper.

The affordability stress captured by the NAR index sits alongside a separate and counterintuitive dynamic: housing market decoupling from broader economic performance has become a recurring theme in 2026, with homebuilder ETFs posting positive year-to-date returns even as new single-family sales recorded their steepest monthly decline since 2013.

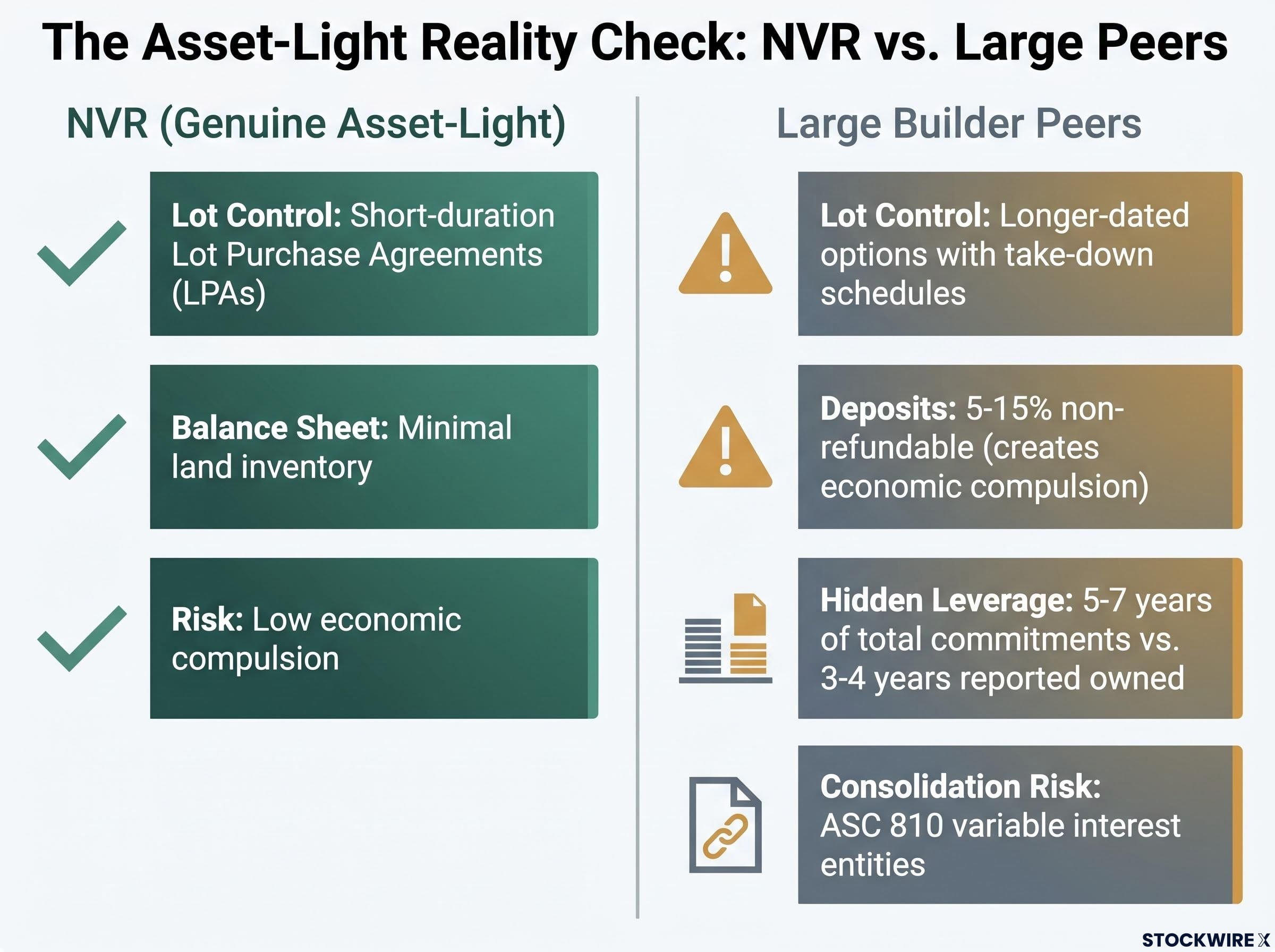

The asset-light label has become a selling point for homebuilders pitching investors on capital efficiency. The question is whether the label matches the economic reality underneath it.

NVR built its model around short-duration Lot Purchase Agreements (LPAs) with developers, acquiring finished lots close to production rather than carrying raw land on the balance sheet. The result: minimal land inventory, high returns on capital, and low financial leverage. Morningstar and CFRA note that NVR’s approach depends on deep developer relationships, strong order visibility, and dominant local scale, conditions that are not easily replicated across all markets by peers.

Most large builders adopted the language of NVR’s model without replicating its mechanics. Their option contracts frequently require non-refundable deposits of 5-15% of land value, according to UBS analyst commentary. Those contracts include predefined take-down schedules, meaning builders must close on lots in quarterly tranches over several years or forfeit deposits and risk legal disputes.

This creates economic compulsion. Builders are motivated to close on optioned lots even in deteriorating markets to protect deposits and developer relationships, behaving like land owners regardless of what the balance sheet shows. Moody’s notes that total land commitments (owned plus controlled) often represent 5-7 years of deliveries, even when builders report only 3-4 years of owned land supply.

UBS analysts further note that optioned land may need to be consolidated on balance sheets if developers are deemed variable interest entities under ASC 810, which governs how entities with limited equity or dominant financial backers must be reported. If that consolidation occurs, the asset-light narrative unwinds in a single filing.

| Feature | NVR (genuine asset-light) | Large builder peers |

|---|---|---|

| Lot control method | Short-duration LPAs with developers | Longer-dated options with take-down schedules |

| Deposit terms | Flexible, close-to-production | Non-refundable deposits (5-15% of land value) |

| Balance sheet treatment | Minimal land inventory | Options recorded as contract assets; full exposure may be off-balance-sheet |

| Economic compulsion risk | Low; flexible terms and short duration | High; deposit forfeiture and schedule obligations compel take-down |

If the asset-light framing is wrong, the valuation built on it is wrong. That is the accounting core of Loeb’s thesis.

The margin data functions as the real-time scorecard. It shows whether the compression Loeb identified is accelerating, stabilising, or reversing.

| Builder | Most recent gross margin | Quarter reported | Direction |

|---|---|---|---|

| Lennar | 15.2% | Q1 FY2026 (ended 28 February 2026) | Compressing |

| PulteGroup | 24.4% | Q1 FY2026 (ended 31 March 2026) | Compressing from peaks |

| D.R. Horton | ~20.4% | Fiscal Q1 FY2026 (ended 31 December 2025) | Compressing |

Lennar’s 15.2% homebuilding gross margin is the sharpest compression among the three, with net earnings of $229 million and diluted EPS of $0.93 for the quarter. PulteGroup reported net income of $347 million and diluted EPS of $1.79, while D.R. Horton posted net income of $594.8 million and diluted EPS of $2.03 for its fiscal first quarter.

All three margins sit below their 2021-2022 cycle peaks. JPMorgan equity research frames the compression as 150-300 basis points from those peaks, while noting that margins still sit 300-500 basis points above 2015-2019 norms, a range the bank attributes to structural improvement rather than purely cyclical forces.

The bull-bear tension in one data point: JPMorgan frames current margins as compressed from peaks but still structurally above pre-pandemic norms, suggesting the industry has made genuine efficiency gains. The bear case argues that incentives and rate buydowns are masking the true rate of deterioration.

Evercore ISI and Bank of America housing research reinforce that point. Rate buydowns, closing cost incentives, and design-centre credits are sustaining headline sales pace, but they function as de facto price cuts, eroding underlying margins even when list prices hold.

The bull case is not a dismissal of Loeb’s observations. It is a structurally grounded alternative framework that explains why large builders have not collapsed despite visible margin pressure.

Single-family supply dynamics reinforce part of the bull case: stabilising mortgage rates have supported refinancing activity and limited forced selling, while multifamily commercial properties face a distinct set of pressures from maturity walls and oversupply that do not apply to the new-construction market Loeb is targeting.

Berkshire’s Taylor Morrison acquisition, announced at a 24% premium to market and representing Greg Abel’s largest deal as CEO, provides the most direct institutional counterpoint to Loeb’s thesis: Berkshire assessed Taylor Morrison’s 8.79x price-to-earnings ratio as undervalued relative to intrinsic value at a moment when Third Point sees structural impairment across the sector.

These counterarguments explain why a homebuilder short requires precise timing and specific catalyst identification. The structural demand floor is real. The question is whether it is large enough to offset the margin compression and capital misrepresentation that Loeb’s thesis targets.

Loeb himself has cautioned that purely valuation-based short selling is dangerous, citing instances where logically overvalued stocks were driven higher by momentum. Structural impairment shorts require a different evaluation process. The following five questions apply to any capital-intensive sector where asset-light narratives are in play:

Cyclical sector positioning in late-cycle conditions typically involves reducing exposure as margin compression signals a turn, but the homebuilder case complicates that framework because the sector’s structural supply deficit gives it a demand floor that most cyclicals lack, making the standard playbook harder to apply mechanically.

The homebuilder case is not unique. The pattern of asset-light narratives unravelling under cycle stress recurs across capital-intensive industries:

Loeb’s invocation of the Jesse Livermore principle, that nothing is entirely new, anchors the point. When management teams emphasise flexibility and light capital structures, the historical record suggests the stress test is not whether those descriptions hold in good markets but whether they survive the turn.

The structural problems Loeb identified, the cost trap, capital misrepresentation, and margin compression, are already visible in reported financials. Lennar’s 15.2% gross margin and the sector-wide reliance on rate buydowns to sustain volume confirm that the dynamics are in motion, not hypothetical. At the same time, the demand floor from chronic undersupply and demographic tailwinds is genuine, and it makes the timing of any sharp dislocation uncertain.

That tension is what separates a well-constructed structural short from a speculative macro bet. The former is anchored in identifiable accounting and capital mechanics. The latter relies on a specific price or rate outcome materialising on schedule.

For investors monitoring this thesis, the practical tracking indicators are gross margin trends, incentive intensity, and land impairment disclosures in quarterly earnings from Lennar, D.R. Horton, and PulteGroup. Changes in incentive language and directional margin shifts are the leading indicators of whether the cost trap is tightening or easing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Dan Loeb's Third Point argues that major US homebuilders are structurally impaired due to cost inflation, margin compression, and a misleading asset-light narrative that obscures the true scale of land commitments, making their valuations vulnerable even before any cyclical demand downturn.

A reading below 100 means a median-income American family generally cannot qualify for a mortgage on the median-priced home, signalling persistent buyer affordability stress that constrains demand and supports the bear case on homebuilder revenue and margins.

Large builders use the asset-light label because they control land through option contracts rather than outright ownership, but those contracts typically require non-refundable deposits of 5-15% and predefined take-down schedules, creating economic compulsion to close on lots that functions like fixed capital ownership regardless of balance sheet treatment.

Bulls point to a multi-million-unit structural housing deficit from years of underbuilding, strong demographic demand from Millennials and Gen Z entering prime buying ages, and balance sheets with lower net leverage than pre-2008 cycles, all of which provide a demand floor that makes timing a sharp dislocation difficult.

Investors should monitor gross margin trends, the intensity of rate buydowns and closing cost incentives, and land impairment disclosures in quarterly earnings from Lennar, D.R. Horton, and PulteGroup, as directional shifts in these figures are the leading indicators of whether the cost trap is tightening or easing.