Most retail investors treat an IPO as the moment insiders cash out and leave the table bare. The data from the current cycle increasingly suggests the opposite: the largest portion of value creation in high-growth technology companies has historically occurred after the public listing, not before it. Cerebras Systems’ IPO in May 2026, the largest U.S. listing of the year at the time with approximately $5.55 billion raised at $185 per share, and Planet Labs’ tenfold public-market appreciation following its 2021 SPAC listing have reignited a debate about who actually captures the upside in transformative tech companies. Against the backdrop of a potentially record-breaking 2026 IPO pipeline, this question carries direct implications for retail investors deciding how to approach new listings. What follows unpacks the structural forces that have historically shifted value toward public investors, examines the mechanisms that can work against that outcome, and explains why the current cycle may represent a genuine window rather than the usual insider exit.

The conventional wisdom about IPOs is largely wrong

The assumption is familiar: venture capitalists and insiders capture the majority of upside before a company lists, and public buyers inherit whatever growth remains. It is a reasonable-sounding framework, and the available evidence from this cycle contradicts it.

Brad Gerstner, founder and CEO of Altimeter Capital, cited a prior investment made pre-IPO at a $1 billion valuation. Altimeter distributed shares to its limited partners at a $3-4 billion valuation, a solid 3-4x return by any venture standard.

The company subsequently reached approximately $50 billion in value within roughly 24 months of that distribution, a 12-17x return that public investors, not the fund’s limited partners, could have captured.

Gerstner’s example is not an isolated anecdote. Andrew Feldman, founder and CEO of Cerebras Systems, stated that studies consistently show more total return, in both percentage and absolute dollar terms, is available after an IPO than before it. The structural logic is straightforward: the amount of capital that can be deployed in a private-stage company is limited by round size, whereas the post-IPO opportunity accommodates far larger deployment. Even when pre-IPO percentage gains are impressive, the absolute dollar opportunity concentrates in the public phase.

The question is not whether insiders make money. They do. The question is whether public investors arrive at a depleted table. The evidence suggests they do not.

IPO access mechanics explain much of the asymmetry: retail investors typically cannot access shares at the offer price, instead entering the secondary market after institutional allocations are filled, which means they absorb the first-day premium rather than benefiting from it.

When big ASX news breaks, our subscribers know first

Why the “stay private” decade locked retail investors out

The prior decade of venture capital was defined by an explicit philosophy: stay private indefinitely. Major venture firms championed this approach, and the rationale was sound from their perspective. Private companies could avoid public scrutiny, preserve operational flexibility, and allow private valuations to compound across successive funding rounds.

The cost fell on public investors. Each late-stage private round at an escalating valuation set a progressively higher entry price for the next participant, concentrating the largest gains in the earliest investors and pushing the eventual IPO price toward a level that compressed remaining upside.

Feldman quantified the cost with a concrete hypothetical. Had Cerebras gone public 18 months earlier, it likely would have listed at approximately $10 billion rather than the actual $50-56 billion fully diluted valuation at IPO. The difference of approximately $40-46 billion in value creation occurred entirely in the private phase, meaning public investors were excluded from it by definition.

The structural costs of the “stay private” model accumulated in three ways:

- LP pressure build-up: Extended private hold periods created distribution pressure from limited partners seeking returns, ultimately forcing concentrated selling at or shortly after listing.

- Compliance and governance burden: Remaining private longer incurred ongoing costs that delayed liquidity events without proportional benefit to eventual public shareholders.

- Delayed liquidity concentrating final value: By the time companies listed at $50 billion-plus valuations, the most rapid phase of appreciation had already passed in private markets.

Sentiment is now shifting. Panel participants described companies at $1-5 billion valuations actively reconsidering earlier public listings, a reversal of the prior decade’s orthodoxy that could meaningfully change who captures the next phase of growth.

How IPO mechanics determine who captures the upside

Three specific mechanisms at the intersection of venture fund structure and IPO design determine how value distributes between private and public investors. Understanding each one provides a working framework for assessing any given listing’s post-IPO risk profile.

LP distribution pressure

Venture funds face contractual distribution obligations to their limited partners. When a portfolio company lists, fund managers face pressure to distribute shares at or shortly after the IPO, often before full value is realised. The Altimeter case illustrates the dynamic precisely: shares were distributed at a $3-4 billion valuation, and the subsequent appreciation to $50 billion accrued to whoever held the stock in public markets, not to the fund’s LPs who had already received their distribution.

Traditional lockup expiry

The standard 180-day lockup creates a predictable, concentrated selling event at expiry. Insiders and early shareholders are freed to sell simultaneously, generating supply pressure that historically weighs on the share price at the precise moment retail investors may be most exposed. The mechanism is well understood, yet its impact recurs with each IPO cycle.

Modified and staggered lockups

Cerebras implemented a graduated, milestone-tied lockup in coordination with its underwriting banks, spreading insider share releases over a longer period rather than concentrating them at a single expiry date. SpaceX is reportedly expected to adopt a similar structure. For public investors, this model reduces the predictable selling-pressure event at 180 days, potentially providing more price stability in the post-IPO period.

| Mechanism | How it works | Impact on public investors |

|---|---|---|

| LP distribution pressure | Fund managers distribute shares to LPs at or shortly after listing, often before full appreciation is realised | Subsequent gains accrue to public-market holders rather than fund LPs |

| Traditional lockup (180-day) | Fixed expiry triggers simultaneous insider selling at a single date | Concentrated supply pressure can depress share price at expiry |

| Modified/staggered lockup | Graduated release tied to performance milestones, spreading sales over time | Reduces predictable selling-pressure events; may improve post-IPO price stability |

The asymmetry between capital that can be deployed privately (limited by round size) and post-IPO (where far larger sums can be put to work) means these mechanics are not peripheral details. They determine who is positioned to capture the next phase of appreciation.

Planet Labs and Cerebras: two case studies with different lessons

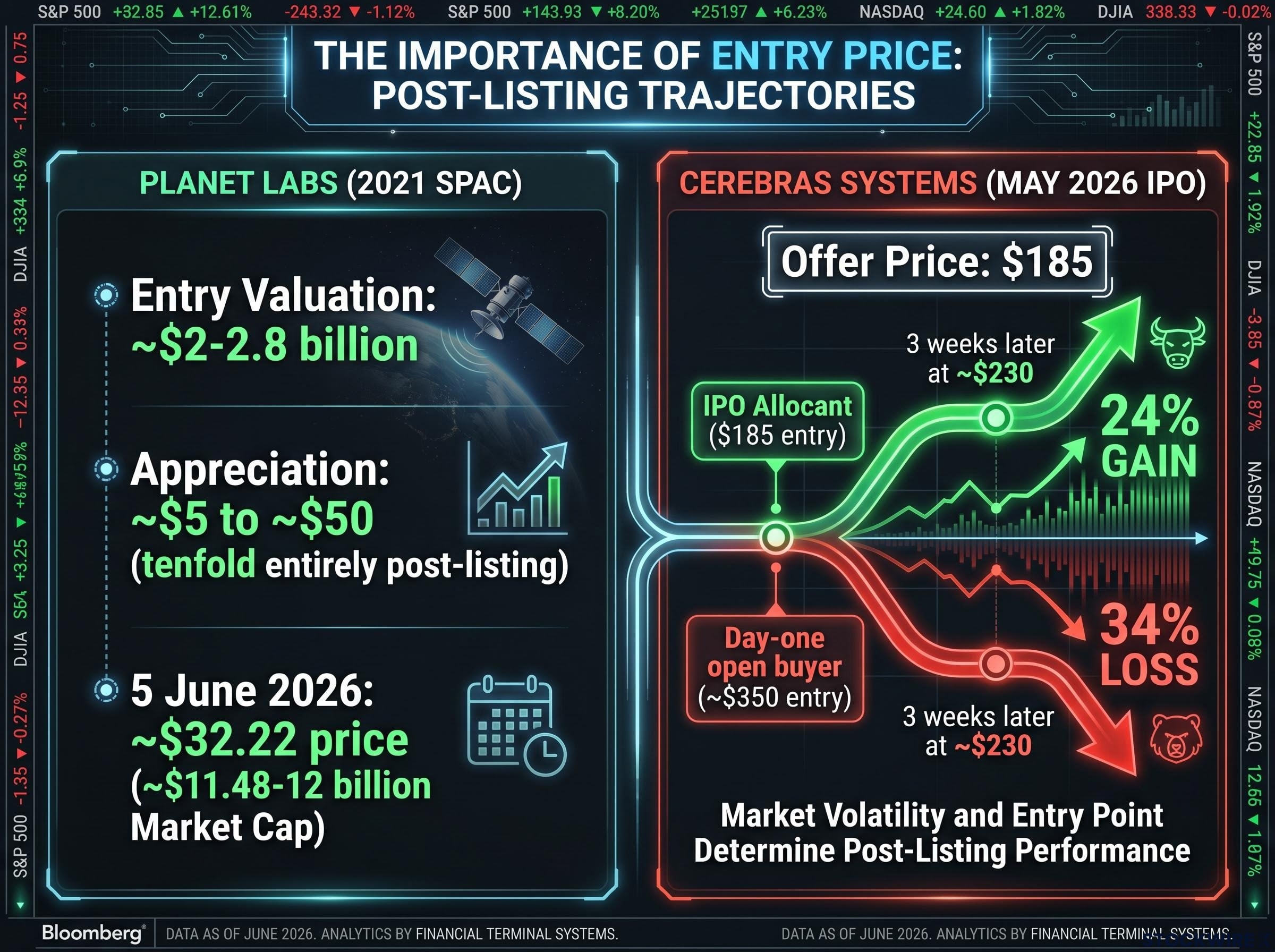

Planet Labs provides the cleanest evidence for the core thesis. The company listed via SPAC in 2021 at an approximate valuation of $2-2.8 billion. Shares subsequently appreciated from approximately $5 to roughly $50, a tenfold increase, with the entire gain occurring in public markets, specifically in years three and four of being publicly traded.

The tenfold appreciation in Planet Labs happened entirely after the public listing, not before it.

As of 5 June 2026, Planet Labs traded at approximately $32.22 with a market capitalisation of approximately $11.48-12 billion, indicating that while the stock has pulled back from its peak, the public-market value creation still dwarfs the original SPAC entry.

Cerebras complicates the picture in a useful way. The offer price of $185 delivered a 68% first-day gain for IPO allocants when shares closed at $311.07. But the opening price of approximately $350, representing an 89% premium to the offer, meant that investors buying in the aftermarket on day one paid a radically different entry price. By early June, shares traded near $230, approximately three weeks post-IPO. An IPO allocant at $185 held a 24% gain. A day-one open buyer at $350 sat on a 34% loss.

| Company | Listing method and year | Entry valuation | Post-listing trajectory |

|---|---|---|---|

| Planet Labs | SPAC, 2021 | ~$2-2.8 billion | ~$5 to ~$50 (tenfold); entire appreciation post-listing |

| Cerebras Systems | IPO, May 2026 | ~$56 billion (fully diluted at offer) | $185 offer → $350 open → $311 close → ~$230 three weeks later |

“Public investor” is not a homogeneous category. The IPO allocant, the day-one open buyer, and the investor who entered at $230 three weeks later all hold different cost bases. The opportunity is real, but the entry point within the public phase matters enormously.

The honest caveats: survivorship bias and valuation risk

The cases above are compelling. They are also exceptional, and treating them as representative would be analytically dishonest.

Three co-equal caveats apply to the thesis that public investors capture more upside than venture investors:

- Survivorship bias: Planet Labs and Cerebras are standout outcomes. The average IPO cohort does not deliver tenfold post-listing gains. Many public-market investors in new listings experience flat or negative returns. Renaissance Capital data shows 202 U.S. IPOs priced in 2025 and 68 priced year-to-date in 2026 (as of early June), running approximately 18.1% behind prior-year pace; a significant portion of those names will underperform their offer prices.

- Valuation compression at aggressive pricing: When an offer price is raised approximately twice during bookbuilding and shares open 89% above the offer price, as with Cerebras, investors entering after the opening pop are paying a structurally different price than IPO allocants. The gap between the $185 offer and the approximately $350 open is the concrete illustration of how intra-“public investor” entry price dispersion can compress or eliminate subsequent upside.

- Limited systematic academic evidence: No broad quantitative studies precisely comparing aggregate post-IPO public returns versus aggregate pre-IPO venture returns were identified in available research. The strongest evidence for the core thesis currently rests on case studies and practitioner testimony rather than systematic cross-cohort data.

No named expert in available sources argued the counter-thesis explicitly. The survivorship-bias and valuation-compression arguments represent the strongest structural counterarguments, and they deserve full weight in any investor’s assessment.

Historical IPO underperformance data complicates any optimistic reading of the current cycle: Jay Ritter’s longitudinal dataset shows newly listed companies have trailed comparable established peers by an average of 3.3% per year over five years since 1980, a drag that compounds the entry-price disadvantage retail investors face when they cannot access the institutional offer price.

A structural shift in who benefits from the 2026 IPO pipeline

The structural conditions that defined the prior decade are changing, and the evidence points to a shift that could favour public investors more than any cycle in recent memory.

Goldman Sachs projects approximately $160 billion in 2026 IPO proceeds across roughly 120 deals, approximately double the prior year’s volume.

AI IPO absorption pressure adds a macro-level variable that individual company analysis cannot capture: Standard Chartered’s global CIO warned in early June 2026 that the near-simultaneous arrival of SpaceX, Anthropic, and OpenAI into public markets within a compressed mid-to-late 2026 window creates market digestion difficulties that could affect pricing conditions for the entire pipeline, not just individual listings.

That forecast reflects more than cyclical recovery. Companies at $1-5 billion valuations are now actively considering earlier public listings rather than pursuing additional private rounds at escalating valuations. If this pattern holds, public investors would gain access to companies at an earlier stage of their growth trajectories than the prior decade permitted.

Modified lockup structures, as implemented by Cerebras and reportedly planned by SpaceX, signal that market participants are aligning incentives more deliberately with public-investor interests. These are not cosmetic changes; they alter the mechanics of post-IPO selling pressure in ways that directly affect the return profile for public shareholders.

For retail investors evaluating the incoming pipeline, three factors warrant assessment for any given listing:

- Entry price relative to valuation trajectory: Where the company is priced at listing relative to its likely growth path over the subsequent 12-24 months.

- Lockup structure type: Whether the lockup is a traditional 180-day fixed expiry or a graduated, milestone-tied structure that distributes selling pressure over time.

- Capital deployment scale post-listing: Whether the public-market phase accommodates the kind of capital deployment that drives the largest absolute dollar returns.

The relevant question is no longer whether to dismiss IPOs categorically. It is how to evaluate which post-listing windows represent genuine opportunity.

Investors exploring how the 2026 issuance wave interacts with broader market structure will find our deep-dive into US equity supply dynamics, which examines how Alphabet’s capital programme has already swung net equity supply by $84 billion and how trillion-dollar AI listings could compress price-to-earnings multiples across incumbent technology holdings even without any deterioration in earnings.

Public markets, not private rounds, are where this cycle’s gains may accumulate

The assumption that venture capitalists capture the majority of upside and public investors arrive late to a depleted opportunity is not supported by the available evidence from this cycle. The Altimeter distribution-to-peak trajectory and Planet Labs’ tenfold public-market appreciation directly contradict it.

This is not a universal law. Aggressive IPO pricing, survivorship bias, and the absence of systematic cross-cohort studies mean the thesis should be applied with discrimination, not as a blanket rule. Entry price within the public phase matters as much as the decision to participate at all, as Cerebras’ divergent outcomes for allocants versus aftermarket buyers demonstrate.

With Goldman Sachs projecting a record-scale IPO year and structural signals, from modified lockups to earlier listings at lower valuations, suggesting the market is realigning incentives, retail investors have reason to engage more seriously with post-listing opportunities rather than ceding the field by assumption. The data from this cycle suggests that public markets may be where the largest share of value creation accumulates, not where it ends.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.