A ceasefire that held for barely two months collapsed over the weekend, and by Monday morning Asian equity markets were already tallying the cost. On 8 June 2026, investors are absorbing a rare simultaneous convergence: renewed Iran-Israel military strikes, rising oil prices feeding through to risk sentiment, and a stronger-than-expected U.S. jobs report that reinforces the Federal Reserve’s rationale for holding rates elevated. Each of these forces would move markets in isolation. Together, they are compressing risk appetite across global equities on a single trading session. What follows breaks down how each shock operates independently, how the three amplify one another, and what signals U.S. investors should monitor as domestic markets open, including whether early equity gains can hold against the combined weight of geopolitical escalation and tighter monetary policy expectations.

The ceasefire that wasn’t: what happened between Iran and Israel over the weekend

The April ceasefire was supposed to be the floor under a diplomatic recovery. It lasted roughly two months. Over the weekend of 7-8 June 2026, Iran and Israel exchanged direct airstrikes, marking the first open military engagement since that ceasefire was established in early April 2026. The exchange did not arrive from a vacuum; U.S. officials had publicly characterised peace negotiations as being in an advanced stage.

The key facts in the escalation sequence:

- A ceasefire between Iran and Israel was established in early April 2026, anchoring a period of declining geopolitical risk premium in energy and equity markets.

- Mutual airstrikes on 7-8 June broke that ceasefire, representing the first direct military engagement between the two nations since April.

- President Donald Trump publicly urged Israel not to retaliate, citing ongoing progress in peace negotiations, a signal that U.S. diplomatic involvement remained active but had failed to prevent the rupture.

President Trump urged Israeli restraint, citing ongoing peace negotiations that U.S. officials had described as being in an advanced stage.

For investors, the significance is not the violence alone but the destruction of an assumption. Markets had priced in a durable peace trajectory. When that expectation evaporates overnight, reassessment tends to be sharp and broad.

The gap between geopolitical risk and stock market behaviour has been a persistent feature of recent crises, with markets processing headline shocks as probability-adjusted inputs to future earnings rather than proportional responses, a framework that holds until sustained disruption, major-power escalation, or recession-level knock-on effects break the adaptive mechanisms.

When big ASX news breaks, our subscribers know first

How oil prices transmit a Middle East military shock to global markets

A military exchange between two countries thousands of miles from New York or Chicago does not, on its face, change the earnings profile of a U.S. consumer goods company. The mechanism that connects one to the other runs through a single commodity: oil.

The transmission follows a specific sequence:

- Military event raises supply risk. Iran is a significant oil producer, and the broader Middle East contains supply routes that underpin global crude flows. Military escalation immediately reprices the probability of supply disruption.

- Oil prices respond within hours. Rising crude prices from the 7-8 June conflict were explicitly cited as an intensifying factor in Asian market anxiety on Monday, compounding the geopolitical sentiment already in play.

- Equity markets absorb the cost. Higher oil prices act as a tax on corporate margins and consumer spending across sectors. Airlines, logistics operators, and consumer discretionary businesses face direct cost pressure. Inflation expectations rise, which in turn shapes central bank posture, feeding back into the discount rate applied to future earnings.

EIA analysis of Iran’s oil production places the country’s output at approximately 4.0 million barrels per day as of 2023, with assessed full-capacity potential near 3.8 million barrels per day, a scale that makes any credible supply disruption risk immediately consequential to global crude pricing.

The oil price impact was not merely additive to the geopolitical anxiety; it was compounding. Energy costs affect inflation expectations, which affect rate expectations, which affect equity valuations. Each link in that chain amplifies the original shock rather than simply adding to it.

A hot jobs report adds the third pressure: what the June 6 payrolls data means for the Fed

Strong employment is ordinarily good news. On Friday, 6 June, it landed badly. U.S. nonfarm payrolls came in above consensus forecasts, and the immediate market read was not relief but concern: the Federal Reserve now has even less reason to cut rates.

The mechanism is straightforward. Above-consensus employment data gives the Fed cover to hold borrowing costs elevated or, in a more hawkish scenario, move them higher. Higher rates raise the cost of capital for equities and reduce the present value of future corporate earnings, a pressure that falls hardest on growth and technology stocks where valuations depend on cash flows years into the future.

By early 2026, rate-cut expectations had already shifted substantially. Bank of America Global Research had pushed its expectation for a first rate cut into mid-to-late 2027 in its general outlook materials, reflecting a broader market repricing of the monetary policy timeline.

Bank of America Global Research pushed its expectation for a first Federal Reserve rate cut into mid-to-late 2027, reflecting the degree to which the higher-for-longer consensus had hardened by early 2026.

The Federal Reserve rate path has been complicated by an internal fracture that predates the June payrolls data: the FOMC’s 8-4 dissenting vote was the largest since 1992, with members pulling in opposite directions on whether to cut or signal hikes, leaving incoming Chair Kevin Warsh to inherit a divided institution at precisely the moment when three simultaneous macro pressures are demanding a coherent policy signal.

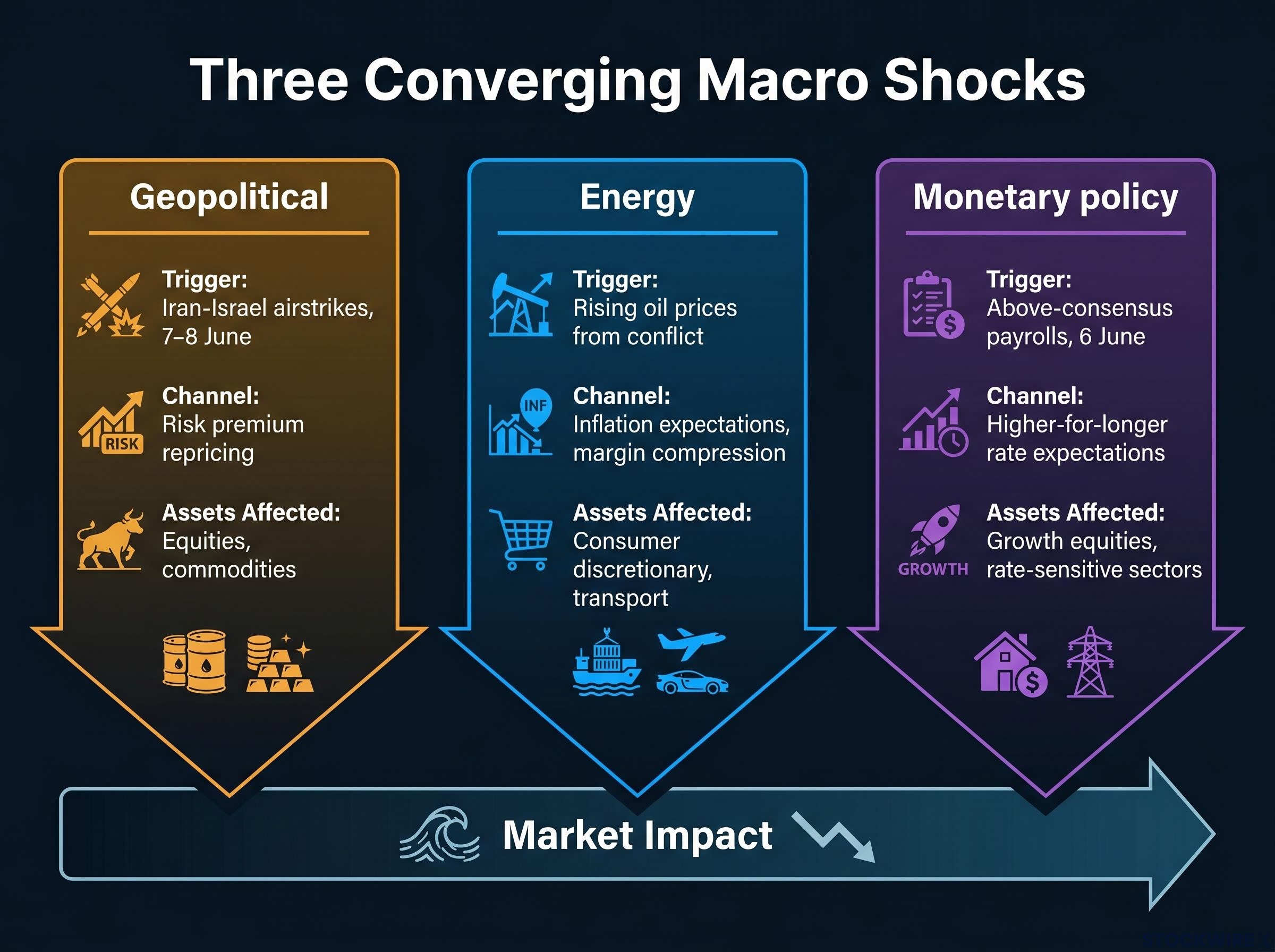

| Shock Type | Triggering Event | Market Channel | Asset Class Most Affected |

|---|---|---|---|

| Geopolitical | Iran-Israel airstrikes, 7-8 June | Risk premium repricing | Equities, commodities |

| Energy | Rising oil prices from conflict | Inflation expectations, margin compression | Consumer discretionary, transport |

| Monetary policy | Above-consensus payrolls, 6 June | Higher-for-longer rate expectations | Growth equities, rate-sensitive sectors |

For equity investors, this combination removes the policy cushion. In a typical geopolitical selloff, rate-cut expectations often rise as markets price in a potential Fed response. This time, the payrolls data closed that door before the geopolitical shock arrived.

How Asian markets absorbed the shock on June 8, and what U.S. investors should watch next

The Asian session provided the first real-time read of how institutional participants priced these three simultaneous pressures. The verdict was largely risk-off.

| Index | Country | Move (%) | Primary Driver |

|---|---|---|---|

| CSI 300 | China | -1.6% | Geopolitical risk, oil prices |

| Shanghai Composite | China | -1.2% | Geopolitical risk, oil prices |

| Hang Seng | Hong Kong | -1.0% (approx.) | Regional risk-off sentiment |

| Straits Times Index | Singapore | -1.2% | Oil price pressure, risk repricing |

| Nifty 50 futures | India | +0.3% | Recovery from prior week losses |

India’s Nifty 50 futures edged higher, a notable divergence likely reflecting a recovery from heavy losses in the prior week rather than an optimistic read on the geopolitical situation. The broader regional pattern was clear: sellers dominated.

What to watch as U.S. markets open

With Asian markets having set the early baseline, U.S. investors face a session where three variables will compete for dominance:

- Oil price direction in the first two hours of U.S. trading, which will serve as the market’s real-time verdict on how seriously participants are treating the escalation risk.

- Further Iran-Israel diplomatic or military developments, particularly any formal statements from U.S. officials on renewed ceasefire progress.

- Federal Reserve official commentary in response to the 6 June payrolls data, which could either reinforce or soften the higher-for-longer signal.

- Nasdaq futures durability. Premarket indications showed early gains, but the historical pattern in multi-shock sessions is that sustained escalation tends to erode opening optimism as the day progresses.

When three macro shocks converge, the danger is what investors stop watching

Each of these three pressures operates on a different timescale. Geopolitical de-escalation can shift with a single statement. Oil prices adjust within hours. Federal Reserve rate expectations move on a slower cycle tied to a data schedule that does not bend to weekend events.

The interaction of geopolitical risk premium, energy cost transmission, and a rate headwind creates a compound pressure, not three separate inputs. When the policy cushion is absent, the other two shocks have nowhere to dissipate.

The Federal Reserve’s April 2025 Financial Stability Report noted that geopolitical shocks, inflation dynamics, and policy uncertainty can interact to tighten financial conditions in compounding ways. That general framework describes the specific configuration facing markets on 8 June: a geopolitical shock feeding energy prices, energy prices feeding inflation expectations, and a hawkish labour market removing the monetary policy offset.

The Federal Reserve Financial Stability Report from April 2025 identified geopolitical shocks, inflation dynamics, and policy uncertainty as forces capable of interacting to tighten financial conditions in compounding ways, a framework that maps directly onto the configuration facing markets on 8 June.

The historical pattern for such convergences is that one factor tends to dominate early and the others resurface as lagged pressures. The question this session leaves unresolved is whether ceasefire diplomacy can recover quickly enough to remove the geopolitical premium before oil prices embed themselves in broader inflation expectations.

The open question markets cannot yet answer

The single most consequential variable on 8 June is not a data release or an earnings report. It is whether U.S.-brokered diplomacy can produce a credible de-escalation signal before the domestic session closes.

President Trump’s public urging of Israeli restraint confirms that U.S. diplomatic engagement remains live. The question is whether it remains effective. The three shocks are not equally reversible: a formal statement on renewed ceasefire talks could shift geopolitical sentiment within minutes, and oil prices would follow within the session. But Federal Reserve rate expectations are anchored to a data schedule. The 6 June payrolls print will shape monetary policy assumptions for weeks regardless of what happens in the Middle East.

For investors monitoring the session, the hierarchy of what matters is specific:

- First priority: U.S. diplomatic statements on Iran-Israel ceasefire progress, the highest-leverage variable in play.

- Second priority: Oil price trajectory in the first two hours of U.S. trading, the market’s real-time escalation barometer.

- Third priority: Fed official commentary in response to the payrolls data, which will shape the rate backdrop for the weeks ahead.

The diplomatic channel is the one item on that list that could change the risk calculus for the entire session. Everything else moves on a slower clock.

For investors who want to stress-test the diplomatic scenario in more depth, our full explainer on US-Iran deal risk and market positioning examines the specific sequencing impasse that characterised negotiations in late May 2026, the major-bank scenario analysis projecting Brent in the $110-150 range under a deal collapse, and why consumer inflation expectations reaching 4.8% in the University of Michigan survey represent a separate amplifier that would engage if diplomacy fails again.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding geopolitical developments and monetary policy are speculative and subject to change based on events and new data.