Passive Income Investing in Australia: What Actually Works

58 mins ago

Most income investors assume they face a binary choice: collect high yields or participate in capital growth. Covered call ETF mechanics make that trade-off structurally real, not just theoretical.

As covered call ETFs have proliferated globally, with yields ranging from 10% to above 20%, the tension has sharpened. Morningstar analysts have consistently described these funds as sacrificing upside participation for current income. For investors whose portfolios already generate enough to cover living expenses, dismantling income positions to chase growth is an unattractive option, and the standard advice to “just rebalance toward growth” ignores the real cost of unwinding income streams that are already meeting financial needs.

This guide lays out a capital-efficient companion framework: how to allocate a targeted slice to modestly or aggressively leveraged ETFs to recapture the upside that covered call holdings systematically surrender, without selling a single income-generating position. What follows is a concrete sizing methodology, a clear view of the trade-offs involved, and an honest assessment of who should and should not attempt this leveraged ETF strategy.

The portfolio is working. Yields are high, distributions are consistent, and the income covers household expenses without touching capital. Then a quarter passes where the underlying index rallies 8% or 10%, and the covered call holdings barely move. The income kept flowing, but the capital sat still.

That experience repeats. It compounds. And over time, the gap between what the portfolio earns and what it could have grown becomes the number that keeps income investors awake.

Morningstar analysts have repeatedly characterised covered call ETFs, including products such as JPMorgan’s JEPI and Global X covered call funds, as sacrificing capital appreciation potential in exchange for higher current income.

The problem is not a matter of picking the wrong fund. It is structural. Covered call mechanics impose an upside cap regardless of which issuer or product an investor chooses. And the instinct to keep chasing higher yields, pushing from 10% toward 20% and beyond, compounds the trade-off in three ways:

Reinvestment capacity sits behind much of this tension: an investor who spends distributions needs different fund characteristics than one who compounds them, and chasing a higher headline yield without first resolving that question is the most common structural error in covered call portfolio construction.

Yields above roughly 25% make the upside trade-off increasingly difficult to justify over extended holding periods. Fund managers have generally positioned approximately 20% as a more achievable threshold for long-term sustainability. But even at that level, the growth ceiling is real, and it is the investor’s own success at building income that makes it progressively harder to ignore.

The mechanics are straightforward once laid out. A covered call ETF writes call options on a portion of its underlying portfolio. Those options generate premium income, which is the source of the elevated yield. In exchange, the fund transfers the benefit of any price appreciation above the option’s strike price to the buyer of the option.

The portion of the portfolio subject to this transfer is the coverage ratio. In many Canadian and international partial-overlay structures, the coverage ratio typically sits between 30% and 50%. That means only the covered fraction of the underlying holdings is subject to the upside cap. The remaining 50-70% of the portfolio retains full exposure to price appreciation.

Fully overwritten strategies push coverage ratios toward 100%, capping upside across the entire portfolio. The distinction matters enormously for anyone attempting to size an offset.

| Coverage Type | Typical Coverage Ratio | Upside Cap Applies To | Income Premium Effect | Example Issuers |

|---|---|---|---|---|

| Partial overlay | 30-50% | Covered portion only | Moderate yield boost | BMO, Horizons, Harvest |

| Full overlay | Up to ~100% | Entire portfolio | Higher yield boost | Global X, JPMorgan, Evolve |

Coverage ratios for individual funds are detailed in issuer fact sheets and product disclosure statements rather than in consolidated secondary sources. Finding the number requires checking the specific fund’s documentation directly.

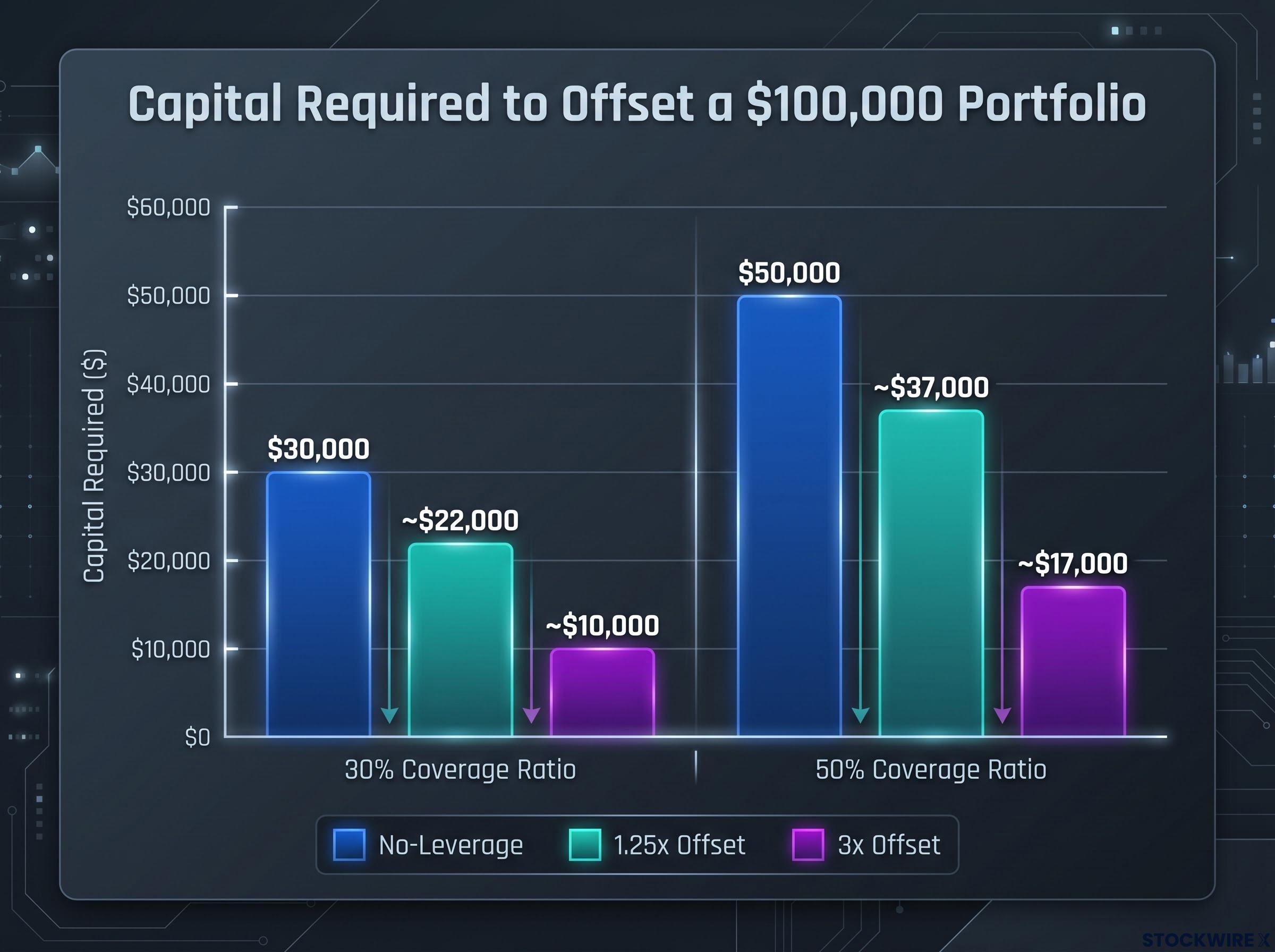

Apply that ratio to a hypothetical $100,000 portfolio. At a 30% coverage ratio, the upside cap applies to $30,000 of notional exposure. At 50%, the capped portion rises to $50,000. The offset target, the amount of growth exposure that needs recapturing, is that covered fraction, not the full $100,000.

This single number is the entry point to the companion sizing methodology that follows. Without it, any offset allocation is guesswork.

The coverage ratio math leads to a direct question: if $30,000 or $50,000 of a portfolio’s growth exposure is being surrendered through the option overlay, what would it take to recapture that exposure without liquidating any income-generating positions?

The core idea is a separate, modestly leveraged ETF allocation, sized to the covered fraction of the income portfolio, that generates the growth exposure the covered call overlay surrenders. The income base stays intact. The leveraged companion is additive.

This companion framework is an original conceptual design. No major 2024-2026 article, white paper, named strategist, or model portfolio has been identified that explicitly endorses or models this specific pairing. Readers should treat it as a portfolio design worth exploring, not a validated strategy with institutional backing.

Some Canadian ETF issuers have developed integrated products that combine modest leverage with covered call overlays in a single fund. Hamilton’s HYLD and HDIV apply approximately 25% leverage alongside covered calls. Harvest’s HBIE (launched April 2024) takes a similar integrated approach. Evolve ETFs has published research discussing what it describes as a symbiotic relationship between leverage and covered calls. These are related but structurally different from the two-vehicle companion framework described here, because integrated products do not allow independent sizing of the offset.

For the separate companion approach, three leveraged ETF tiers are relevant:

The reset period is the dividing line between the two leverage tiers in the companion framework: 1.25x modestly leveraged products carry no daily reset at all, functioning as a permanent structural feature of the fund, while 3x products reset every 24 hours and accumulate compounding drag in proportion to market volatility.

For Canadian financial sector exposure, BNKL at 1.25x is used in place of a triple-leverage equivalent, as no equal-weight triple-leverage Canadian banking ETF is currently available.

The efficiency argument for leverage in this context is arithmetic, not abstract. Consider a $100,000 portfolio with a 30% coverage ratio. Without leverage, offsetting the capped growth exposure requires approximately $30,000 in a companion growth position. With a 1.25x leveraged companion, the required capital drops to approximately $22,000, because each dollar of capital delivers $1.25 of market exposure.

Higher leverage multiples reduce the required capital further. The trade-off is that higher leverage introduces proportionally greater volatility risk, a point addressed in the following section.

| Coverage Ratio | Portfolio Value | No-Leverage Offset | 1.25x Offset | 3x Offset (Approx.) |

|---|---|---|---|---|

| 30% | $100,000 | $30,000 | ~$22,000 | ~$10,000 |

| 50% | $100,000 | $50,000 | ~$37,000 | ~$17,000 |

These figures are illustrative conceptual estimates based on the framework’s own reasoning, not empirically validated targets. They should be treated as a starting calculation methodology that readers can adapt to their own coverage ratios and leverage preferences.

To illustrate directionally how the three leverage tiers might behave relative to one another, consider a hypothetical CAD $100,000 companion portfolio allocated across Nasdaq-tracking funds (30%), S&P 500-tracking funds (30%), TSX-tracking funds (20%), and Canadian financial sector funds (20%). In a rising market, a 1.25x-only construction would be expected to modestly outperform an unleveraged equivalent. A triple-leverage-only construction would amplify those gains substantially, but with commensurately greater exposure to drawdowns. A mixed construction (80% at 1.25x, 20% at triple-leverage) would sit between these two extremes, delivering meaningfully higher expected returns than the 1.25x-only version while limiting the volatility drag that a fully triple-leveraged portfolio would introduce in choppy conditions.

These are conceptual illustrations only and do not represent actual or backtested performance results. The relationship between leverage tiers will vary considerably depending on market conditions, the path of returns, and the specific instruments used. The simulated companion portfolios remain in early observation as of mid-2026.

The companion framework introduces a specific set of risks that income investors, who typically prioritise stability and predictable cash flow, may be unfamiliar with.

The most consequential is volatility decay, sometimes called beta slippage. Leveraged ETFs target a multiple of the daily return of an index, not the long-term cumulative return. This daily reset structure means that compounding in volatile, choppy markets causes the portfolio’s actual return to diverge from the expected multiple over time, typically to the downside. In a market that drops 10% and then recovers 10%, a triple-leveraged fund does not return to its starting value. It ends lower. The more volatile the path, the greater the decay.

Daily reset mechanics create the asymmetry: a triple-leveraged fund tracking an index that drops 10% and then recovers 10% does not return to its starting value, because percentage losses and gains compound on a base that shrinks and grows unequally with each session.

The SEC and FINRA guidance on leveraged ETFs explicitly identifies the daily reset structure as the mechanism by which these instruments diverge from their stated multiples over longer holding periods, a divergence that compounds materially in volatile or choppy markets.

Bankrate’s 2026 ETF guidance states explicitly that leveraged ETFs are best-suited for traders seeking short-term returns rather than long-term investors. The SEC, FINRA, and CIRO/IIROC have all issued longstanding guidance characterising leveraged ETFs as complex, high-risk instruments unsuitable as core long-term buy-and-hold positions for retail investors.

The entire companion framework remains in early experimental stages as of mid-2026 and has not been empirically validated over a complete market cycle.

The following suitability disqualifiers are listed in descending order of risk severity:

Three questions require honest answers before committing capital. Do you understand how daily leverage reset causes returns to diverge from the expected multiple over weeks and months? Can you tolerate the companion position losing 30-50% of its value without liquidating? Does the companion position represent a true minority of your total portfolio, small enough that its worst-case scenario does not affect your income base?

If any answer is no, this framework is not appropriate at this stage.

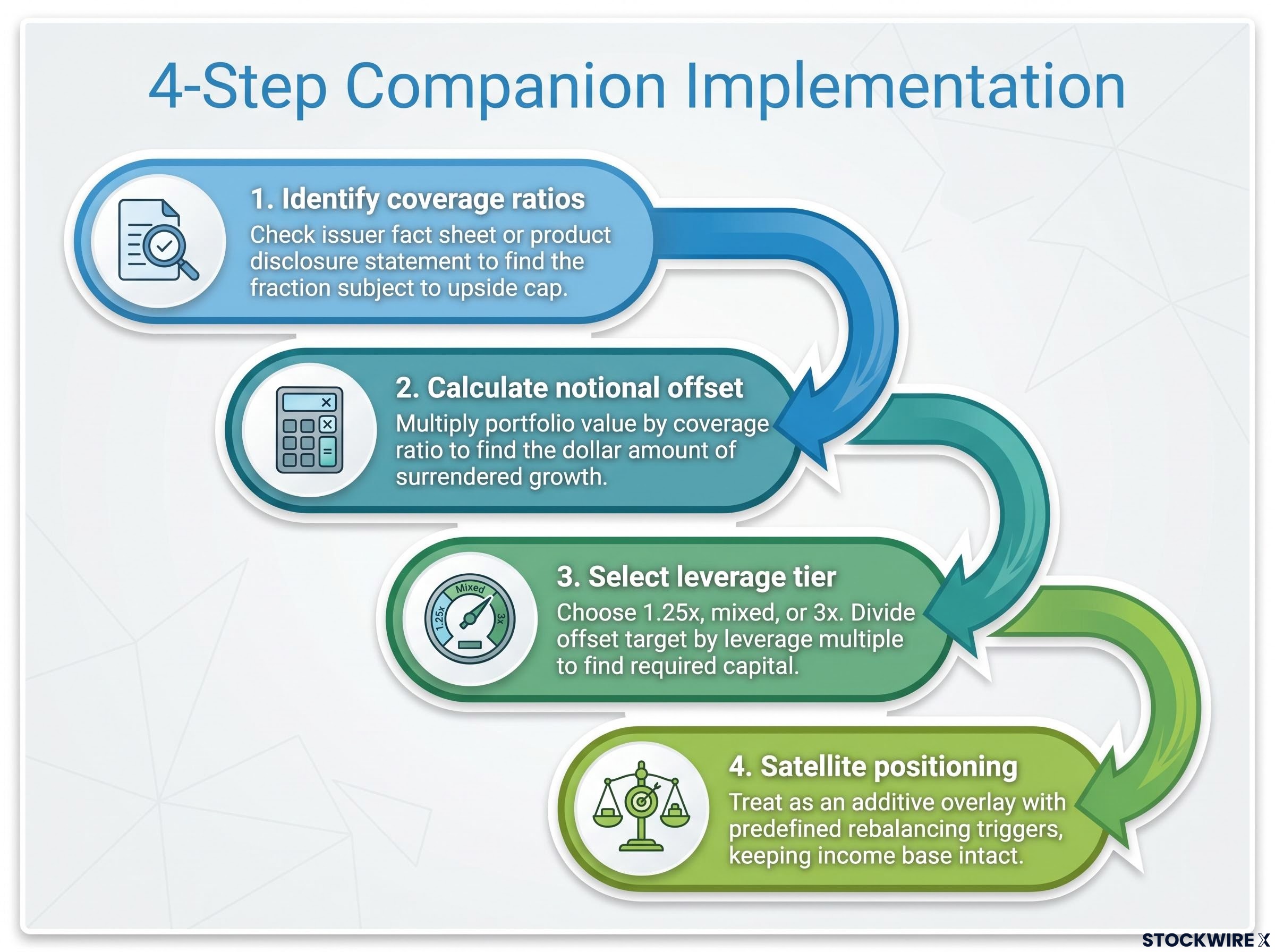

For investors who have worked through the mechanics and the suitability assessment, the implementation follows a four-step sequence:

The mixed approach, primarily 80% at 1.25x with 20% at triple-leverage, distributed across Nasdaq (30%), S&P 500 (30%), TSX (20%), and Canadian financials (20%) exposure targets, represents the most practical starting point for income investors new to this framework.

For investors who prefer not to manage two separate positions, integrated products offer an alternative path:

The income-growth tension in covered call portfolios is structural, and solving it requires a structural response: a deliberately sized companion position rather than a product replacement. The framework described here is conceptual, early-stage, and has not been validated over a complete market cycle. It deserves exploration, not uncritical adoption.

The first concrete action is small. Pull one covered call ETF fact sheet and find the coverage ratio. That single number is the entry point to the entire sizing methodology, and it costs nothing to look.

For investors ready to move beyond the conceptual framework and into execution-level detail, our dedicated guide to leveraged ETF position sizing covers concrete sizing formulas for TQQQ, UPRO, and SOXL, hedge construction using inverse leveraged funds, and the practitioner consensus that caps total leveraged ETF exposure at 5-10% of portfolio across all tickers.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The companion framework described is speculative and based on conceptual reasoning rather than empirical validation. Past performance does not guarantee future results, and leveraged ETF positions carry significant risk of capital loss.

—

A covered call ETF writes call options on a portion of its underlying portfolio to generate premium income, but in exchange transfers the benefit of any price appreciation above the option's strike price to the option buyer, structurally limiting capital growth for the fund's investors.

By allocating a separately sized, modestly or aggressively leveraged ETF position equal to the covered fraction of the income portfolio, investors can recapture the growth exposure surrendered by the option overlay without liquidating any existing income-generating holdings.

Multiply your total portfolio value by your covered call ETF's coverage ratio to find the notional growth exposure being surrendered, then divide that figure by your chosen leverage multiple (1.25x or 3x) to determine the required companion capital.

Volatility decay, also called beta slippage, occurs because leveraged ETFs reset their exposure daily, meaning that in choppy or declining markets the fund's actual return diverges from the stated leverage multiple over time, typically producing lower cumulative returns than the multiple suggests.

Investors who are unfamiliar with daily reset mechanics, have low tolerance for drawdowns of 30-50% or more, intend to use triple-leverage as a core long-term position, or lack a sufficient capital buffer that keeps the companion position from affecting household income should not attempt this framework.