UBS Backs Five Non-Dollar Currencies as Bearish Dollar Bet Builds

5 hrs ago

The SOX semiconductor index has climbed 80% from its March 2026 lows. Multiple memory chipmakers have crossed trillion-dollar market capitalisations. And yet the loudest call from Barclays’ macro strategy desk this week is not to buy more of what is already working. It is to look at Japan instead. Barclays strategist Ajay Rajadhyaksha published a client note on 3 June 2026 positioning the Nikkei 225 as the most favourable risk-adjusted entry point into the global AI investment cycle among major equity markets. The argument is not that Japan is cheap in absolute terms. It is that Japan’s structure, its mix of AI supply-chain exposure, its valuations relative to the United States, and its underlying economic reforms, makes it a more durable vehicle than the concentrated bets Korea and Taiwan represent. What follows unpacks the Barclays thesis, explains the concentration risk embedded in the KOSPI and TAIEX that Japan avoids, and provides a framework for evaluating international equity markets as AI trade vehicles in a cycle that has already priced in considerable optimism.

The rotation happened beneath the headline rally. While U.S. large-cap technology stocks underperformed through early 2026, semiconductor equities posted the kind of gains that typically mark the late-middle innings of a cycle. Capital moved from the platforms consuming AI to the companies building its physical infrastructure.

The SOX semiconductor index rose 80% from its March 2026 lows, according to Barclays’ 3 June 2026 client note, with multiple memory chipmakers reaching trillion-dollar market capitalisations during the rally.

That backdrop is precisely what makes Rajadhyaksha’s Japan call counterintuitive. Barclays is not rejecting AI as a theme. The note explicitly frames Japanese equities as AI beneficiaries. The question it raises is different: whether the most crowded expressions of the AI trade still offer the best risk-reward profile at a point where U.S. markets are trading at what Barclays describes as near-peak valuations.

The distinction matters for positioning. Investors who entered the AI theme early may now hold concentrated exposure to the very segment of the market where optimism has been most aggressively priced. The Barclays thesis suggests that diversification within the AI trade, rather than away from it, is the adjustment the cycle now demands.

The rotation Barclays describes maps directly onto how institutional strategists at J.P. Morgan, Goldman Sachs, and Morgan Stanley have independently structured their AI investment framework: hardware as the highest-beta expression of direct capex, cloud platforms as diversified core holdings, and pure-play software as tactical or thematic positions, with each tier carrying distinct concentration and cycle sensitivities.

Strip the AI narrative from Japan entirely, and the investment case still stands on its own structural legs. That independence is what separates Japan from every other AI-exposed equity market in Asia.

The Tokyo Stock Exchange has been pressuring companies trading below book value or carrying chronically low return on equity (the profit a company generates relative to shareholder funds) to publish capital-efficiency improvement plans. The campaign began in 2023-2024 and has been reinforced through 2025-2026, with increasing numbers of companies responding in 2026 with explicit ROE targets, cross-shareholding reductions, and higher payout-ratio commitments. Three structural tailwinds now operate in parallel:

The TSE capital efficiency requirements, published and updated by the Japan Exchange Group through April 2026, formally mandate that Prime and Standard Market companies trading below book value disclose concrete improvement plans covering return on equity targets, cross-shareholding reductions, and payout commitments, giving the governance reform campaign a regulatory backbone that investor pressure campaigns in other markets lack.

J.P. Morgan Private Bank Asia’s 2026 Outlook describes Japan as sitting “at the intersection of global fragmentation, AI revolution and inflation’s structural shift.”

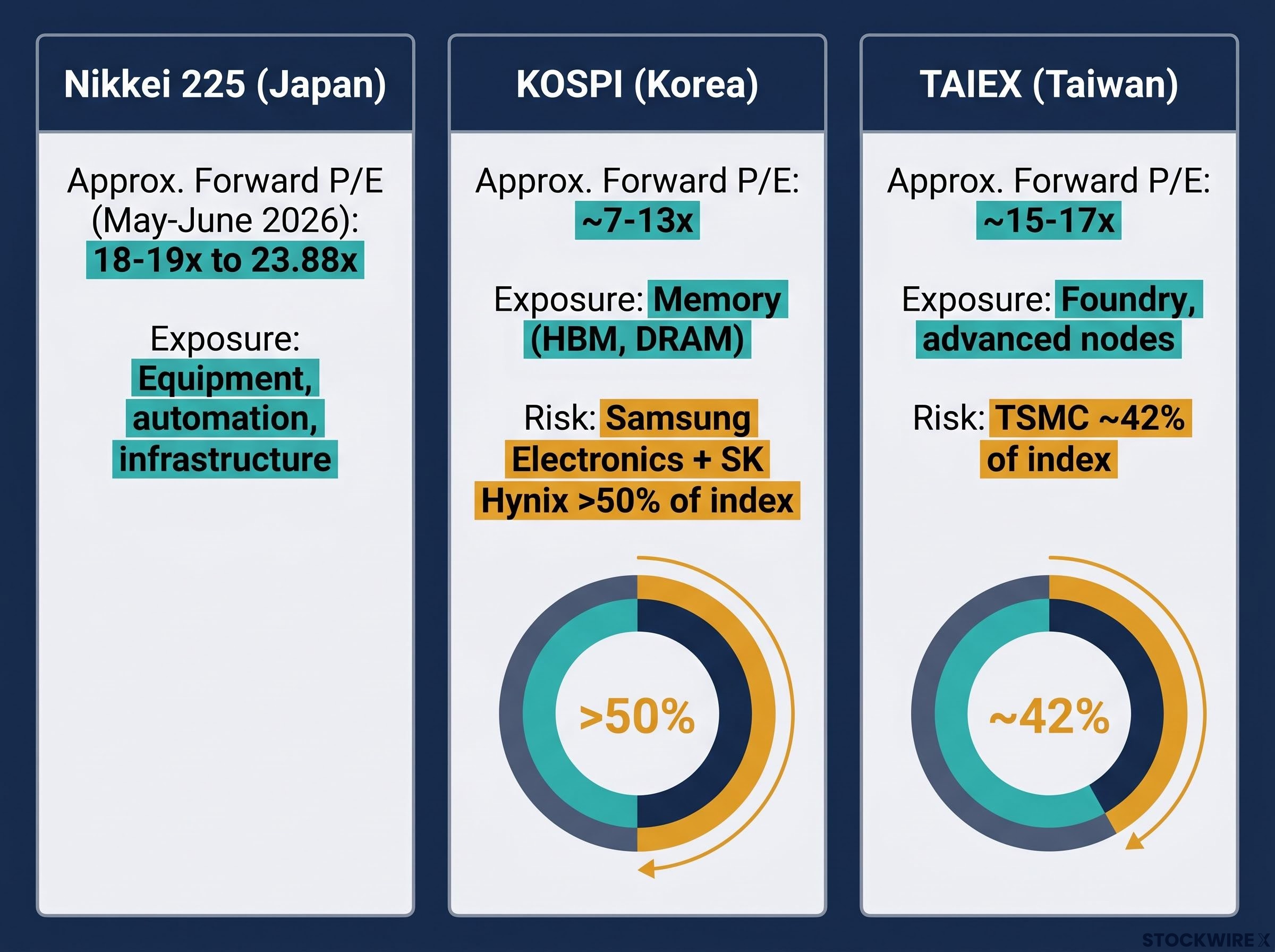

Barclays places the Nikkei 225 at 18-19 times projected earnings as of its 3 June 2026 note. Broader data aggregates from MacroMicro and Simply Wall St place the index in a range of approximately 18.8x-23.88x over May-June 2026. Against U.S. near-peak multiples, Barclays characterises these valuations as relatively undemanding.

A market with genuine structural reform tailwinds offers downside protection that a pure-play AI market cannot. For investors assessing position sizing, Japan’s dual-driver case changes the risk profile in a way that Korea and Taiwan’s single-segment exposures do not.

Japan’s structural re-rating has produced measurable results that predate the AI narrative: TOPIX average price-to-book has risen from 1.1x to 1.5x since 2023, average return on equity has climbed toward 9-10%, and Berkshire Hathaway’s accumulated stakes across Japan’s five major trading houses now exceed 10% each, providing a carry-positive, financially substantiated institutional validation of the governance thesis.

The KOSPI looks like a diversified equity index. It contains hundreds of listed companies spanning electronics, industrials, financials, and consumer sectors. The TAIEX carries a similar breadth on paper. The index mechanics tell a different story.

KOSPI and TAIEX performance in 2026 makes the concentration argument concrete: the KOSPI has posted approximate year-to-date gains of 87.2% and the TAIEX roughly 52.4%, both dwarfing the S&P 500’s roughly 9.3% return, yet both indices behave more like semiconductor sector funds than diversified country exposures, meaning every basis point of that outperformance is tied directly to AI capital expenditure cycles rather than broad economic momentum.

TSMC and KOSPI benchmark concentration data published in May 2026 places TSMC’s index weighting in the TAIEX at 42-44% and Samsung plus SK Hynix at over 52% of the KOSPI, figures that convert what appear to be diversified national benchmarks into effectively single-sector vehicles for AI hardware exposure.

When two names dominate more than half of a benchmark, investors are not buying a market. They are buying a sector thesis wrapped in an index structure. The KOSPI is, in structural terms, a memory-cycle trade. Its returns rise and fall with HBM and DRAM pricing dynamics, regardless of what the remaining index constituents do. The TAIEX is a high-quality but highly concentrated foundry play; when TSMC re-rates, the index moves with it.

The valuation picture reinforces the structural story. Korea Economic Daily, Bloomberg data, and Goldman Sachs Research place the KOSPI forward price-to-earnings ratio (the price investors pay per dollar of expected earnings) at approximately 7-8x as of May 2026, below long-run averages. J.P. Morgan Private Bank Asia’s May 2026 update cites a higher range of approximately 11-13x. The TAIEX sits in the mid-teens, approximately 15-17x, per J.P. Morgan Private Bank Asia and regional strategy commentary.

| Index | Approx. Forward P/E (May-June 2026) | Primary AI Exposure | Key Concentration Risk |

|---|---|---|---|

| Nikkei 225 (Japan) | 18-19x (Barclays); 18.8x-23.88x (aggregators) | Equipment, automation, infrastructure | Broader but peripheral to core compute |

| KOSPI (Korea) | ~7-8x (Goldman/Bloomberg); ~11-13x (J.P. Morgan) | Memory (HBM, DRAM) | Samsung + SK Hynix >50% of index |

| TAIEX (Taiwan) | ~15-17x (J.P. Morgan/regional commentary) | Foundry (TSMC), advanced nodes | TSMC ~42% of index |

Index-level valuations can appear compelling on a screen. Knowing what those valuations actually represent, whether a diversified economy or a two-name sector bet, matters for sizing, hedging, and scenario planning.

Japan does not design the GPUs. It does not fabricate the leading-edge chips. It does not produce the high-bandwidth memory. What it does is build, test, and maintain the machinery that makes all of those things possible, and that structural position carries a specific kind of resilience.

Three companies anchor the thesis:

Advantest’s role illustrates the logic. Every HBM chip and every GPU must be tested before it ships. Advantest builds the systems that perform those tests. Its revenue is tied to AI capital expenditure volumes, not to memory pricing or the success of any single chip architecture. If the industry shifts from one memory standard to another, or from one accelerator design to the next, the testing still happens. Both Barclays (Rajadhyaksha, June 2026) and J.P. Morgan Private Bank Asia’s 2026 Outlook cite Advantest as a primary AI-linked beneficiary in Japan.

Tokyo Electron occupies a parallel position in the manufacturing process itself, supplying the deposition and etch equipment that advanced semiconductor fabrication requires. Its exposure is to the build-out of fabrication capacity, not to the end-market pricing of the chips those fabs produce.

The “picks and shovels” framing describes a structurally different sensitivity to the AI cycle. Equipment makers benefit from capex spending regardless of which chip architecture or memory standard wins, insulating investors from winner-takes-most dynamics at the application layer.

SoftBank offers a distinct risk-return profile within the same market. Its large stake in Arm, the architecture licensor whose CPU and accelerator designs underpin a growing share of AI-capable processors, provides exposure to the design layer rather than the equipment layer. Vision Fund investments add further AI venture optionality.

Strategists consistently position SoftBank as more volatile than the equipment names. It carries higher beta, meaning larger moves in both directions. For investors seeking leveraged exposure to Japan’s AI story rather than the steadier equipment-capex sensitivity, SoftBank fills that role within the Nikkei 225.

The Barclays note is optimistic on a relative basis. It is not unconditional. Three distinct risks sit alongside the thesis, and each operates independently.

The capex-to-revenue lag is the mechanism that most directly threatens the Japan thesis alongside the others: Morningstar analyst Dennis Li has identified an 18-24 month gap between hyperscaler infrastructure spending and the revenue it ultimately generates, meaning the SOX’s 80% rally from March 2026 lows reflects capital markets pricing outcomes that won’t be confirmed or denied for another one to two years.

No investment thesis is stronger than its weakest assumption. Investors who understand the specific conditions under which the Japan AI trade breaks down are positioned to monitor those risks before consensus reassesses.

The Barclays thesis is a risk-adjusted argument for a specific stage of a cycle, not a claim that Japan will outperform Korea or Taiwan if the AI hardware cycle re-accelerates from here. That distinction shapes how to use it.

The commercial question for investors is not whether Japan is a good AI market in the abstract. It is what structure offers the best AI equity exposure at the current stage of the cycle, given where valuations, concentration, and pricing already sit. Diversification across the AI supply chain, structural reform tailwinds, and relative valuation all point in the same direction for Japanese equities as of June 2026.

The thesis is conditional. It depends on the current cycle positioning and will require monitoring as the SOX rally evolves, as Bank of Japan policy develops, and as the global AI capex trajectory reveals whether the build-out is accelerating or plateauing. Japan offers a framework, not a conclusion. The framework says: at this point in the cycle, durability may matter more than concentration.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Barclays strategist Ajay Rajadhyaksha published a note on 3 June 2026 arguing that the Nikkei 225 represents the most favourable risk-adjusted entry into the global AI investment cycle among major equity markets, citing Japan's supply-chain diversification, governance reforms, and valuations that are relatively undemanding compared to U.S. near-peak multiples.

Samsung Electronics and SK Hynix together account for over 50% of the KOSPI's weighting, while TSMC alone represents approximately 42% of the TAIEX, meaning both benchmarks behave more like single-sector semiconductor funds than diversified national equity markets.

Barclays and J.P. Morgan both cite Advantest (semiconductor test equipment for HBM and GPU chips) and Tokyo Electron (deposition and etch equipment for advanced nodes) as primary AI-linked beneficiaries, with SoftBank offering higher-beta AI exposure through its Arm stake and Vision Fund investments.

The three key risks are yen volatility and Bank of Japan policy uncertainty, absolute valuation risk if global AI equities broadly de-rate, and Japan's structural peripherality given that core AI compute production remains concentrated in non-Japanese firms like TSMC, Nvidia, Samsung, and SK Hynix.

The Tokyo Stock Exchange has been requiring companies trading below book value or with low return on equity to publish capital-efficiency improvement plans since 2023-2024, driving higher dividends, share buybacks, and cross-shareholding reductions that provide structural reform tailwinds independent of the AI cycle.