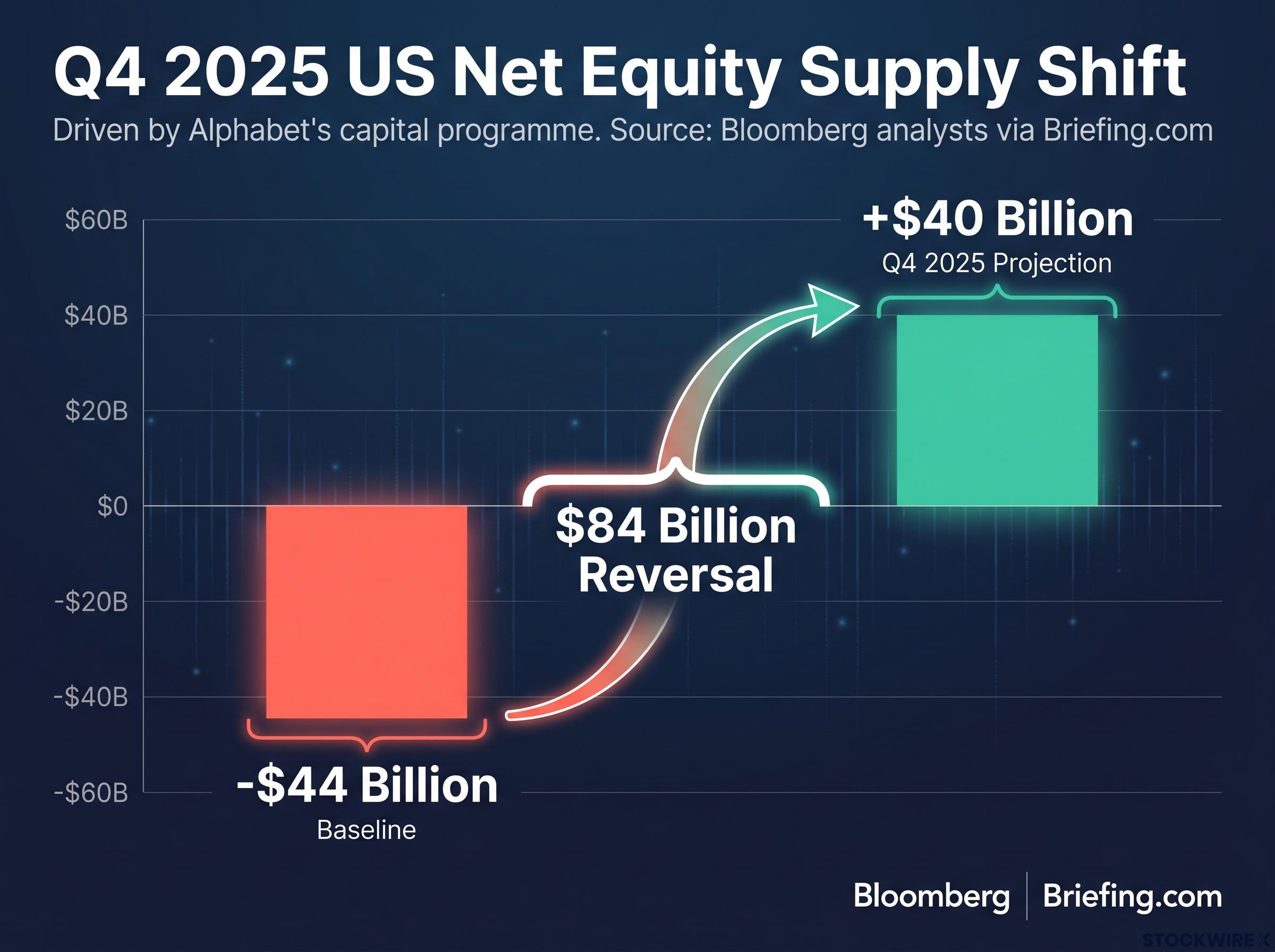

A single company’s stock offering is projected to flip US net equity supply from negative $44 billion to positive $40 billion. That company is Alphabet. And it is not acting alone.

In late May and early June 2026, a cluster of the largest AI and technology companies simultaneously moved to raise equity capital at a scale not seen since the dot-com era. Anthropic has reportedly filed for an IPO targeting a valuation above $1 trillion. SpaceX is said to be planning a listing of approximately $75 billion. And Alphabet’s confirmed $80 billion capital programme is already reshaping the structural conditions of the US equity market. The buyback-dominated era that supported stock prices for more than a decade is being tested by a wave of AI-linked issuance that could permanently alter how much equity supply investors must absorb. This analysis maps the documented and reported capital-raising activity, explains the specific market mechanism at work, and draws out what the pattern means for US investors now.

Alphabet’s $80 billion raise just flipped the US equity market’s supply equation

The arithmetic arrived before the narrative. Bloomberg analysts, as cited by Briefing.com in late May 2026, projected that Alphabet’s capital programme, combined with reduced buybacks, would move net US equity supply in Q4 2025 from approximately negative $44 billion to approximately positive $40 billion.

That is an $84 billion swing driven by a single company’s financing decision.

Bloomberg analysts project Alphabet’s programme will shift Q4 2025 net US equity supply from approximately -$44 billion to approximately +$40 billion, an $84 billion reversal of the buyback-era baseline. Source: Bloomberg analysts via Briefing.com, late May 2026

The components of the programme are now documented:

- An at-the-market (ATM) equity offering of approximately $40 billion, the largest equity component

- A $10 billion commitment from Berkshire Hathaway, reported by CNBC, as part of the broader capital plan

- A stated purpose of funding AI infrastructure expansion and capital expenditure at a scale Alphabet’s existing cash flows and debt capacity could not support alone

The total programme sits at approximately $80 billion. This is not a secondary offering designed to let insiders exit. It is a capital raise designed to finance physical infrastructure: data centres, chips, and the computing capacity required to compete in AI at scale. The structural consequence, a reversal from net negative to net positive equity supply, is not a side effect. It is the price the market pays for absorbing a programme of this magnitude.

When big ASX news breaks, our subscribers know first

What “net equity supply” actually means, and why it has held prices up

Net equity supply is the difference between shares entering the market and shares leaving it. When companies issue new stock through IPOs, secondary offerings, or ATM programmes, supply increases. When companies buy back their own stock or delist, supply decreases.

For much of the period since 2010, US equity markets have operated in a net negative supply environment. Buybacks consistently exceeded new issuance, meaning the total pool of available shares was shrinking year after year. Fewer shares competing for the same pool of investor capital tends to support prices, even before earnings growth enters the equation.

The Alphabet programme, by itself, reverses this condition for an entire quarter. The $84 billion net swing projected by Bloomberg analysts illustrates the scale: a single AI-linked capital raise is sufficient to undo years of accumulated buyback support in a single reporting period.

NBER research on equity issuance and asset prices documents a reliable empirical relationship between elevated new share issuance and subsequent stock market underperformance, a finding that gives the current AI supply wave a quantitative basis for concern beyond narrative comparison alone.

When buybacks dominate versus when issuance dominates

The two regimes produce distinct conditions for equity valuations:

- Negative net supply (buyback dominance): Shrinking share count supports earnings-per-share growth even when total earnings are flat. Price-to-earnings multiples can expand as scarcity drives demand for a smaller pool of available equity. Investor sentiment tends to benefit from the perception of corporate confidence embedded in buyback programmes.

- Positive net supply (issuance dominance): More shares compete for the same capital. Earnings-per-share growth slows unless total earnings rise proportionally. Price-to-earnings multiples face compression pressure as investors demand higher returns to absorb greater supply. Sentiment can shift if large issuance is perceived as a signal that companies need external capital rather than generating sufficient cash internally.

The shift from one regime to the other does not guarantee a market decline. It does, however, remove a structural support that many investors have benefited from without necessarily recognising it.

Anthropic and SpaceX: trillion-dollar ambitions entering public markets

Alphabet’s programme is confirmed. The next two potential contributors to the AI equity supply wave are not.

Anthropic has reportedly filed for an IPO targeting a valuation above $1 trillion, according to Axios as cited in the original reporting. As of early June 2026, this filing has not been independently corroborated in accessible reporting from Bloomberg, Reuters, the Wall Street Journal, the Financial Times, or CNBC. No lead underwriters or binding timetable have been publicly named.

Anthropic’s confidential S-1 filing with the SEC on 1 June 2026 confirmed the company’s path to public markets at a valuation that had already more than doubled from $380 billion to $965 billion in approximately four months, a compression of the price discovery timeline that leaves less room for public investors to form independent valuation views before allocation decisions must be made.

SpaceX is reported to be planning an IPO of approximately $75 billion at a valuation approaching $1 trillion, according to Bloomberg as cited in the original reporting. The company is also said to be targeting underwriting fees below 0.75%, well beneath the industry standard range of 1-3%. At $75 billion, even that fractional difference represents hundreds of millions of dollars in fees, a signal of the negotiating leverage a company of this scale commands. These terms have not been independently confirmed in accessible 2025-2026 public reporting beyond the original source citation.

| Company | Reported/Confirmed Raise | Valuation Target | Verification Status |

|---|---|---|---|

| Alphabet | ~$80B total (~$40B ATM equity) | Existing public company | Confirmed (Bloomberg analysts via Briefing.com) |

| Anthropic | IPO (size undisclosed) | Above $1 trillion | Reported (Axios); not independently corroborated |

| SpaceX | ~$75B IPO | Approaching $1 trillion | Reported (Bloomberg); not independently corroborated |

If even one of these reported deals proceeds alongside the Alphabet programme, the cumulative equity supply effect compounds well beyond the already-documented $84 billion swing. Multiple trillion-dollar AI valuations entering public markets simultaneously would be without modern precedent.

Convertible bonds and the parallel funding wave running alongside the IPO pipeline

The equity deals are the headlines. The convertible bond market is the second channel.

US convertible bond issuance is described as running at record pace in 2025-2026, according to Bloomberg as cited in the original reporting. A precise aggregate dollar total has not been independently confirmed in accessible public sources, but the general characterisation of elevated activity is consistent across multiple outlets.

The structural logic of convertibles for AI companies is straightforward. Three features make them particularly attractive for firms with high capital expenditure needs but uncertain near-term cash flows:

- Lower coupon cost: Convertible bonds carry lower initial interest payments than straight debt because investors accept a reduced yield in exchange for the option to convert into equity later

- Deferred dilution: Unlike a direct stock offering, convertibles do not immediately increase the share count, delaying the dilutive impact until conversion occurs

- Investor appeal via embedded equity upside: The conversion feature gives bondholders exposure to potential share price appreciation, making the instruments attractive in a market where AI valuations are expected to rise

The combination of large equity issuance programmes and elevated convertible activity means capital absorption is occurring across multiple instruments simultaneously. Investors tracking only IPO headlines may underestimate the total volume of new paper entering markets. The convertible channel is a second, less visible source of supply pressure on the same pool of investor capital.

The convertible channel is operating against a broader institutional backdrop: leveraged finance demand for AI debt has been amplified by a $15 trillion corporate refinancing wall expected between 2026 and 2028, pushing institutional capital away from traditional broadly syndicated loans and toward hybrid AI instruments that carry higher yield potential alongside meaningfully higher complexity and default risk.

History’s warning: what thematic IPO waves have done to investors before

Trillion-dollar valuations and record-pace issuance generate momentum. History suggests they also warrant scrutiny.

Financial Times and Wall Street Journal columns in 2025-2026 have noted the recurring pattern that thematic IPO waves tend to cluster near late-cycle points in sector enthusiasm. The dot-com era, the SPAC surge, and the clean energy listing boom each shared structural features that are visible again today.

Barclays issued a parallel warning on record IPO supply pressure in late May 2026, identifying 63 deals already priced raising $28.8 billion through that date as mechanical capital absorption pressure on existing holdings, a figure that does not yet include the Alphabet ATM programme or the reported pipeline from Anthropic and SpaceX.

Three warning signals have appeared consistently across prior thematic IPO waves:

- Elevated valuations relative to earnings visibility. Companies enter public markets at price points that imply years of flawless execution, leaving little margin for operational disappointment.

- Retail over-participation driven by narrative rather than fundamentals. Thematic excitement draws capital from investors who may not fully assess the risk embedded in early-stage or high-growth companies at peak valuations.

- Post-IPO underperformance as supply exceeds sustainable demand. When multiple large deals compete for the same capital pools in a concentrated period, the market’s capacity to absorb new supply at initial valuations is tested, and prices often adjust downward in subsequent quarters.

How the current AI wave compares to prior thematic surges

The structural parallels are visible without asserting equivalence. The valuation-to-earnings-visibility gap in a company like Anthropic, which lacks a public earnings history, echoes the dynamics of late-1990s technology IPOs. The simultaneous supply surge from multiple mega-scale deals mirrors the SPAC wave of 2020-2021, where the volume of listings outran the market’s absorptive capacity. Narrative-led retail participation is present in AI markets, where investor enthusiasm for the technology’s potential can outpace evidence of commercial returns.

None of this means AI companies are overvalued. It means the structural conditions share features with prior waves that ended poorly for late entrants. As of early June 2026, no SEC rulemaking specifically addressing mega-AI IPO clustering has been identified; regulators have addressed AI in trading and disclosure contexts, but the listing wave itself has not yet drawn a targeted regulatory response.

What the AI capital wave means for US investors positioning today

Three considerations flow directly from the analysis above.

- The net equity supply shift is already underway. The Alphabet programme alone flips Q4 supply from negative to positive. Broad market multiples face compression pressure from the increased supply of available equity, independent of earnings trajectory.

- Valuation opacity is high for the incoming IPOs. Anthropic and SpaceX, if they list as reported, will enter public markets at trillion-dollar valuations without the multi-year public earnings histories that allow investors to calibrate price against performance. The challenge is not that these companies lack value; it is that the market lacks the data to independently verify the valuations being proposed.

- Capital crowding is a timing problem. Multiple large deals concentrated in a single quarter compound the supply effect. Deals spread across 12-18 months allow more gradual absorption. The timing and sequence of any Anthropic or SpaceX listing, should they proceed, will determine whether the supply effect is concentrated or distributed.

Investors should also distinguish clearly between the confirmed and the reported. The Alphabet programme is documented and quantified. The Anthropic and SpaceX deals are reported by credible outlets but have not been independently corroborated. Portfolio risk assessment that treats reported deals as confirmed overstates near-term supply pressure; assessment that ignores them entirely understates the pipeline.

The convertible bond wave offers one additional signal. If AI company management teams are issuing instruments with embedded equity upside, those teams are implicitly signalling confidence in their own equity trajectory. Companies expecting their stock to fall would not issue convertibles; the conversion feature would work against them.

Bloomberg analysts project Q4 2025 net US equity supply will reach approximately +$40 billion, a confirmed reversal from the -$44 billion buyback-era baseline. This remains the single most quantified anchor for assessing the AI capital wave’s market impact. Source: Bloomberg analysts via Briefing.com, late May 2026

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The market is already absorbing the first wave. The bigger question is what comes next.

The AI capital-raising wave is not a future event to monitor. It is underway. Alphabet’s $80 billion programme has already provided the first confirmed, quantified evidence of its market impact: an $84 billion swing in net US equity supply for a single quarter, documented by Bloomberg analysts and reported by Briefing.com.

The question for investors is not whether AI companies deserve high valuations. It is whether public markets can absorb this volume of new supply without a structural repricing of risk. The answer depends heavily on what follows.

If Anthropic and SpaceX proceed as reported, the supply effect compounds. If they delay or scale down, the market has more time to absorb what Alphabet has already introduced. Monitoring that pipeline, distinguishing confirmed programmes from reported plans, and tracking the timing of any additional listings is the most actionable step available to US investors today.

For investors assessing their exposure to this supply wave, our dedicated guide to US portfolio concentration risk examines how the average US investor’s 70-76% domestic equity weighting has become a de facto concentrated bet on the AI infrastructure capex cycle, with Bridgewater, BlackRock, Goldman Sachs, and JPMorgan all identifying this tilt as structurally disadvantageous under a reflationary macro regime, and walks through specific reallocation steps toward international equities and real assets.