How a 4.75% Wage Rise Repriced the Entire ASX in One Morning

6 hrs ago

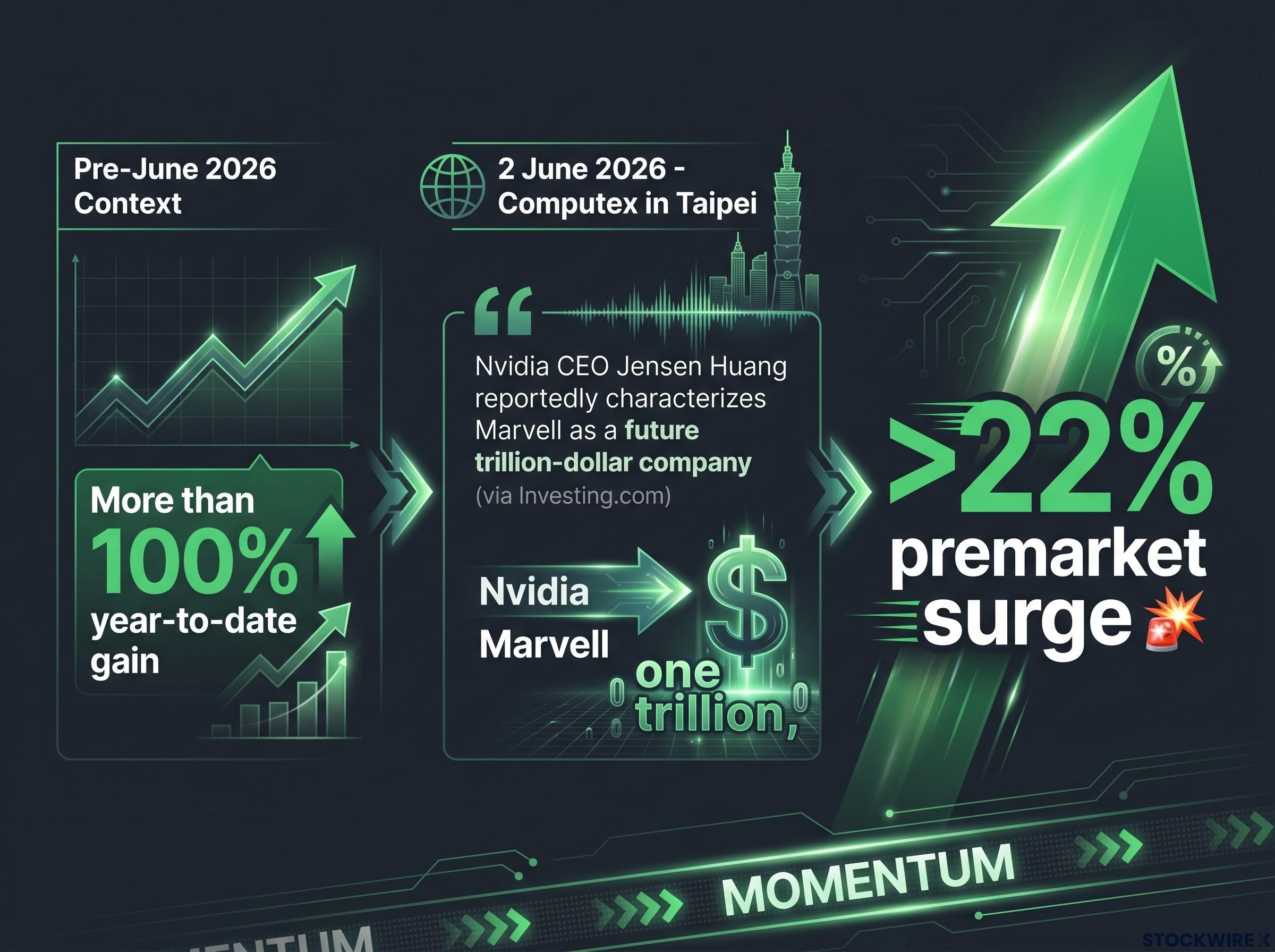

Marvell Technology stock surged more than 22% in premarket trading on 2 June 2026, following a reported public endorsement from Nvidia CEO Jensen Huang at Computex in Taipei. The move marked one of the sharpest single-session premarket gains in the semiconductor sector this year. It also landed on a stock that had already more than doubled on a year-to-date basis, placing Marvell Technology at the centre of a broader investor conversation about which chipmakers stand to capture the most value from hyperscaler AI infrastructure buildout. What follows is an examination of the catalyst behind the surge, the company’s own revised financial guidance, the structural demand dynamics underpinning its growth thesis, and whether the fundamentals beneath the price action justify the momentum.

The catalyst was specific: Nvidia CEO Jensen Huang and Marvell CEO Matt Murphy reportedly made a joint appearance at Computex in Taipei, during which Huang characterised Marvell as a future trillion-dollar company. The appearance and the language were reported by Vahid Karaahmetovic via Investing.com on 2 June 2026.

Source context: The “future trillion-dollar company” characterisation is attributed to Jensen Huang as reported by Investing.com. As of the time of publication, major financial and technology outlets, including Reuters, Bloomberg, CNBC, and the Wall Street Journal, had not independently confirmed the exact language or the joint appearance.

That reporting caveat matters, but it does not diminish the observable market event. The 22% premarket surge is the concrete fact. Shares moved on the report regardless of whether the precise quotation is later confirmed verbatim or softened in subsequent coverage.

For investors, the distinction is between a catalyst that has been independently verified across institutional research desks and one that is, for now, single-sourced. The price action is real. The evidentiary basis for the specific trigger remains narrow.

The Computex report did not create Marvell’s momentum. It accelerated it.

Marvell Technology shares had already gained more than 100% on a year-to-date basis as of 2 June 2026, according to Investing.com.

That trajectory had been building on the back of the company’s strategic positioning in custom AI silicon and data-centre interconnect, two product categories that sit directly in the path of hyperscaler capital expenditure. Investor interest had been compounding for months before Huang’s name entered the narrative.

A 22% premarket move is extraordinary in isolation. Layered on top of a 100%+ year-to-date run, it raises a sharper question: is the valuation trajectory tracking the fundamentals, or has sentiment begun to outpace the revenue base that has to justify it? The answer depends on what Marvell’s own numbers say.

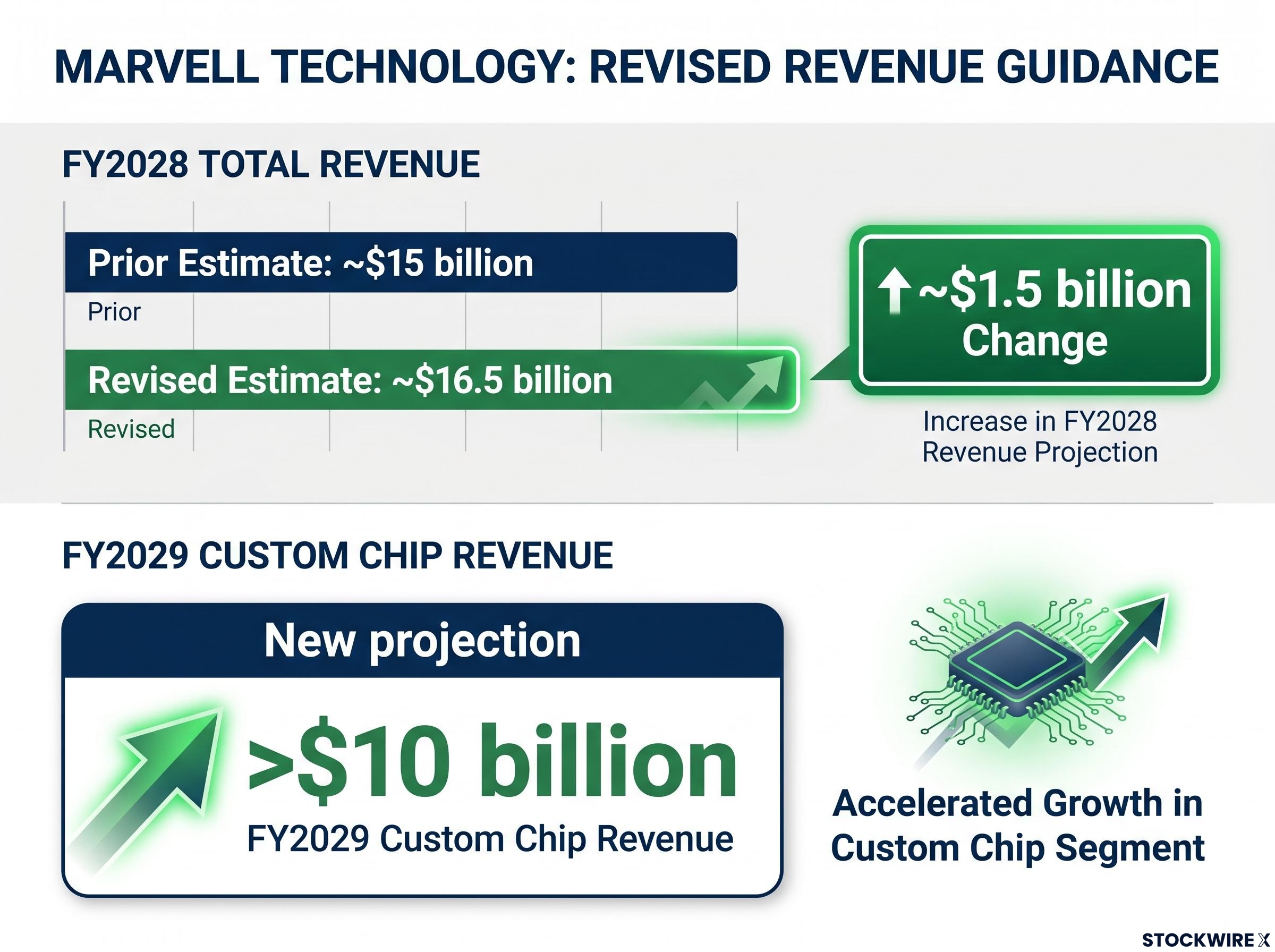

The strongest available signal sits in Marvell’s revised forward-looking guidance, released in the week prior to the Computex event.

| Metric | Prior Estimate | Revised Estimate | Change |

|---|---|---|---|

| FY2028 Total Revenue | ~$15 billion | ~$16.5 billion | +~$1.5 billion |

| Custom Chip Revenue (FY2029) | Not previously specified | >$10 billion | New projection |

An upward revision of approximately $1.5 billion in total revenue guidance for a single fiscal year is rare in the semiconductor sector. It signals management confidence in demand visibility, the kind of forward commitment that typically reflects contracted or near-contracted customer commitments rather than speculative pipeline.

The custom chip segment projection adds a second layer. Projecting that a single business line could exceed $10 billion annually by FY2029 positions custom silicon as the company’s dominant growth engine, not a secondary contributor.

No third-party analyst note has been located that explicitly bridges this guidance to a trillion-dollar valuation path. The revenue figures give investors a concrete basis for independent assessment, but the analytical connection between the guidance and the Huang characterisation remains undrawn by institutional research as of today.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The revenue projections above do not exist in a vacuum. They rest on a specific structural demand thesis that has been building across the semiconductor industry for the past two years.

Marvell’s AI-driven growth rests on two product pillars:

The demand driver behind both is straightforward. Major cloud providers are scaling AI data-centre construction at an accelerating pace and are motivated to reduce dependency on any single chip supplier for their AI hardware needs. That supplier diversification impulse structurally expands the addressable market for companies offering custom silicon alternatives.

Custom ASICs and interconnect serve different functions in the data-centre stack. ASICs replace general-purpose processors with chips designed for a narrow set of tasks, offering efficiency gains on specific workloads. Interconnect technology, by contrast, is the networking fabric that allows thousands of GPUs or accelerators to communicate during training runs. Both are required at scale; neither substitutes for the other.

Marvell’s investor materials describe the company as an active supplier of data-centre and cloud networking silicon, though no named hyperscale customers, such as Amazon Web Services, Google Cloud, or Microsoft Azure, have been confirmed in recent 2025-2026 disclosures for the custom AI ASIC programme specifically.

Two threads run through this story, and they point in the same direction without fully converging.

The fundamental thread is real. A $1.5 billion upward revision to FY2028 revenue guidance and a $10 billion+ custom chip projection for FY2029 represent the kind of forward commitments that institutional investors price into valuation models. These numbers existed before Huang spoke at Computex. They would matter even if he had not.

The sentiment thread is also real, and it carries a different risk profile. A stock that has gained more than 100% year-to-date and then surges an additional 22% on a single reported endorsement, one not yet confirmed by major financial outlets, is exhibiting momentum characteristics that deserve scrutiny alongside the fundamentals.

The question is not whether the fundamental story is genuine. The question is whether a trillion-dollar characterisation, currently sourced to a single report, is doing more work in the stock price than the revenue guidance can support on its own.

What would convert the current trajectory into confirmed validation is specific: named customer disclosures for the custom ASIC programme, independent analyst coverage explicitly linking the revised guidance to a valuation framework, and revenue execution against the FY2028 and FY2029 targets over the coming quarters.

The picture is two-layered. Beneath the sentiment event sits a genuine fundamental story: revised upward guidance, a custom silicon segment projected to exceed $10 billion by FY2029, and a structural demand thesis driven by hyperscaler diversification away from single-supplier dependence. Above it sits a catalyst whose exact details remain single-sourced and unconfirmed by major financial outlets.

The FY2028 and FY2029 revenue targets are the most reliable signal available. Execution against those targets, not a reported endorsement, will determine whether the current valuation reflects rational repricing or gets ahead of itself. Investors watching this name from here have a clear checklist: named customer confirmations, independent analyst coverage of the guidance revision, and Q3-Q4 2026 earnings execution.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Marvell Technology stock surged more than 22% in premarket trading on June 2 2026 following a reported public endorsement from Nvidia CEO Jensen Huang at Computex in Taipei, where he reportedly characterised Marvell as a future trillion-dollar company.

A custom AI ASIC is a purpose-built chip co-developed with a specific hyperscaler customer for targeted workloads, offering an alternative to off-the-shelf GPU procurement. Marvell projects this business line could exceed $10 billion in annual revenue by FY2029, making it the company's dominant growth engine.

Marvell revised its FY2028 total revenue estimate upward by approximately $1.5 billion, from roughly $15 billion to roughly $16.5 billion, and introduced a new projection that its custom chip segment would exceed $10 billion annually by FY2029.

The endorsement is currently single-sourced to a report by Investing.com, and as of publication major outlets including Reuters, Bloomberg, CNBC, and the Wall Street Journal had not independently confirmed the exact language or the joint appearance at Computex.

Investors should monitor named customer confirmations for the custom ASIC programme, independent analyst coverage explicitly linking the revised guidance to a valuation framework, and revenue execution against the FY2028 and FY2029 targets across Q3-Q4 2026 earnings reports.