In April 2026, the Australian Securities and Investments Commission published a report that described one of the country’s most systemically important financial institutions as having weakened resilience, inadequate governance, and risk management practices not properly integrated into day-to-day operations. The subject was not a failed bank or a collapsed broker. It was the ASX itself.

The ASX Inquiry Panel Final Report, delivered on 31 March 2026 and published by ASIC on 2 April 2026, is the product of an unprecedented regulatory intervention. ASIC characterised the inquiry as a step taken only after prior regulatory efforts, including expert reviews, enforcement actions, licence conditions, and legislative reform, had failed to produce the required improvements. What follows is an analysis of what the Final Report actually found, why its conclusions matter beyond regulatory compliance, and what the ASX case reveals about the governance responsibilities attached to operating critical market infrastructure in Australia.

A stock exchange with a structural identity problem

The ASX operates under a dual identity that sits at the centre of every finding in the inquiry report. It is a publicly listed commercial entity, optimising for shareholder returns. It is also the licensed operator of Australia’s critical market infrastructure, responsible for the clearing and settlement systems through which every equity transaction in the country passes.

That duality is not incidental. It is structural, and the inquiry concluded it produced a specific result: the prioritisation of shareholder returns undermined the resilience of the infrastructure the ASX is licensed to protect.

The six entities under examination

The inquiry’s scope covered six ASX group licensees, spanning both market operations and clearing and settlement functions under the Corporations Act 2001 (Cth).

| Entity | Licence Type | Statutory Provision |

|---|---|---|

| ASX Limited | Australian market licence | Section 795B(1) |

| Australian Securities Exchange Limited | Australian market licence | Section 795B(1) |

| ASX Clear Pty Limited | CS facility licence | Section 824B(1) |

| ASX Settlement Pty Limited | CS facility licence | Section 824B(1) |

| ASX Clear (Futures) Pty Limited | CS facility licence | Section 824B(1) |

| Austraclear Limited | CS facility licence | Section 824B(1) |

The breadth of that scope is itself significant. This was not a review of a single system or a single operational failure. It was an assessment of the entire ASX group’s fitness to operate the infrastructure the Australian market depends on.

When big ASX news breaks, our subscribers know first

How escalating regulatory intervention led to a formal inquiry

ASIC did not arrive at the decision to commission a formal inquiry quickly. The regulator exhausted a series of conventional tools before reaching for this one, and the escalation ladder matters for understanding the weight of what followed.

Prior to the inquiry, ASIC had pursued:

- Expert reviews of ASX operations and technology

- Enforcement actions related to specific operational failures

- Licence conditions imposed to compel improvements

- Legislative reform efforts aimed at strengthening the regulatory framework

Each intervention produced insufficient change. The inquiry was commissioned under sections 794C(1) and 823C(1) of the Corporations Act 2001 (Cth), provisions that authorise ASIC to investigate whether a licensed operator is meeting its obligations. Using them represented a formal declaration that conventional regulatory oversight had not worked.

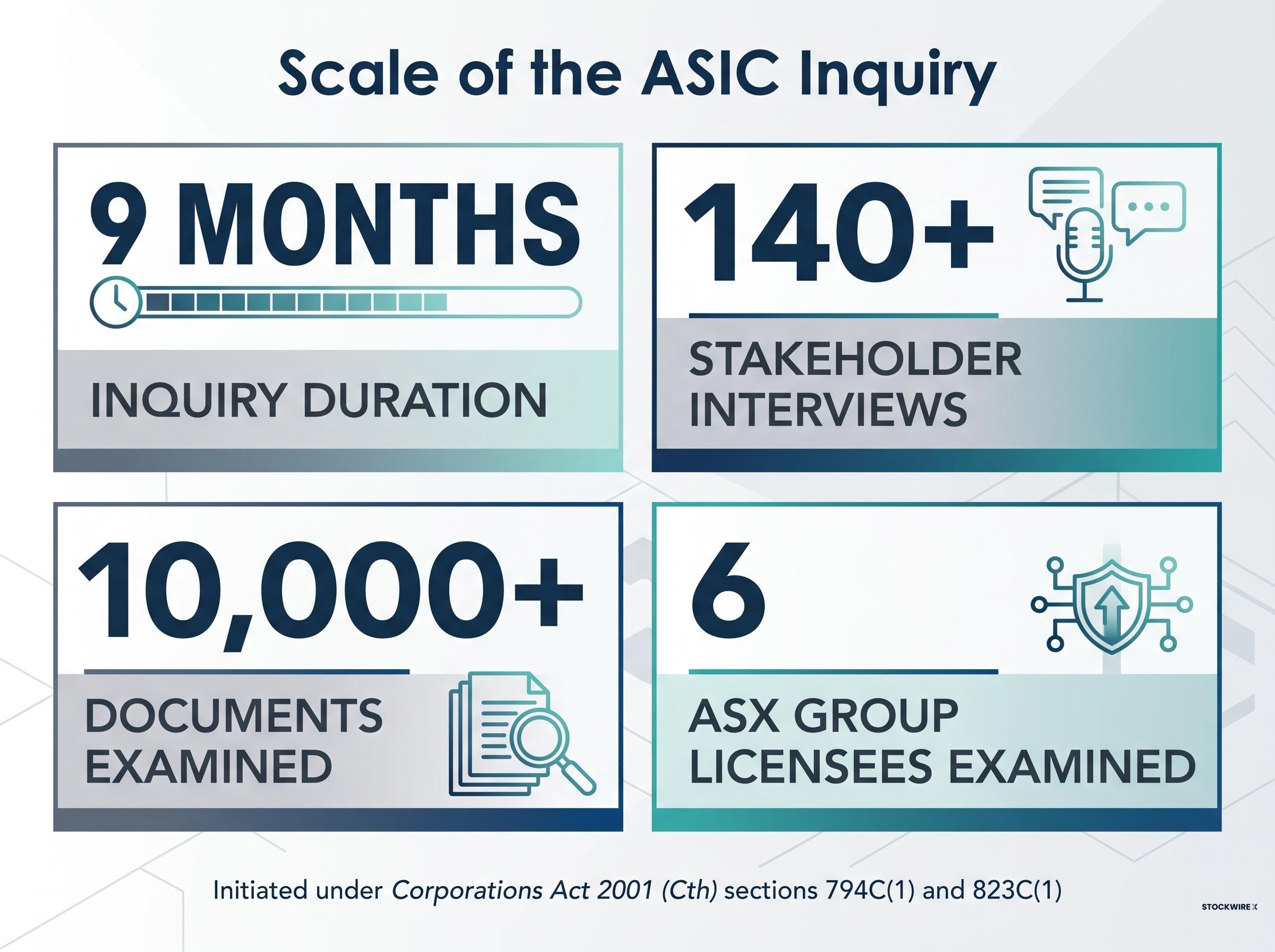

The inquiry commenced in June 2025, with Terms of Reference established in July 2025. Over nine months, the Panel conducted more than 140 stakeholder interviews, examined over 10,000 documents, commissioned an independent technical assessment of the CHESS system, undertook international benchmarking, and held focus groups with ASX personnel. An Interim Report was released in December 2025 before the Final Report was delivered on 31 March 2026.

ASIC Chair Joe Longo confirmed upon publication that the Final Report substantiated the scale of reform deemed necessary and validated the appropriateness of commissioning the inquiry in the first place.

That statement carried a specific message: ASIC stood behind the decision to escalate, and the findings justified the intervention.

What good governance looks like for critical market infrastructure

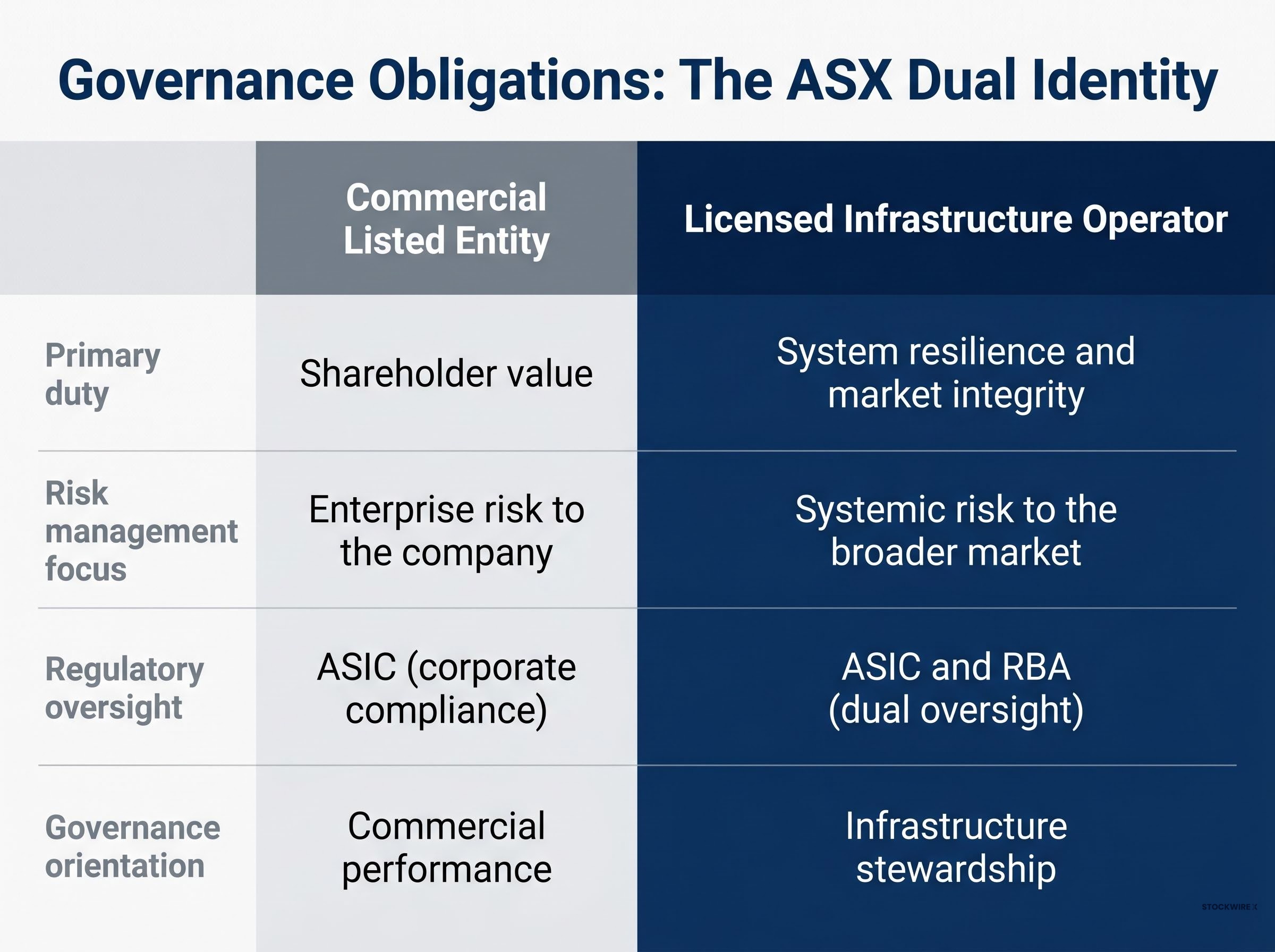

Understanding why the Panel’s findings carry the weight they do requires understanding the governance standard against which the ASX was measured, and why that standard differs from what is expected of an ordinary listed company.

Critical market infrastructure, in the Australian regulatory context, refers to systems whose failure or degradation would impair the functioning of the broader financial system. Clearing and settlement facilities fall squarely into this category. Every equity transaction on the Australian market relies on these systems to complete.

That designation attracts heightened governance obligations. An ordinary listed company must satisfy its shareholders and comply with general corporate law. A licensed critical infrastructure operator must go further: system resilience, fair access, and participant protection are primary duties, not secondary considerations subordinate to commercial returns.

| Obligation | Commercial Listed Entity | Licensed Infrastructure Operator |

|---|---|---|

| Primary duty | Shareholder value | System resilience and market integrity |

| Risk management focus | Enterprise risk to the company | Systemic risk to the broader market |

| Regulatory oversight | ASIC (corporate compliance) | ASIC and RBA (dual oversight) |

| Governance orientation | Commercial performance | Infrastructure stewardship |

The standard is not unusually high. It is the standard the ASX’s licences require. Risk management must be integrated into day-to-day operations as a systematic function, not deployed reactively when incidents occur. The Panel concluded that the ASX lacked “the organisational orientation required to function as a proper steward of critical market infrastructure.” That language is precise, and it points to a gap not in individual processes but in the institution’s fundamental posture.

How deeply the failures ran: governance, culture, and risk management

The Panel’s findings did not describe surface-level deficiencies correctable by a board resolution or a policy update. They described failures embedded across three interconnected domains, each reinforcing the others.

Governance failures

Existing governance arrangements were assessed as failing to provide adequate focus on the responsibilities associated with operating critical market infrastructure. The board lacked the organisational orientation required of an infrastructure steward, a finding that speaks to the institution’s priorities at the highest level rather than to the competence of individual directors.

The implication is structural. When governance does not orient the institution toward its infrastructure obligations, every decision downstream, on capital allocation, on technology investment, on risk resourcing, is shaped by that misalignment.

Culture and capability constraints

The Panel assessed cultural and capability constraints not as isolated shortcomings but as systemic barriers to meaningful transformation. This distinction matters. Isolated problems can be addressed with targeted hiring or process changes. Systemic barriers require significant organisational change because they are embedded in how the institution operates, communicates, and prioritises.

The finding suggests that even well-intentioned reform initiatives would face resistance or dilution within the existing organisational culture, a pattern consistent with institutions where commercial metrics have historically determined internal status and resource allocation.

Risk management and compliance gaps

Risk management and compliance practices were found to be insufficiently developed and not properly integrated into day-to-day business operations.

The Panel characterised the ASX’s approach to incidents and identified shortcomings as “overly reactive and ad hoc,” producing responses to problems after they materialised rather than systematic prevention.

The additional dimension flagged by the Panel extends beyond internal operations. The ASX’s execution of its own market supervision responsibilities, including monitoring and enforcing adherence to Operating and Listing Rules, was identified as warranting further examination. This raises a separate set of questions about whether the governance and cultural failures within the organisation also affected the quality of its supervisory functions over market participants.

The simultaneous failure across governance, culture, and risk management points to a reinforcing system: inadequate governance permitted a commercial culture to dominate, which in turn starved risk management of the integration and resources required for systematic operation.

Regulatory accountability mechanisms now attached to ASX’s reform programme

The inquiry did not conclude with a report that sits on a shelf. Regulatory consequences began accumulating before the Final Report was even published, and the accountability structure now in place carries ongoing supervisory weight.

- December 2025: Regulatory actions taken under sections 794C(1) and 823C(1) of the Corporations Act 2001 (Cth), including commitments secured from the ASX during the inquiry process

- 2 April 2026: ASIC published the Final Report; the ASX issued its own response on the same day

- Ongoing: Supervision of the ASX’s Commitments Plan confirmed as falling jointly to ASIC and the Reserve Bank of Australia

- 20 April 2026: CHESS Release 1 went live, representing one operational milestone within the broader reform context (this date is sourced from reporting not independently confirmed)

The dual oversight arrangement, with both ASIC and the RBA supervising the reform programme, signals the seriousness of the regulatory response. The RBA’s involvement reflects the systemic importance of clearing and settlement functions to financial stability, a domain that extends beyond ASIC’s market conduct mandate.

The ASX’s decision to publish its response on the same day as the Final Report’s release suggests an organisation that anticipated the findings and sought to demonstrate engagement with the reform process from the outset. The technology dimension, including the CHESS replacement programme, represents one component of a much larger governance and culture transformation the inquiry demands.

What the ASX inquiry tells Australia about governing market infrastructure

The ASX case carries implications beyond a single institution’s reform programme. It demonstrates what can happen when commercial incentive structures operate unchecked within institutions that carry public-interest obligations, a tension that exists wherever critical infrastructure is privately operated.

The inquiry’s unprecedented status raises a question about Australia’s existing regulatory toolkit. If ASIC had to exhaust expert reviews, enforcement actions, licence conditions, and legislative reform before reaching the point of a formal inquiry, the toolkit may not be calibrated for the speed of intervention that complex, systemic infrastructure operators require. The nine-month duration and the scale of resources deployed, more than 140 interviews, 10,000 documents, independent technical assessment, international benchmarking, suggest that even identifying the full scope of the problem demanded a level of investigative commitment that routine supervision cannot provide.

The forward implication is a shift in the regulatory posture available to ASIC and the RBA. The inquiry establishes a precedent for more assertive intervention when licensed critical infrastructure operators fail to meet governance standards. Every operator holding market or clearing and settlement licences in Australia now operates in a regulatory environment where ASIC has demonstrated its willingness to commission a formal inquiry, publish the findings, and attach ongoing supervisory accountability to the reform programme that follows.

The standard ASX must now meet, and why it matters for Australian markets

The reform demands placed on the ASX are comprehensive: governance restructuring, culture transformation, risk management integration into daily operations, and ongoing supervisory accountability to both ASIC and the RBA. These are not incremental improvements. They represent a fundamental reorientation of how the institution approaches its infrastructure obligations.

The stakes are proportionate to the ASX’s role. Its clearing and settlement infrastructure underpins every equity transaction in Australia. Governance failures at this level carry systemic risk implications that extend to listed companies, market participants, and the investors whose assets move through these systems daily.

The publication of the Final Report on 2 April 2026 is not the conclusion of the reform story. It is the beginning of a supervised accountability process whose outcomes will determine whether the inquiry’s findings translate into durable institutional change, or whether they join the list of prior interventions that failed to shift the ASX’s orientation toward the infrastructure stewardship its licences demand.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.