How to Spot AI Investment Scams Before They Cost You Money

28 mins ago

Nearly two-thirds of Gen Z Australians now turn to social media for financial guidance. That single statistic, drawn from ASIC’s own commissioned research published in March 2026, captures a behavioural shift that has moved faster than the regulatory infrastructure designed to protect consumers from bad advice. In April 2026, ASIC responded by issuing warning notices to four finfluencers and joining 16 international regulators in a coordinated global crackdown, signalling that this is no longer a theoretical concern but an active consumer harm issue. Weeks earlier, ASIC’s Moneysmart report had revealed just how deeply finfluencer content has embedded itself in the financial decision-making of young Australians. What follows is a clear explanation of why algorithm-driven platforms create financial misinformation risk, what the law actually says about who can give financial advice in Australia, and the specific steps readers can take right now to verify whether someone is licensed before acting on their content.

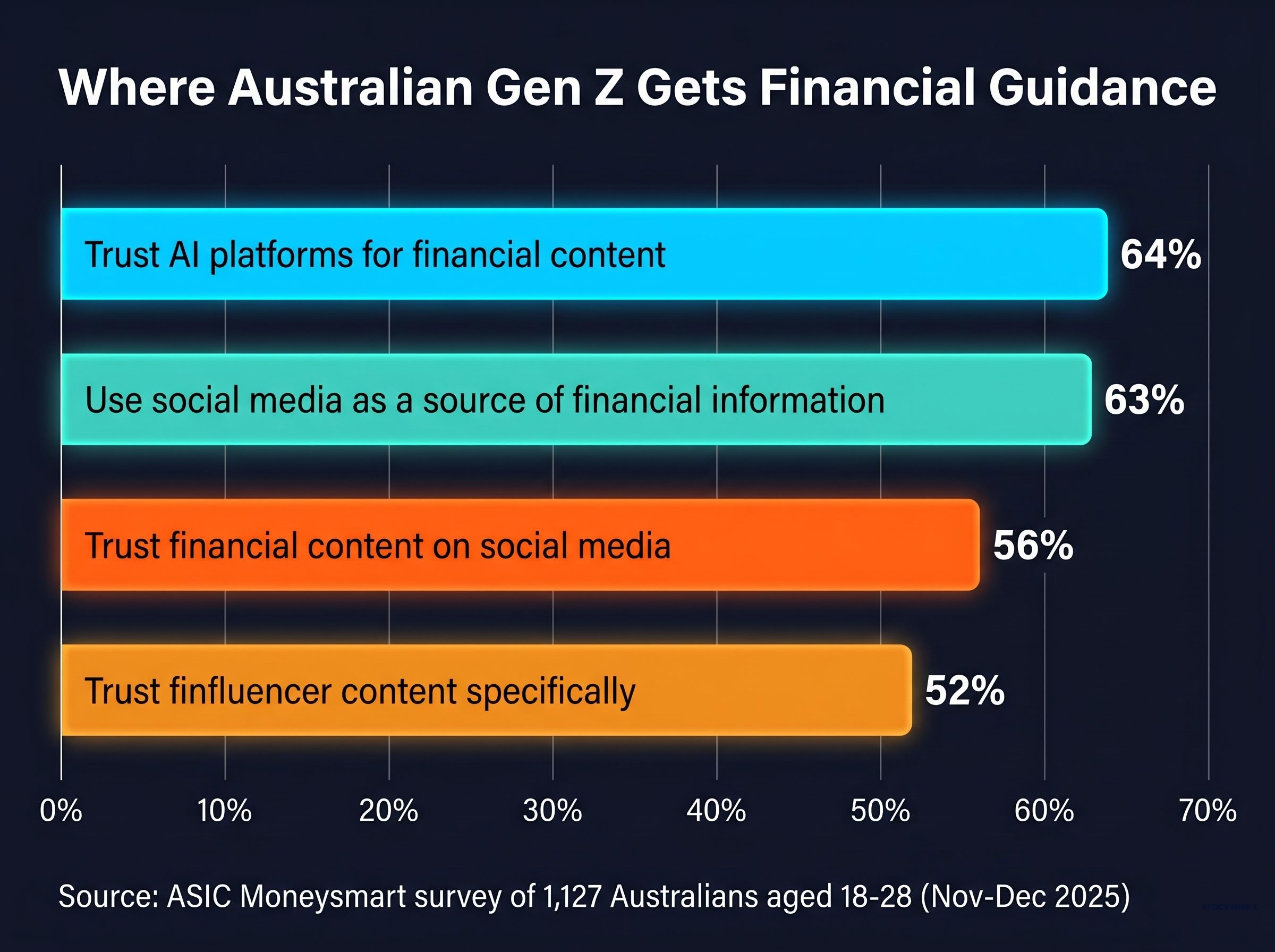

The scale of the shift is difficult to overstate. ASIC’s Moneysmart Gen Z Financial Behaviours Report, based on YouGov fieldwork surveying 1,127 Australians aged 18-28 between November and December 2025, found that 63% of Gen Z respondents use social media as a source of financial information and guidance.

The trust figures sharpen the picture further:

These are not fringe behaviours. More than half of young Australians surveyed placed trust in content that carries no regulatory obligation to be accurate, suitable, or in the viewer’s interest. The AI platform figure is the highest of the three, suggesting this is a cross-channel phenomenon that extends well beyond individual influencers.

Gen Z investing patterns show a generation that is simultaneously more engaged with financial markets than any prior cohort at the same life stage and more exposed to unregulated information channels; Australian Millennials already allocate roughly 70% of investment capital to ETFs, and the trajectory for Gen Z points toward even greater active portfolio engagement, raising the stakes of decisions made on the basis of unverified social media content.

ASIC Commissioner Alan Kirkland observed that platform algorithms prioritise engagement and clicks over accuracy, heightening consumer exposure to biased or inaccurate financial content.

That structural observation sits beneath all three trust figures. Popularity on these platforms is not a proxy for reliability, yet the trust data suggests a significant proportion of young Australians treat it as one.

A finfluencer, in its simplest form, is a social media creator who produces financial content. That content can range from stock tips and crypto recommendations to general budgeting commentary. From a viewer’s perspective, all of it may look the same: a person on a screen talking confidently about money.

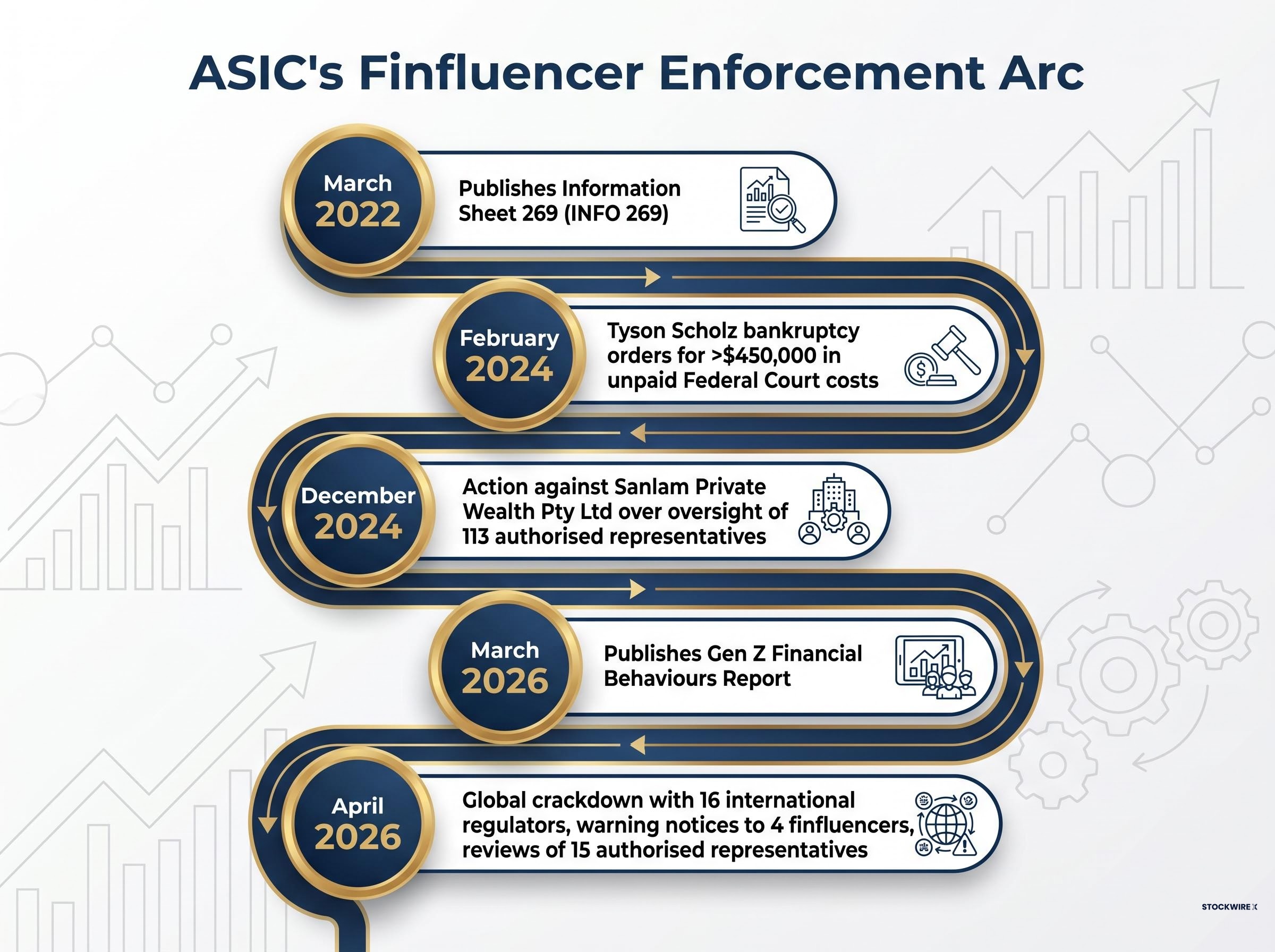

The legal distinction, however, exists specifically to protect viewers. ASIC Information Sheet 269 (INFO 269), first issued in March 2022 and unrevised as at May 2026, draws the boundary. General financial commentary, such as discussing market trends or explaining how compound interest works, does not require a licence. Providing financial product advice does. That threshold is crossed when a creator recommends specific financial products or tailors recommendations to a viewer’s circumstances. At that point, an Australian Financial Services (AFS) licence is required.

AFS licence obligations do not disappear when a business winds down or goes dormant; financial reporting, competence standards, and breach reporting requirements under s 912A of the Corporations Act continue to apply, which is part of why ASIC actively manages its register and cancelled or suspended 215 licences in FY 2024-25 alone.

ASIC Information Sheet 269 draws the operative boundary between general financial commentary and financial product advice, specifying that recommending specific products or tailoring guidance to individual circumstances triggers the AFS licence requirement under the Corporations Act.

There is a legal mechanism for unlicensed finfluencers to operate within the regulatory framework. An AFS licensee can appoint a finfluencer as an authorised representative, granting them the ability to provide financial product advice under the licensee’s supervision. In this arrangement, the AFS licensee bears full legal liability for the finfluencer’s conduct.

The table below sets out the three operating categories:

| Category | Licence Required | Who Bears Liability | Legal Basis |

|---|---|---|---|

| Unlicensed general commentator | No | Creator (limited; no advice obligation) | INFO 269 general commentary safe harbour |

| Authorised representative under AFS licensee | No (operates under licensee) | AFS licensee | Corporations Act; AFS licence conditions |

| AFS licence holder | Yes | Licence holder | Corporations Act; AFS licence obligations |

ASIC’s April 2026 enforcement announcement explicitly cited INFO 269, confirming it remains the operative guidance framework. Most viewers cannot tell which category a creator falls into. Understanding these distinctions gives readers a framework for asking the right question before they act on what they see.

On 26 April 2026, ASIC issued warning notices to four finfluencers suspected of providing unlicensed financial advice or engaging in misleading or deceptive conduct. The action was not isolated. It formed part of a coordinated global crackdown conducted alongside 16 other international regulators, a signal that finfluencer misconduct is a cross-border problem attracting cross-border regulatory resolve.

At the same time, ASIC commenced reviews of several AFS licensees regarding their supervision of 15 finfluencers operating as authorised representatives. The message to licensees was direct: supervisory obligations in the finfluencer context are not optional, and ASIC is actively testing whether they are being met.

The April actions sit within a longer enforcement arc:

Tyson Scholz’s unpaid Federal Court costs exceeded $450,000, a figure that illustrates the real financial consequences already flowing from ASIC’s enforcement actions against individual finfluencers.

The Sanlam case is equally instructive. It demonstrated ASIC’s willingness to pursue not just the individuals creating content but the institutions responsible for supervising them. Readers who think “it’s just social media” should note that real legal consequences have already followed from real harm.

Social media recommendation algorithms are designed to maximise watch time, shares, and emotional engagement. They are not designed to surface factual accuracy or consumer benefit. This structural incentive creates a systematic disadvantage for careful, qualified financial content. A cautious, licensed adviser explaining the limitations of a strategy will almost always lose the algorithmic contest to a confident, entertaining creator promising outsized returns.

ASIC Commissioner Alan Kirkland identified this dynamic directly, noting that platform algorithms prioritise engagement and clicks over accuracy, which heightens consumer exposure to biased or inaccurate financial content. The problem extends beyond traditional social media. ASIC’s own data shows 64% of Gen Z respondents trust AI platforms for financial content, suggesting that algorithm-driven amplification of unreliable guidance is not confined to any single platform type.

The AI financial advice risks are compounded by a confidence problem: tools like ChatGPT and Claude deliver correct and incorrect answers in the same assured tone, and research suggests roughly three in ten responses to Australian financial queries contain errors, with SMSF rules and superannuation contribution limits among the highest-risk categories for mistakes.

Consider what each system optimises for:

ASIC’s commentary accompanying the March 2026 report specifically noted that reliance on social media and AI platforms can fuel riskier financial decisions, including crypto investment. The crypto context grounds the algorithm problem in a concrete asset class risk: content promoting speculative crypto trades performs well algorithmically precisely because it triggers the emotional engagement signals platforms reward.

Understanding this structural mismatch changes how readers evaluate what they encounter. Virality and trustworthiness are not merely different qualities; on financial topics, they are structurally at odds.

The verification process is straightforward. ASIC maintains a publicly accessible professional registers search tool that allows Australians to check whether any individual or business holds an AFS licence or is listed as an authorised representative.

The steps are sequential:

Suspected unlawful finfluencer activity can be reported to ASIC by phone at 1300 300 630 or through the online misconduct reporting page. Moneysmart also offers free, independent financial information as an alternative resource.

The two-level check matters. A creator may not hold their own AFS licence but may appear as an authorised representative on a licensee’s register. Both results indicate a regulated arrangement. The absence of both is the signal that the creator operates outside the regulatory framework, and that their content, however confident, carries no obligation to be accurate, suitable, or in the viewer’s interest.

Not all finfluencer content is harmful. General financial literacy content, market commentary, and budgeting education can be genuinely useful. The risk arises when general content is treated as personalised advice, or when viewers act on specific product recommendations from creators who carry no regulatory obligation to get it right.

ASIC’s own language from the March 2026 Moneysmart report offers a practical framework. Before acting on any financial content encountered online, apply three questions:

If any answer is no, the content may still be worth watching for general education, but it should not drive a financial decision. Moneysmart, ASIC’s free independent financial information resource, offers a reliable alternative for consumers seeking general guidance. For decisions with real financial stakes, such as product selection, investment allocation, or retirement planning, licensed financial advisers remain the appropriate source of advice that carries regulatory accountability.

For readers who have taken the verification steps and are now ready to build a structured approach to wealth-building, our dedicated guide to financial sequencing for young Australians covers the ordered framework of income growth, borrowing capacity, superannuation optimisation, and first home buyer scheme access that licensed financial practitioners recommend as the evidence-based alternative to social media shortcuts.

The goal is not to stop consuming financial content. The goal is to recognise the difference between content that informs and advice that should come from a qualified professional.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

ASIC’s April 2026 global crackdown and its own research showing elevated Gen Z trust levels are two sides of the same problem: a generation placing confidence in content that platforms are structurally incentivised to amplify regardless of accuracy, delivered by creators who may have no legal obligation to get it right. The framework for sitting on the right side of that line is now clear.

Algorithms reward confidence over credentials. Australian law requires an AFS licence for financial product advice. ASIC’s professional registers make verification a 60-second task.

Before acting on any financial content encountered online, spend those 60 seconds on the ASIC professional registers search tool. Check the creator’s name. Confirm their status. That single step is the difference between consuming content and consuming advice, and only one of those carries regulatory protection.

General financial commentary covers topics like market trends or budgeting concepts and does not require a licence. Financial product advice, which involves recommending specific products or tailoring guidance to an individual's circumstances, requires an Australian Financial Services (AFS) licence under the Corporations Act, as outlined in ASIC Information Sheet 269.

You can search the creator's name or business name on ASIC's publicly accessible professional registers search tool to confirm whether they hold an AFS licence or are listed as an authorised representative under an existing licensee. If neither result appears, treat their content as general commentary only, not as regulated financial product advice.

On 26 April 2026, ASIC issued warning notices to four finfluencers suspected of providing unlicensed financial advice or engaging in misleading or deceptive conduct, as part of a coordinated global crackdown alongside 16 other international regulators. ASIC also commenced reviews of several AFS licensees regarding their supervision of 15 finfluencers operating as authorised representatives.

Social media algorithms are designed to maximise watch time, shares, and emotional engagement rather than surface accurate or suitable financial content. This means confident, entertaining creators promising high returns will typically outperform cautious, qualified advisers algorithmically, as ASIC Commissioner Alan Kirkland directly acknowledged.

According to ASIC's Moneysmart Gen Z Financial Behaviours Report, based on a YouGov survey of 1,127 Australians aged 18-28 conducted in late 2025, 63% use social media as a source of financial information, 52% trust finfluencer content specifically, and 64% trust AI platforms for financial content.