Betashares ERTH ETF: Macro Tailwind Meets Real Volatility Risk

27 mins ago

After the February 2026 reporting season, companies outside Australia’s largest 50 delivered some of the strongest earnings surprises on the ASX. Their share prices, largely, did not reflect it. The S&P/ASX 50 continues to dominate headline returns and investor attention, anchored by familiar names like BHP Group and Commonwealth Bank of Australia. But a combination of earnings momentum, historical breadth patterns, and a US market already signalling a leadership rotation raises a pointed question for Australian investors: is the mid-cap discount a temporary anomaly or a genuine setup? This analysis unpacks the valuation gap between ASX mid-cap stocks and their large-cap counterparts, examines what the February 2026 reporting season revealed about earnings trajectory, and provides a framework for assessing whether current conditions favour a broadening of market leadership.

BHP and CBA are not simply large companies. They are structural anchors of the ASX, disproportionately driving headline returns for the S&P/ASX 200 in a way that is self-reinforcing rather than coincidental. The dominance persists because three mechanisms feed on each other, concentrating capital and attention at the top of the market.

This creates a specific asymmetry. Large-cap stocks carry high analyst coverage and priced-in expectations, meaning positive surprises are harder to deliver. Mid-cap companies, by contrast, operate with lower visibility and therefore lower priced-in optimism, a dynamic that matters most when earnings begin to shift. According to VanEck analysis, phases in which only a handful of stocks drive overall market returns are atypical relative to longer-run norms. Understanding why that concentration persists is the prerequisite for recognising when it might break.

The self-reinforcing nature of large-cap dominance is inseparable from index inclusion mechanics: float-adjusted market capitalisation thresholds and quarterly rebalance cycles mean that passive flows are structurally directed toward the names already at the top, regardless of their forward earnings trajectory.

ECB research on passive investing and market concentration published in November 2024 found that growing passive fund flows measurably increase return co-movement and index-level concentration in developed equity markets, providing a cross-market evidence base for the self-reinforcing dynamic observed on the ASX between index weighting, passive inflows, and large-cap dominance.

Mid-cap is not a vague descriptor. On the ASX, it refers to a specific segment benchmarked by the S&P/ASX MidCap 50 Index, which tracks 50 established listed companies sitting below the top 50 by market capitalisation. The VanEck S&P/ASX MidCap ETF (ASX: MVE) provides a practical market proxy for this segment, holding 50 positions across multiple sectors:

The risk-return positioning of these companies is distinct from both ends of the market-cap spectrum. Mid-caps are more defensive than small-caps, which often include developmental-stage businesses with unproven revenue models. They are more growth-oriented than large-caps, where earnings bases are large and incremental growth becomes harder to sustain.

That positioning carries particular weight in the current environment. VanEck has observed that periods of elevated interest rates and subdued economic growth have historically coincided with investors becoming more discerning about where earnings growth originates. In such conditions, companies capable of sustaining earnings growth under challenging circumstances tend to attract greater investor focus, independent of company size. The question shifts from “how big is the company?” to “how durable is the growth?”

ASX mid-caps are currently trading at a discount to the S&P/ASX 50 even as their earnings trajectory has strengthened. Morningstar data for MVE shows a price-to-earnings ratio of 14.34 and a price-to-book ratio of 1.72, metrics that, while directional and subject to independent verification, indicate valuations sitting below large-cap averages.

The justification for the large-cap premium has historically rested on more predictable earnings and deeper liquidity. That justification narrows when large-cap earnings expectations become harder to sustain, and when mid-cap companies begin delivering upside surprises. The February 2026 reporting season tested exactly this dynamic.

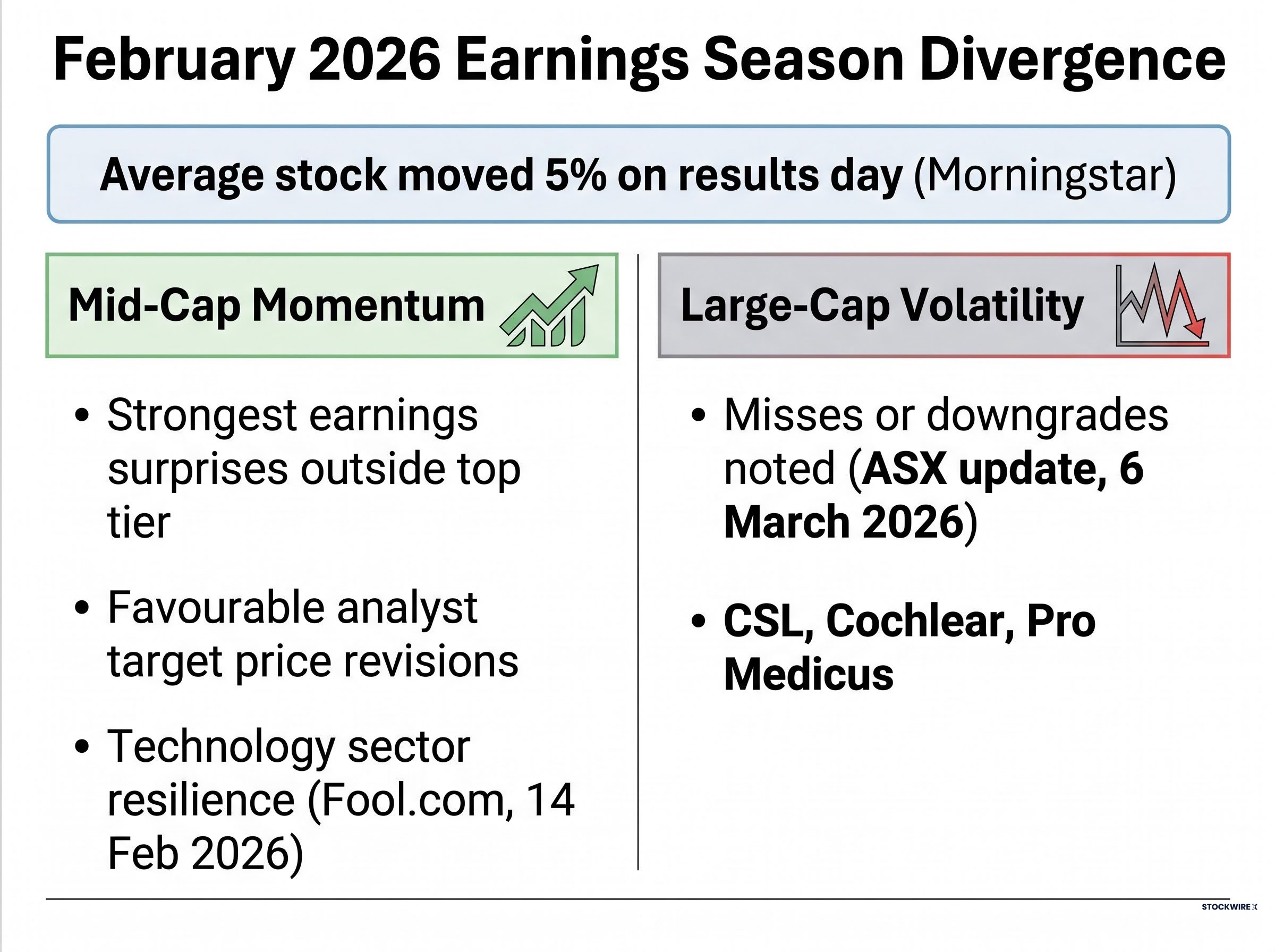

The pattern that emerged from the February 2026 reporting season was specific and measurable. Companies outside the largest ASX tier produced some of the strongest earnings surprises and the most favourable analyst target price revisions across the market. Large-cap stocks, however, outperformed in share price terms following the reporting period.

That disconnect, between fundamental momentum and price response, is where the analytical signal sits.

Cameron McCormack, Senior Portfolio Manager at VanEck, characterised the earnings data as showing that analysts and investors are identifying increasing scope for earnings growth and share price appreciation in smaller companies.

The large-cap earnings picture told a different story. An ASX investor update published on 6 March 2026 highlighted greater volatility and notable misses or downgrades at companies including CSL, Cochlear, and Pro Medicus, three of the ASX’s most closely followed healthcare names. According to Morningstar, the average stock moved 5% on results day during the February season, but the direction of that move diverged sharply between market-cap tiers.

Large-cap earnings delivery risk is quantifiable in the current environment: with the ASX 200 equity risk premium sitting at approximately 80 basis points and the forward P/E at the upper boundary of the range historically consistent with 5%-6% bond yields, even moderate guidance cuts produce outsized share price responses because there is almost no valuation buffer absorbing disappointment.

Earnings revisions are a leading indicator of where analyst and institutional attention is migrating. When revisions are consistently stronger in a segment that trades at a discount, the valuation gap becomes harder to sustain over time.

In the United States, a record proportion of S&P 500 constituents outperformed the broader index in the current period, reversing the concentrated leadership that characterised much of the prior two years. VanEck presents this as a potential leading signal for a similar broadening dynamic in Australian markets, though not a guarantee.

The Australian macro backdrop adds a layer of context. The 10-year Commonwealth government bond yield stood at approximately 4.25% as of 29 May 2026, according to Bloomberg, having pulled back from a reading near 4.96% in April 2026 (YieldReport, 10 April 2026). Elevated yields create an environment where the cost of capital is higher and investors become more discriminating about earnings quality, a dynamic the RBA’s Financial Stability Review (April 2025) noted tends to weigh on longer-duration assets and create sectoral differentiation.

The RBA Financial Stability Review (April 2025) noted that concentration risk in global equity markets has increased in recent years, and that elevated policy rates create refinancing pressure for higher-risk firms, both dynamics that inform how Australian investors should interpret the current divergence between large-cap and mid-cap earnings trajectories.

Pitcher Partners, in a January 2026 Australian equities outlook, noted mid-cap growth momentum and potential for outperformance relative to large-caps amid economic recovery themes.

| Indicator | US reading | Australian reading / context |

|---|---|---|

| Market breadth trend | Record proportion of S&P 500 constituents outperforming the index | Earnings momentum shifting outside ASX top tier; breadth data limited |

| 10-year bond yield | Elevated, supporting earnings-quality rotation | Approximately 4.25% (29 May 2026), down from 4.96% (April 2026) |

| Reported earnings surprise distribution | Broad-based outperformance reversing concentrated leadership | Strongest surprises and target revisions outside ASX top 50 (February 2026) |

Cross-market breadth signals matter because institutional capital is globally mobile. A confirmed leadership rotation in the US removes one of the behavioural barriers to a similar shift on the ASX.

The valuation discount between ASX mid-caps and large-caps is observable. The timing of its closure is not predictable. Before treating the gap as an actionable opportunity, three questions warrant consideration.

Quality-filtered rotation exposure adds a dimension that raw market-cap tier analysis misses: within the segment of companies sitting below large-cap benchmarks, those with demonstrated profitability and balance sheet discipline have historically outperformed the broader small and mid-cap cohort during the early phase of a leadership shift, a pattern visible in the divergence between the quality-screened S&P 600 and the broader Russell 2000 in mid-2026.

The S&P/ASX MidCap 50 Index, accessible through vehicles such as MVE, provides a diversified, 50-stock entry point for investors who conclude the conditions warrant deliberate exposure. A valuation gap is only actionable if the investor has a clear view of the conditions under which it closes.

The combination of a persistent valuation discount, stronger-than-expected earnings momentum from the February 2026 season, a macro environment that historically disadvantages priced-in large-cap premiums, and a US breadth signal that tends to precede similar dynamics elsewhere constitutes a credible thesis. It is not, however, a confirmed one.

The primary risk is straightforward: if Australian macro conditions deteriorate sharply or if large-cap earnings recover strongly in the second half of 2026, the discount may persist without closing. VanEck’s historical observation that narrow mega-cap leadership phases tend to be temporary does not specify how long the temporary period lasts.

For investors wanting to situate the ASX mid-cap thesis within a broader global context, our full explainer on global market leadership rotation examines the multi-decade valuation spreads between US Technology and international developed markets, the institutional positioning data from BlackRock, Vanguard, JPMorgan, and Goldman Sachs, and the historical precedents from the Nifty Fifty, Japan Inc., and the TMT bubble that show how concentrated leadership cohorts have performed in the decade following peak concentration.

The valuation gap between ASX mid-caps and large-caps is real, the earnings signal from February 2026 is building, and the question for investors is one of timing rather than direction.

The sequencing matters. Investors who wait for full confirmation of a rotation may pay a significantly higher entry price than those who build exposure while the discount is observable. Those who move too early may endure an extended period of underperformance relative to large-cap benchmarks. The framework, not the conviction, is what protects against either mistake.

The February 2026 reporting season confirmed that earnings momentum has shifted toward companies outside the ASX’s largest tier, while valuations have not yet followed. The gap between improving fundamentals and lagging share price recognition is observable across multiple data points, from analyst target revisions to earnings surprise distribution.

For investors assessing their positioning, the next steps are specific: review existing portfolio exposure across market-cap tiers, consider whether a structured vehicle tracking the S&P/ASX MidCap 50 Index provides a deliberate entry point, and monitor upcoming reporting seasons for continued analyst revision patterns that either reinforce or challenge the current signal.

The question for the second half of 2026 is not whether a mid-cap valuation gap exists. The data suggests it does. The question is whether the conditions that would allow it to close, including sustained earnings outperformance, macro pressure on large-cap premiums, and eventual institutional reallocation, are assembling at a pace that rewards early positioning.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and valuations discussed are subject to market conditions and various risk factors.

ASX mid-cap stocks refer to the segment tracked by the S&P/ASX MidCap 50 Index, which covers 50 established listed companies sitting below the top 50 by market capitalisation. The VanEck S&P/ASX MidCap ETF (ASX: MVE) provides a practical market proxy for this segment.

Large-cap dominance is driven by three self-reinforcing mechanisms: heavy index weighting that directs passive fund flows, growing ETF and superannuation inflows that concentrate capital at the top, and dense analyst and media coverage that keeps large-cap names visible while mid-tier companies receive less institutional attention.

Companies outside the largest ASX tier produced the strongest earnings surprises and the most favourable analyst target price revisions of the February 2026 season, while notable large-cap names including CSL, Cochlear, and Pro Medicus experienced misses or downgrades.

Morningstar data for the MVE ETF shows ASX mid-caps trading at a price-to-earnings ratio of 14.34 and a price-to-book ratio of 1.72, metrics that indicate valuations sitting below large-cap averages even as mid-cap earnings momentum has strengthened.

The valuation gap closing would require sustained earnings outperformance from mid-cap companies, continued macro pressure on priced-in large-cap premiums, and eventual institutional reallocation toward the segment, with the US market already signalling a similar broadening of leadership as a potential leading indicator.