Are Rate Hikes Actually Bad for Stocks? What the Data Shows

2 hrs ago

Warren Buffett once said he learned everything he needed about investing from Aesop, whose fable about a bird in hand versus two in the bush dates to roughly 600 BC. The entire discipline of value investing extends that single idea into a rigorous analytical framework: lay out money now to receive more money later, and the only questions worth asking are how much more, how certain, and how long the wait.

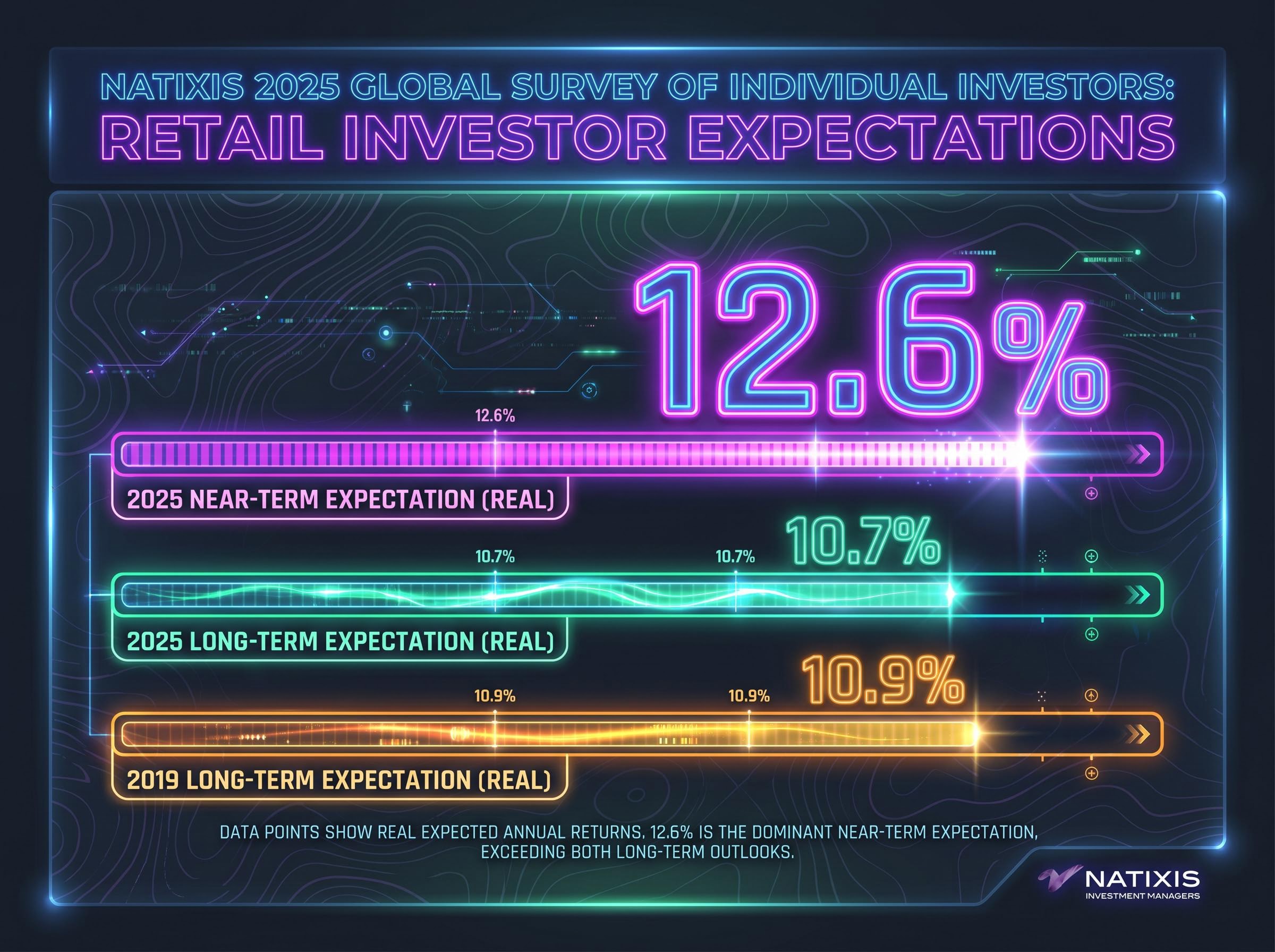

In a market environment where U.S. retail investors still expect inflation-adjusted returns of around 10.7% annually over the long run, according to the Natixis 2025 Global Survey of Individual Investors, the gap between what investors expect and what disciplined fundamental analysis would suggest is achievable from current prices is one of the most consequential questions in personal finance. Intrinsic value estimation is the tool that closes that gap with evidence rather than sentiment.

This guide walks through the two core analytical tools of value investing: estimating a stock’s intrinsic value using discounted cash flow principles, and applying a margin of safety to protect against the inevitable imprecision of any forecast. By the end, readers will understand not just the mechanics but the reasoning behind each step, and will be equipped to stress-test any valuation they build.

Intrinsic value is the discounted present value of all future cash flows a business will generate across its lifetime. That definition sounds precise. It is not.

The honest word for what investors do when they estimate intrinsic value is exactly that: estimate. Warren Buffett has described the process as more art than science, because the inputs, how much cash the business will produce, when, and at what growth rate, are matters of judgment rather than measurement. Howard Marks reinforced this framing in his August 2025 memo “The Calculus of Value,” describing intrinsic value based on earning power and fundamentals as the anchor for assessing whether price aligns with value.

When an investor cannot estimate a business’s future cash flows with any reasonable confidence, the activity crosses from investing into speculation.

What intrinsic value is:

What intrinsic value is not:

Bond valuation is largely deterministic. Coupon payments and maturity value are contractual obligations; the investor knows, barring default, exactly what cash flows to expect and when.

Equity valuation is probabilistic. The investor must project how much cash the business will generate, at what growth rate, and over what time horizon, before discounting any of those figures back to the present. Every input is a judgment call, and every judgment call introduces uncertainty.

This distinction matters because it sets the boundary for the rest of the guide. Every technique that follows is a tool for managing uncertainty, not eliminating it.

A discounted cash flow (DCF) model is not a formula to solve. It is a sequence of decisions, and every number an investor inputs is a choice with consequences rather than an objective fact waiting to be discovered.

Three primary inputs drive the model: estimated future cash flows (typically net income or free cash flow), a projected growth rate for those cash flows, and a discount rate used to convert future value back to present value. The discount rate functions as a hurdle: at a 10% discount rate, a benchmark used by practitioners including Sven Carlin, Ph.D., any investment that cannot return at least 10% annually at the current price is passed over in favour of better alternatives.

Damodaran’s DCF valuation framework establishes that terminal value calculations must use internally consistent assumptions, meaning the growth rate embedded in the terminal value cannot exceed the nominal growth rate of the broader economy without producing a logically incoherent model.

The current rate environment shapes these choices. Aswath Damodaran’s early 2026 valuation work references the 10-year U.S. Treasury yield at approximately 4.18% as the risk-free rate input, and his analysis emphasises that discount rate assumptions and growth assumptions must be internally consistent with each other and with the prevailing macroeconomic environment.

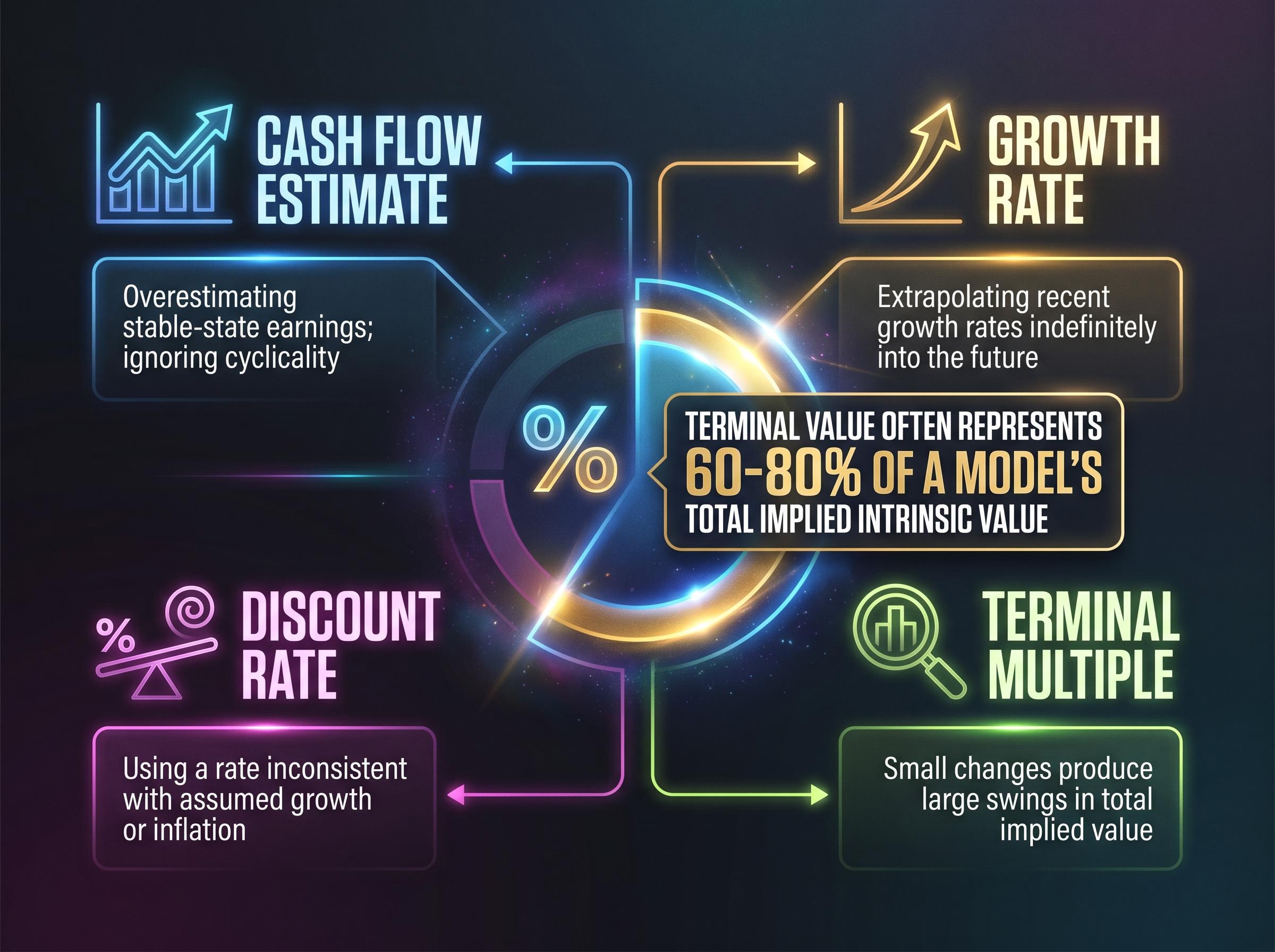

The table below summarises where each input carries the most risk of error.

| Cash Flow Estimate | Growth Rate | Discount Rate | Terminal Multiple | |

|---|---|---|---|---|

| What it represents | Annual free cash flow or net income the business generates | Projected annual increase in cash flows over the forecast horizon | Minimum acceptable return; converts future value to present value | Assumed valuation ratio applied at end of projection period |

| Where errors typically occur | Overestimating stable-state earnings; ignoring cyclicality | Extrapolating recent growth rates indefinitely into the future | Using a rate inconsistent with assumed growth or inflation | Small changes produce large swings in total implied value |

A terminal value, the estimated worth of the business at the end of the projection horizon, is typically added to the sum of discounted annual cash flows. This single figure often represents 60-80% of a model’s total implied intrinsic value.

That concentration is not a flaw. It is a signal. It tells investors exactly where their model is most sensitive and where stress-testing is most necessary. A small change to the assumed terminal multiple, say from 15x to 25x earnings, can move the implied intrinsic value by hundreds of billions of dollars for a large business. The worked example in the next section makes this concrete.

Sven Carlin, Ph.D., presented a simplified valuation model for Berkshire Hathaway referencing conditions as of early 2024. The inputs are straightforward: estimated annual net income of approximately $40 billion, a projected growth rate of 5%, and a discount rate of 10%.

The outputs diverge sharply depending on a single assumption.

| Terminal Multiple | Terminal Value | Discounted Intrinsic Value | Market Cap at Time | Implied Annual Return |

|---|---|---|---|---|

| 15x | Conservative estimate | Below $880B | ~$880 billion | ~6% |

| 25x | ~$1.5 trillion | ~$600 billion | ~$880 billion | Could nearly double over 10 years |

The same business. The same cash flows. The same discount rate. Yet one scenario suggests modest 6% annual returns while the other suggests the investment could nearly double over a decade. The entire gap comes from a single terminal multiple assumption.

Berkshire’s approximately $150 billion cash holding adds a further layer. That figure can be treated as a tangible asset component in margin-of-safety calculations, reducing the effective downside even under the more conservative scenario.

The question is not what Berkshire earns today. Returning to Aesop’s framework, the question is how many birds are in the bush, and at what discount rate they are worth having.

This is the practical tension at the heart of every DCF model. The imprecision is not a limitation to work around. It is a discipline to embrace, and it is precisely why margin-of-safety thinking exists.

Building a model is the optimistic part. Doubting it is the discipline.

A margin of safety is the practice of purchasing assets at prices meaningfully below estimated intrinsic value, specifically to absorb forecasting errors, bad luck, and unexpected adverse events. No model is reliable enough to act on without a buffer, because every input, from the growth rate to the terminal multiple, carries irreducible uncertainty.

Practitioner threshold Seth Klarman, author of Margin of Safety, targets a minimum yield of approximately 15% annually when evaluating potential investments, with the expectation the business may not immediately achieve that return but should reach it within a few years.

Howard Marks’ 2025 commentary reinforces the principle: margins of safety should be built into valuations based on intrinsic value estimates, with the buffer proportional to the uncertainty in the underlying projection. The wider the uncertainty, the wider the discount demanded before committing capital.

Genuine margin-of-safety opportunities are uncommon. Markets are reasonably efficient much of the time, which means wide discounts to intrinsic value tend to appear only under specific conditions:

Identifying undervalued stocks in practice combines DCF-derived intrinsic value estimates with screening metrics that filter for candidates worth modelling in the first place, with free cash flow yield, price-to-earnings ratios, and debt-to-equity constraints working together to surface businesses whose market prices diverge from fundamental worth.

A margin of safety calculated under benign assumptions may dissolve under adverse macro conditions, which is why stress-testing is part of margin-of-safety analysis, not separate from it. The margin of safety converts an estimate into a decision rule, and preserving capital through that rule is the prerequisite for compounding.

A valuation that survives only the base case is a hope, not a conviction. Stress-testing is the process of deliberately challenging each assumption to see whether the margin of safety holds under adversity.

The following four steps can be applied to any DCF model:

Aswath Damodaran’s principle from his 2025 and 2026 data updates provides an important filter before these rate-sensitivity tests: rising interest rates have neutral effects on intrinsic value for businesses with pricing power but negative effects for those without it.

The Berkshire example illustrates this interaction. The $150 billion cash holding functions as a stress-test buffer that reduces downside under adverse macro scenarios, demonstrating how balance sheet strength interacts with DCF-derived estimates.

The Natixis 2025 data point adds context: U.S. retail investors expecting 10.7% real long-term returns are implicitly assuming growth and multiple conditions in their mental models. Stress-testing makes those hidden assumptions explicit.

The Natixis 2025 Global Survey of Individual Investors documents that U.S. retail investors expected inflation-adjusted long-term returns of 10.7% annually, a figure that has remained remarkably stable since the 10.9% reading recorded in 2019 and one that most DCF-based frameworks would struggle to justify from current market valuations.

Before running interest-rate stress tests, evaluate whether the business can raise prices to offset rising input costs and maintain real cash flow growth.

If the answer is yes, the DCF model’s intrinsic value estimate is relatively resilient to rate increases, because higher revenues offset the impact of a higher discount rate. If the answer is no, the discount rate sensitivity is severe, and the margin of safety must be correspondingly wider. Pricing power is not a bonus. It is the first filter.

The Natixis 2025 Global Survey of Individual Investors quantifies a gap that intrinsic value analysis is designed to address.

| Survey Year | Near-Term Expectation (real) | Long-Term Expectation (real) |

|---|---|---|

| 2019 | Not separately reported | 10.9% |

| 2025 | 12.6% | 10.7% |

These figures remain substantially above what most DCF-based intrinsic value frameworks would consider achievable over long horizons from current market valuations. The persistence of these expectations, 10.9% in 2019 and 10.7% in 2025, suggests this is not a temporary post-pandemic distortion but a durable calibration problem.

The connection to margin-of-safety thinking is direct. When investors expect 10-17% annual real returns, they are implicitly assuming either high cash flow growth, expanding valuation multiples, or both. A margin-of-safety framework forces those assumptions into the open where they can be evaluated and stress-tested.

The price paid relative to intrinsic value, not the quality of the underlying business, is the single most consequential variable in long-term investment returns; Howard Marks’ analysis of the Nifty Fifty collapse illustrates how investors in world-class companies including Coca-Cola and IBM lost approximately 90% of portfolio value between 1968 and 1973 by ignoring this distinction.

Buffett’s 10% discount rate as a hurdle provides a useful reference. At prices where the market is already pricing in more than 10% annual returns, the investor is buying something the market considers fairly or generously valued. That is exactly when margin-of-safety discipline is most necessary.

Intrinsic value estimation forces investors to make their assumptions explicit. Explicit assumptions can be stress-tested. Implicit ones cannot.

Intrinsic value estimation and margin of safety are not techniques reserved for professional analysts. They are tools for any investor who wants to replace market sentiment with a personal, reasoned estimate of what a business is worth.

The framework reduces to two steps. Intrinsic value estimation converts a business’s expected future cash flows into a present-value figure. Margin of safety converts that estimate into a purchase discipline by demanding a discount before committing capital.

No model produces a precise intrinsic value. The practitioner’s judgment about growth rates, terminal multiples, and discount rates introduces irreducible uncertainty. The goal is not precision but a range of defensible estimates, tested under both base-case and adverse assumptions, that provide a rational basis for action.

Investors who want to apply these tools should begin with businesses whose cash flows are relatively predictable: mature, stable businesses with pricing power. Build the DCF model under base and adverse assumptions. Identify the discount to intrinsic value required to meet the chosen hurdle rate. Then wait for the market to offer it.

Related guides on DCF model construction, free cash flow analysis, and how to evaluate competitive moats each build directly on the skills covered here, and strengthening any one of them improves the quality of every intrinsic value estimate that follows.

For readers wanting to build a cross-check into every intrinsic value estimate they produce, our dedicated guide to combining valuation methods walks through a structured five-step sequence using P/S screening, EV/EBITDA benchmarks, DCF analysis, and DDM cross-checks, showing how each method reveals blind spots that the others cannot detect on their own.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Intrinsic value is the discounted present value of all future cash flows a business is expected to generate across its lifetime. It is an estimate based on judgment about growth rates, cash flows, and discount rates, not a precise calculation.

A DCF model projects a company's future free cash flows, applies a growth rate over a forecast horizon, then discounts those future values back to today using a required rate of return, typically around 10%, to arrive at a present-value estimate of the business.

A margin of safety means buying a stock at a price meaningfully below your estimated intrinsic value, creating a buffer that absorbs forecasting errors, unexpected bad news, and model imprecision before your capital is at risk.

The terminal value, which represents the estimated worth of the business at the end of the projection period, typically accounts for 60-80% of a DCF model's total implied intrinsic value, meaning small changes to the assumed terminal multiple can shift the result by hundreds of billions of dollars.

Investors can stress-test by raising the discount rate by 2 percentage points, cutting the growth rate assumption in half, lowering the terminal multiple to a historical trough level, and then checking whether the margin of safety survives all three scenarios simultaneously.