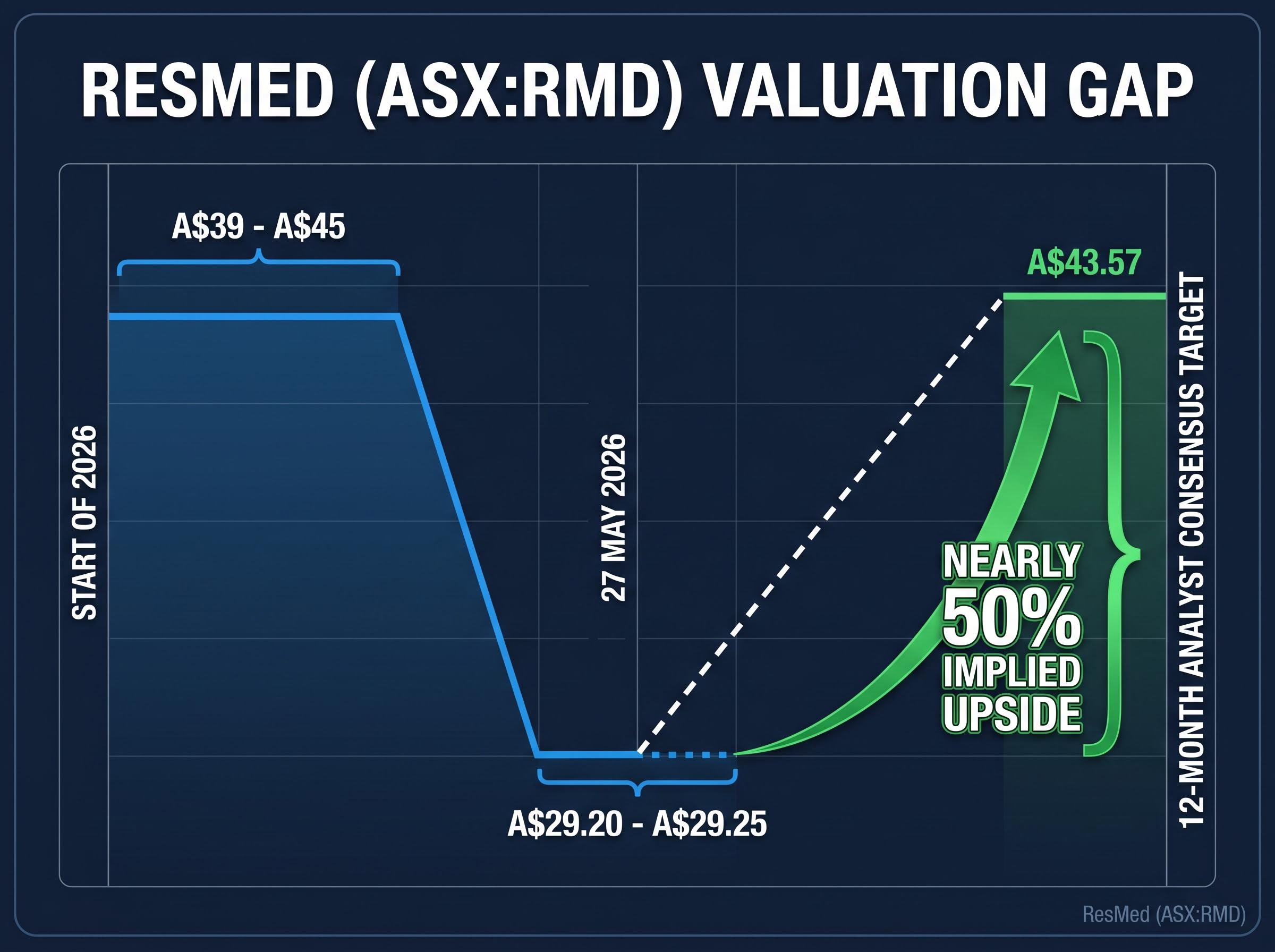

ResMed (ASX:RMD) has fallen roughly 19% since the start of 2026, dropping from near A$39-A$45 to approximately A$29.20-A$29.25 as of 27 May 2026. The decline has been sharp, sustained, and dominated by a single narrative: the threat that GLP-1 weight-loss drugs pose to long-term CPAP demand. Yet analyst consensus points to a 12-month price target of approximately A$43.57, implying nearly 50% upside from current levels. The gap between what the market is pricing and what professional analysts are projecting is unusually wide for a company of ResMed’s scale and profitability.

For Australian investors watching this through an ASX CDI lens, the question is whether the share price reflects a business in genuine decline or a sentiment-driven re-rating that has overshot the fundamentals. What follows works through ResMed’s financial performance, balance sheet, valuation relative to its own history, and the competitive threat in structured layers, providing a framework for forming a grounded view rather than reacting to price momentum.

What is driving ResMed’s 19% fall in 2026

The most concrete catalyst arrived in June 2025, when Australia’s Therapeutic Goods Administration (TGA) approved Eli Lilly’s Mounjaro (tirzepatide) for moderate-to-severe obstructive sleep apnoea (OSA) in adults with obesity. That approval extended GLP-1 drug indications directly into ResMed’s core clinical territory for the first time.

Key regulatory milestone: The TGA’s June 2025 approval of tirzepatide for OSA marked the first time a GLP-1 drug received regulatory endorsement specifically for treating sleep apnoea in Australia, as reported by the Australian Financial Review on 4 June 2025.

The TGA’s Mounjaro product registration confirms that tirzepatide is indicated for the treatment of moderate to severe obstructive sleep apnoea in adults with obesity, establishing the regulatory basis for the displacement thesis that has weighed on ResMed’s share price since mid-2025.

The 2026 price weakness did not emerge from that single event. It built on a multi-year GLP-1 overhang that began in 2023, making the current decline an accumulated re-rating rather than a sudden shock. Three interlocking forces have compressed the share price:

- GLP-1 demand overhang: persistent investor concern that weight-loss drugs will permanently reduce sleep apnoea prevalence and long-term CPAP device demand

- Multiple compression: investors reassessing the premium historically priced into high-multiple healthcare growth names, including ResMed

- Margin and operating expenditure anxiety: periodic concern about gross margin sustainability and cost growth, amplified by broader risk-off sentiment in the healthcare sector

The year-to-date decline of approximately 18.83% reflects all three forces compounding, not any single earnings miss or operational failure.

ASX healthcare valuation compression over the past five years has been driven primarily by interest rate-driven multiple contraction rather than deteriorating business fundamentals, a pattern that helps explain why companies like ResMed can simultaneously report double-digit revenue growth and a declining share price.

When big ASX news breaks, our subscribers know first

How ResMed actually makes its money (and why that structure matters here)

Before assessing ResMed’s financial resilience, it is worth understanding what the business actually does and how its revenue divides.

ResMed operates two core divisions. The first, Sleep and Respiratory Care, manufactures CPAP devices, masks, and accessories for patients with sleep-disordered breathing. The second, its Software-as-a-Service (SaaS) segment, provides cloud-based clinical and operational software for out-of-hospital care providers. SaaS revenue is recurring by nature, structurally distinct from the one-off economics of device sales.

What connects the two is data. ResMed’s hardware integrates with its connected-care platform to generate clinical information on patient compliance and therapy outcomes. That data loop creates retention and switching costs that pure device sales metrics do not capture. A competitor can sell a CPAP machine; replicating the integrated clinical ecosystem is a different proposition.

| Division | Revenue driver | Key products / platforms | GLP-1 exposure level |

|---|---|---|---|

| Sleep and Respiratory Care | Device and mask sales | AirSense CPAP devices, masks, accessories | Higher (device demand linked to OSA prevalence) |

| SaaS / Digital Health | Recurring software subscriptions | Brightree, connected-care platform | Lower (software revenue less tied to new device volumes) |

Australian investors should also note the listing structure. ASX:RMD trades as CHESS Depositary Interests (CDIs) in AUD, but the underlying business, founded in Adelaide by Peter Farrell and now headquartered in San Diego, reports all financials in USD. Currency movements between the Australian and US dollars add a layer of complexity when interpreting share price moves against reported earnings. ResMed employs over 10,000 people across operations in more than 140 countries.

AUD/USD currency exposure adds an independent return variable for ASX CDI holders that NYSE investors do not face: a strengthening Australian dollar reduces the translated value of ResMed’s US-dollar earnings in local portfolio terms, meaning the total return outcome for Australian investors depends on both the business performance and the exchange rate trajectory.

Revenue growth, profit expansion, and margin trends: what the numbers show

The financial data tells a story that sits in direct tension with the share price trajectory.

- Revenue growth has been consistent. ResMed’s three-year revenue compound annual growth rate (CAGR) stands at 13.6% per annum. Full-year FY25 revenue reached US$5.146 billion, up 9.84% year-on-year. Top-line growth has not deteriorated during the period of the share price decline.

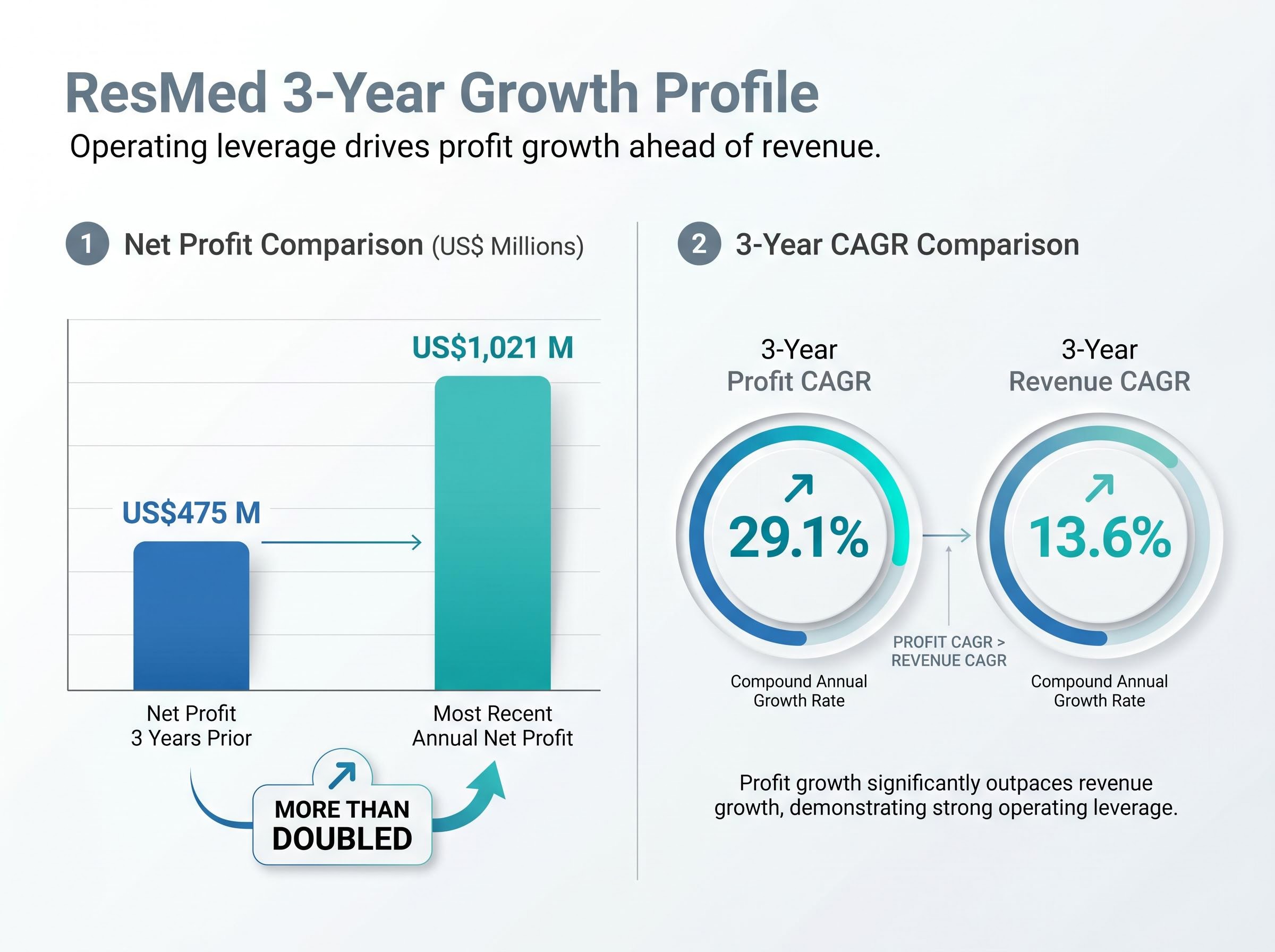

- Profit growth has outpaced revenue growth significantly. Net profit three years prior stood at US$475 million. The most recently reported annual net profit reached US$1,021 million. That represents a three-year profit CAGR of 29.1%, more than double the revenue growth rate, indicating meaningful operating leverage.

Three-year profit CAGR: 29.1%. ResMed has more than doubled its annual net profit over the same period that its share price has come under sustained pressure from GLP-1 sentiment.

- Gross margins have expanded, not contracted. The most recently reported annual gross margin was 57.4%. The most recent quarterly result showed further expansion to 62.2%, a trajectory that runs counter to the margin-compression narrative.

Most recent quarterly snapshot (Q3 FY26)

The quarter ended 31 March 2026 provides the most current data point. ResMed reported revenue of US$1.431 billion, up 11% year-on-year (or 8% on a constant-currency basis). Net income came in at US$398.7 million, with diluted earnings per share of US$2.74. Gross margin expanded year-on-year to 62.2%.

ResMed’s non-GAAP earnings trajectory tells a sharper story than GAAP net income alone: non-GAAP diluted EPS rose 21% in Q3 FY26 to US$2.86, a figure that strips out acquisition-related amortisation and reflects the underlying cash generation capacity of the business more directly than headline profit.

All results are reported in USD. ResMed’s fiscal year ends 30 June, so Q3 FY26 covers the January to March 2026 period.

The question these numbers raise is specific: when a stock falls nearly 19% while the underlying business continues to grow revenue at double-digit rates and more than doubles net profit over three years, the analytical focus shifts from whether the business is struggling to whether the market is pricing in a future deterioration that has not yet appeared in any reported metric.

Balance sheet health and what it signals about financial risk

Growth metrics capture one dimension. The balance sheet captures another: resilience.

- Net debt: negative A$624 million. In plain terms, ResMed holds more cash than total debt. The company could repay all its borrowings and still retain a cash surplus, providing a financial buffer against downside scenarios.

- Debt-to-equity ratio: 18.0%. For a company of ResMed’s scale and maturity, this is a conservative capital structure. Low leverage reduces financial risk during periods of revenue uncertainty.

- Return on equity (FY24): 22.7%. ROE measures how efficiently a company converts shareholder equity into profit. A reading of 22.7% suggests management is allocating capital productively rather than allowing returns to dilute as the business scales.

Return on equity: 22.7%. This figure indicates ResMed is generating strong returns on the capital shareholders have invested, a signal of efficient management rather than a business relying on leverage for growth.

Management has reaffirmed a five-year outlook of high single-digit revenue growth, with earnings growth targeted above revenue growth. The effective tax rate for FY26 is guided at 21-23%.

A declining share price can reflect genuine business distress or a shift in market sentiment. A net cash position, low leverage, and strong return on equity suggest ResMed’s current situation falls into the latter category, which matters when assessing whether the valuation represents risk or opportunity.

The GLP-1 question: structural threat or sentiment overhang?

The GLP-1 debate is the central valuation question for ResMed in 2026, and both sides carry verifiable weight.

The valuation discount is already significant. ResMed’s current price-to-sales ratio of 4.30x sits approximately 51% below its five-year historical average of 8.70x.

| Argument | Supporting evidence | Key uncertainty |

|---|---|---|

| Bear case: GLP-1 drugs reduce CPAP addressable market | TGA approved tirzepatide for OSA in June 2025; clinical trials show weight loss reduces OSA severity in obese patients | Pace and scale of real-world GLP-1 adoption; long-term patient adherence rates remain unproven at population level |

| Bull case: Market has overpriced the threat | Sleep apnoea has non-obesity causes; CPAP market remains structurally underpenetrated globally; demographic ageing sustains demand; ResMed’s SaaS segment provides diversification | Degree of overlap between obesity-linked OSA and non-obesity OSA in ResMed’s actual addressable market |

The bear case is straightforward. If GLP-1 drugs reduce obesity-linked OSA prevalence at scale, the addressable market for CPAP devices contracts over time. The TGA’s June 2025 tirzepatide approval for OSA was a concrete regulatory step in that direction, not a hypothetical.

The constructive counter-case rests on several pillars. Sleep apnoea has causes beyond obesity, including craniofacial structure, ageing, and neurological factors. GLP-1 drug compliance and long-term adherence remain uncertain; early data on weight regain after discontinuation complicates the displacement thesis. The global CPAP market remains significantly underpenetrated, with millions of patients undiagnosed or untreated.

Management’s strategic diversification has extended beyond organic product development, with the US$340 million acquisition of Noctrix Health broadening ResMed’s addressable market into restless leg syndrome treatment, a therapeutic area that carries no GLP-1 exposure and represents a direct structural hedge against the OSA demand overhang.

Analyst consensus, spanning approximately 15-19 analysts covering NYSE:RMD, remains predominantly Buy or Outperform. The average 12-month price target sits at approximately US$270-286 (equivalent to roughly A$43.57 on ASX), with a range from US$180-225 at the low end to US$340-345 at the high end. The breadth of that range reflects genuine disagreement about the GLP-1 impact, but the consensus centre of gravity leans constructive.

Whether the current 51% discount to historical price-to-sales is appropriate or excessive is what separates the two camps.

A 19% decline, strong financials, and a 51% valuation discount: what investors need to decide

The data presented across this analysis produces a specific tension. ResMed is growing revenue at double-digit rates, has more than doubled net profit over three years (a CAGR of 29.1%), holds net cash, and trades at a 4.30x price-to-sales ratio against a five-year average of 8.70x. The analyst consensus target of approximately A$43.57 implies roughly 50% upside from the current price near A$29.20-A$29.25.

Yet the share price implies that future deterioration is already baked in. The market is making a forward-looking bet that GLP-1 adoption will erode the business in ways that have not yet appeared in reported earnings.

An investor forming a view on ASX:RMD at this level would need to answer several specific questions:

- How quickly and broadly will GLP-1 drugs achieve real-world adoption for OSA, and what does long-term patient adherence look like?

- What proportion of ResMed’s addressable market is obesity-linked OSA versus non-obesity OSA, and how exposed is the revenue base to the former?

- Does the SaaS and digital health segment provide genuine insulation from CPAP device volume declines, or does it depend on the device installed base for growth?

- Is a single-metric valuation comparison (price-to-sales) sufficient, or would a discounted cash flow (DCF) or dividend discount model (DDM) analysis produce a materially different picture?

These questions do not have consensus answers. They are the questions that determine whether the current price is a discount or a fair re-rating.

ResMed in 2026: the gap between price and fundamentals is the question, not the answer

The share price decline in 2026 reflects a market pricing in disruption that has not yet materialised in ResMed’s financial results. Revenue is growing. Margins are expanding. The balance sheet carries net cash. Analyst consensus remains overwhelmingly constructive. None of this means the GLP-1 threat is irrelevant; it means the investment debate is about the pace and scale of a potential future impact, not about current business deterioration.

The financial and valuation data presented here is a starting point, not a conclusion. Investors considering a position in ASX:RMD would benefit from extending this analysis using multiple valuation methodologies, including DCF and DDM frameworks, and monitoring real-world GLP-1 adherence data as it emerges over the coming quarters.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.