The Australian Prudential Regulation Authority (APRA) oversees institutions holding approximately $9.8 trillion in assets on behalf of depositors, policyholders, and superannuation members. Its latest assessment, published 21 May 2026, says those institutions can absorb severe shocks. The stress test results are reassuring. The regulator’s tone on what lies beyond Australia’s borders is notably less settled.

APRA’s semi-annual System Risk Outlook lands during a period of elevated geopolitical volatility, accelerating artificial intelligence adoption across financial services, and a global private credit market that has expanded well beyond what regulators had fully mapped a decade ago. This analysis unpacks what APRA’s stress test findings mean in practical terms, traces how geopolitical shocks travel from overseas conflict zones into Australian bank funding costs, and examines why a private credit market that remains modest domestically can still carry serious external risk for Australian institutions.

Australia’s banks and insurers just passed a serious stress test. Here is what that means.

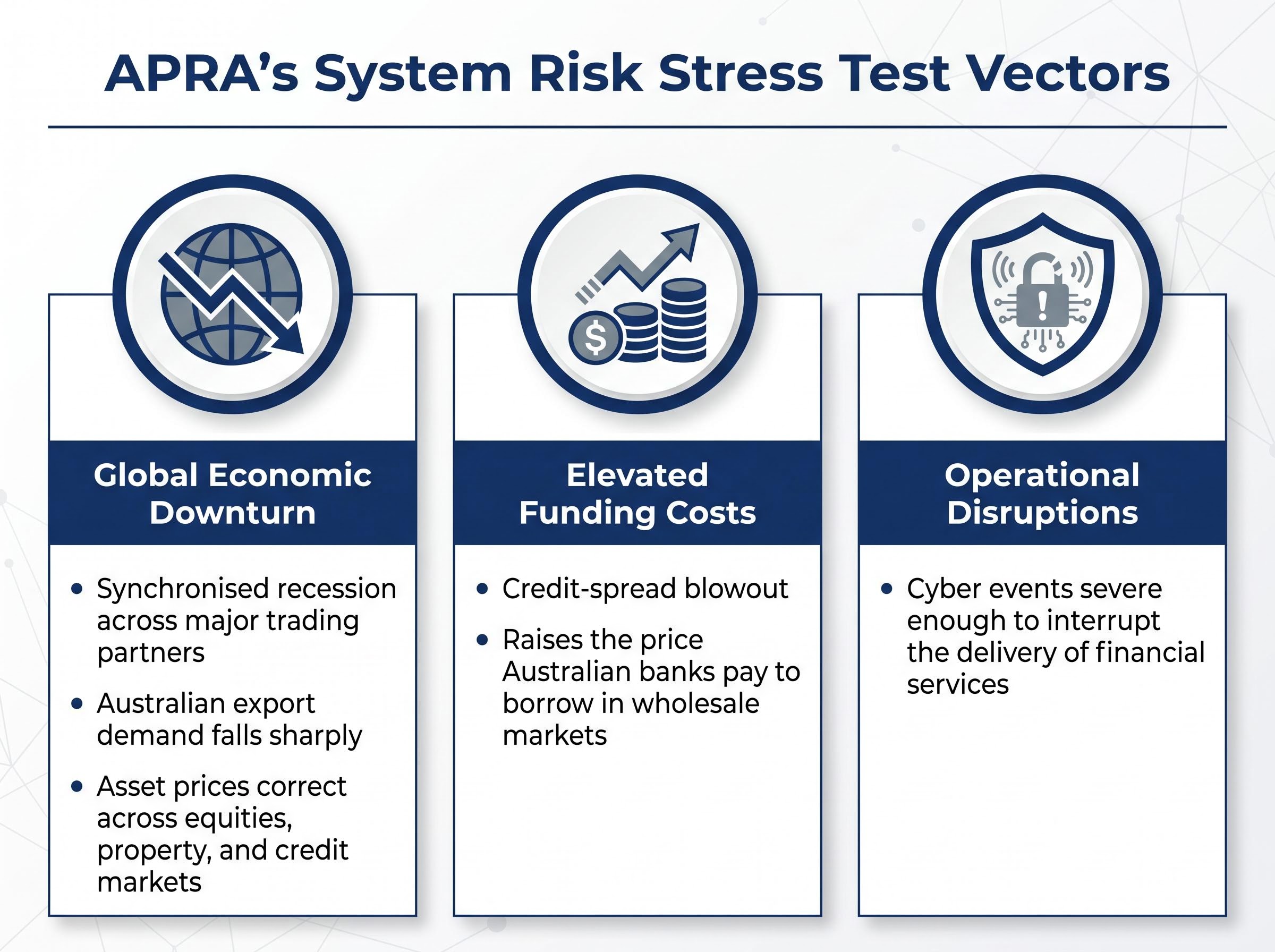

APRA designed its system risk stress test around scenarios it describes as “severe but plausible,” a regulatory term of art meaning the modelled conditions are harsh enough to be meaningful but grounded in events that could realistically occur. The scenarios were not abstract. They were built around three concrete stress vectors:

- A significant global economic downturn, analogous to a synchronised recession across major trading partners

- Elevated funding costs, reflecting a credit-spread blowout that raises the price Australian banks pay to borrow in wholesale markets

- Operational disruptions, including cyber events severe enough to interrupt the delivery of financial services

These three components test different parts of an institution’s balance sheet simultaneously, which is the point. A single-variable shock is survivable by design; the question regulators need answered is whether institutions hold up when multiple pressures arrive at once.

What the stress scenarios actually modelled

The global downturn component captures a world in which Australian export demand falls sharply and asset prices correct across equities, property, and credit markets. The funding cost component maps to a scenario where risk aversion drives investors away from bank-issued debt, forcing institutions to pay materially more to roll over wholesale borrowings. The operational disruption component reflects cyber incidents capable of impairing core banking or insurance platforms for extended periods.

What “passing” the test does and does not guarantee

Both the banking and insurance sectors were assessed as maintaining strong capital positions and solid liquidity buffers under these conditions. APRA Chair John Lonsdale framed the result in terms of continuity rather than invulnerability:

The system remains “well-placed to continue delivering critical services” to Australians.

That language is precise. “Well-placed to continue delivering critical services” is not the same as “unaffected.” It means the system can absorb the modelled shocks and keep operating, not that it would operate without friction, elevated costs, or periods of market stress. Phase 1 results were published in the November 2025 Outlook; the Phase 2 final report is due mid-2026, and those results will materially update the picture.

When big ASX news breaks, our subscribers know first

How geopolitical shocks reach Australian bank balance sheets

A conflict in the Middle East or a trade dispute between the United States and China can feel abstract from an Australian investor’s perspective. The transmission channels, however, are concrete and documented. Geopolitical disruption reaches Australian financial institutions through three primary mechanisms: commodity demand and terms of trade, risk-off episodes in global markets, and wholesale funding spread widening.

Each of these channels has been active over the past 18 months. US-China tensions operate through lower demand for Australian commodity exports, weaker terms of trade, and risk-off episodes that raise the cost of capital for Australian issuers. Middle East tensions have contributed to higher energy price volatility and bouts of risk aversion that repriced risk assets and widened funding spreads, as documented in the Reserve Bank of Australia’s (RBA) Financial Stability Review of October 2025.

The RBA Financial Stability Review October 2025 dedicated a focus topic to the specific channels through which overseas shocks transmit into Australian financial conditions, providing granular detail on how commodity demand shifts, risk-off episodes, and wholesale funding spread widening interact to raise costs for Australian banks and other regulated institutions.

The RBA’s Financial Stability Review of March 2026 continued to identify geopolitical risks as a primary channel for transmission to Australian financial conditions, including funding spreads. These are not theoretical warnings. The market is already pricing in elevated geopolitical risk.

ASX interest rate derivatives trading volumes in Q1 2026 rose 23% versus Q4 2025 and 32% versus Q1 2025, a surge the ASX explicitly linked to heightened macroeconomic and geopolitical volatility.

That hedging activity is evidence of institutions paying real money to protect against outcomes they consider plausible, not merely possible.

| Risk Source | Transmission Channel | Australian Market Impact | Key Evidence |

|---|---|---|---|

| Middle East conflict | Energy price volatility and risk aversion | Risk-asset repricing, wider funding spreads | RBA FSR October 2025 |

| US-China tensions | Lower commodity demand, weaker terms of trade, risk-off episodes | Higher bank funding costs, credit spread widening | RBA FSR series 2025-2026 |

For retail investors holding bank shares or fixed-income products, the implication is direct: geopolitical risk is not a separate category from credit risk and funding risk. They are connected through channels that both APRA and the RBA have now explicitly named.

Understanding private credit: why a small domestic market carries an outsized external risk

Private credit refers to loans made directly to companies outside public markets, typically to mid-market businesses that do not issue listed bonds or equities. These loans are originated by non-bank lenders, specialist credit funds, or alternative asset managers, and they sit on balance sheets where secondary liquidity is limited. If a lender wants to exit a private credit position, there is no exchange to sell it on. This illiquidity is the defining structural feature of the asset class.

The private credit liquidity mismatch sits at the structural core of why offshore exposures are difficult to unwind quickly; when stress events force funds to meet redemptions, the absence of a secondary market for the underlying loans can push managers to liquidate public equities instead, transmitting losses into portfolios that carry no direct private credit allocation.

Australia’s domestic private credit market remains modest relative to the banking system, as the RBA’s Financial Stability Review of March 2024 noted, while also observing that non-bank lenders and private credit funds are increasing their share of business lending. The Australian Financial Markets Association’s 2025 Annual Report confirmed continued growth in non-bank lending and private credit as alternative financing channels. The domestic market, in isolation, does not pose a systemic threat.

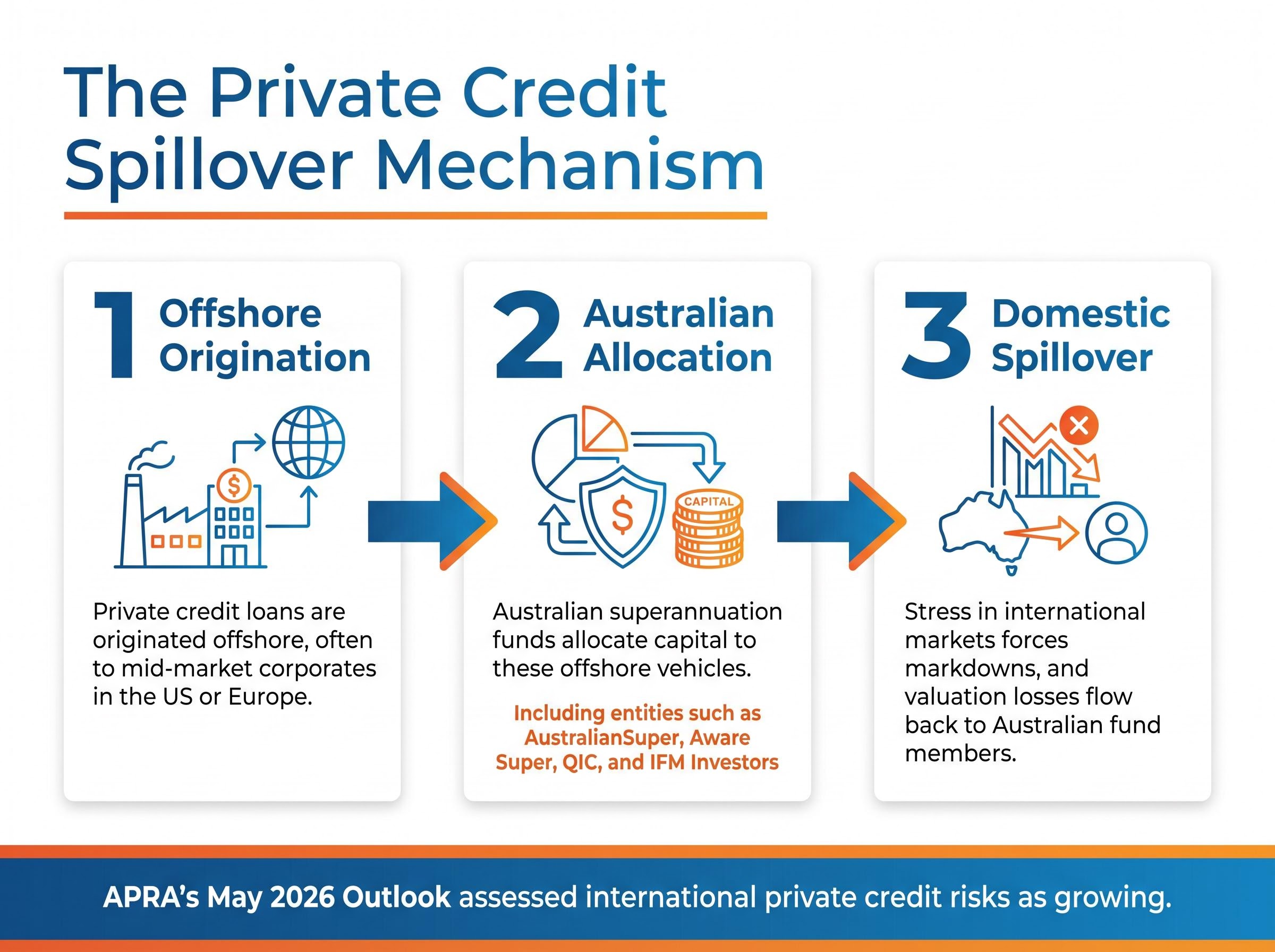

The risk enters through the back door. Large Australian superannuation funds and asset managers, including entities such as AustralianSuper, Aware Super, QIC, and IFM Investors, hold private debt allocations within their alternatives portfolios. Those allocations include exposure to offshore private credit vehicles.

The spillover mechanism works in three steps:

- Private credit loans are originated offshore, often to mid-market corporates in the US or Europe, by international fund managers

- Australian superannuation funds allocate capital to these offshore vehicles as part of their alternatives or private debt strategies

- If stress in international private credit markets forces markdowns, the valuation losses flow back to Australian fund members through their alternatives allocation

APRA’s May 2026 Outlook assessed international private credit risks as growing and warranting close, ongoing regulatory monitoring.

The offshore private credit transmission channels connecting global mid-market stress to Australian superannuation fund valuations involve multiple intermediary steps, and quantifying the exposure requires understanding both the scale of the international market (approximately US$2.3 trillion) and the specific allocation patterns of major Australian funds, including AustralianSuper and IFM Investors, at a point in the credit cycle where defaults are beginning to surface.

Why transparency is the central problem

Unlike listed bonds or equities, private credit positions are valued using models rather than market prices. Valuations are updated periodically, not continuously. This means losses can accumulate before they become visible in reported fund returns. By the time a valuation adjustment appears, the underlying credit deterioration may have been building for months. For superannuation members, understanding that their fund’s alternatives allocation may carry indirect offshore private credit exposure is material to assessing how their retirement savings are positioned against an opaque and growing international risk.

An academic survey of private credit systemic risks published in early 2026 identified structural illiquidity, valuation opacity, and cross-border interconnection as the three features most likely to amplify stress in offshore private credit markets, each of which maps directly onto the exposure pathway that Australian superannuation funds carry through their alternatives allocations.

AI governance gaps: the risk APRA is most worried about internally

Artificial intelligence adoption across APRA-regulated sectors is not a future consideration. It is already happening across banking, insurance, and superannuation, and APRA’s May 2026 Outlook makes clear that internal governance frameworks have not kept pace.

APRA has escalated beyond routine supervisory commentary. Prior to the May 2026 report, the regulator issued a formal letter to industry on AI governance, a step that signals supervisory urgency rather than advisory interest. Formal correspondence of this kind carries implicit expectations that boards and senior management will respond with demonstrable action, not just acknowledgement.

APRA’s 30 April supervisory letter set the regulatory stage for the May 2026 Outlook findings, formally declaring that AI risk management controls across banks, insurers, and superannuation trustees were materially inadequate under existing prudential standards and placing board-level accountability for those gaps on the record before any new rules were introduced.

Governance and oversight arrangements within regulated entities “have not evolved at a rate consistent with the speed of AI deployment,” according to APRA’s May 2026 System Risk Outlook.

The risk operates on two fronts:

- Internal governance gaps: Institutions deploying AI models for credit decisioning, claims processing, or customer interactions without governance frameworks mature enough to manage model risk, bias, and accountability

- External AI-enhanced cyber threats: Advanced AI models are contributing to an increasingly sophisticated threat environment, making cyber attacks harder to detect and more damaging when they succeed

For investors in financial institutions, this is a category of operational risk that capital buffer stress tests do not capture. A bank can hold surplus capital and still suffer material reputational and operational damage from a poorly governed AI system that produces biased lending decisions or fails to detect a sophisticated intrusion. AI governance quality is becoming a material factor in assessing operational resilience.

The next major ASX story will hit our subscribers first

What APRA’s heightened supervisory posture signals for regulated institutions

APRA’s May 2026 Outlook describes not just what the regulator sees, but what it intends to do about it. The language throughout the report points to a deliberate escalation in supervisory intensity, distinct from the regulator’s standard ongoing monitoring activities.

In practice, this means sharper expectations around sound risk management practices, active monitoring of geopolitical preparedness across regulated entities, and formal AI governance correspondence that carries supervisory weight. APRA has sharpened its expectations rather than simply restating them.

The breadth of APRA’s remit amplifies the significance of this escalation. The regulator covers banks, mutual institutions, general and reinsurance providers, life insurers, private health insurers, friendly societies, and the majority of the superannuation sector. When APRA raises supervisory intensity, the signal reaches across the full financial services sector, not just the four major banks.

| Supervisory Action | Risk Category Targeted | Entities Covered |

|---|---|---|

| Sharpened risk management expectations | Geopolitical, macroeconomic | All APRA-regulated entities |

| Formal AI governance letter to industry | Operational, technology | All APRA-regulated sectors |

| Phase 2 system risk stress test (due mid-2026) | Capital adequacy, systemic resilience | Major banks, large super funds |

| Ongoing private credit monitoring | Credit, liquidity, transparency | Super funds, asset managers |

Phase 2 of the system risk stress test is due for its final report mid-2026, and the next System Risk Outlook edition is expected toward the end of 2026. The stress-testing programme is still deepening, not concluding. For investors assessing the stability of Australian banks and super funds, APRA’s escalating posture is itself a signal worth interpreting: more intensive oversight can reduce tail risk over time, but it also signals that regulators see enough uncertainty to justify the effort.

Resilient, but not insulated: the honest read on Australia’s financial system in mid-2026

APRA’s May 2026 assessment holds two truths in tension. The domestic fundamentals are strong: capital buffers are substantial, liquidity positions are solid, and the system passed a rigorous multi-variable stress test. At the same time, the principal vulnerabilities are almost entirely imported, arriving through geopolitical transmission channels that are active and documented, an offshore private credit market that is growing and opaque, and AI governance gaps that are widening in real time.

The four risk themes covered in this analysis break down as follows:

ASX equity risk premium compression toward near-zero levels means the valuation cushion that would ordinarily absorb earnings disappointments in a rising-rate environment is largely absent, a condition that makes the funding spread widening APRA has documented in its stress scenarios more consequential for bank shareholders than the headline capital adequacy numbers alone would suggest.

- Stress test resilience: Banking and insurance sectors demonstrated the capacity to absorb severe but plausible shocks, though Phase 2 results remain pending

- Geopolitical transmission: Middle East conflict and US-China tensions are actively flowing into Australian funding costs, hedging demand, and risk premia through well-documented channels

- Private credit spillover: Australia’s domestic market is small, but superannuation fund exposure to offshore private credit vehicles creates a transparency and liquidity risk that regulators are monitoring closely

- AI governance: Adoption has outpaced governance across all APRA-regulated sectors, prompting formal regulatory escalation

The $9.8 trillion in APRA-overseen assets sits behind buffers that are real and tested. The risks that could erode those buffers are also real, and APRA’s ongoing monitoring of geopolitical preparedness reflects an active rather than passive response. Phase 2 stress test results, expected mid-2026, and the next System Risk Outlook, expected toward the end of 2026, will materially update this picture.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. APRA’s assessments represent point-in-time regulatory evaluations, and forward-looking statements regarding stress test outcomes and supervisory actions are subject to change based on evolving market conditions.