WTI Jumps 1.6% as Iran Strikes Shatter Hormuz Deal Hopes

7 hrs ago

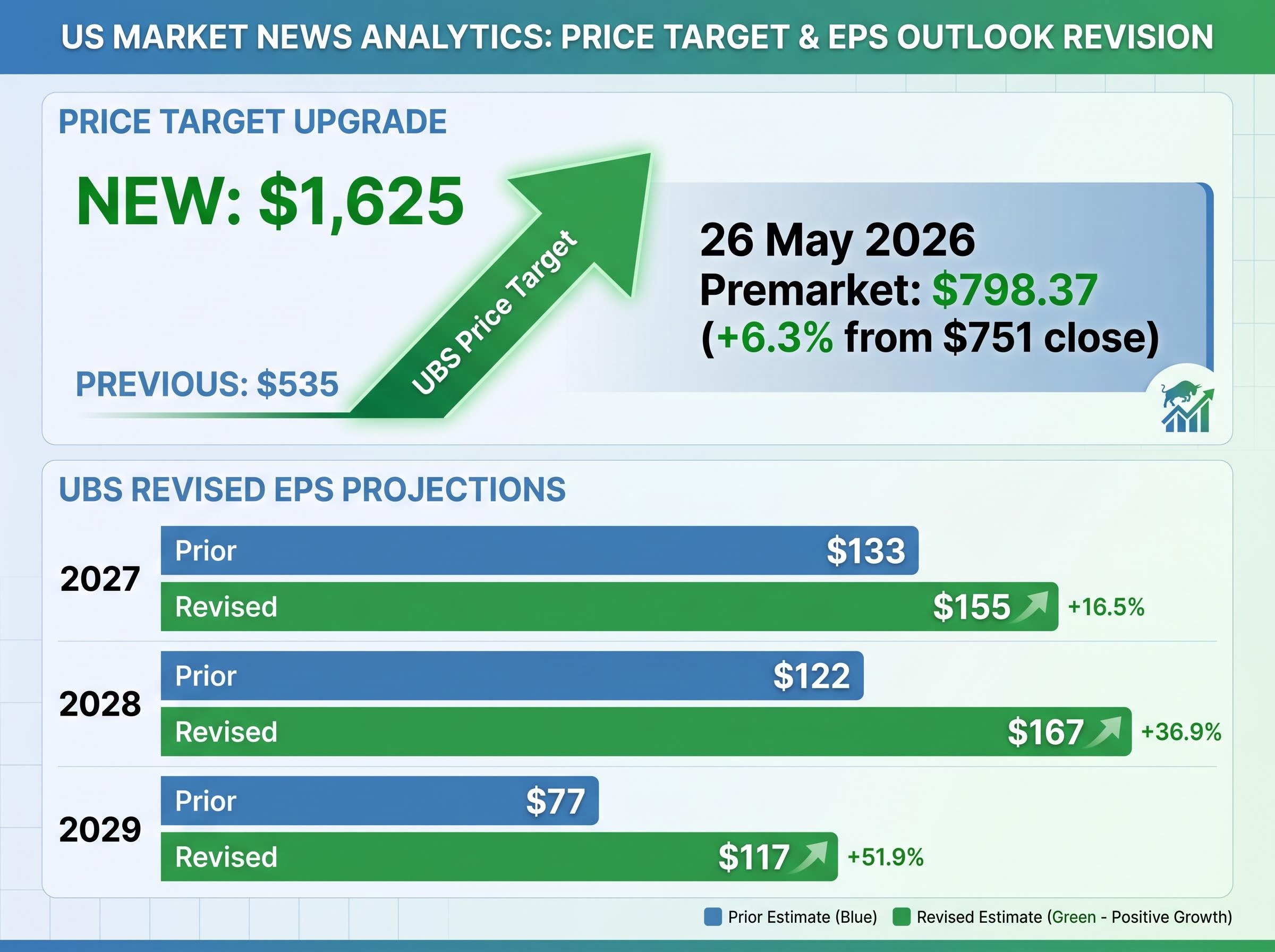

Micron Technology shares surged 6.3% in premarket trading on 26 May 2026 after UBS more than tripled its price target on the stock overnight, lifting it from $535 to $1,625. The revision, attributed to UBS analyst Timothy Arcuri, is not a routine adjustment. It reflects a structural argument that multi-year supply contracts between memory manufacturers and hyperscale cloud providers are fundamentally reducing the cyclicality that has historically capped Micron’s valuation. Mizuho simultaneously reiterated its Outperform rating the same day, adding a second independent bullish voice. What follows breaks down the specific reasoning behind the UBS call, the contract structures underpinning the thesis, the valuation comparison to NVIDIA that makes it provocative, and where Micron’s competitive position in the AI memory race actually stands.

Before US markets opened on 26 May 2026, Micron shares were changing hands at approximately $798.37 in premarket trading, up roughly 6.3% from the prior close of $751.00. The catalyst was a single analyst note.

Micron’s prior rally of more than 20% over two sessions in May 2026, which carried the stock to an all-time closing high of $795.33, was itself driven by a geopolitical catalyst: the composition of the Trump China trade delegation, specifically the inclusion of Micron’s CEO and the exclusion of semiconductor equipment company executives, which the market read as a signal that US export controls on Chinese memory rivals would remain intact.

Premarket reaction: Micron shares jumped approximately 6.3% to $798.37 ahead of the opening bell on 26 May 2026.

UBS analyst Timothy Arcuri published the revision overnight, moving the firm’s price objective from $535 to $1,625, a more-than-threefold increase. The new target implies approximately 116% upside from the $751 close. The key figures tell the story of the call’s scale:

A target revision of this magnitude from a major Wall Street firm is unusual by any measure. The premarket reaction suggests institutional and retail participants alike treated the note as a material event, not a routine upgrade.

Memory stocks have historically traded at compressed valuation multiples for a straightforward reason: the business is cyclical. DRAM and NAND prices swing with supply-demand imbalances, and earnings can collapse as quickly as they expand. That cyclicality has long kept investors from assigning memory makers the kind of premium multiples awarded to companies with more predictable revenue streams.

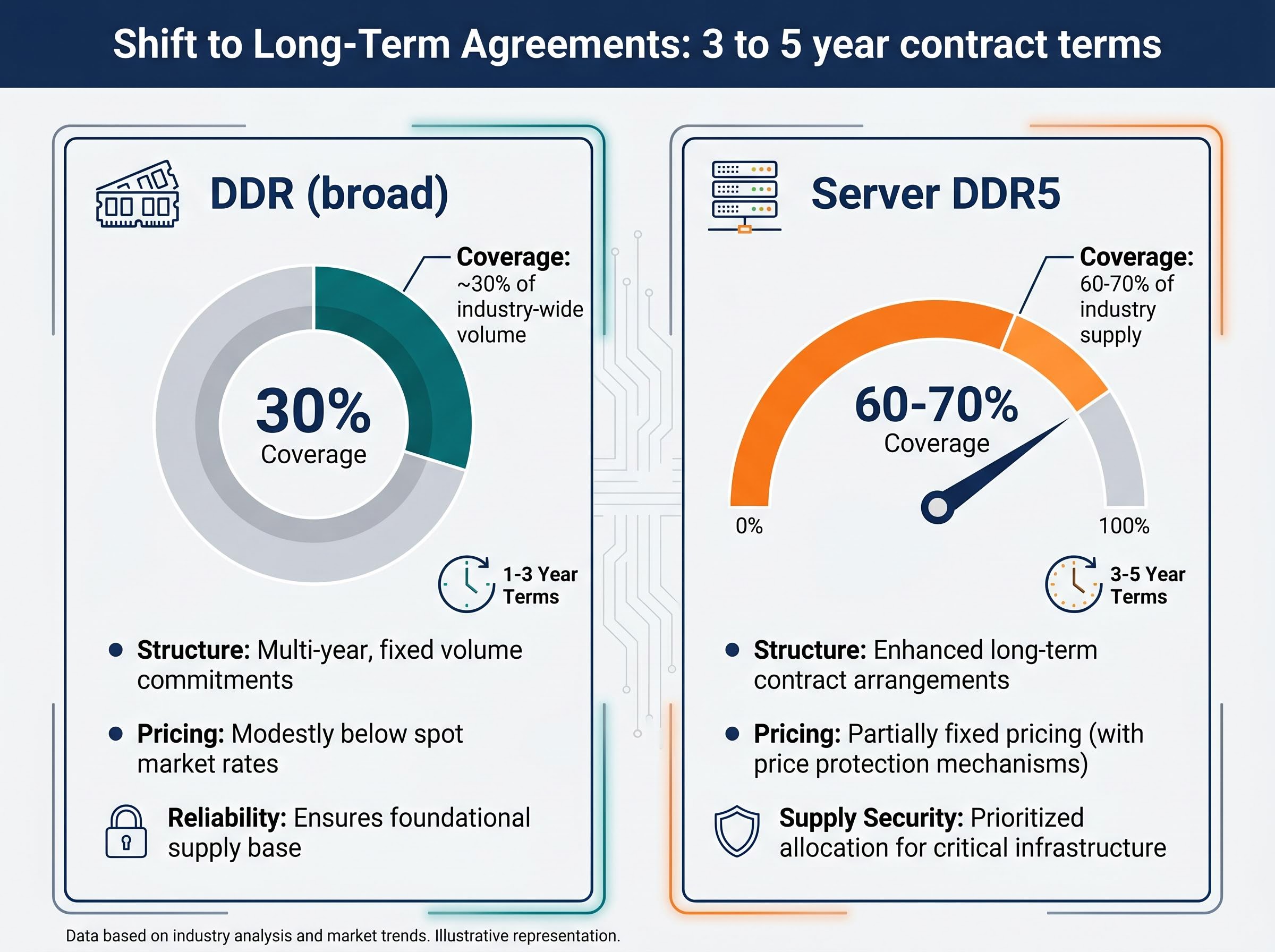

The UBS note argues that dynamic is changing. According to the Investing.com report on Arcuri’s note, multi-year supply agreements between memory manufacturers and hyperscale cloud providers now span three to five years, with fixed volume commitments and partially fixed pricing structures. These are not spot-market transactions. They are capacity reservation arrangements in which hyperscalers accept minimum-volume obligations in exchange for priority access to memory supply, particularly high-bandwidth memory (HBM) and advanced DDR5.

Industry analysis from SemiAnalysis and ChinaTalk (2025) corroborates the broader pattern: hyperscalers have been entering multi-year capacity reservation deals due to chronic HBM and DRAM shortages tied to AI GPU demand.

The Samsung and SK Hynix contract shift to multi-year structures, covering both DDR5 and HBM supply with Google and Microsoft, illustrates how the long-term agreement trend UBS identifies is playing out across all three major memory suppliers rather than being unique to any single player.

The coverage figures reported in the UBS note, as cited by Investing.com, quantify the shift:

| Segment | Estimated coverage share | Structure | Pricing basis |

|---|---|---|---|

| DDR (broad) | Approximately 30% of industry-wide volume | Multi-year, fixed volume commitments | Modestly below spot market rates |

| Server DDR5 | 60-70% of industry supply | Enhanced long-term contract arrangements | Partially fixed pricing |

UBS frames these agreements as a trade-off: memory makers give up some short-term revenue upside in exchange for meaningfully improved demand predictability. If that characterisation is accurate, the traditional case for a cyclicality discount weakens considerably.

The foundry-style contracting model SK Hynix has adopted, with multi-year supply agreements reportedly extending through 2028-2030, is the same structural shift UBS attributes to the broader memory sector; KB Securities analyst Jeff Kim made a parallel argument in May 2026, targeting SK Hynix at 3,000,000 won on the basis that these arrangements could permanently re-rate memory earnings from commodity to infrastructure multiples.

The contract argument leads directly to the note’s most attention-grabbing claim. According to the Investing.com report, Arcuri argues there is little reason Micron and NVIDIA should trade at meaningfully different price-to-earnings multiples, provided the structural demand shift holds.

The logic runs in sequence. If long-term contracts reduce earnings volatility, memory makers no longer carry the cyclicality risk that justified their discount. If AI workloads are increasingly memory-bandwidth constrained, as SemiAnalysis analysis from 2024-2025 argues, then memory occupies a position in the AI value chain comparable in economic importance to GPUs. Those two premises together support a re-rating toward multiples more typically associated with AI infrastructure leaders.

UBS anchored its $1,625 target to approximately 15 times forward twelve-month earnings, using revised EPS projections reported as follows:

Investors wanting to calibrate whether Arcuri’s NVIDIA multiple comparison is stretched will find that AI infrastructure valuation multiples vary considerably even within the GPU and ASIC tier: Nvidia trades at a forward P/E of approximately 24.6x while Broadcom commands roughly 36.8x, a spread that illustrates how much the market differentiates by business model even among direct AI infrastructure leaders, let alone when extending that framework to memory manufacturers.

| Calendar year | Prior EPS estimate | Revised EPS estimate |

|---|---|---|

| 2027 | $133 | $155 |

| 2028 | $122 | $167 |

| 2029 | $77 | $117 |

UBS projects cumulative free cash flow exceeding $400 billion across calendar years 2027-2029, according to the Investing.com report.

Even under UBS’s own downside scenario, in which a moderate downcycle materialises in 2029, the firm estimates EPS would remain above $100. These specific financial projections are attributed to the Investing.com report on Arcuri’s note and have not been independently corroborated through publicly available broker documents.

Seeking Alpha’s reporting on Arcuri’s revised EPS forecasts details how the upward revisions through 2029 underpin the $1,625 target, with the structural contract argument serving as the primary justification for assigning Micron a materially higher earnings multiple than the Street had previously applied.

UBS was not the only firm constructive on Micron on 26 May 2026. Mizuho analyst Vijay Rakesh maintained an Outperform rating and an $800 price target the same day, framing memory as foundational AI infrastructure with durable demand tailwinds.

The gap between UBS’s $1,625 and Mizuho’s $800 is wide. Yet the direction is the same. Both firms point to structural demand durability as the core reason to be constructive, even if they differ sharply on magnitude.

Mizuho’s assessment that no clear resolution to the memory supply-demand imbalance is currently visible carries a specific implication: persistent supply shortfall through 2026-2027 supports elevated DRAM and NAND pricing, which in turn reinforces the earnings visibility thesis UBS also relies on.

One qualification matters here. SemiAnalysis analysis from 2024-2025 notes that Micron holds a third-place position in HBM behind SK Hynix and Samsung. Mizuho’s secular demand framing does not eliminate the competitive risk embedded in that ranking. Broad memory demand durability benefits all three players, but market share within the highest-growth segment remains unevenly distributed.

Analyst price targets represent a specific scenario playing out. Understanding Micron’s competitive position adds the context needed to assess probability alongside potential.

The HBM market, the most supply-constrained and fastest-growing segment of the memory industry, operates as a three-player structure:

SK Hynix’s competitive position in HBM is reinforced by its estimated 52-70% share of Nvidia’s HBM orders, a concentration that reflects first-mover manufacturing advantages rather than pricing alone, and which Samsung is actively working to close through an accelerated HBM3E qualification program with multiple accelerator vendors.

SemiAnalysis has characterised HBM as the most constrained segment in the AI hardware stack, with a multi-year shortage of HBM capacity expected to persist through at least 2026-2027.

Micron’s competitive picture looks different outside HBM. In DDR5 and conventional DRAM, the company is widely regarded as technologically competitive with both Samsung and SK Hynix, and is positioned as a beneficiary of the platform shift toward DDR5-rich AI server configurations.

The broader industry pattern of hyperscaler contract concentration adds a further dimension. In January 2025, The Korea Economic Daily reported that Samsung had expanded a multi-year AI server and HBM collaboration with Microsoft, illustrating how long-term agreements are concentrating around leading suppliers. Micron’s ability to secure similar arrangements in HBM, not just DDR5, remains a variable the bull case depends on.

The UBS note arrives with a clear structural argument: long-term contracts are reducing cyclicality, AI demand is persistent, and memory makers deserve valuation multiples closer to those assigned to GPU leaders. The $1,625 target implies approximately 116% upside from the 26 May 2026 close of $751. Mizuho’s $800 target implies approximately 6.5% upside from the same level, a far more measured claim built on structurally similar reasoning.

The distance between those two numbers captures the genuine uncertainty in the thesis.

For the UBS re-rating argument to be validated, several conditions would need to hold simultaneously:

UBS itself builds in a 2029 downcycle scenario, which signals the firm is not assuming an uninterrupted supercycle. That acknowledgment adds credibility to the note’s framework, even as the target itself remains aggressive relative to the broader Street.

The UBS note and Mizuho’s concurrent rating are arriving at a moment when the memory sector is genuinely at an inflection point. Long-term contracts and AI demand are creating real structural change, even as competitive dynamics remain unresolved. The variables to watch from here are specific: contract renewal announcements, Micron HBM design win disclosures, quarterly DRAM pricing trends, and hyperscaler capital expenditure guidance in coming earnings cycles.

The analyst case is data-supported and structurally reasoned. The re-rating from cyclical memory name to structural AI infrastructure play, however, remains a thesis in progress rather than a settled outcome.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this article are subject to market conditions and various risk factors, and past performance does not guarantee future results.

UBS analyst Timothy Arcuri raised the Micron price target to $1,625 from $535, implying approximately 116% upside from the May 26, 2026 closing price of $751. The target is anchored to roughly 15 times forward twelve-month earnings using revised EPS projections through 2029.

UBS argues that multi-year supply contracts between memory manufacturers and hyperscale cloud providers are reducing the earnings cyclicality that has historically compressed memory stock multiples, and that AI-driven demand makes memory economically comparable to GPU infrastructure in the AI value chain.

Under the UBS framework, multi-year contracts covering 60-70% of server DDR5 supply and roughly 30% of broad DDR volume lock in predictable revenue, weakening the traditional argument for a cyclicality discount and supporting higher price-to-earnings multiples closer to those of AI infrastructure leaders.

Micron is the third-place participant in HBM behind SK Hynix, which leads with an estimated 52-70% share of Nvidia's HBM orders, and Samsung, which occupies second place; Micron is ramping HBM3E products but trails both Korean rivals in volume and active design-win count.

Mizuho analyst Vijay Rakesh maintained an Outperform rating and an $800 price target on May 26, 2026, characterising memory as foundational AI infrastructure with no clear resolution to the supply-demand imbalance visible through at least 2026-2027.