Lenovo Shares Hit All-Time High After 479% Profit Surge

1 hr ago

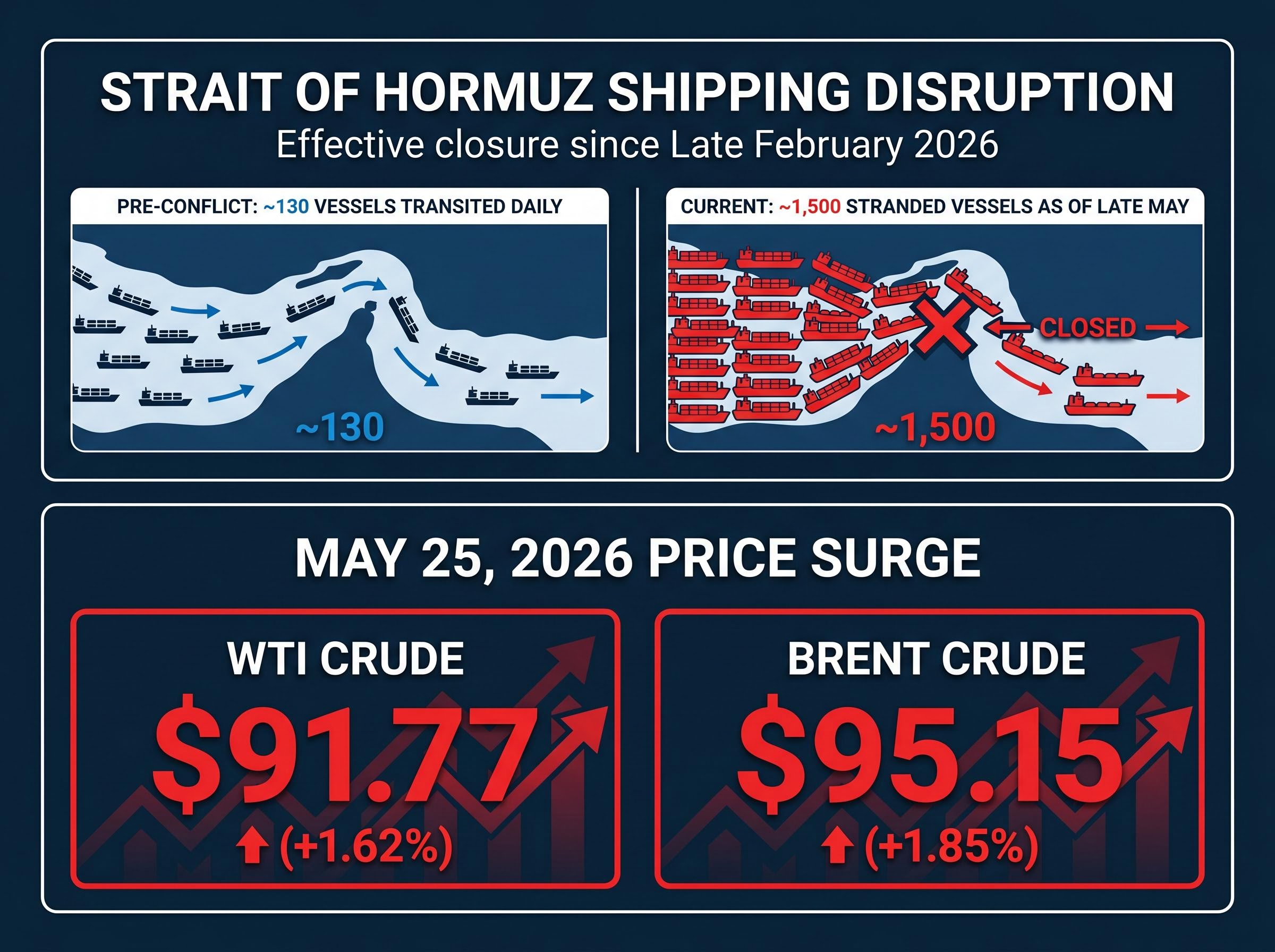

WTI crude surged 1.62% on 25 May 2026, settling at $91.77 per barrel after US Central Command struck missile launch sites and mine-laying vessels in southern Iran. The move snapped a week of falling crude oil prices that had been built on growing diplomatic optimism about a framework deal to reopen the Strait of Hormuz. That optimism evaporated in hours. Brent followed, climbing 1.85% to $95.15, and the broader energy complex repriced accordingly, unwinding days of constructive positioning in a single session.

The strikes arrived at a particularly sensitive moment for global oil markets. Crude had been retreating as reports circulated that Washington and Tehran were approaching a framework agreement to restore commercial shipping through the strait. Instead, markets received confirmation of fresh military action targeting the very infrastructure sustaining the chokepoint closure. What follows is an explanation of the price reversal, the structural supply disruption behind it, the inflation and monetary policy implications, and the cross-asset signals investors should be tracking as diplomacy and conflict continue in parallel.

WTI Crude Oil Futures: $91.77 per barrel, up $1.46 (approximately 1.62%) on 25 May 2026.

For five consecutive sessions, crude had been doing something unusual in a wartime environment: falling. Traders were pricing in a resolution. Reports of advancing negotiations between Washington and Tehran had steadily compressed the geopolitical risk premium that had kept WTI anchored in the $90-$105 range through late May.

Then the strikes landed. Within hours, a week of deliberate repositioning toward diplomatic resolution reversed. The move was not a gradual drift back upward; it was a sentiment break. Traders who had sold the risk premium bought it back in a single session, and the speed of the repricing reflected the degree to which the market had leaned into optimism it could no longer support.

The 25 May reversal is not the first time a week of constructive positioning unwound in hours: a prior diplomatic breakdown on 11 May, when Washington rejected Tehran’s nuclear counteroffer, produced a near-identical pattern of rapid risk-premium reinstatement that erased the preceding week’s decline in a single session.

The 1.6-1.85% gains in WTI and Brent are meaningful on their own, but their significance is amplified by direction. This was not a rally from a base; it was a reversal of a trend that the market had committed to with conviction.

The 25 May strikes did not create the supply disruption. They deepened one that has been running for months.

The Strait of Hormuz has been effectively closed to normal commercial traffic since late February 2026, a consequence of the broader 2025-2026 Iran-United States conflict. Before the crisis, approximately 130 vessels transited the strait daily. That throughput collapsed after hostilities intensified, and as of late May, an estimated 1,500 vessels remained stranded (a figure directionally consistent with reporting, though not independently confirmed by a single named source).

| Strait of Hormuz: Key Figures | Detail |

|---|---|

| Effective closure date | Late February 2026 |

| Estimated stranded vessels | Approximately 1,500 (as of late May 2026) |

| Pre-conflict daily transit volume | Approximately 130 ships per day |

| Negotiation status (as of 25-26 May) | Advancing but not finalised; no reopening timeline confirmed |

The 25 May strikes specifically targeted:

These were not targets selected at random. They struck the infrastructure sustaining the chokepoint closure itself. For investors who had been treating the week’s price decline as evidence that a resolution was imminent, the strikes reframed the situation: the military apparatus keeping the strait closed is still operational, still being reinforced, and now actively under fire.

The strait is the world’s most significant oil transit chokepoint. Its effective closure since February means the $90-plus crude environment reflects sustained multi-month supply disruption, not a geopolitical spike tied to any single headline.

EIA data on Hormuz transit volumes puts the scale of the disruption in context: in 2024, approximately 20 million barrels per day moved through the strait, representing roughly 20% of global petroleum liquids consumption, with no comparable alternative route available to producers on the western side of the Gulf.

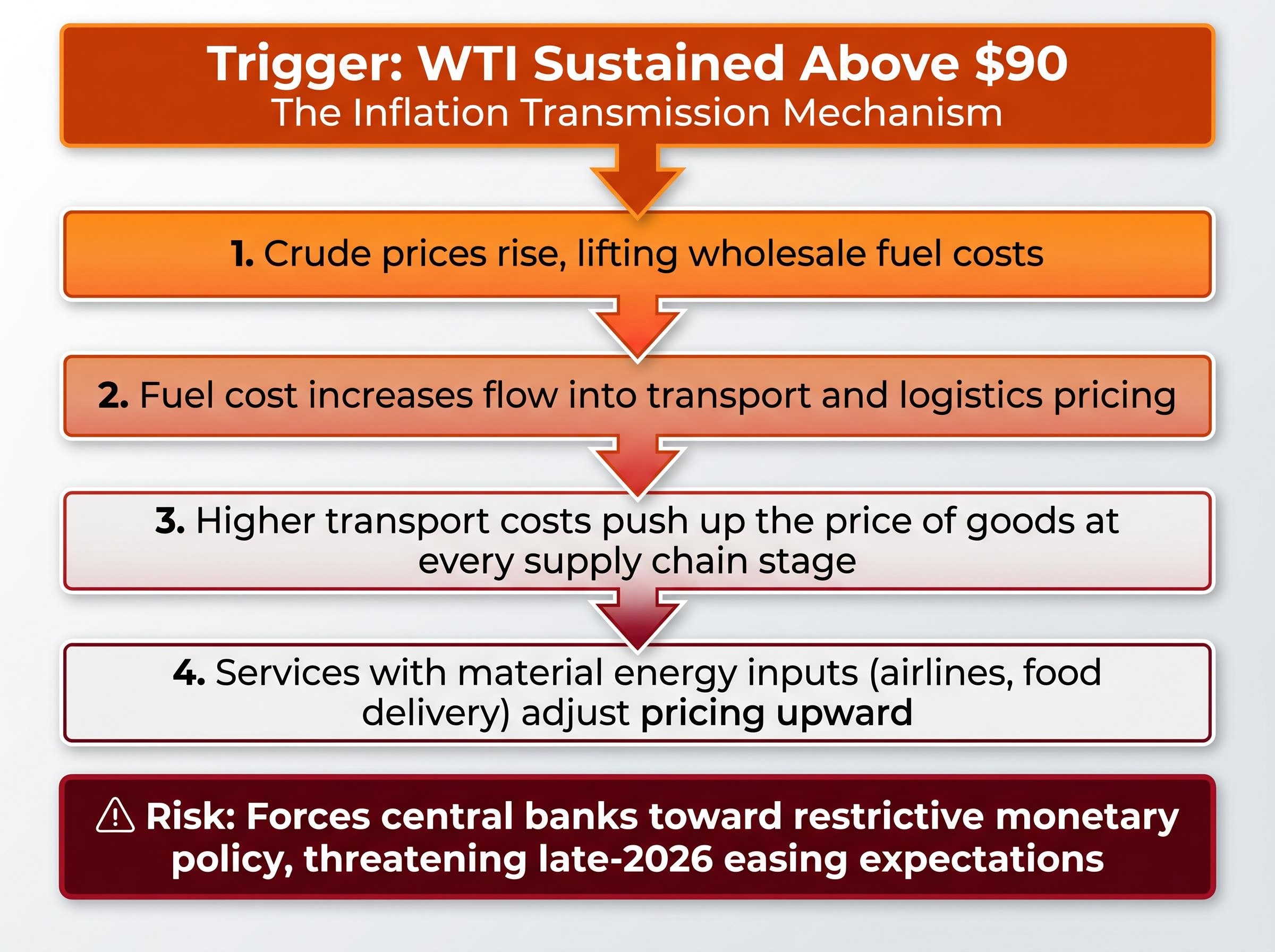

Crude at $91.77 does not stay contained in energy markets. It moves through the economy in a predictable sequence:

This transmission mechanism is why sustained WTI above $90 is a concern that extends well beyond energy portfolios. With crude trading in the $90-$105 range through late May, driven by the Hormuz disruption, the pass-through into consumer prices has been building for months.

Market participants have identified a concern that higher energy costs could push central banks globally toward more restrictive monetary policy, a headwind for risk assets and rate-sensitive instruments across multiple classes, according to Investing.com.

No formal central bank statements explicitly tying the 25 May strikes to revised monetary policy outlooks had been issued as of 26 May 2026. But the concern among rate-watchers is structural, not speculative. If energy-driven inflation feeds into core inflation prints over the coming months, the rate path that markets have been pricing, particularly expectations for easing later in 2026, could shift materially. That repricing would affect bonds, equities, and currencies simultaneously.

Bond market repricing adds a further transmission channel to the inflation concern: US 30-year Treasury yields have reached 5.145% while Japanese government bond yields simultaneously hit 29-year highs, signalling that energy-driven inflation is functioning as a global term-premium driver affecting duration exposure across major markets, not just a domestic US rate story.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Gold fell on 25 May. Oil surged. On the surface, that is a contradiction: a military escalation in the Middle East would typically be expected to drive safe-haven demand for gold upward, not down.

The explanation lies in the rate-expectations channel. The same energy inflation concern that pushed crude higher also reinforced the case for tighter monetary policy. A tighter rate path strengthens the dollar and raises real yields, both of which increase the opportunity cost of holding non-yielding assets like gold. The US dollar stabilised following the military developments, adding direct downward pressure on precious metals priced in dollars.

| Asset | Price | Change (%) | Date/Time |

|---|---|---|---|

| Spot Gold | $4,535.17/oz | -0.8% | 25 May 2026, 21:37 ET |

| Gold Futures | $4,568.67/oz | -0.8% | 25 May 2026 |

| Spot Silver | $76.4495/oz | -2.1% | 25 May 2026 |

| Spot Platinum | $1,955.02/oz | -0.6% | 25 May 2026 |

Gold had been gaining in prior sessions precisely because diplomatic progress toward a Hormuz deal was reducing perceived geopolitical risk, allowing the metal to trade on softer rate expectations rather than fear. The strikes reversed that logic. The 25 May session is a useful case study: in an energy-disrupted macro environment, inflation expectations and rate-path repricing can override the simple safe-haven reflex.

The counterintuitive pattern of oil up and gold down under active military escalation has played out across the full three months of the US-Iran conflict, with dollar strength and rate expectations consistently overriding traditional safe-haven demand whenever crude-driven inflation concerns dominated the session narrative.

The environment following the 25 May strikes is defined by dual-track uncertainty. Active military escalation is running alongside unfinished ceasefire negotiations, creating a binary risk profile for energy markets where the next development in either direction could produce an outsized reaction.

Rather than attempting to predict which track prevails, a structured monitoring framework offers more utility. The signals that matter most:

The broader 2025-2026 conflict context means these oil market conditions reflect sustained multi-month supply risk. A resolution, or further escalation, would likely produce a market reaction far larger than a typical daily fluctuation.

Investors wanting to understand why a supply shock of this magnitude has not pushed Brent past its March peak will find our deep-dive into the Brent pricing paradox, which examines how demand destruction, partial reopening probability, and divergent IEA, EIA, and OPEC demand forecasts are all simultaneously embedded in the current futures curve.

A week of diplomatic optimism collapsed in hours on 25 May 2026. Oil repriced upward, gold repriced downward, and rate expectations shifted toward tighter policy, all from a single military action that targeted the infrastructure keeping the world’s most significant oil chokepoint closed.

The Strait of Hormuz situation is not a headline. It is a sustained structural disruption that has been shaping the macro environment since late February 2026, and its resolution or deepening will be one of the defining variables for energy, inflation, and monetary policy through the remainder of the year. Staying informed on both the military and diplomatic tracks is not optional for anyone making asset allocation decisions in this environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

US Central Command struck missile launch sites and mine-laying vessels in southern Iran on 25 May 2026, ending a week of falling crude prices that had been driven by optimism over a potential Strait of Hormuz framework deal.

The Strait of Hormuz is the world's most significant oil transit chokepoint, handling roughly 20 million barrels per day before the crisis; its effective closure since late February 2026 has sustained elevated crude prices by cutting off a major supply route with no comparable alternative.

Gold fell because the same military escalation that pushed crude higher also reinforced expectations of tighter monetary policy; a stronger dollar and higher real yields increase the opportunity cost of holding non-yielding assets like gold, overriding the typical safe-haven demand.

Sustained crude above $90 flows through the economy via higher fuel, transport, and goods costs, and if energy-driven inflation feeds into core inflation prints, central banks may delay or reverse expected rate cuts, creating a headwind for bonds, equities, and rate-sensitive assets.

Key signals include any confirmation or breakdown of a Hormuz framework deal, evidence of commercial vessels resuming strait transit, central bank statements referencing energy inflation, and whether WTI sustains a move above $105 or below $90.