BlackRock Raises AI and Tech Decoupling to Top Risk Tier

21 hrs ago

Kogan.com shares surged approximately 15% on 26 May 2026, marking one of the sharpest single-day moves the ASX-listed online retailer has posted in recent memory. The catalyst was an operational update covering 10 months of trading to 30 April 2026, and the numbers landed well ahead of where the market had positioned. With growth accelerating across both the Australian and New Zealand segments, the update triggered a rapid repricing that raises two immediate questions: what exactly drove the reaction, and does the post-rally share price leave room for further upside? What follows is a full breakdown of the group-level scorecard, the segment-level mechanics, and the valuation question investors now face.

The 15% single-session move places Kogan.com (ASX: KGN) among the sharpest daily gainers on the ASX this year. Moves of that magnitude on a mid-cap retailer do not happen when results land in line with expectations.

The trigger was the company’s April 2026 operational update, released as an ASX investor announcement and covering the 10-month period ended 30 April 2026. As reported by Rask Media’s Jaz Harrison on 26 May 2026, the update delivered broad-based improvement across revenue, earnings, and customer metrics simultaneously. The scale of the repricing signals that consensus expectations were sitting meaningfully below the actual figures, catching short-term positioning offside and forcing a rapid adjustment.

Rate expectations shape consumer discretionary sector dynamics well before any central bank decision lands, as the 12.8% surge in Australian consumer sentiment in November 2025 on rate cut expectations alone demonstrated; for Kogan.com, a platform whose active customer base tracks household discretionary budgets, that sensitivity runs directly through its revenue line.

What makes this result unusual is the breadth. It is not a single headline number carrying the rest; every major group-level metric improved over the prior corresponding period.

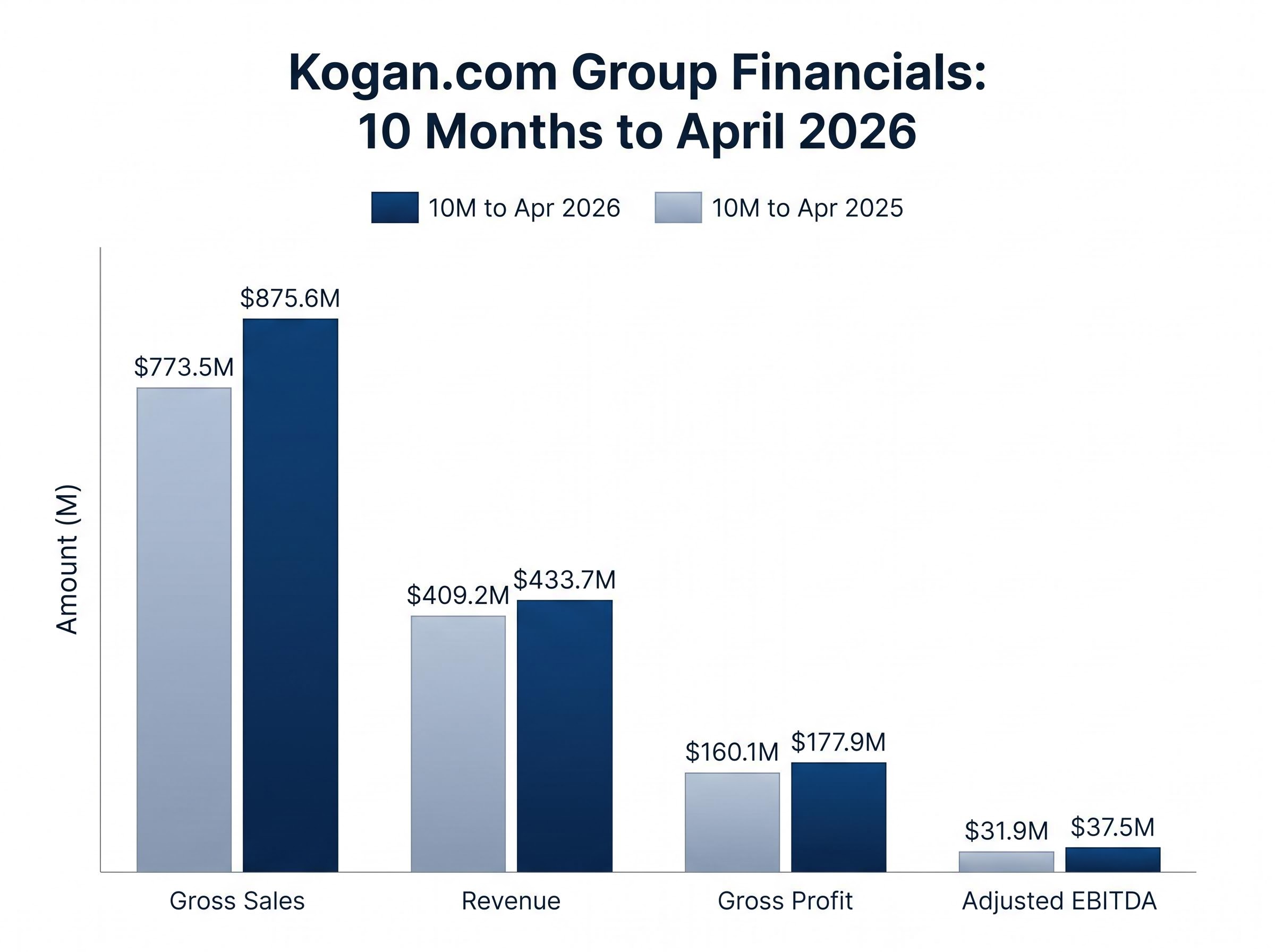

Gross sales rose 13.2% to $875.6 million. Revenue increased 6% to $433.7 million. Active customers grew 4% to 3.5 million. Those top-line gains would be solid on their own, but the more telling signal sits further down the income statement.

Group gross profit climbed 11.1% to $177.9 million, with the gross profit margin expanding 1.9 percentage points to 41%. Adjusted earnings before interest, taxes, depreciation, and amortisation (EBITDA) rose 17.4% to $37.5 million, while adjusted earnings before interest and taxes (EBIT) grew 25.4% to $26.9 million.

The margin expansion is where this result separates itself. Retailers can grow revenue by discounting. Growing gross profit margin by nearly 2 percentage points while simultaneously expanding the top line suggests pricing discipline and a favourable product mix, not volume-bought growth.

| Metric | 10M to Apr 2025 | 10M to Apr 2026 | Change |

|---|---|---|---|

| Gross sales | $773.5M | $875.6M | +13.2% |

| Revenue | $409.2M | $433.7M | +6.0% |

| Active customers | 3.37M | 3.5M | +4.0% |

| Gross profit (margin) | $160.1M (39.1%) | $177.9M (41.0%) | +11.1% (+1.9pp) |

| Adjusted EBITDA | $31.9M | $37.5M | +17.4% |

| Adjusted EBIT | $21.5M | $26.9M | +25.4% |

The group result is strong. The Australia segment result explains why.

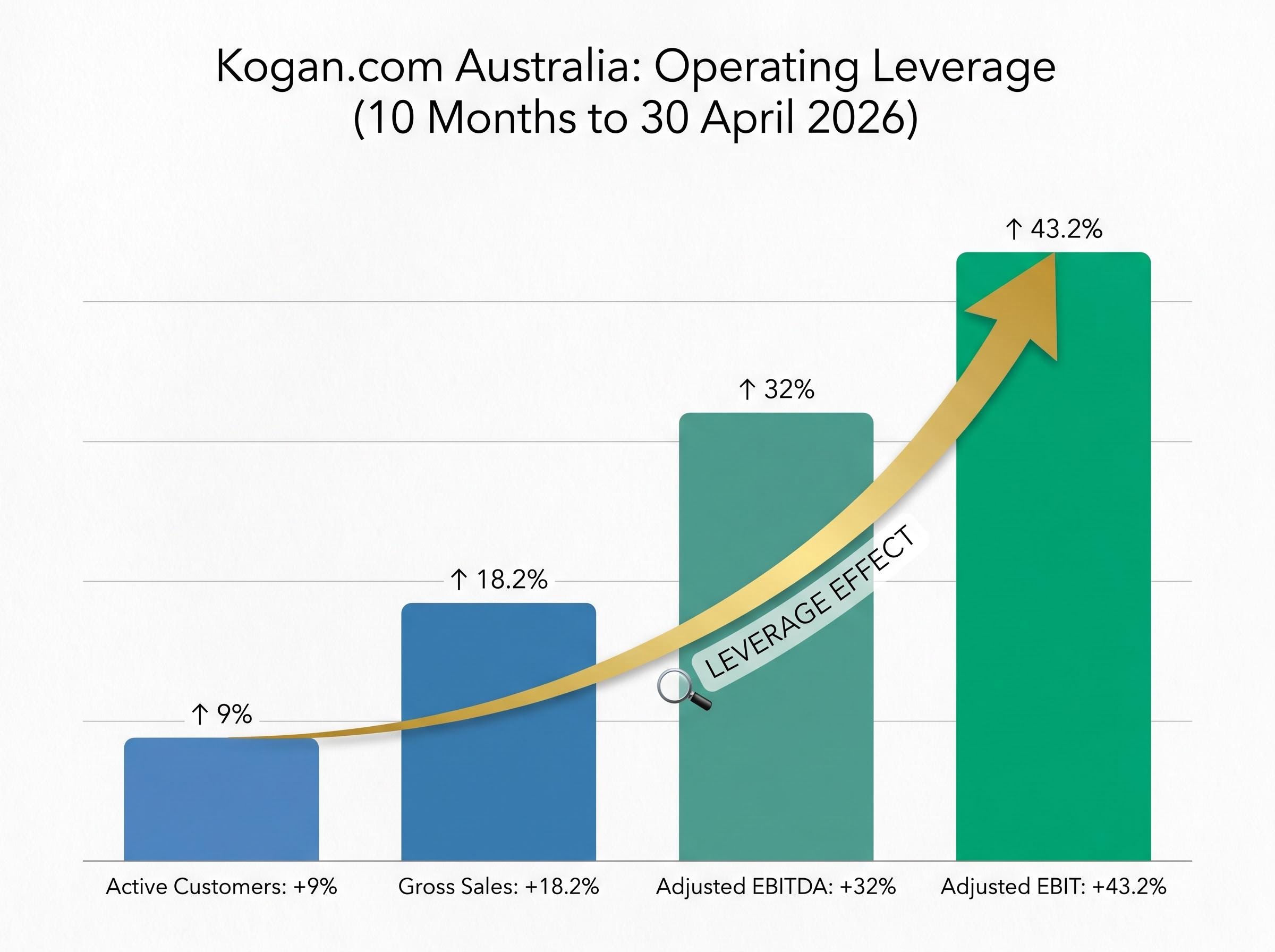

Kogan.com Australia delivered gross sales growth of 18.2% year-on-year for the 10 months ended 30 April 2026, with segment revenue up 18.1% over the same period. Active customers in the Australia division grew 9%, nearly double the group-level customer growth rate of 4%, suggesting the Australian platform is pulling in new buyers at an accelerating clip.

The compounding effect shows up clearly in the earnings progression:

Operating leverage signal: Adjusted EBIT grew at 43.2% on gross sales growth of 18.2%, meaning each additional dollar of revenue is dropping through to profit at more than twice the rate of the top-line expansion.

That ratio is the number that matters most for full-year FY26 earnings estimates. It indicates that the cost base has reached a point where incremental sales generate disproportionate profit, a dynamic management attributed to targeted marketing expenditure and platform-based sales growth rather than broad promotional spending.

Operating leverage in ASX e-commerce is not unique to Kogan.com: Temple and Webster reported a record April 2026 EBITDA of $2.5 million against upgraded FY26 revenue guidance of $665-$675 million even as its share price traded near a 52-week low, creating a sector-wide question about whether the market is systematically mispricing the profit inflection that capital-light online retail models produce at scale.

Mighty Ape, Kogan’s New Zealand subsidiary, has been a recurring drag on consolidated margins. That narrative is shifting.

The business has been restructuring toward a capital-light, higher-margin model: discontinuing underperforming product lines, launching private label ranges through the Kogan.com marketplace as a third-party seller, and executing structural cost reductions. The full 10-month figures show progress:

Steady improvement, but not yet the kind of inflection that changes the investment case. The acceleration in the most recent four-month window tells a different story.

Over the four months to 30 April 2026, Mighty Ape’s results sharpened considerably:

The gap between those two timeframes is the signal. A 1.3 percentage point margin gain over 10 months suggests gradual improvement. An 8.4 percentage point gain over the most recent four months suggests the operational changes are compounding. If the four-month run-rate holds, Mighty Ape approaches breakeven within a foreseeable horizon, removing one of the more persistent bear case arguments against KGN’s consolidated earnings quality.

Kogan.com Ltd (ASX: KGN) is an Australian online retail platform operating across electronics, general merchandise, and marketplace categories. The business runs two primary segments:

The group reported 3.5 million active customers as of the 10-month period to 30 April 2026.

ASX-listed companies release operational updates at intervals between formal half-year and full-year results. These updates carry market-moving weight because they provide revenue and earnings visibility before the audited result, filling an information gap that investors price accordingly. When the data in an operational update deviates meaningfully from consensus expectations, as it did on 26 May 2026, the share price adjusts to reflect the new information in a single session. For a retailer like Kogan.com, where earnings are sensitive to customer acquisition trends and margin trajectory, these updates function as the market’s most timely read on the business between formal reporting dates.

The ASX continuous disclosure obligations under Listing Rule 3.1 require listed companies to immediately notify the market of any information that a reasonable person would expect to have a material effect on the price or value of their securities, which is why operational updates like Kogan’s April 2026 release carry immediate share price consequences rather than waiting for formal half-year filings.

The 18.2% Australia segment growth rate and 43.2% EBIT leverage are strong by any measure. The question is whether they represent a sustainable trajectory or a period of outperformance that compresses toward the mean.

Bull case variables:

Bear case variables:

The Australia Post eCommerce Report tracks total online spend and year-on-year growth rates across the domestic market, providing the sector-level baseline against which Kogan’s 18.2% Australia segment growth can be benchmarked, with broader Australian e-commerce growth having normalised toward single-digit and low-double-digit annual rates in the post-pandemic period.

Rask Media’s Jaz Harrison, writing on 26 May 2026, explicitly flagged uncertainty around whether the current growth rate is sustainable and questioned whether the share price at post-rally levels represents good value. Harrison also noted that other ASX-listed growth companies may offer a more defined pathway to long-term profit expansion. The author disclosed no financial or commercial interest in KGN at the time of publication.

The partial-year adjusted EBITDA of $37.5 million over 10 months provides a base for investors constructing full-year FY26 estimates, but the sustainability of the growth rate will ultimately determine whether those estimates prove conservative or optimistic.

Investors exploring whether KGN’s post-rally price represents fair value or the start of a re-rating will find our dedicated guide to valuing ASX growth stocks useful; it walks through the four-metric framework covering revenue trajectory, profit expansion trend, ROE direction, and operating leverage that is most applicable to companies at exactly this stage of their earnings cycle.

The April 2026 operational update delivered broad-based improvement across every group and segment metric that matters: revenue, margins, earnings, and customer growth. The market’s 15% repricing reflected the gap between expectations and reality.

Two distinct stories are converging. The Australia segment is demonstrating structural operating leverage, with earnings growing more than twice as fast as sales. Mighty Ape is restructuring toward breakeven at an accelerating rate. If both trajectories hold through the final two months of FY26, the formal full-year result becomes the next material catalyst.

The open question is valuation. A 15% rally in a single session absorbs a meaningful portion of near-term upside, and sustainability of the growth rate remains unresolved. The upcoming FY26 full-year result will provide the clearest test of whether today’s price reflects fair value or the beginning of a longer re-rating.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

An ASX operational update is a company announcement released between formal half-year and full-year results that provides early visibility on revenue and earnings. For Kogan.com, when the April 2026 update showed results meaningfully above market expectations, the share price adjusted 15% higher in a single session to reflect the new information.

Kogan.com reported gross sales up 13.2% to $875.6 million, revenue up 6% to $433.7 million, active customers up 4% to 3.5 million, and adjusted EBITDA up 17.4% to $37.5 million for the 10 months ended 30 April 2026, with gross profit margin expanding 1.9 percentage points to 41%.

Kogan.com Australia delivered gross sales growth of 18.2% for the 10 months to April 2026, which is well above the broader Australian e-commerce market, where growth has normalised toward single-digit to low-double-digit annual rates in the post-pandemic period.

Operating leverage occurs when a fixed cost base means each additional dollar of revenue generates a disproportionately large increase in profit. In Kogan's Australian segment, adjusted EBIT grew 43.2% on gross sales growth of just 18.2%, meaning profit expanded at more than twice the rate of the top-line increase.

Mighty Ape's gross profit margin improved 1.3 percentage points across the full 10-month period, but the most recent four months showed sharper progress, with gross profit margin up 8.4 percentage points to 37.8% and adjusted EBITDA losses declining 52.8% year-on-year, indicating the restructuring changes are accelerating.