SpaceX’s $800 Price Target: Right Direction, Wrong Timeline?

1 hr ago

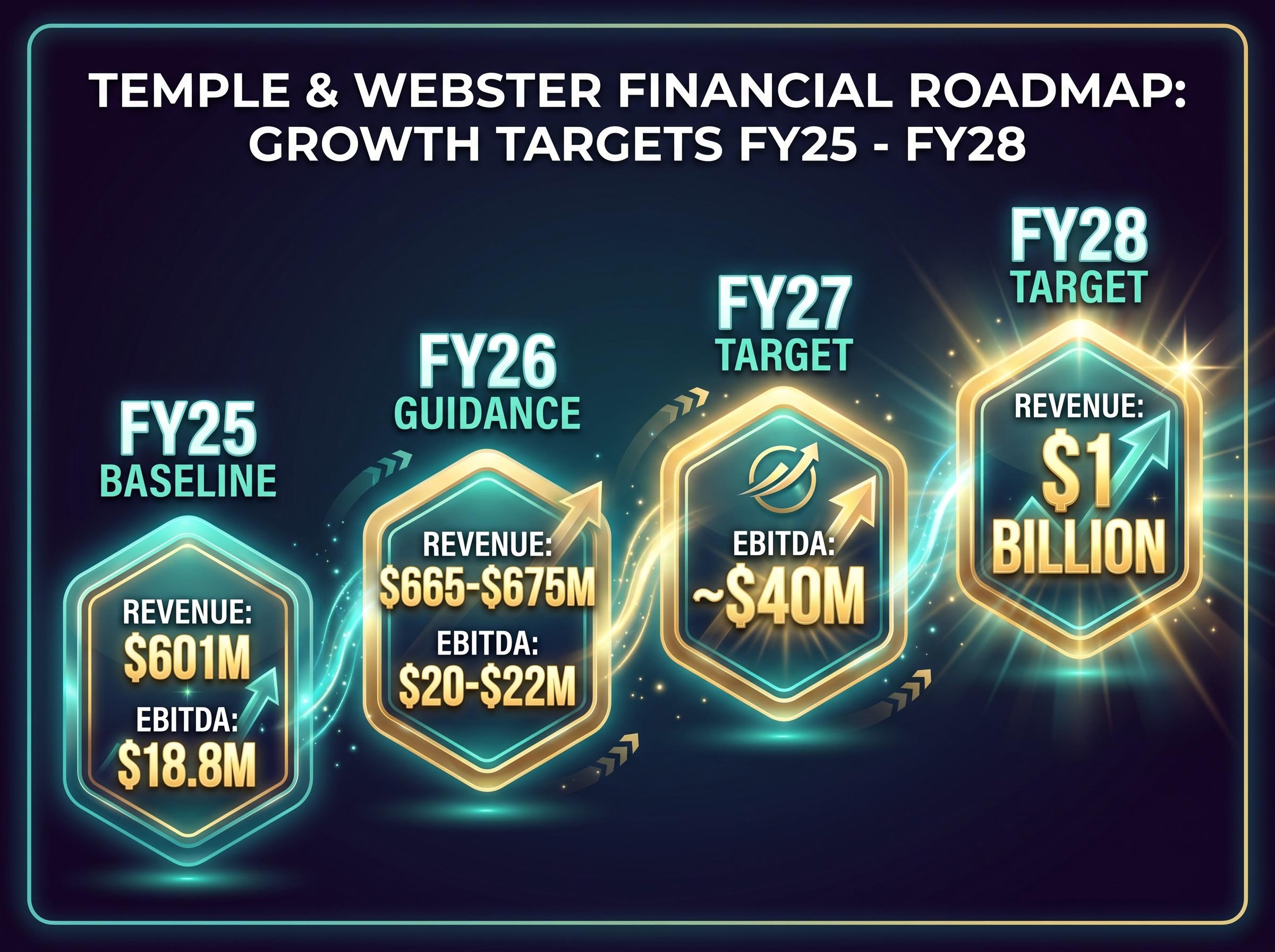

Temple & Webster is posting record monthly EBITDA and upgrading FY26 revenue guidance, yet its share price sits near a 52-week low after falling roughly 72% year-to-date. That gap between operational momentum and market pricing is the central question facing investors right now. The company’s 13 May 2026 trading update confirmed FY26 revenue of $665-$675 million and a record April EBITDA of $2.5 million, while CEO Mark Coulter simultaneously outlined a roadmap to approximately $40 million EBITDA in FY27 and $1 billion in revenue by FY28. For investors weighing the long-term case, the numbers arriving from the business and the signal coming from the TPW share price are pointing in opposite directions.

What follows is an analysis of the strategic pillars underpinning Temple & Webster’s multi-year growth targets, the operational pivot already shifting the margin trajectory, and what the analyst consensus implies about whether the current share price represents a mispricing or a rational discount.

The first half of FY26 told one story. Temple & Webster accepted thinner margins to chase market share, a strategy that delivered $14.9 million in EBITDA (excluding New Zealand start-up costs) on a 4.0% margin. That was growth-first thinking in a consumer environment that rewarded volume.

The May 2026 trading update told a different one. Full-year EBITDA guidance of approximately $20-$22 million implies 6%-17% expansion on FY25’s $18.8 million baseline, and April’s $2.5 million EBITDA set a record for that calendar month. The shift was not accidental. Management pulled five specific levers:

CEO Mark Coulter framed the pivot as a prudent response to economic uncertainty, describing it as a deliberate choice to prioritise profitability while consumer confidence remains at historically low levels.

The distinction matters. If these levers are structural and repeatable rather than one-off adjustments, the FY27 EBITDA doubling case gains a mechanical foundation beneath the headline number.

Temple & Webster reported $601 million in FY25 revenue. The company’s stated target is $1 billion-plus by FY28. That gap implies roughly 66% cumulative growth over three years, a figure that demands specificity about where the incremental revenue is expected to originate.

Four divisions carry the load.

| Division / Initiative | H1 FY26 Performance | Strategic Role in $1B Target |

|---|---|---|

| Home Improvement | +47% revenue growth; ~20% private label penetration | Highest-growth category; expands addressable market beyond furniture |

| Trade & Commercial (B2B) | +24% revenue growth | Higher average order values; recurring demand from holiday/student accommodation |

| New Zealand | $1M in first ~4 months (launched October 2025) | International proof of concept; long-term revenue diversification |

| Private Label | ~20% penetration in Home Improvement | Margin accretive; reduces supplier dependency |

The $1 billion target is explicit management guidance, not analyst extrapolation. That makes it a testable commitment, and the divisional performance data above offers the first layer of evidence for or against its achievability.

Beyond organic growth, Temple & Webster’s $161 million cash position and zero debt create genuine optionality. Coulter specifically referenced the company’s improved earnings position as enabling it to capitalise on a more favourable acquisitions environment.

No specific targets have been confirmed. M&A remains a potential upside scenario rather than a base-case assumption, but the balance sheet capacity to act is unambiguous: $23 million in free cash flow generated in H1 FY26 alone continues to build the war chest.

E-commerce M&A consolidation is accelerating across the sector, with the Etsy and eBay transaction in April 2026 illustrating how platform businesses are using strategic divestitures and acquisitions to sharpen competitive positioning and deploy accumulated capital, a dynamic that shapes the environment in which Temple & Webster might deploy its own $161 million war chest.

The projected doubling of EBITDA from approximately $21 million at FY26’s midpoint to roughly $40 million in FY27 sounds aggressive in isolation. Broken into its component parts, the mechanics become more legible.

The model is supported by a growing demand base. Active customers reached approximately 1.4 million in H1 FY26, up 14% year-on-year, while market share sits at 2.7% of the Australian furniture and homewares market.

The FY27 EBITDA target of approximately $40 million has been referenced by CEO Mark Coulter and in analyst commentary but has not been formalised as official company guidance. Investors should treat it as a directional indicator rather than a confirmed commitment.

Temple & Webster operates a drop-shipping model, meaning the company holds minimal inventory. Suppliers ship products directly to customers, which eliminates warehousing costs and substantially reduces working capital requirements. This is not merely an operational detail; it is the structural reason the EBITDA doubling story is plausible.

The difference from traditional furniture retail economics shows up in three areas:

That capital efficiency is why a 2.7% market share in a large, fragmented category represents a long runway rather than a ceiling.

Temple & Webster outperforms traditional bricks-and-mortar peers on online growth metrics, benefiting from the ongoing structural shift toward online purchasing in furniture and homewares. That tailwind remains intact.

The Australia Post eCommerce Report 2026 recorded total Australian online retail spend at $82.6 billion in 2025, with 24% of all retail transactions conducted online, a market-level data point that contextualises Temple and Webster’s 2.7% share as a genuinely small slice of a large and still-expanding channel.

IKEA’s January 2026 Matter-compatible smart home launch in Australia signals increased investment in adjacent categories, a development worth monitoring for its potential overlap with Temple & Webster’s Home Improvement division. Among other online competitors, Koala, Brosa, and Wayfair Australia have not made significant disruptive strategic moves based on available data through May 2026.

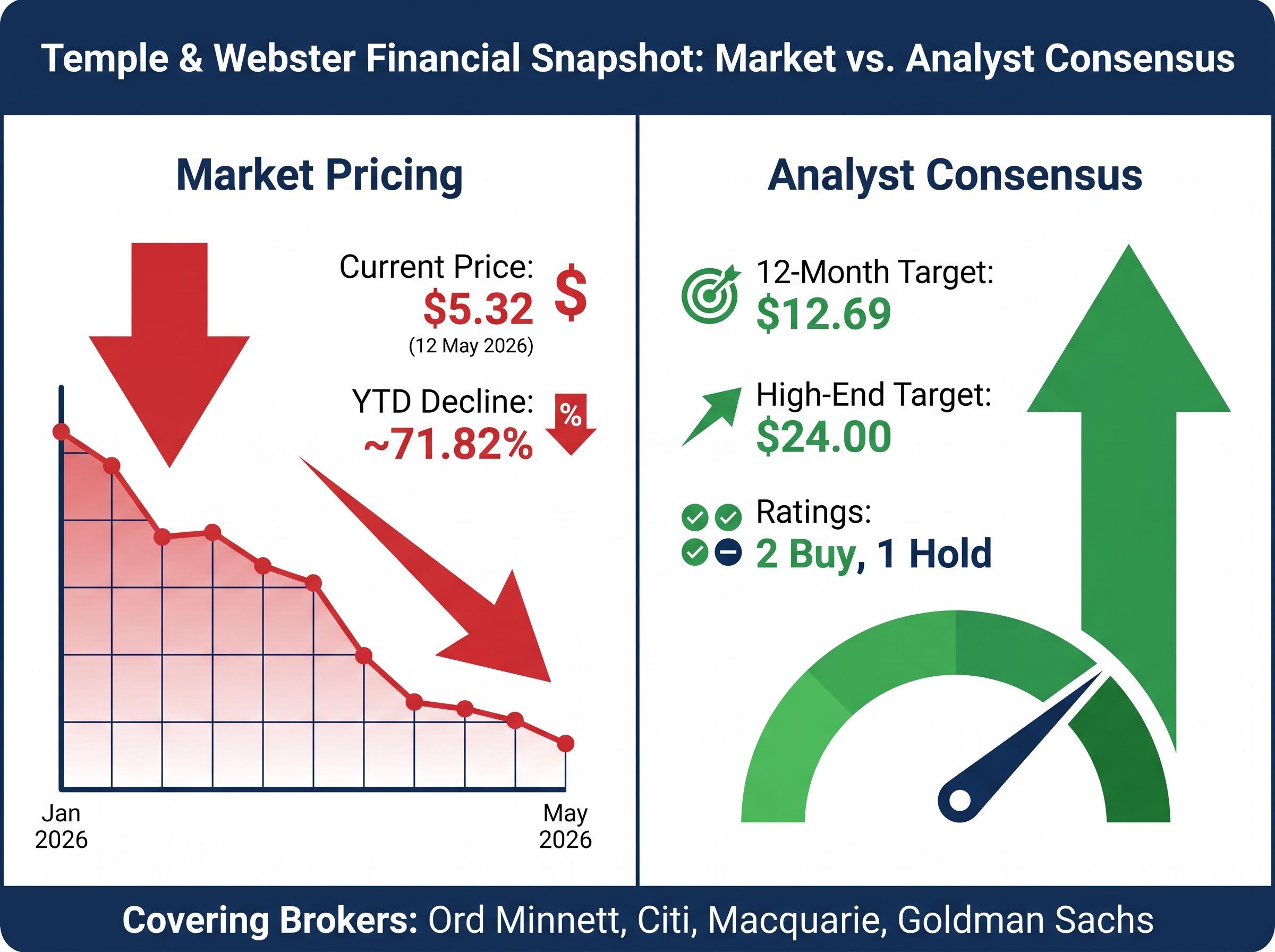

The share price is the fact every Temple & Webster investor already knows. Approximately $5.32 at the 12 May 2026 close, down 6.01% on the session, and sitting at or near a 52-week low of $5.25 reached that same day. Year-to-date, the decline stands at approximately 71.82%.

Retail investor behaviour in Australia has shifted materially in 2026, with capital rotating rapidly in response to macroeconomic signals and RBA policy moves, a pattern that partly explains why Temple & Webster’s share price can fall sharply on macro sentiment even when the company’s own operating metrics are improving.

The analyst consensus tells a strikingly different story.

| Metric | Value |

|---|---|

| Current Share Price (12 May 2026) | $5.32 |

| 52-Week Low | $5.25 |

| Year-to-Date Decline | ~71.82% |

| 12-Month Consensus Price Target | $12.69 |

| 3-Month Average Price Target | $12.15 |

| High-End Analyst Target | $24.00 |

| Analyst Ratings | 2 Buy, 1 Hold |

The 12-month consensus target of $12.69 implies more than 100% upside from the current price. Covering brokers include Ord Minnett, Citi, Macquarie, and Goldman Sachs.

That spread forces a specific analytical question. For the market to be correct at $5.32, something would need to be deteriorating in the business that is not yet visible in the operating results, or the macro environment would need to worsen materially beyond what management has already flagged. The consensus, by contrast, implies the share price has overshot to the downside relative to the FY27-FY28 growth roadmap.

The investment thesis rests on a set of specific execution dependencies. Each one is testable against incoming data:

Against those dependencies sit clear risk factors:

The CEO transition at Temple & Webster, announced in April 2026, adds a layer of execution context that sits beneath the financial roadmap: co-founder Mark Coulter moves to Executive Chair from 1 July 2026, with returning executive Susie Sugden taking the operating reins at precisely the point where the FY27 EBITDA doubling must be delivered.

The M&A optionality cuts both ways. A well-timed bolt-on acquisition could accelerate the path to $1 billion in revenue. A poorly executed one could distract management and introduce costs that erode the capital-light model’s advantages.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The operational metrics are moving in one direction: record monthly EBITDA, upgraded revenue guidance, a growing customer base, and a balance sheet carrying $161 million in cash with zero debt. The share price is moving in the other, down approximately 72% year-to-date and sitting near 52-week lows.

The $1 billion FY28 revenue target is explicit management guidance. The FY27 EBITDA doubling has a stated mechanical basis in the operating leverage of the drop-shipping model. The analyst consensus of $12.69 implies significant undervaluation at current levels.

Whether that consensus proves correct depends on whether the execution dependencies outlined above hold through a period of weak consumer confidence and macroeconomic pressure. The Temple & Webster story is not yet resolved, but the analytical framework to assess it is now in the reader’s hands.

The 12-month consensus price target for Temple and Webster is $12.69, based on coverage from brokers including Ord Minnett, Citi, Macquarie, and Goldman Sachs, implying more than 100% upside from the May 2026 share price of approximately $5.32.

Temple and Webster's share price declined approximately 72% year-to-date by May 2026, driven largely by macro sentiment, weak Australian consumer confidence, and elevated interest rates pressuring discretionary spending, even as the company's own operating metrics continued to improve.

Temple and Webster has set explicit management guidance of more than $1 billion in revenue by FY28, up from $601 million in FY25, with growth expected to be driven by its Home Improvement, Trade and Commercial, New Zealand, and Private Label divisions.

Temple and Webster's drop-shipping model means suppliers ship products directly to customers, eliminating warehousing costs and reducing working capital needs, which results in higher incremental margin contribution on each additional dollar of revenue compared with traditional furniture retailers.

Key risks include a prolonged deterioration in Australian consumer confidence, a potential reversion to margin-sacrificing market-share tactics, macroeconomic pressure from elevated interest rates, a CEO transition in July 2026, and the possibility that any M&A deployment of the $161 million cash position proves dilutive rather than accretive.