Why the 2026 Midterm Could Break a Rare Presidential Streak

1 hr ago

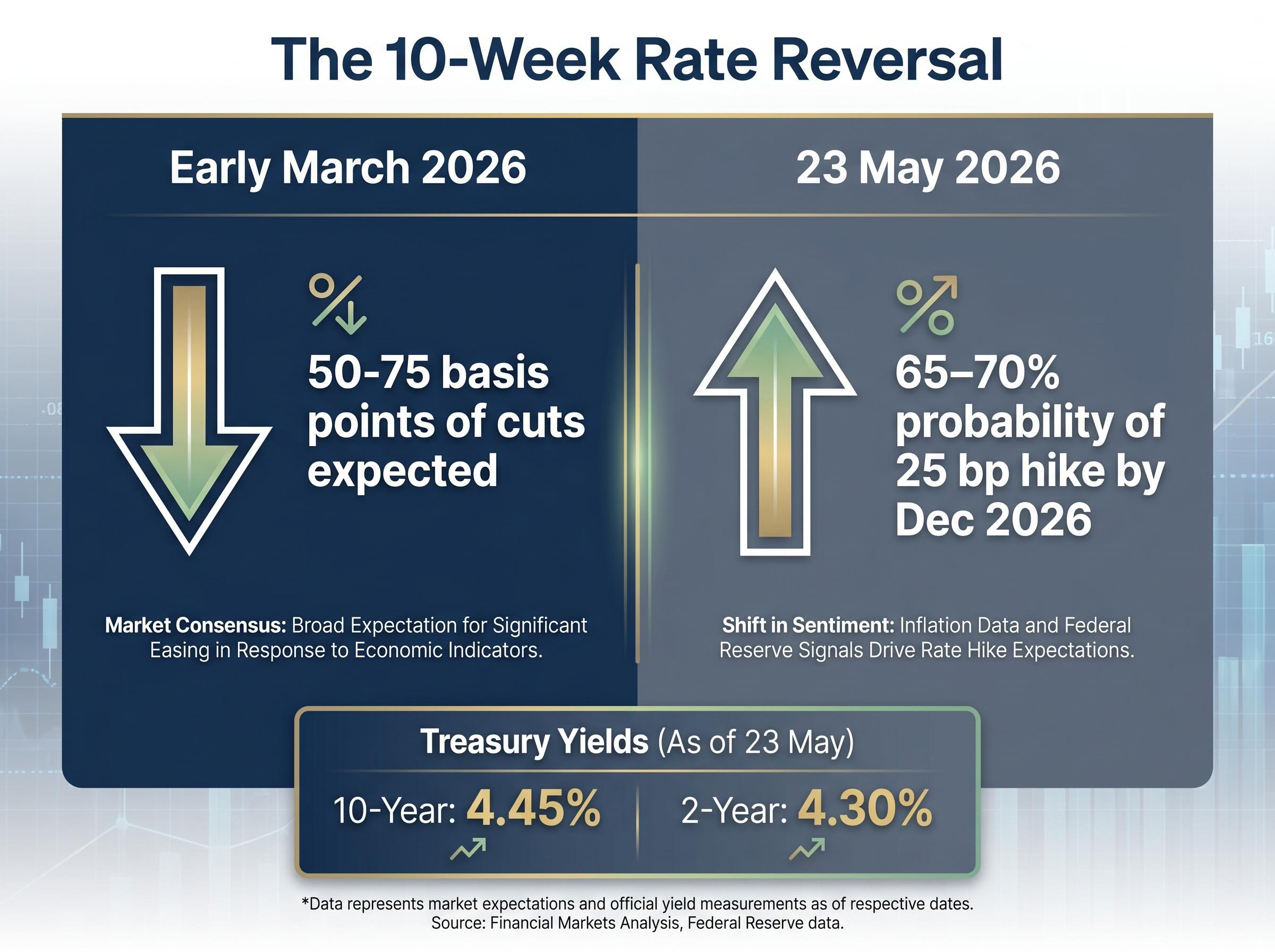

Markets began the week of 26 May 2026 pricing a 65-70% probability of a Federal Reserve rate hike by December, a figure that stood at zero just ten weeks earlier, when traders were instead expecting 50-75 basis points of cuts. The swing in rate expectations has been driven by sticky core inflation, surging Treasury yields, and a series of unusually explicit signals from Fed officials about the conditions under which they would reverse course. The imminent release of April Core PCE data on 28 May, forecast by Goldman Sachs and Bank of America to print at 3.7-3.8% year-over-year, threatens to sharpen this repricing further. What follows is an examination of the mechanics behind the shift, the specific data thresholds that would force the Fed’s hand, what a mid-cycle rate hike would mean historically, and how institutional investors are restructuring portfolios in response.

The speed of the repricing is the story. In early March 2026, fed funds futures implied 50-75 basis points of cuts by year-end. As of 23 May, CME FedWatch probabilities assign approximately 65-70% odds of at least one 25 bp hike by the December 2026 FOMC meeting. OIS markets price roughly 30 bps of additional tightening over the same horizon.

That is not a gradual drift. It is a full reversal of the rate trajectory that defined portfolio construction for most of the past 18 months.

The 10-year Treasury yield reached 4.45% and the 2-year hit 4.30% as of 23 May, both at their highest levels since late 2025. The front end of the curve led the selloff, a signature that distinguishes a policy repricing from a growth or supply-driven move.

“The front end of the curve has led the selloff as traders now see the Fed’s next move more likely to be a hike than a cut.” — Bloomberg News, 20 May 2026

Four forces converged to drive the yield surge:

The current inflation overshoot did not emerge from broad demand excess alone; the relationship between the energy shock and Fed rate path calcified in May 2026 as Brent crude trading roughly 52% above its pre-conflict baseline compressed the window for cuts and began opening the door to hikes before most strategists had updated their base cases.

Investors who anchored to the March narrative are positioned for a world that no longer exists in market pricing.

Core PCE, the Personal Consumption Expenditures price index excluding food and energy, is the inflation measure the Federal Reserve officially targets. Understanding why this particular number carries such weight requires a brief look at how it works and what distinguishes it from the more widely cited Consumer Price Index (CPI).

Core PCE uses a broader, chain-weighted basket that adjusts for substitution effects as consumers shift spending patterns. It tends to run 20-30 basis points below CPI on an annual basis. The Fed targets 2% on this specific measure, which means Core PCE, not CPI, is the directly relevant input for any discussion of whether the Fed hikes, holds, or cuts.

The BEA’s PCE price index methodology uses a chain-weighted basket that adjusts for substitution effects, which is precisely why it captures consumer behavior shifts more dynamically than the fixed-weight CPI basket and why the Fed adopted it as its official inflation benchmark.

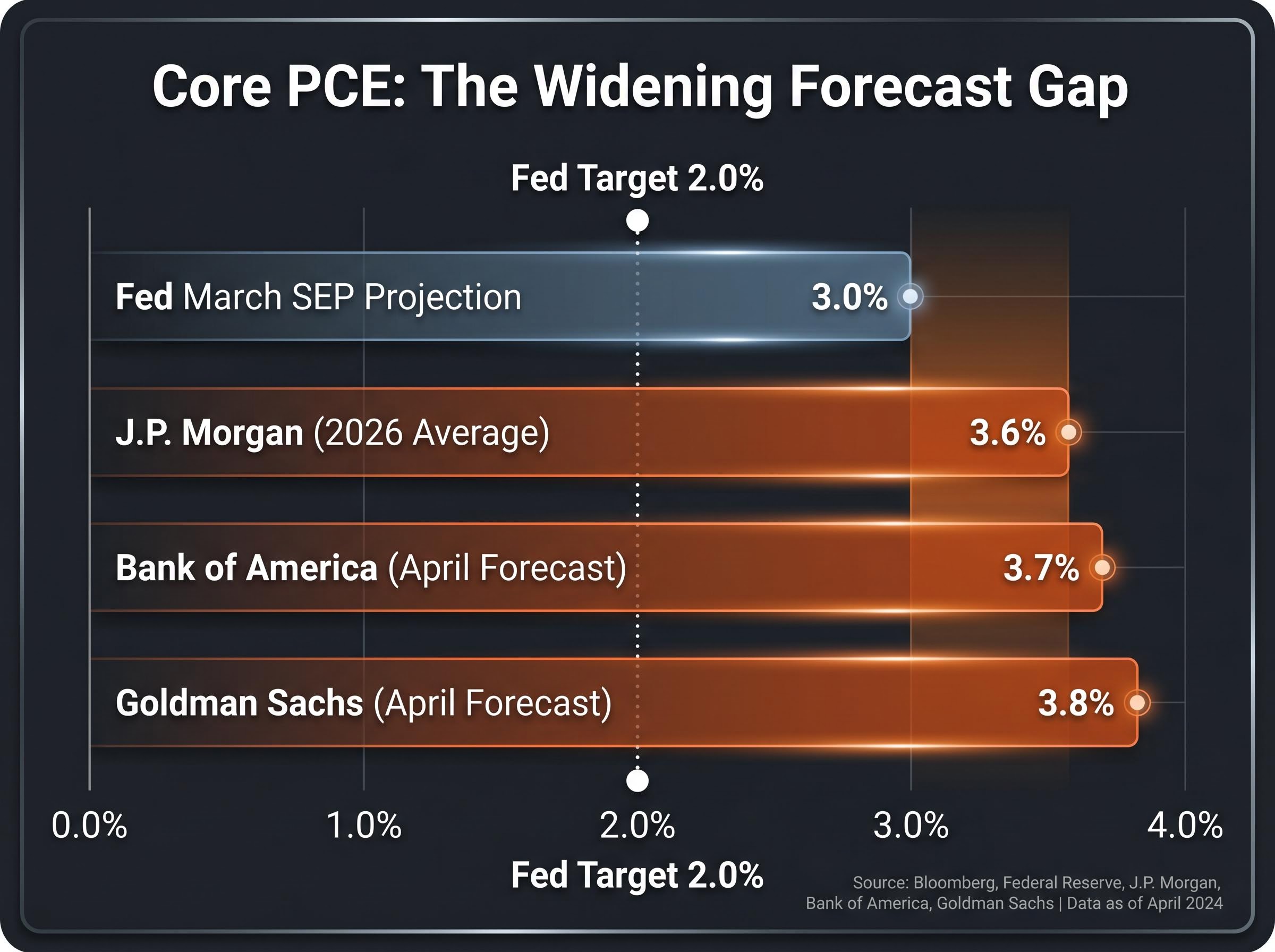

The April Core PCE release on 28 May arrives at a moment when the gap between the Fed’s own projections and private-sector forecasts has become uncomfortably wide. Goldman Sachs forecasts a 3.8% year-over-year reading. Bank of America expects 3.7%. Either figure would represent the highest annual print for core PCE since 2022.

The Fed’s own median projection from the March 2026 Summary of Economic Projections (SEP) targets 3.0% core PCE on a Q4/Q4 basis. A 3.8% reading before the year is even half over would put actual inflation running nearly 80 basis points above that projection, forcing a public reassessment of whether the rate-cutting cycle was premature.

J.P. Morgan projects a full-year 2026 average of 3.6%, with risk that a firmer-than-expected services component keeps core PCE in a 3.5-4% range into 2027.

| Institution | April 2026 Core PCE Y/Y Forecast | Year-End 2026 Forecast | Key Risk |

|---|---|---|---|

| Fed (March SEP) | N/A | 3.0% (Q4/Q4) | Projection increasingly detached from incoming data |

| Goldman Sachs | 3.8% | 3.3% (base case) | Non-trivial chance core PCE ends 2026 closer to 3.5% |

| J.P. Morgan | N/A | 3.2-3.3% (Q4) | Services component could keep core in 3.5-4% range into 2027 |

| Bank of America | 3.7% | 3.4-3.6% range | Sticky inflation keeps Fed constrained through year-end |

The shift toward hike pricing is not just a market phenomenon. Four senior Fed officials have articulated specific, quantitative conditions under which they would support reversing the easing delivered in 2024 and 2025. Their statements convert a vague sense of hawkishness into measurable goalposts.

Governor Christopher Waller, speaking at the Federal Reserve Bank of Dallas on 7 April 2026, was the most explicit:

“If core PCE were to level out around 3.5 to 4 percent and show no sign of moving lower over several months, I would see a strong case for at least reversing part of last year’s cuts.”

Waller identified three specific conditions: core PCE stalling or re-accelerating above the Fed’s forecast path, long-term inflation expectations drifting higher, and no meaningful deterioration in unemployment. The first condition is already being approached.

Chair Jerome Powell, at the 18 March 2026 press conference, framed his threshold as inflation “proving more persistent and moving materially above our projection path,” accompanied by an uptick in inflation expectations. Cleveland Fed President Loretta Mester told Bloomberg on 10 April that she would be “open to reversing some of the easing” if a “string of higher readings” called into question whether a sustainable path back to 2% remained intact. New York Fed President John Williams stated on 2 May that “additional policy firming would be on the table” if inflation proved more persistent than expected and the labour market remained strong.

Private-sector economists have attempted to quantify these thresholds. Goldman Sachs outlined three requirements for a pivot:

J.P. Morgan framed the threshold as “a 3-4 month run of 0.3-0.4% month-over-month core PCE prints combined with resilient payrolls.” Investors can now monitor these specific inputs in real time rather than waiting for Fed guidance to shift.

The nomination of Kevin Warsh as the next Federal Reserve Chair introduces a policy variable that compounds the data-driven case for a hike. His stated positions are a matter of public record, not speculation, and they represent a directional shift from the approach that delivered the 2024-2025 easing cycle.

The Warsh confirmation and balance sheet mandate arrived together: the 54-45 Senate vote that installed him also ratified an explicit pledge to accelerate quantitative tightening, a commitment that carries independent upward pressure on long-term Treasury yields beyond whatever the FOMC decides on the funds rate itself.

In prepared testimony before the Senate Banking Committee on 6 May 2026, Warsh stated:

“If the data show that inflation is not moving convincingly toward 2 percent, I would not hesitate to support additional policy firming, even if that proves unpopular.”

In a November 2025 Wall Street Journal op-ed, he warned against “premature declarations of victory” on inflation, arguing: “The lesson of the 1970s is that the central bank must err on the side of toughness when inflation remains elevated.” The Financial Times reported that investors see Warsh as “likely to prioritize returning inflation to 2 per cent, even if that means higher-for-longer or reversing cuts.” Bloomberg noted that traders interpret his comments as signalling “a lower tolerance for inflation overshoots.”

NBER research on go-stop monetary policy documents how the Federal Reserve’s cyclical pattern of stimulus followed by aggressive tightening in the 1970s repeatedly unanchored inflation expectations, a historical episode Warsh himself cited as a cautionary example in his November 2025 op-ed.

A mid-cycle return to hikes would be historically unprecedented for the Fed. Such a move under a new Chair would intensify both the policy signal and the institutional scrutiny.

Market confidence in the Fed’s independence affects inflation expectations, which are themselves one of the hike triggers Waller identified. A perception that political pressure could influence tightening decisions would risk unanchoring those expectations.

Warsh addressed this directly in his 6 May testimony: “I will resist any effort to use monetary policy for short-term political gain.” The statement appears designed to pre-empt concerns that his nomination carries political strings, a signal that, if credible, supports the Fed’s ability to act on the data without external constraint.

The repricing from cuts to hikes has triggered measurable shifts in institutional positioning across both fixed income and equities. The broad direction is consistent; the nuances are where the framework becomes useful.

On the fixed income side, Goldman Sachs recommends underweighting duration, particularly in the 5-10 year sector, favouring shorter-maturity investment-grade corporates and floating-rate instruments. J.P. Morgan advises neutral to slightly short duration with a preference for agency mortgage-backed securities (MBS) and front-end investment-grade credit. BlackRock is underweighting long-term government bonds and preferring short-term paper.

The logic connecting these positions to hike risk is straightforward: longer-duration bonds lose more value when yields rise, and the probability of further tightening makes the long end of the curve the highest-risk segment of a fixed income portfolio.

On the equity side, the tilt is toward value over growth, financials over rate-sensitive sectors. Morgan Stanley warns of continued pressure on long-duration growth stocks if core PCE remains near 4%, overweighting quality value, financials, energy, and select industrials. Bank of America favours banks and insurers that benefit from higher yields, alongside dividend-paying defensives. J.P. Morgan employs a barbell between short-duration value and cyclicals on one side and select quality growth with strong earnings on the other.

| Institution | Fixed Income Stance | Equity Stance | Key Avoid |

|---|---|---|---|

| Goldman Sachs | Underweight duration; favour short IG and floating rate | N/A | 5-10 year Treasurys |

| J.P. Morgan | Neutral to short duration; agency MBS, front-end IG | Barbell: value/cyclicals and select quality growth | REITs, leveraged small caps |

| BlackRock | Underweight long government bonds; prefer short-term paper | N/A | Long-dated Treasurys |

| Morgan Stanley | N/A | Overweight quality value, financials, energy, industrials | Long-duration growth, unprofitable tech |

| Bank of America | N/A | Overweight value, banks, insurers, dividend defensives | Rate-sensitive sectors |

Sectors explicitly flagged as underweights or risks across these frameworks include:

A Fed that eased aggressively in 2024-2025 and then reversed to hikes within the same cycle would be doing something without modern precedent. That rarity is the reason the stakes feel elevated beyond just 25 basis points.

A rate hike in this context would communicate far more than a marginal adjustment to the funds rate. It would amount to an institutional acknowledgement that the timing of the easing cycle was misjudged, that inflation had not been subdued to the degree the projections assumed. That signal carries consequences for Fed credibility, inflation expectations, and the discount rate assumptions embedded across every asset class.

“The bar for the Fed to resume hikes is high but not insurmountable.” — J.P. Morgan Global Research, May 2026

The base case is not a hike. Goldman Sachs projects core PCE easing to 3.3% by December 2026 under a scenario with no additional tightening. The Fed’s own SEP median targets 3.0%. The 65-70% hike probability priced by markets reflects a risk-weighted assessment, not a consensus prediction that a hike will happen.

A single 3.8% core PCE print on 28 May does not trigger a hike. The Fed has made clear, through Waller’s “several months” framing and J.P. Morgan’s “3-4 month run” threshold, that a pattern is required before the Committee would act. June and July data carry equal weight in the probability calculus.

What Thursday’s release will resolve is whether the Fed’s 3.0% year-end projection remains a credible baseline. A print at or above 3.8% before the year is half over would make that target appear increasingly detached from the trajectory of actual data, sharpening the repricing that has already redefined the rate outlook.

Whether or not the Federal Reserve ultimately delivers a rate hike in 2026, the environment investors need to plan around has already shifted. Treasury yields at 4.45% on the 10-year, hike risk priced at 65-70%, and an incoming Fed Chair with an explicit anti-inflation record represent a durable change in the rate regime, not a temporary dislocation waiting to revert.

Treating the bond market as the primary policy lever rather than equity drawdowns reshapes how investors should interpret Washington’s next move: with CPI running from 2.9% in January to 3.8% in April and the Fed no longer able to use rate cuts as a circuit breaker, yield levels rather than index points are the input that most predictably triggers a policy response.

The positioning shifts across fixed income and equities documented above are not responses to a single data point. They are responses to a new regime in which the direction of the next policy move is genuinely uncertain for the first time since 2023.

Three data points will determine whether this regime intensifies or softens: the 28 May Core PCE release, the subsequent monthly inflation prints through the summer, and the first FOMC meeting under Warsh’s chairmanship. Each will either validate or challenge the probability calculus that has already reshaped portfolio construction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Core PCE (Personal Consumption Expenditures price index excluding food and energy) uses a broader, chain-weighted basket that adjusts for consumer substitution effects, and it typically runs 20-30 basis points below CPI. The Fed officially targets 2% on this specific measure, making it the directly relevant input for rate decisions.

According to Fed officials, a rate hike would require core PCE stalling at or above 3.5% year-over-year for several months with no sign of moving lower, unemployment remaining at or below 4%, and market-based inflation expectations moving decisively above 2.5%. Goldman Sachs and J.P. Morgan have outlined similar quantitative thresholds for a policy reversal.

As of 23 May 2026, CME FedWatch probabilities assign approximately 65-70% odds of at least one 25 basis point rate hike by the December 2026 FOMC meeting, a dramatic reversal from March when markets were pricing 50-75 basis points of cuts. The shift has been driven by sticky core inflation, surging Treasury yields, and explicit hawkish signals from multiple Fed officials.

Major institutions recommend underweighting long-duration bonds and favouring shorter-maturity investment-grade credit and floating-rate instruments in fixed income. On the equity side, Goldman Sachs, Morgan Stanley, and Bank of America tilt toward value, financials, energy, and dividend-paying defensives, while avoiding REITs, highly leveraged small caps, and long-duration growth stocks.

Kevin Warsh was confirmed as the next Federal Reserve Chair in a 54-45 Senate vote and has publicly stated he would not hesitate to support additional policy tightening if inflation is not moving convincingly toward 2%. Analysts and traders interpret his track record and testimony as signalling a lower tolerance for inflation overshoots, adding a structural hawkish variable to the existing data-driven case for a rate hike.