The Australian Prudential Regulation Authority (APRA) oversees approximately $9.8 trillion in assets held on behalf of depositors, policyholders, and superannuation members. Its System Risk Outlook, published on 21 May 2026, rates the financial system as resilient, well-capitalised, and prepared to absorb severe adverse scenarios. That assessment is credible. It is also incomplete in ways that matter.

Two externally driven forces sit at the edge of APRA’s domestic stress-testing framework: geopolitical instability spanning the Middle East and US-China rivalry, and early stress signals in a US$2.3 trillion global private credit market that regulators across four continents have flagged independently. Neither threat originates in Australia. Both reach Australian institutions through indirect, cross-border channels that are harder to see on a balance sheet and easier to underestimate. This article maps the specific transmission pathways through which these risks could arrive, drawing on APRA’s own assessment alongside intelligence from the Financial Stability Board (FSB), the International Monetary Fund (IMF), the Bank for International Settlements (BIS), and the Reserve Bank of Australia (RBA).

A $9.8 trillion system that is resilient, but not immune

APRA’s regulatory remit spans the breadth of Australia’s financial sector. The entities under its supervision include:

- Authorised deposit-taking institutions (banks and mutuals)

- General insurers and reinsurers

- Life insurers and friendly societies

- Private health insurers

- Superannuation trustees

APRA Chair John Lonsdale has characterised the system as adequately prepared to absorb severe adverse scenarios. Capital buffers across the banking sector sit above regulatory minimums, and APRA has sharpened its supervisory intensity, elevating risk management expectations across regulated entities.

APRA’s System Risk Outlook, released on 21 May 2026, rates the Australian financial system as resilient and well-capitalised while explicitly naming geopolitical instability and offshore private credit developments as evolving risk factors that domestic stress-testing frameworks were not originally designed to capture in full.

What “resilient” means in APRA’s terms

APRA’s stress tests probe the system against severe yet plausible scenarios: a major global downturn paired with elevated funding costs and operational disruption. These exercises are designed to measure domestic shock absorption, the capacity of Australian institutions to withstand losses and continue operating.

What they are not designed to capture, at least not fully, is cross-border contagion. The distinction matters. A system can hold ample capital against domestic loan losses while remaining exposed to external forces that operate through global funding markets, commodity channels, and institutional investment linkages. The May 2026 report acknowledges this gap explicitly.

When big ASX news breaks, our subscribers know first

How geopolitical instability reaches Australian bank balance sheets

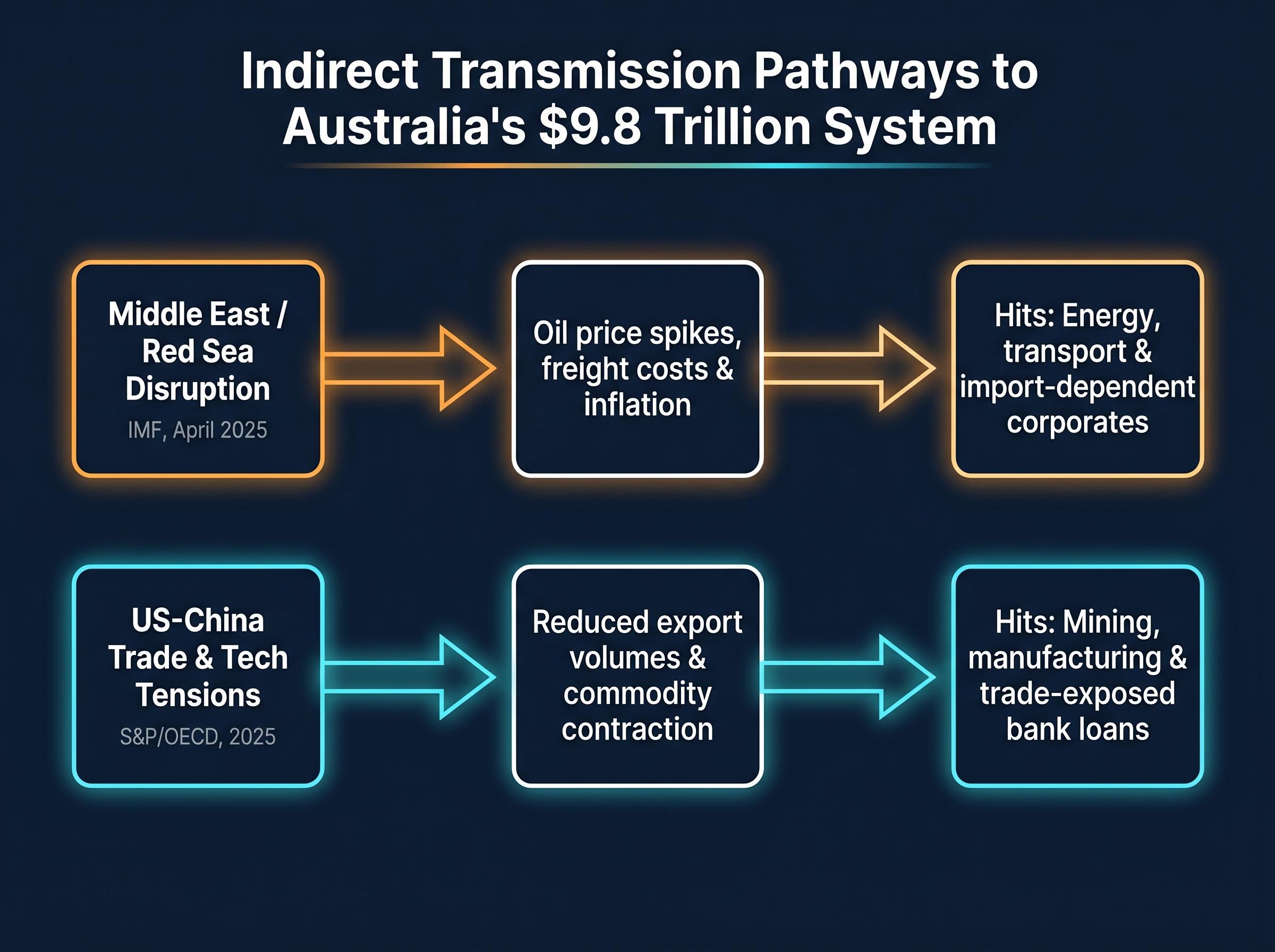

Australian banks do not lend materially into conflict zones. The transmission pathway is indirect, which makes it no less consequential. Two geopolitical flashpoints dominate the international regulatory agenda: Middle East conflict, including Red Sea shipping disruption, and the intensifying US-China technology and trade rivalry.

The IMF’s World Economic Outlook (April 2025) identifies Red Sea shipping disruptions as a risk to global trade and supply chains, with potential oil price spikes affecting inflation and financial conditions. The OECD’s Economic Outlook (May 2025) warns that new or higher tariffs between major trading blocs could significantly reduce Asia-Pacific export volumes, pressuring corporate earnings and asset quality in export-oriented banking systems.

For Australia, the primary macro-transmission channel runs through China. S&P Global Ratings noted in February 2025 that trade-related shocks via China and commodity markets represent the major pathway, with second-round effects flowing through loan quality in mining, energy, and related corporate sectors. ANZ Chief Economist Richard Yetsenga told the Australian Financial Review in March 2025 that geopolitical tensions and trade fragmentation are now the biggest external risks to Australia’s growth outlook.

Viktor Shvets, Head of Global and Asia-Pacific Strategy at Macquarie, argued in the AFR in May 2025 that equity markets underprice the risk that a sharp escalation could trigger global risk-off episodes, raising wholesale funding costs for Australian banks.

| Geopolitical flashpoint | Transmission channel | Australian sector affected | Key source |

|---|---|---|---|

| Middle East / Red Sea disruption | Oil price spikes, freight costs, inflation pass-through | Energy, transport, import-dependent corporates | IMF World Economic Outlook, April 2025 |

| US-China trade and technology tensions | Reduced export volumes via China, commodity demand contraction | Mining, manufacturing, bank loan books tied to trade-exposed sectors | S&P Global Ratings, February 2025; OECD, May 2025 |

Understanding that geopolitical risk reaches Australian banks through funding costs and commodity-linked loan quality, rather than direct conflict exposure, helps readers interpret bank earnings and stress-test results with greater precision.

The gap between headline severity and market reaction reflects how equity markets process geopolitical risk and market pricing as probability-adjusted inputs to forward earnings rather than proportional shocks, a distinction that helps explain why Australian bank share prices can remain stable even as the macro transmission channels described here are actively building.

The global private credit market and the leverage hidden inside it

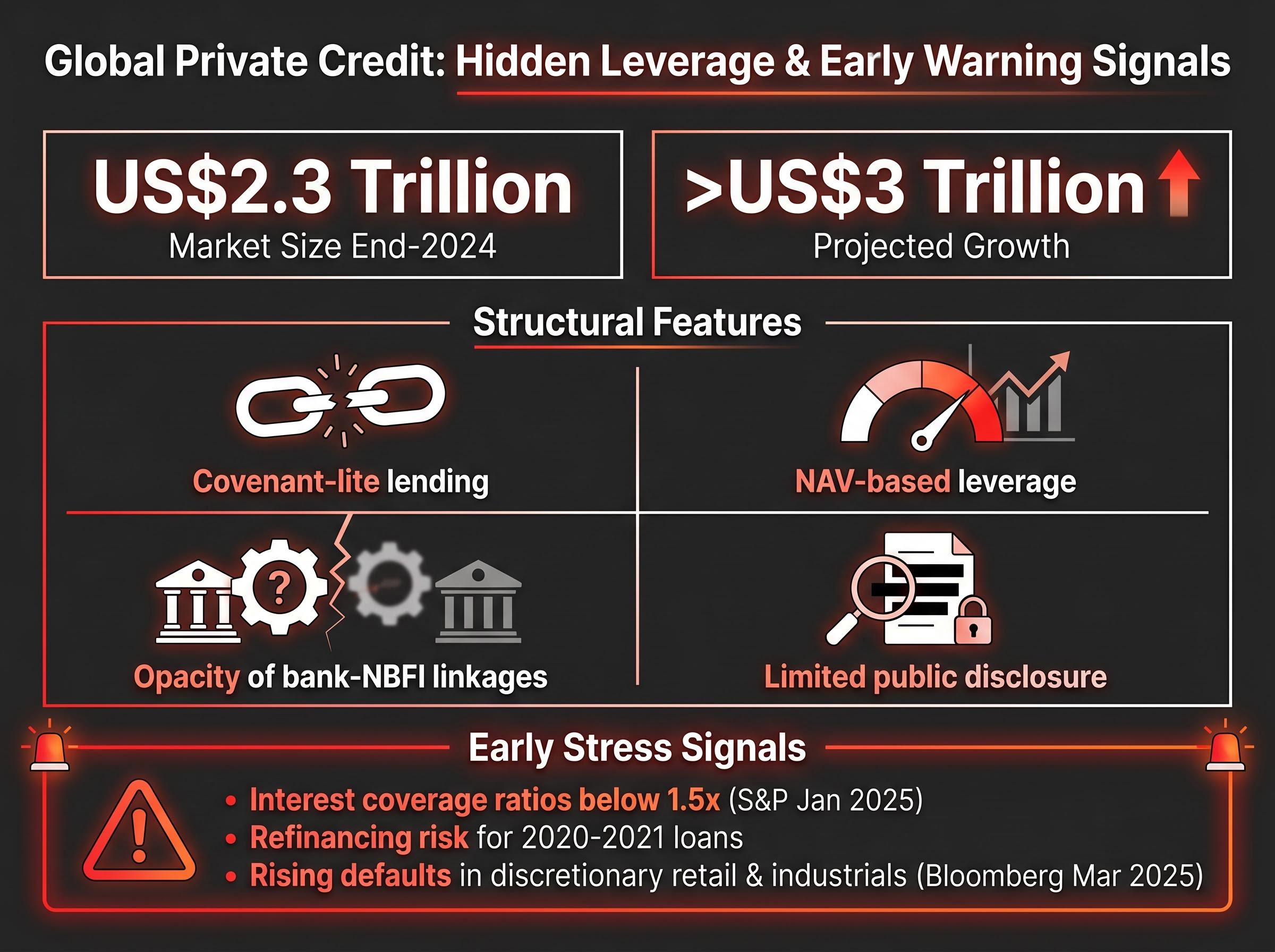

Global private credit assets under management reached approximately US$2.3 trillion by end-2024, according to Preqin data cited by the Financial Times in April 2025. BlackRock projected the market could exceed US$3 trillion within a few years, per Bloomberg reporting in February 2025. The growth trajectory reflects a structural shift: as banks have retreated from certain lending categories under tighter post-crisis regulation, non-bank lenders have expanded to fill the gap.

The FSB, in its Global Non-Bank Financial Intermediation Monitoring Report published in March 2025, described private credit as one of the fastest-growing segments of non-bank credit globally.

The FSB’s private credit vulnerability assessment, published in May 2026, identifies rapid growth in private credit assets, opacity in interconnections between private credit funds and banks, and challenges in data collection as compounding structural concerns, reinforcing the difficulty any single national regulator faces in quantifying exposures that originate offshore.

The FSB flagged “hidden leverage,” weaker creditor protections, and significant data gaps, alongside opacity in the interconnections between private credit funds and traditional banks and insurers.

Four structural features concentrate the concern:

- Covenant-lite lending: Borrower protections have weakened, reducing early warning triggers for lenders when portfolio companies deteriorate

- NAV-based leverage: Funds borrow against portfolio net asset value, amplifying losses in a downturn when valuations decline

- Opacity of bank-NBFI linkages: Warehousing lines, fund financing, and syndication connect private credit funds to banks in ways that are difficult to quantify from public data

- Limited public disclosure: Complex fund structures obscure leverage, liquidity terms, and risk concentrations

Early stress signals are visible. S&P Global Ratings observed in January 2025 a rising share of interest coverage ratios below 1.5x among leveraged borrowers, alongside growing refinancing risk for loans originated in 2020-2021 as maturities approach. Bloomberg reported in March 2025 an uptick in defaults and distressed restructurings among smaller sponsor-backed firms, with weaknesses appearing first in cyclical sectors including discretionary retail and some industrials. Loss rates remain low but are rising.

US leveraged loan defaults are accelerating faster than headline credit spreads suggest, with Proskauer’s Private Credit Default Index reaching 2.73% in Q1 2026 and Fitch projecting a 4.5-5.0% rate for leveraged loans across the full year, a deterioration that feeds directly into the refinancing pressure and rising loss rates that international regulators have flagged as early stress indicators.

Private credit, in its simplest form, refers to loans made by investment funds rather than banks. These loans are not traded on public markets, which means they lack the daily pricing transparency of listed bonds or equities. For most retail investors, this market is largely invisible, yet it now represents a significant share of corporate lending globally.

The cross-border channels connecting offshore private credit to Australian institutions

Australian superannuation funds represent the primary domestic link to global private credit markets. AustralianSuper, the country’s largest fund, has been expanding its private credit portfolio with a focus on offshore transactions in North America and Europe, targeting tens of billions of dollars over the medium term according to the Australian Financial Review in February 2025.

Nik Kemp, Head of Private Credit at AustralianSuper, noted the fund is “very mindful” of late-cycle risks and higher leverage in some segments, and has been tightening risk criteria.

That caution signals awareness of the timing risk. The expansion into US and European mid-market corporate loans comes at a point in the credit cycle where refinancing pressure and rising defaults are beginning to surface in precisely those markets.

The RBA’s Financial Stability Review (October 2025) acknowledged that while Australian banks have only limited direct exposure to private credit, superannuation funds and other institutional investors are increasing allocations. Global private market stress could affect Australia through valuation losses and weaker funding markets, even where domestic private credit positions remain small.

Why bank funding costs are the second channel

A separate contagion pathway runs through wholesale funding markets. If widespread private credit stress triggered broader risk-off conditions globally, Australian banks could face higher funding costs regardless of their direct private credit exposure.

The BIS Quarterly Review (March 2025) identified potential spill-overs to banks via credit lines, derivatives exposures, and common asset holdings with non-bank lenders. The Bank of England’s Financial Policy Committee found evidence in June 2025 of increased fund-level leverage in some private credit strategies, with subscription lines to private credit funds identified as an indirect contagion channel. Superannuation is the savings vehicle for most Australian workers. Understanding these linkages connects an abstract global risk to concrete retirement savings implications.

The next major ASX story will hit our subscribers first

What international regulators are watching, and what Australia’s own watchdogs are doing

The regulatory response to private credit risk is coordinated in concern but fragmented in jurisdiction. Multiple international bodies have flagged overlapping vulnerabilities since early 2025.

| Regulator | Key report / date | Core concern | Gap identified |

|---|---|---|---|

| FSB | NBFI Monitoring Report, March 2025 | Hidden leverage, weaker covenants, bank-NBFI opacity | Significant data gaps across private credit |

| IMF | GFSR, April 2025 | Non-linear losses from concentrated sector and sponsor exposures | Limited public disclosure obscures leverage |

| FSOC (US) | Annual Report, April 2025 | Private credit as systemic vulnerability | Limited public data on leverage and liquidity terms |

| BIS | Quarterly Review, March 2025 | Spill-overs to banks via credit lines and common holdings | Limited transparency in non-bank credit |

| APRA | System Risk Outlook, May 2026 | Offshore private credit risks increasing; multiple indirect linkages | Remit covers domestic institutions, not source of offshore risk |

APRA’s response posture combines three elements:

- Sharpened supervisory intensity across regulated entities

- Elevated expectations for risk management, particularly around external shock preparedness

- Ongoing evaluation of how regulated entities are affected by overseas developments

The acknowledged limitation is structural. APRA’s remit is prudential regulation of domestic institutions. It does not have direct oversight of the global private credit funds or geopolitical developments that represent the transmission source. The next System Risk Outlook is expected toward end of 2026, signalling an ongoing and iterative monitoring cycle.

AI vendor concentration and frontier AI-enabled cyber threats represent a third category of externally-originating systemic risks that APRA formally identified in its 30 April 2026 letter, sharing the same structural feature as geopolitical and private credit contagion: the source lies outside Australia’s domestic regulatory perimeter, and no individual institution can fully resolve the vulnerability through internal compliance alone.

The resilience that matters most is the kind you can test before the shock arrives

The two threat vectors traced through this analysis, geopolitical instability and private credit contagion, share a structural characteristic. Both operate through indirection, opacity, and cross-border channels that standard domestic stress tests were not originally designed to capture. The system’s capital buffers address the known; these risks live in the spaces between what is known and what is visible.

APRA’s May 2026 report carries a constructive signal: it names these risks explicitly. Identifying a threat is the prerequisite for managing it. The IMF and BIS have called for enhanced monitoring of bank-NBFI linkages and improved data disclosure as structural remedies across jurisdictions. Whether those calls translate into actionable transparency before conditions change remains an open question.

APRA characterised the current environment as one of “elevated uncertainty” in its May 2026 System Risk Outlook.

For readers monitoring the health of Australia’s financial system, the key variables to watch are not the capital ratios published in bank earnings. Those remain strong. The variables that matter sit further upstream: APRA’s ongoing monitoring cycle, the pace of international regulatory coordination on private credit data gaps, and whether the indirect channels mapped here remain stable or begin to transmit pressure.

For investors wanting to translate this risk mapping into concrete portfolio positioning, our comprehensive walkthrough of geopolitical portfolio resilience covers gold allocation targets from Goldman Sachs and BlackRock, safe-haven asset frameworks, defence sector exposure mechanics, and a five-component resilience checklist designed to function before, during, and after a geopolitical shock materialises.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking regulatory assessments and market projections are subject to change based on evolving geopolitical and financial conditions.