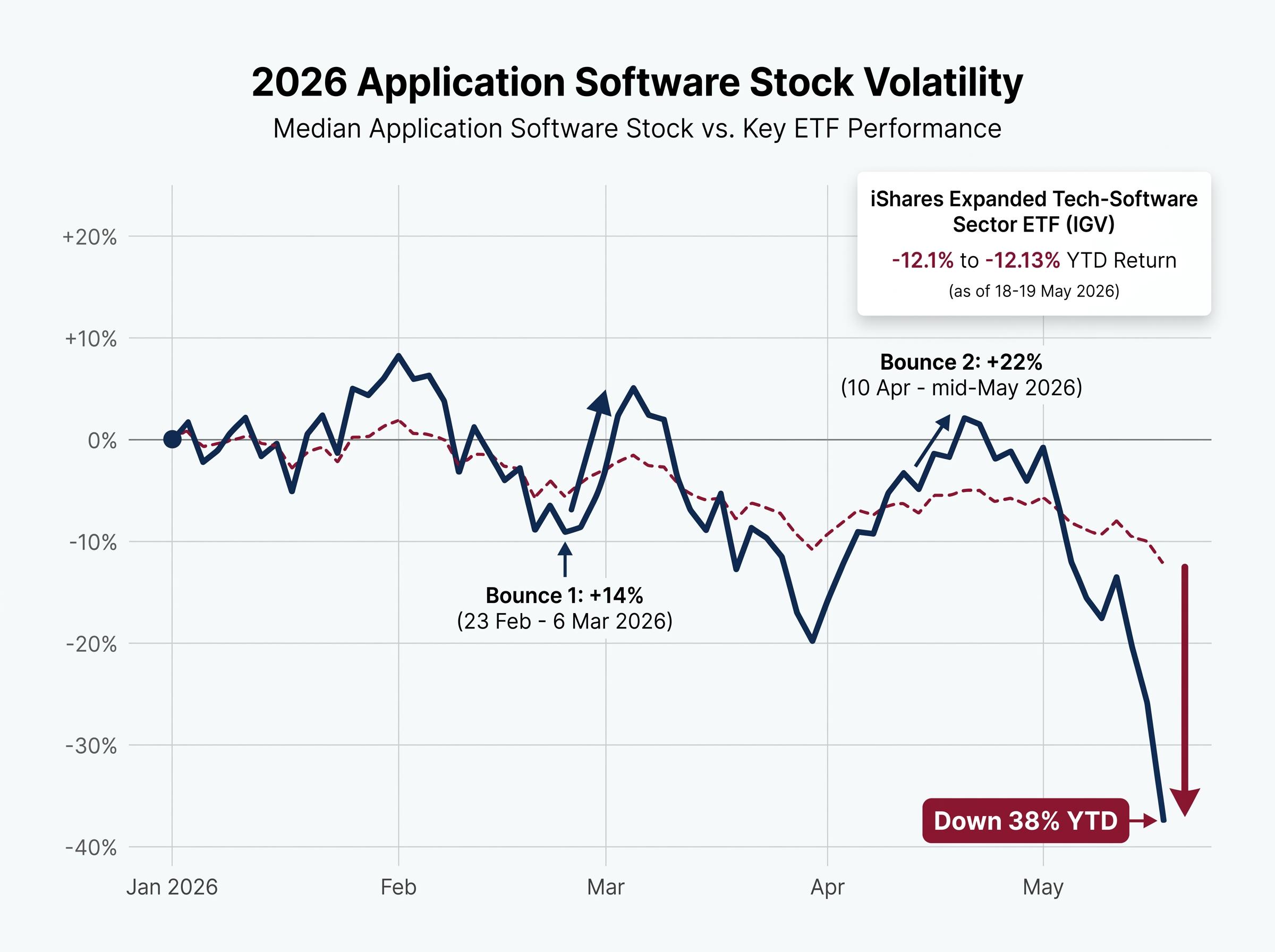

The median application software stock in Goldman Sachs’s coverage universe has fallen approximately 38% year-to-date in 2026. Two separate recoveries, one of 14% and one of 22%, have each faded without converting into a sustained rally. That pattern carries a specific message, and Goldman Sachs analyst Gabriela Borges spelled it out on 19 May 2026: meaningful AI-driven revenue outperformance across software companies is unlikely before 2027, with most firms signalling monetisation delays of 12 to 18 months beyond their current AI product launches. For investors holding software positions partly on the expectation that AI will accelerate growth in the near term, the implications are direct. What follows unpacks Goldman’s specific analytical argument, examines the additive versus cannibalistic revenue distinction at the centre of their thesis, and identifies which companies are being named as exceptions and why. The goal is a clearer framework for separating AI momentum stories from AI fundamental stories within software holdings.

The pattern of short-lived software recoveries in 2026

The price action tells the story before any analyst note does. According to Goldman Sachs research reported by Investing.com on 19 May 2026, application software stocks have traced a consistent pattern this year:

- Year-to-date decline: The median application software stock in Goldman’s coverage universe has fallen approximately 38% in 2026

- First bounce: Approximately 14% recovery from 23 February to 6 March 2026

- Second bounce: Approximately 22% recovery from 10 April through mid-May 2026

Each rally coincided with moments when investors appeared to price in the possibility that AI monetisation was arriving sooner than expected. Each time, the evidence did not follow the enthusiasm.

The iShares Expanded Tech-Software Sector ETF (IGV), the primary benchmark for North American software stocks, posted a year-to-date total return of approximately -12.1% to -12.13% as of 18-19 May 2026. That figure is less severe than the median individual stock decline, reflecting the index’s heavier weighting toward mega-cap names with more resilient fundamentals.

The hardware and software divergence in 2026 illustrates the capital rotation dynamic operating beneath the surface of the software selloff: the Morningstar Global Semiconductor Equipment index gained 47.6% year-to-date while the Software Applications index fell 22.7%, a spread of more than 70 percentage points that reflects investors directing AI conviction toward infrastructure spend rather than waiting for software monetisation to materialise.

Goldman Sachs characterises the application software sector as likely to remain range-bound, implying neither a collapse nor a recovery as the base case in the near term.

That framing matters. It suggests the next bounce attempt should be treated with structural scepticism until the specific conditions discussed below change.

When big ASX news breaks, our subscribers know first

What Goldman Sachs is actually arguing: 2027, not 2026

Goldman’s thesis is not a vague caution about software stocks. It is a dated, mechanistic claim: meaningful AI-driven revenue outperformance across application software companies is a 2027 event, not a 2026 one.

The bridge between those two years is a specific figure. According to Borges’s analysis, multiple companies have publicly signalled AI monetisation timelines of 12 to 18 months beyond their current AI product launch dates. When a company launches an AI feature in early 2026, the revenue impact, if it materialises at all, is therefore a late 2027 or 2028 event for most vendors.

The 12 to 18 month monetisation delay is the mathematical mechanism behind Goldman’s 2027 timeline, not a general sense of caution, but a calculation drawn from company-level disclosure patterns.

Why “meaningful outperformance” is the precise standard

Goldman’s language deserves attention. The claim is not that software companies will generate zero AI revenue before 2027. It is that AI will not produce “meaningful outperformance,” meaning revenue growth that demonstrably lifts a company’s trajectory above what its existing software business would have delivered alone.

That distinction matters for how investors should interpret near-term AI disclosures. A company reporting AI attach rates or product launch milestones is not necessarily contradicting Goldman’s thesis. The question is whether those disclosures translate into incremental revenue at a scale that moves the growth number.

Bank of America and Morgan Stanley have offered qualitatively aligned commentary in 2025-2026 coverage, framing broad AI re-acceleration as a 2027-plus event for most application vendors.

Analysing AI Revenue: New Growth Versus Reallocated Spend

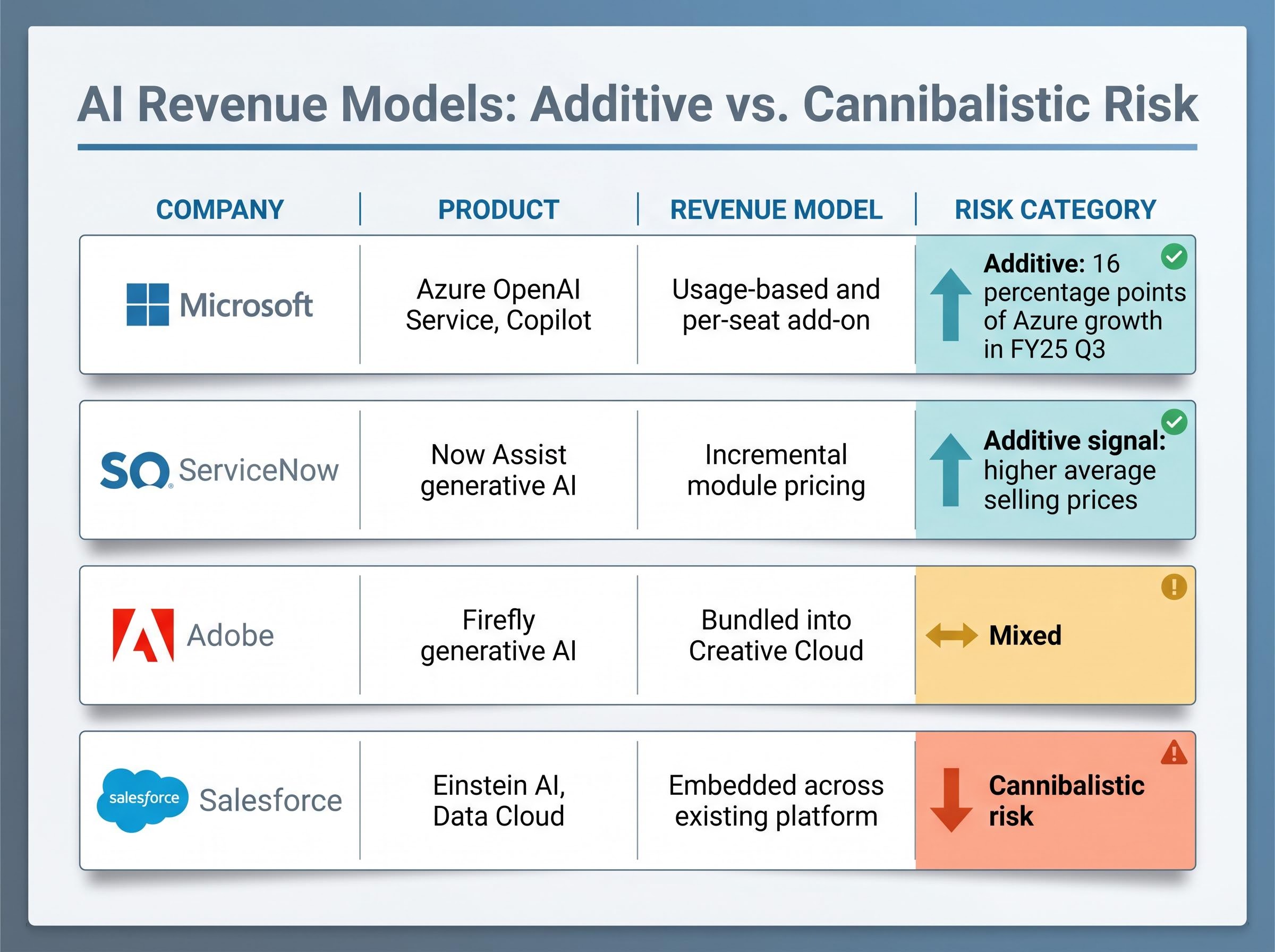

Goldman’s analytical standard is not whether a company is generating AI revenue. It is whether that revenue demonstrably lifts the overall growth trajectory. This is the additive versus cannibalistic distinction, and it is the most practical lens the analysis offers.

Additive AI revenue is revenue that expands total company growth beyond what existing software subscriptions would have generated on their own. It represents genuinely new spending by customers, not a relabelling of existing budgets.

Cannibalistic AI revenue is AI-labelled revenue that is simply redirected from existing software budgets. The customer receives more AI-enhanced functionality, but their total spend with the vendor remains flat or grows only marginally. The company’s headline growth rate does not change.

Reading earnings transcripts through Goldman’s lens

The following table maps how this distinction applies to specific companies based on their 2025-2026 public disclosures:

| Company | AI product example | Revenue model | Additive or cannibalistic risk |

|---|---|---|---|

| Microsoft | Azure OpenAI Service, Copilot | Usage-based and per-seat add-on | Additive: 16 percentage points of Azure growth attributed to AI in FY25 Q3 |

| ServiceNow | Now Assist generative AI modules | Incremental module pricing on enterprise deals | Additive signal: higher average selling prices when AI modules attached |

| Adobe | Firefly generative AI | Bundled into Creative Cloud; some usage-based enterprise | Mixed: bundled features risk cannibalistic; usage-based enterprise services could be additive |

| Salesforce | Einstein AI, Data Cloud | Embedded across existing platform | Cannibalistic risk: AI embedded into existing clouds may limit incremental revenue |

When reviewing software company AI disclosures, three questions clarify whether the revenue meets Goldman’s additive standard:

- Is this AI revenue net-new spend from customers, or a relabelling of existing budget allocations?

- Is the customer expanding their total spend with the vendor, or reallocating within a flat or declining budget?

- Is management providing a specific revenue ramp timeline with dollar figures, or only citing attach rates and qualitative differentiation?

If the answers are relabelled, flat, and qualitative only, the disclosure likely fails the additive test.

Why most software companies still fail the additive test in 2026

Across 2025-2026 earnings cycles, a consistent pattern has emerged. Most application software companies are disclosing AI progress in qualitative terms, attach rates, product differentiation, and pricing uplift language, without providing concrete AI-only revenue figures or specific monetisation timelines. The gap between narrative and quantification is precisely the evidence gap Goldman identifies.

Company by company, the disclosure posture looks remarkably similar:

- Salesforce: AI embedded across the platform with “multi-year” monetisation framing. No discrete AI revenue line item has been disclosed.

- Workday: AI described as embedded and largely non-separately priced into core subscriptions. No AI-specific revenue breakout provided.

- Adobe: Firefly features prominent in product marketing, but no separate AI-only revenue figure or run-rate has been disclosed despite the product’s visibility.

- Atlassian and HubSpot: AI positioned as a driver of product value and pricing power, but revenue reporting aggregates AI into overall subscription figures without separation.

The enterprise IT backdrop compounds the delay. Multiple vendors reported elongated deal cycles, SaaS seat optimisation, and budget consolidation through 2025-2026 earnings. When enterprise customers are scrutinising existing software spend and consolidating vendors, the conditions for net-new AI budget creation are harder to establish.

The legacy software repricing in early 2026, which erased an estimated $2 trillion in US software market value, set the structural backdrop for the specific disclosure gap Goldman identifies: capital had already rotated toward AI-native infrastructure models before most application software companies had produced quantified evidence that AI was lifting their own revenue trajectories.

The IGV ETF’s year-to-date decline is the investable expression of this sector-wide pressure, reflecting not just AI timing uncertainty but the accumulated weight of slower enterprise spending and compressed multiples.

The exceptions Goldman names and what separates them

Goldman’s thesis is not a blanket sell signal. It is a precision tool, and the bank names two companies whose AI disclosures already meet a higher evidential standard: Microsoft and ServiceNow.

What separates them is specificity. Where most software vendors offer qualitative AI commentary, these two have produced quantified evidence:

- Microsoft: CEO Satya Nadella stated in April 2025 that AI services contributed 16 percentage points to Azure’s year-over-year growth in FY25 Q3. That is a specific, quantified additive disclosure, the clearest in the sector.

- ServiceNow: Management reported that over 50% of new large deals in Q1 2025 included at least one generative AI product, and guided that generative AI could add a few points to subscription revenue growth. The higher average selling prices when AI modules are attached represent measurable deal-size uplift.

The Microsoft FY25 Q3 earnings results reported by financial news outlets confirmed that AI services contributed 16 percentage points to Azure’s year-over-year growth, the most precisely quantified additive AI revenue disclosure among major application software vendors as of mid-2026.

Goldman acknowledged incremental progress elsewhere, including leadership transitions at Klaviyo, Workday, and Adobe, and early-stage product refinements at ServiceNow and Salesforce. But the bank was explicit that these developments are not sufficient to change the sector-wide view.

Autodesk’s case illustrates how a proprietary data moat can shift an AI revenue story from qualitative to quantified: Bank of America cited a 60% adoption rate for AutoConstrain among eligible users as the first measurable proof that an AI feature was pulling through to user workflows, a disclosure standard closer to Goldman’s additive test than most enterprise software peers have managed.

Goldman Sachs noted that valuation alone is insufficient justification for purchasing software stocks, and that a newer cohort of value-oriented software investors still requires evidence of positive fundamental developments before adopting a constructive stance.

The message is direct: attractive multiples do not substitute for additive revenue evidence.

What AI software investing actually looks like between now and 2027

The 2027 timeline is not a reason to abandon software positions entirely. It is a framework for disciplined position management over the next 12 to 18 months, built around a specific question: what evidence would need to appear to shift the thesis earlier?

Goldman’s framework implies a concrete set of triggers. Investors monitoring upcoming earnings seasons should watch for:

- Additive AI revenue disclosed as a specific line item or quantified contribution to company-level growth, not simply an attach rate or pricing uplift figure

- Customer spending expansion alongside AI adoption, meaning total deal sizes are growing rather than existing budgets being reallocated toward AI-labelled features

- Management guidance that includes AI-specific revenue ramp timelines with dollar figures or percentage-point contributions, moving beyond qualitative commentary

- Enterprise IT spending stabilisation, which would remove the compounding headwind of budget consolidation that has delayed additive AI revenue recognition

Macro factors extend the patience required. Higher-for-longer interest rates continue to compress multiples on long-duration growth stocks. AI-native competitive threats, including the risk that hyperscalers capture a disproportionate share of AI value, weigh on the sector even where current fundamentals are solid. Regulatory and data privacy headwinds, cited in 2026 coverage from the Financial Times and Wall Street Journal, add execution risk.

BofA and Morgan Stanley qualitatively align with Goldman’s view that broad AI re-acceleration is a 2027-plus event. The consensus is not bearish in the sense of expecting a collapse. It is patient, expecting a protracted period where narrative runs ahead of revenue.

For investors who accept the 2027 thesis and want to reposition capital in the intervening period, our dedicated guide to AI infrastructure stock allocation outlines a structured three-layer framework across hardware, cloud, and software with specific allocation weights, and covers why Goldman Sachs projects $527 billion in hyperscaler capex in 2026 alone as the quantified evidence that infrastructure spend is real even where software monetisation is delayed.

Software stocks and AI: the question to ask before the next rally

The next software rally will arrive. The relevant question is whether it will be built on the same AI narrative optimism that powered and then failed the two 2026 bounces, or whether it will be underpinned by quantified additive revenue evidence.

Goldman Sachs’s framework gives investors a specific test: is AI revenue lifting total company growth above what the existing business would have delivered alone? As of mid-2026, most application software companies have not demonstrated this. Microsoft and ServiceNow have produced the closest approximations. The rest are still disclosing in qualitative terms.

2027 is not far. The companies that arrive there with demonstrated additive AI revenue will occupy a fundamentally different investment profile from those that spent the intervening period bundling AI features into flat-priced subscriptions. Separating those two groups now, rather than during the next sentiment-driven bounce, is where the analytical work pays off.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements reflect analyst opinions and forward-looking views that are subject to change based on market developments and company performance. Past performance does not guarantee future results.