BofA Double-Upgrades Intel to Buy With a $135 Street-High Target

1 hr ago

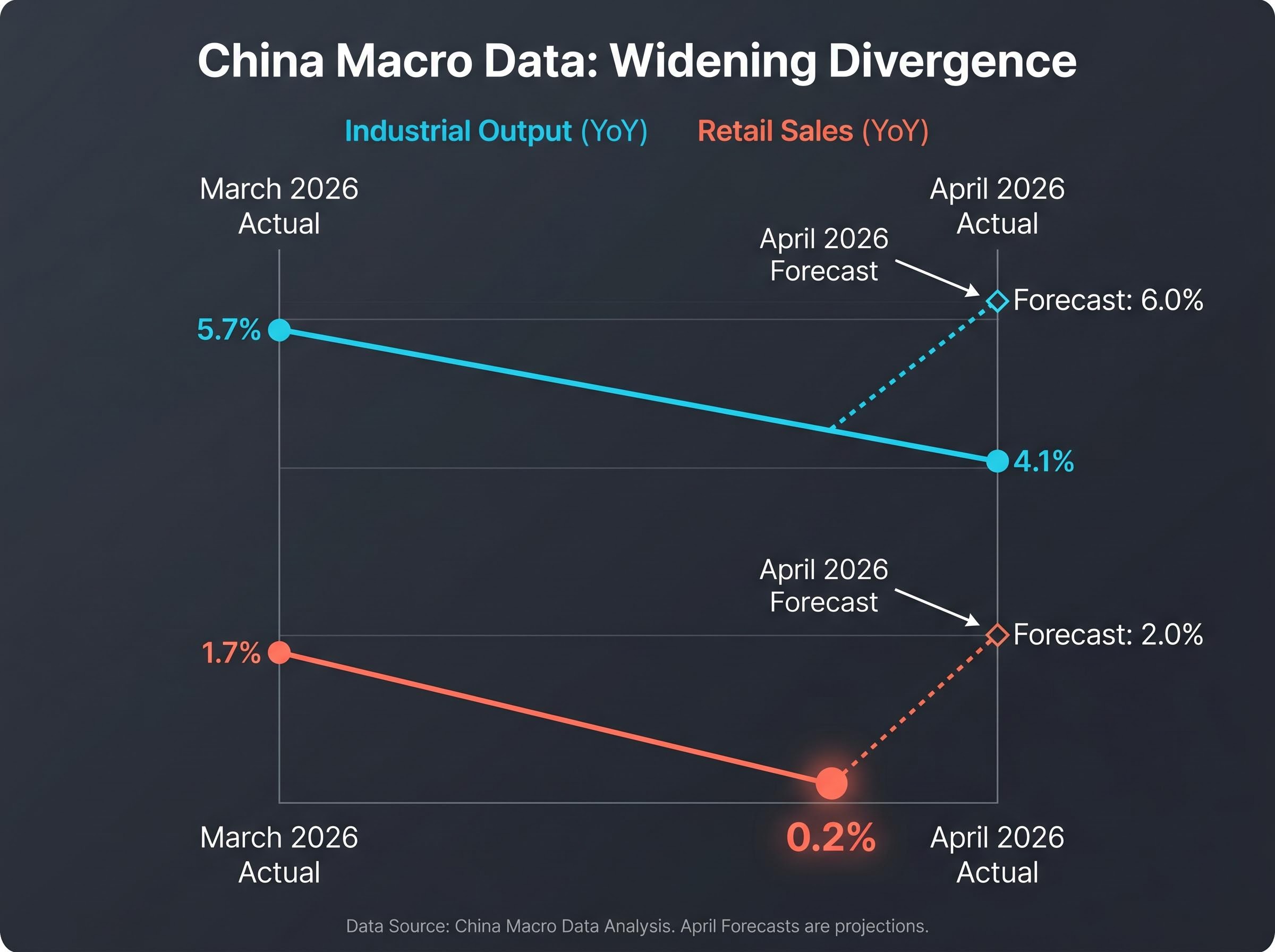

China’s April retail sales grew just 0.2% year on year while industrial output missed its 6.0% forecast by nearly two full percentage points. Yet South Korea’s KOSPI ended 18 May in the green while almost every other major Asian stock market index fell. The session was shaped by at least three distinct forces operating simultaneously: a China macro data miss, a company-specific labour standoff at Samsung Electronics, and oil above $100 per barrel tied to Middle East escalation. These forces are not equivalent in kind, origin, or duration. What follows uses the session’s divergences to illustrate a practical analytical distinction between systemic macro risk and idiosyncratic event risk, and why that distinction matters for interpreting market moves across the region.

The misses arrived in sequence, and the scale widened with each release. Chinese industrial output came in at approximately 6% year on year in April 2026, well below the 6.0% consensus forecast. Retail sales, the figure that speaks most directly to household demand, landed at just approximately 1.9% against a 2.0% expectation.

April retail sales: 0.2% year on year. Against a consensus forecast of 2.0%, the miss represents the starkest evidence yet that Chinese consumer demand is not participating in the recovery narrative.

The March context makes the trajectory harder to dismiss as a one-off. Industrial output decelerated from 5.7% in March to 4.1% in April. Retail sales slipped from 1.7% to 0.2%. Both readings moved in the wrong direction, but the consumption figures fell faster, widening the gap between what factories are producing and what households are buying.

The National Bureau of Statistics of China confirmed that April 2026 retail sales grew just 0.2% year on year and industrial output reached 4.1%, establishing the official baseline for a data set that has now disappointed across two consecutive months.

| Metric | March 2026 Actual | April 2026 Actual | April 2026 Forecast |

|---|---|---|---|

| Industrial Output (YoY) | 5.7% | 4.1% | 6.0% |

| Retail Sales (YoY) | 1.7% | 0.2% | 2.0% |

Analyst commentary from approximately 16 May 2026 characterised this pattern as a K-shaped divergence: production-side metrics running at multiples of consumption growth, a structural gap rather than a cyclical blip. The question is no longer whether April was disappointing. It is whether Beijing’s demand-side problem is solvable in the near term.

A K-shaped consumer recovery, where aggregate spending metrics look stable while lower-income households draw down finite savings to maintain basic expenditure, is not a pattern unique to China; the same structural divergence is visible in US retail data, where high-income spending has propped up headline figures while mass-market demand deteriorates.

The mechanism through which Chinese consumption weakness transmits across the region is direct. Asian economies including South Korea, Japan, and Southeast Asian export markets are structurally linked to Chinese household spending. When that spending stalls, the drag is not abstract; it flows through trade balances, corporate revenue lines, and tourism receipts.

Two competing recovery theses have framed investor positioning on Chinese exposure. The first, a production-led recovery, finds support in the data: industrial output, while decelerating, remains positive. The second, a domestic-demand-led recovery, does not. The multi-month trend visible across March and April 2026 shows consumption moving further from, not closer to, production-side strength.

Any regional recovery thesis anchored to Chinese consumer spending now faces meaningful headwinds until this structural gap closes.

The primary exposure clusters are concentrated in three areas:

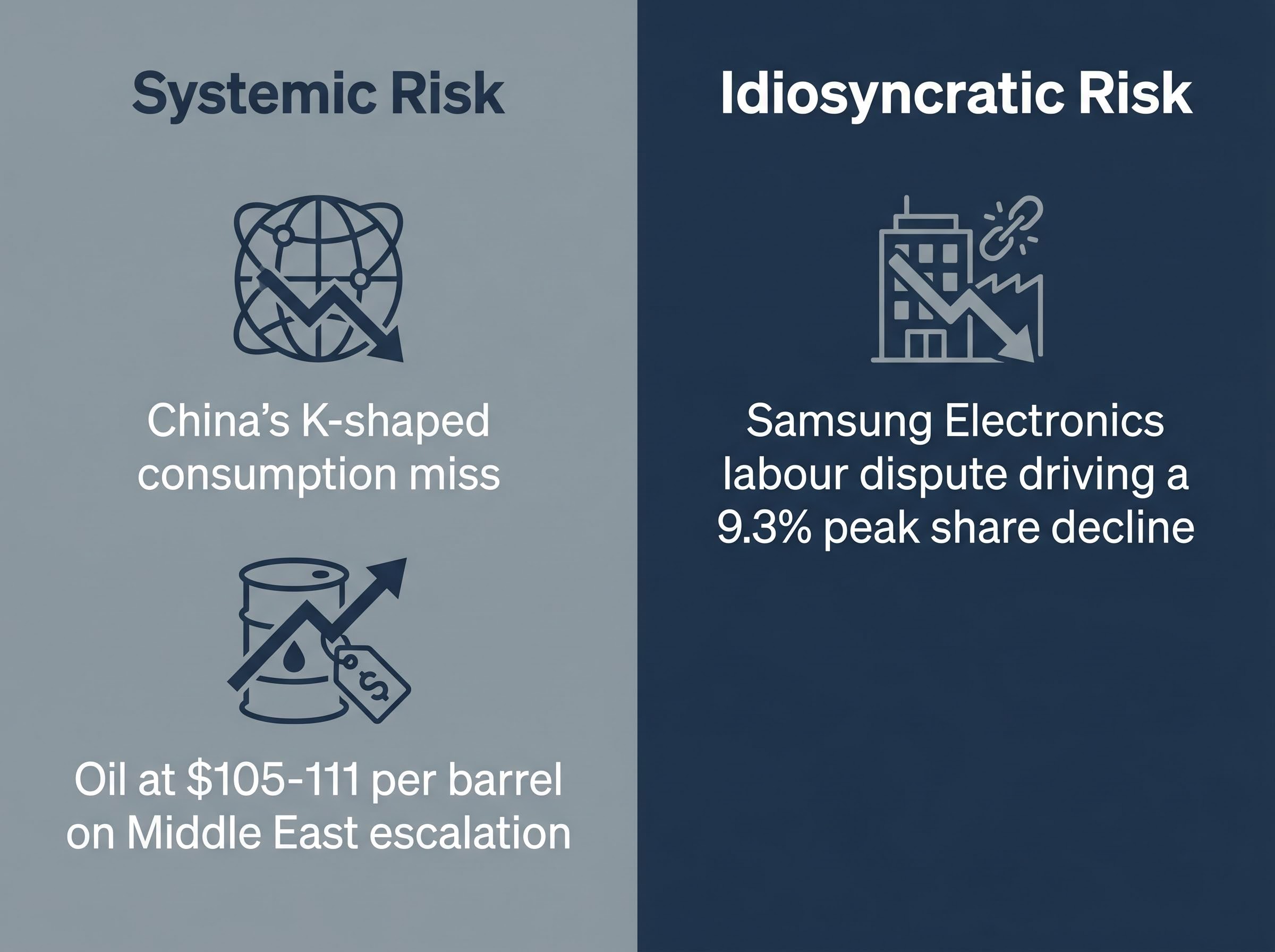

Systemic risk is a macro-level force that affects multiple markets or sectors simultaneously. It tends to be longer in duration and difficult to hedge at the individual-stock level. When Chinese consumption data disappoints across every category, or when oil prices climb above $100 per barrel on geopolitical escalation, the pressure is broad, simultaneous, and not resolved by avoiding any single name.

Idiosyncratic risk is company-specific or event-specific. It is discrete, potentially resolvable, and analytically separable from macro conditions. Samsung’s labour dispute, which drove a 9.3% share-price decline on strike concerns, is a case in point: the cause is a bonus-pay negotiation, not a regional economic deterioration.

| Risk Type | May 18 Example |

|---|---|

| Systemic | China’s K-shaped consumption miss; oil at $105-111 per barrel on Middle East escalation |

| Idiosyncratic | Samsung Electronics labour dispute driving a 9.3% peak share decline |

The KOSPI’s 0.2% gain against broad regional declines is the observable outcome produced by the intersection of these two categories. Without the framework, the divergence looks random. With it, the divergence is legible.

The dispute centres on a bonus-pay gap between Samsung workers and employees at rival chipmaker SK Hynix. Negotiations failed to produce an agreement, and the union has threatened an 18-day strike beginning 21 May 2026. The operational risk the market is pricing is not an abstract labour relations concern; it is the prospect of chip supply disruption at one of the world’s largest semiconductor manufacturers.

Samsung’s semiconductor position at the centre of the HBM memory upcycle, combined with unconfirmed Apple foundry discussions, drove an 11% single-session surge as recently as 6 May 2026, contextualising why a labour dispute capable of disrupting chip supply is treated by markets as an index-level event rather than a routine industrial relations matter.

Reuters reporting on the Samsung pay dispute confirms that government-mediated talks resumed on 18 May 2026 and that the union’s 18-day strike threat remains active if an agreement is not reached before the 21 May deadline.

Samsung’s 9.3% peak decline on strike concerns established the volatility range the market has assigned to this event, making the 21 May deadline the single most consequential date for KOSPI positioning this week.

The KOSPI edged up approximately 0.2% on the session, bucking the broader regional downtrend. That outperformance is directly attributable to Samsung’s rebound. A single large-cap name with heavy index weight decoupled a national market from a regional trend.

Oil prices connect to Asian equity sentiment through two channels. Elevated input costs compress margins across manufacturing-heavy economies. Simultaneously, inflation expectations generated by sustained crude prices above $100 limit central bank flexibility on rate cuts.

The economies most exposed to sustained oil above $100 per barrel as energy importers include:

The Hormuz oil risk premium embedded in current crude prices is not priced to resolve quickly; the IEA projects a two-year supply chain recovery timeline even under best-case resolution, and the near-total withdrawal of commercial war-risk insurance has effectively closed the Strait to standard traffic regardless of whether physical passage remains technically possible.

On 18 May, WTI futures rose approximately 2.22% to the $103-107 per barrel range. Brent climbed approximately 1.86% to $110-111 per barrel. The regional equity response was broad: the Nikkei 225 fell approximately 1%, the Hang Seng dropped approximately 1.7%, the ASX 200 declined approximately 1.6%, and the CSI 300 lost approximately 1%.

Nvidia’s Q1 FY2027 earnings, scheduled for after market close on 20 May 2026, represent the session’s binary catalyst. The Wall Street consensus EPS forecast stands at approximately $1.70, compared to $0.77 in the prior-year period, representing approximately 120% year-on-year earnings growth. Nvidia shares fell 4.42% on 18 May, adding to pre-earnings caution.

A beat could reinforce AI-theme positioning across the semiconductor and electronics supply chain. A miss would add another headwind to a region already under pressure.

| Date | Event | Market Implication |

|---|---|---|

| 20 May 2026 | Nvidia Q1 FY2027 earnings | AI rally bellwether; read-through for Asian tech sentiment |

| 21 May 2026 | Samsung union strike deadline | Chip supply disruption risk; KOSPI index weight impact |

| Ongoing | Oil above $100/barrel | Inflationary pressure on energy-importing Asian economies |

The positioning logic differs by risk category. Systemic risks, including China’s consumption trajectory and oil-driven inflation, are longer-duration forces that are difficult to hedge at the individual-stock level. The Samsung situation, by contrast, is event-driven: it has a deadline, a mediation process, and a resolution pathway.

The co-existence of both risk types within one session is itself a signal. Investors cannot hedge the macro by avoiding single stocks, and they cannot resolve the Samsung risk by repositioning on macro factors.

The Nvidia result on 20 May sits at the intersection: it is the event most likely to either stabilise or amplify tech-sector sentiment heading into the Samsung strike deadline on 21 May.

China’s consumption weakness is not resolved by Nvidia earnings or Samsung negotiations. It is the underlying condition against which this week’s events are playing out. The 0.2% retail sales figure is not a data point that resets next month; it is the latest reading in a multi-month pattern of deterioration.

Oil above $100 is similarly a macro condition rather than a discrete event. Its persistence compounds pressure on energy-importing Asian economies regardless of how near-term equity catalysts resolve.

The oil supply fundamentals driving prices above $100 are more structurally constrained than the headline WTI figure suggests: Saudi Arabia’s crude output collapsed to 6.316 million barrels per day in April 2026, its lowest since 1990, while global inventories are drawing at 8.5 million barrels per day, a rate the IEA sees no mechanism to rebalance before October 2026.

The KOSPI’s outperformance on 18 May is only surprising if all market-moving forces are treated as equivalent. Once Samsung’s idiosyncratic labour catalyst is separated from the systemic macro headwinds, the divergence is explicable. The index rose because its largest constituent rebounded on mediation news, not because South Korea was insulated from the regional pressures.

The week ahead is structured as a sequence of resolvable and unresolvable risks. Nvidia’s earnings on 20 May and Samsung’s strike deadline on 21 May are events with outcomes. China’s 0.2% retail sales growth and oil above $100 are conditions without expiry dates. Knowing which is which is the analytical starting point.

Whether the AI-demand thesis survives Nvidia’s result, and whether Samsung’s labour situation reaches resolution before the strike deadline, will determine whether this week is remembered as a consolidation or the start of a more sustained correction in Asian tech. The data, at minimum, argues for vigilance.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements regarding earnings expectations and market outcomes are speculative and subject to change based on market developments and company performance.

—

Systemic risk is a macro-level force that affects multiple markets or sectors simultaneously, such as China's consumption data miss or oil prices above $100 per barrel. Idiosyncratic risk is company-specific or event-specific, such as Samsung's labour dispute, which is discrete, potentially resolvable, and analytically separable from broader macro conditions.

The KOSPI edged up approximately 0.2% because Samsung Electronics, which carries heavy index weight, rebounded 3.97% after government-mediated talks resumed over its labour dispute, offsetting the regional headwinds from China's weak consumption data and elevated oil prices.

China's April retail sales grew just 0.2% year on year, well below the 2.0% forecast, signalling that Chinese household demand is stalling. Because South Korea, Japan, and Southeast Asian economies are structurally linked to Chinese consumer spending through trade, tourism, and exports, this weakness transmits directly across the region.

Samsung's union has threatened an 18-day strike beginning 21 May 2026 over a bonus-pay dispute, with government-mediated talks ongoing as of 18 May. If mediation fails, the prospect of chip supply disruption at one of the world's largest semiconductor manufacturers makes this deadline a key KOSPI index-level event.

Sustained oil prices above $100 per barrel raise input costs across manufacturing-heavy economies and limit central bank flexibility on rate cuts by stoking inflation expectations. Japan, South Korea, India, and most of Southeast Asia are major energy importers, making them particularly vulnerable to this commodity-driven pressure.