Technology stocks have generated roughly 85% of the S&P 500’s approximately 10% year-to-date gain as of 16 May 2026. The remaining 493 or so constituents have collectively contributed about 3%. That split, documented in Goldman Sachs research, reframes what looks like a strong broad market into something more specific: a concentrated bet on a narrow cluster of mega-cap names tied to the artificial intelligence investment cycle.

For retail investors whose primary equity exposure sits in a cap-weighted S&P 500 index fund or a 401(k) default allocation, the distinction between a broad advance and a narrow one carries direct portfolio consequences. Goldman Sachs has characterised the current environment as a single concentrated trade rather than a diversified market rally. JPMorgan, BlackRock, and Vanguard have each flagged the same structural risk from different angles.

This analysis unpacks what the concentration data means for a typical U.S. retail portfolio, explains why earnings revision quality is the filter Goldman uses to separate justified concentration from fragile concentration, and delivers a tiered diversification framework drawn from institutional sources, including Goldman’s specific call on Consumer Staples.

The S&P 500’s 10% gain is hiding a much narrower story

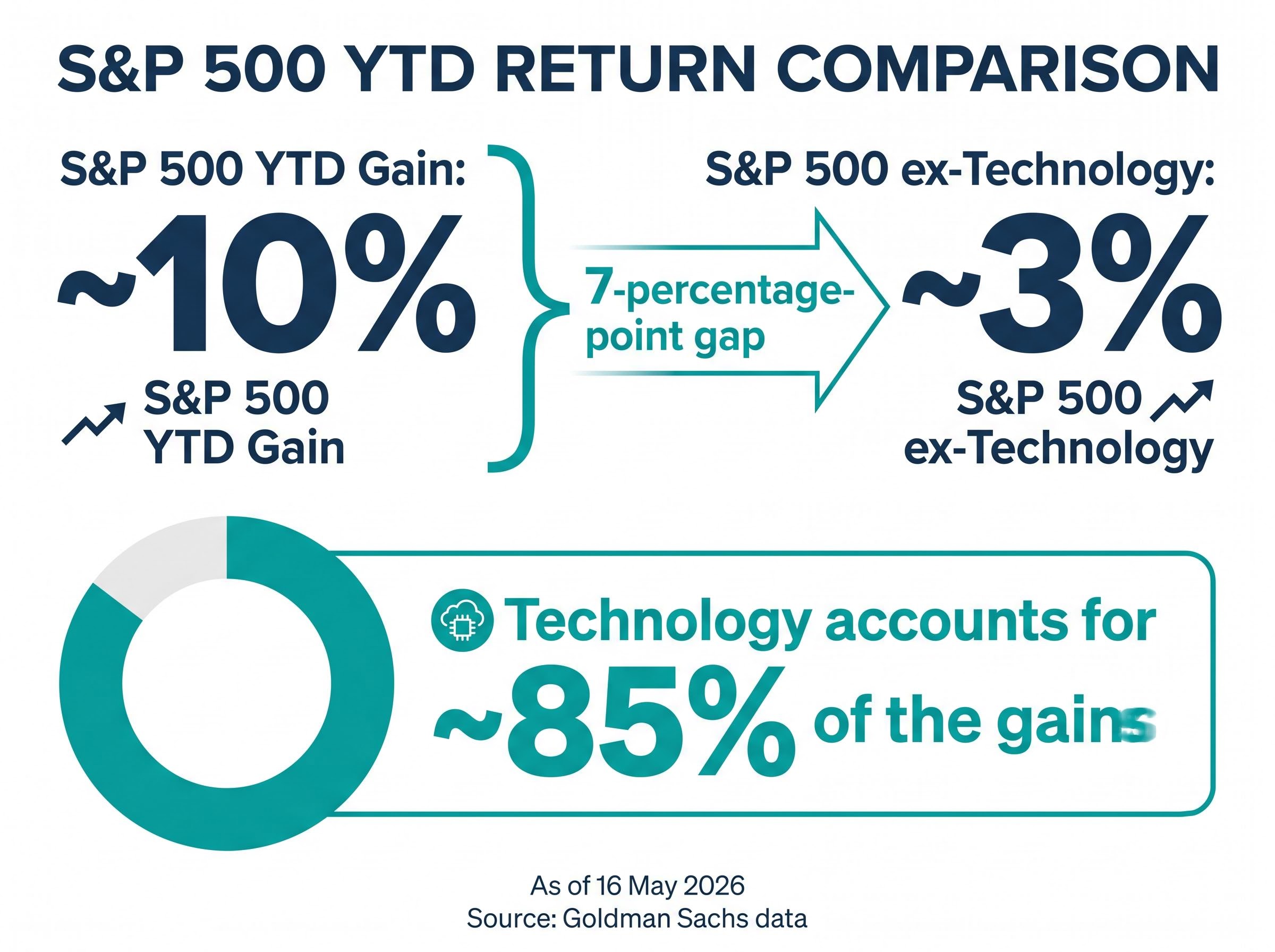

The index is up approximately 10% year-to-date. Strip out technology, and the S&P 500’s return drops to roughly 3%. That is not a rounding error; it is a seven-percentage-point gap between what the benchmark says the market is doing and what most of the market is actually doing.

| Measure | YTD Return (approx.) |

|---|---|

| S&P 500 (cap-weighted) | ~10% |

| S&P 500 ex-Technology | ~3% |

The index has set 14 new all-time highs in the prior one-month period alone, according to Goldman Sachs data. Record highs generate confidence. They do not, on their own, signal broad participation.

Current market concentration records place five companies at roughly 30% of total U.S. equity market capitalisation, a level that Wolfe Research and Goldman Sachs both describe as without modern historical precedent, exceeding even the dot-com peak that preceded a multi-year technology drawdown.

The defining statistic of the current market: Technology has accounted for roughly 85% of the S&P 500’s year-to-date gains, per Goldman Sachs, meaning the headline return is overwhelmingly a single-sector story.

An investor checking a portfolio dashboard sees a healthy 10% gain and may reasonably assume that 500 companies are sharing the load. The arithmetic says otherwise. Nearly all of that return traces back to names the investor is likely already overweight, and the cap-weighting mechanism ensures that overweight grows with every percentage point of further tech outperformance.

When big ASX news breaks, our subscribers know first

Why cap-weighted index funds make you more concentrated than you realise

Cap-weighting is a mechanical process. The larger a company’s market capitalisation, the greater its share of the fund. As a stock rises, the fund automatically allocates more capital to it, not because a portfolio manager made a decision, but because the index’s construction rules dictate it.

The result is a feedback loop that quietly reshapes a portfolio’s risk profile without any action from the investor:

- A stock that doubles in price roughly doubles its weight in the index, pulling more of the fund’s capital into a single name.

- When multiple mega-cap stocks in the same sector appreciate together, the sector’s share of the portfolio compounds.

- Gains from passive appreciation look identical to deliberate overweights in a portfolio summary, but they arrive without any corresponding risk assessment.

- Over a sustained run, a “diversified” 500-stock fund can behave like a concentrated bet on the five or ten largest names.

Cap-weighted concentration amplifies in both directions: the same five names that drove more than half of April 2026’s recovery were also responsible for roughly 70% of the market’s Q1 2026 decline, a dynamic that passive investors holding VOO or VTI absorbed without making any active portfolio decision.

JPMorgan’s February 2026 Monthly Market Review identified mega-cap U.S. technology concentration as a key portfolio risk, noting that the accumulation of “unintentional AI overweights” through passive appreciation represents one of the most underappreciated exposures in retail portfolios. JPMorgan’s Guide to the Markets (updated March 2026) charts top-10 stock concentration in the S&P 500 at historically elevated levels.

JPMorgan’s Guide to the Markets (updated March 2026) charts top-10 stock concentration in the S&P 500 at historically elevated levels, providing a quantitative baseline that reinforces why passive index exposure carries materially different risk today than it did in prior decades.

What this means if your core holding is an S&P 500 ETF

An investor whose primary equity exposure runs through VOO, VTI, or a 401(k) default index allocation is, without any active decision, running a significant bet on the continuation of the AI growth narrative. The position was not chosen. It was inherited through the mechanics of cap-weighting and compounded by the sector’s outperformance.

Goldman Sachs frames this as a structural feature, not a temporary distortion. The current environment is, in its characterisation, “a single concentrated trade rather than a diversified market.”

What earnings revision quality tells you that price momentum does not

The concentration itself is not Goldman’s primary concern. What matters, in Goldman’s framework, is whether the concentration is supported by improving fundamentals or sustained purely by price momentum and valuation expansion.

Goldman Sachs has characterised the current rally as differing from prior comparable episodes precisely because it is backed by earnings revisions, not just multiple expansion.

That distinction carries weight. Price momentum tells an investor that a stock has been going up. Earnings revision momentum tells a different story: that analysts with access to management guidance, order books, and supply chain data are independently raising their estimates of future profitability. One is a reflection of recent price action; the other is a forward-looking signal about business conditions.

The difference between the two matters most at inflection points:

- Price momentum can persist long after fundamentals deteriorate, driven by trend-following flows and retail enthusiasm.

- Earnings revision momentum tends to lead price, turning negative before share prices peak as analysts begin cutting estimates.

- Divergence between the two, where prices keep rising but revisions flatten or turn negative, has historically preceded the sharpest momentum unwinds.

Goldman’s 2026 consensus data shows that bottom-up EPS estimates for 2026 and 2027 have each risen approximately 8% year-to-date as of 16 May 2026, driven primarily by AI capital expenditure expectations. The current EPS revision picture is itself heavily AI-dependent at the index level, which means the fundamental support Goldman cites is real but concentrated in the same theme driving the price action.

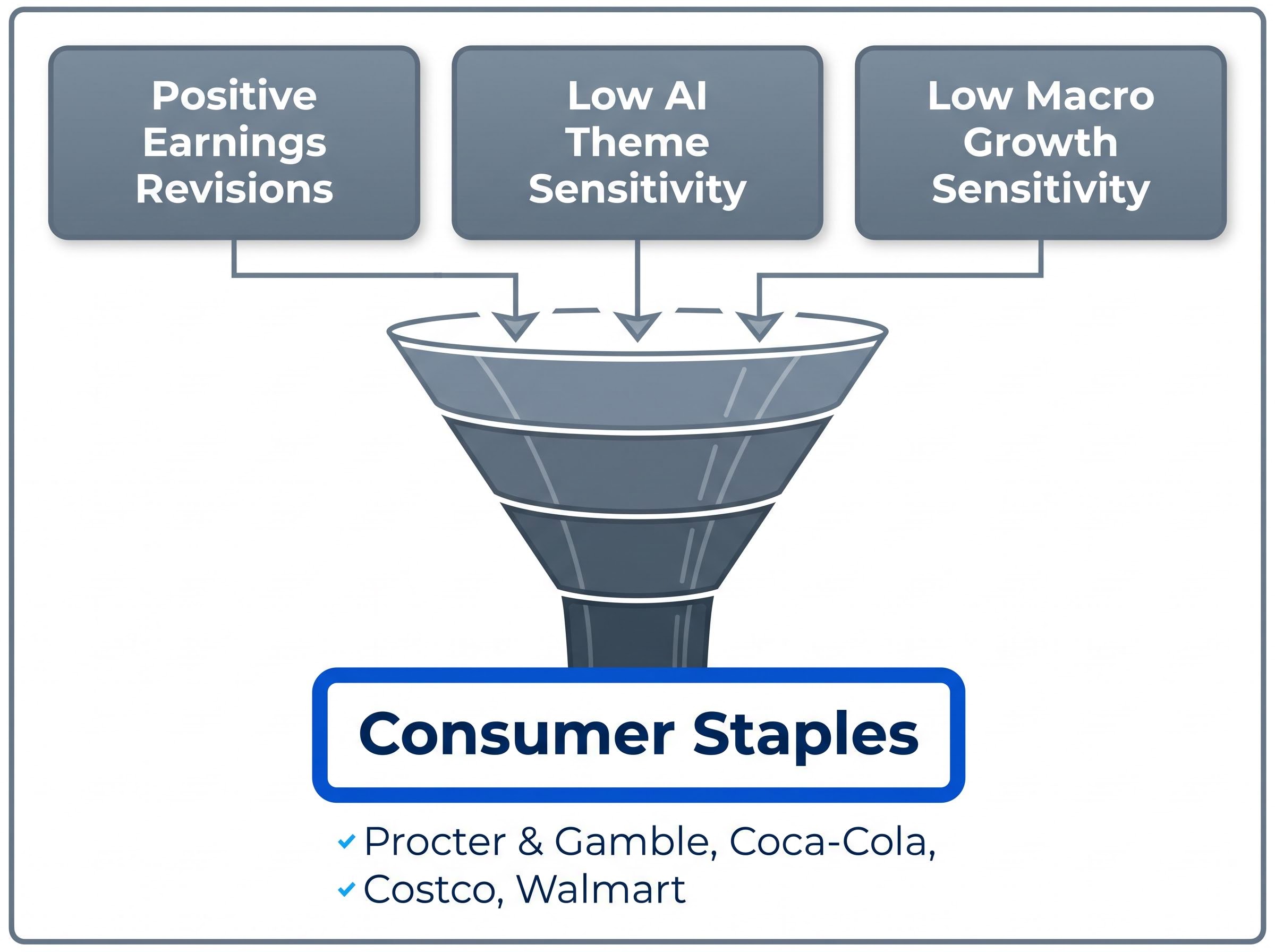

Goldman’s investment strategy guidance points toward stocks with positive earnings revisions and limited sensitivity to AI themes and macroeconomic growth signals, a filter designed to identify companies whose improving fundamentals are independent of the concentrated narrative.

Semiconductor concentration within the broader technology trade adds another layer of fragility: just 19 chip stocks representing roughly 15% of S&P 500 weight drove approximately 70% of the index’s year-to-date market capitalisation gains in 2026, with valuations in the 60-85x forward earnings range leaving little room for any guidance miss.

Why Goldman singles out Consumer Staples as the rotation destination

Apply Goldman’s two-part filter, positive earnings revisions combined with low sensitivity to both AI-related themes and broader macroeconomic growth signals, and Consumer Staples emerges as the sector that scores best on both dimensions.

| Dimension | Consumer Staples | Broader S&P 500 |

|---|---|---|

| Earnings revision direction | Positive | Positive, but AI-concentrated |

| AI theme sensitivity | Low | High (driven by mega-cap tech) |

| Macro growth sensitivity | Low | Moderate to high |

Goldman’s call is not a prediction that technology will collapse. It is a structural recommendation for investors who want to reduce exposure to a single concentrated narrative without leaving equity markets. The sector’s anchor names, Procter & Gamble, Coca-Cola, Costco, and Walmart, generate demand patterns that are largely independent of AI capital expenditure cycles or interest rate trajectories.

SPDR and Invesco 2026 commentary reinforces the broader case: defensive sectors have historically outperformed during momentum unwinds and volatility spikes, serving as a cushioning layer for portfolios that are otherwise growth-heavy.

How Consumer Staples fits within the broader institutional playbook

Goldman’s specificity is unusual. JPMorgan’s March 2026 guidance cites Consumer Staples as portfolio ballast alongside Healthcare and Utilities, without isolating it as the primary rotation destination. BlackRock’s 2026 commentary emphasises selectivity and quality income across multiple defensive sectors. Vanguard favours global diversification over sector-specific calls.

The institutional divergence is one of emphasis, not opposition. No major house has recommended an underweight in Consumer Staples relative to technology in publicly accessible 2026 research. Goldman names the destination explicitly; its peers point in the same direction with a wider lens.

A tiered framework for reducing concentration without abandoning equities

The analysis points toward action. What follows is a three-tier framework, drawn from Goldman Sachs, JPMorgan, BlackRock, and Vanguard guidance, that translates the concentration diagnosis into concrete portfolio adjustments.

- Structural changes to core holdings

- Replace or supplement cap-weighted S&P 500 exposure with an equal-weight alternative such as RSP (Invesco S&P 500 Equal Weight ETF), which directly counteracts mega-cap dominance

- Add international developed-market ETFs (Europe, Japan) where AI concentration in index composition is materially lower

- Consider total-market global index funds as Vanguard’s preferred structural solution

- Tactical sector and factor additions

- Add Consumer Staples exposure through XLP (SPDR Consumer Staples Select Sector ETF), the most direct implementation of Goldman’s specific call

- Include Healthcare and Utilities ETFs as the broader institutional consensus additions

- Consider multi-factor ETFs combining quality, value, and minimum volatility screens as a complement to single-sector positions

- Risk management rules

- Cap any single-stock position at 10-15% of total equity exposure

- Define a maximum thematic sleeve for AI and semiconductor allocations; institutional consensus clusters around 5-10% of total equity

- Trigger rebalancing whenever any allocation drifts more than 5 percentage points from its target weight, or at minimum annually

- For large existing AI or tech positions, staged selling or covered calls can reduce concentration without creating large immediate tax events

The most actionable single rule: Cap total AI, semiconductor, and thematic technology allocations at 5-10% of total equity exposure, and rebalance when the allocation drifts beyond that band, per BlackRock and broader institutional guidance.

The market may keep climbing, but the portfolio math still applies

Goldman’s own data complicates the simple “sell tech” reading. EPS estimates for 2026 and 2027 have each risen approximately 8% year-to-date, providing fundamental support that distinguishes the current episode from prior surges built purely on valuation expansion. The AI theme has real earnings behind it. That is precisely why the concentration exists.

Among 11 comparable historical momentum episodes since 1980, Goldman Sachs research indicates that gains extended for roughly one additional month before reversing. That context is informative but not a forecast; it describes a pattern, not a certainty.

The diversification case does not depend on predicting which outcome materialises. If technology continues to rally, a broadly diversified portfolio still participates through its remaining tech allocation. If momentum reverses, defensive and equal-weight positions absorb the shock. Acting on concentration is not the same as calling a top.

For investors who already hold large technology or AI positions and need a structured process for deciding when to trim rather than simply rebalance by formula, our dedicated guide to post-earnings decision frameworks walks through a three-part hold, trim, or wait methodology built for an environment where 84% of companies beat EPS estimates yet individual stocks still fell sharply on guidance misses.

Vanguard’s 2026 guidance advises against attempting to time a technology reversal, recommending instead that investors maintain disciplined rebalancing to long-term policy weights.

The question is not whether AI will keep delivering. The question is whether a portfolio should depend on it.

Concentration is the condition, not the forecast

The S&P 500’s 85%/15% split between technology gains and everything else is a structural portfolio condition for anyone holding a cap-weighted index fund. It is not a forecast, and it does not require a view on whether technology will outperform next quarter.

Goldman’s framework offers a two-part filter: look for positive earnings revisions and low sensitivity to AI and macroeconomic signals. Consumer Staples is the named destination. The broader defensive basket, Healthcare, Utilities, and equal-weight alternatives, is the supporting context endorsed across multiple institutional sources.

The practical step is straightforward: review current sector weights, identify any AI or technology allocation that has grown beyond a defined cap, and consider one structural addition, whether equal-weight exposure or a defensive sector position, before the next rebalancing window.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.