Why 30% Recession Odds Are Harder to Trade Than 60%

7 hrs ago

Donald Trump’s post-summit interview on Fox News, recorded on 15 May 2026 after two days of talks with Xi Jinping in Beijing, produced a remark that will likely outlast every tariff headline from the trip. The United States, he said, is “not looking to have somebody go independent” in Taiwan and will not write a blank cheque for military support 9,500 miles away. He confirmed he had made “no commitment either way” to Xi on the matter. The Beijing summit of 14-15 May 2026 generated genuine optimism around tariff cuts, agricultural purchases, and bilateral trade councils. But two structural tensions, over Taiwan’s political status and US controls on AI chip exports to China, were bracketed rather than resolved. Both carry direct implications for technology and semiconductor equities globally. What follows examines what Trump’s Taiwan remarks signal for US strategic posture, why AI chip export controls are unlikely to be traded away regardless of summit outcomes, and which companies and sectors carry the greatest structural exposure to escalation.

The words arrived within hours of the summit’s close. Speaking to Bret Baier on Fox News “Special Report” on 15 May 2026, Trump issued three distinct signals on Taiwan in rapid sequence.

“I’m not looking to have somebody go independent… we’re not looking to have somebody say, ‘Let’s go independent because the United States is backing us.’ We’re supposed to travel 9,500 miles to fight a war.”

The three components of that messaging were precise:

US policy on Taiwan has historically relied on deliberate strategic ambiguity: never confirming whether Washington would intervene militarily, but never ruling it out either. That ambiguity has functioned as a deterrent. Trump’s post-summit framing did not abandon it formally, but it tilted the language in a direction that both Global Times (on 16 May 2026, approvingly) and the BBC (the same day, analytically) read as a softening. The timing mattered as much as the words. This was not an offhand rally comment. It was a post-summit policy signal delivered to camera.

The Brookings cross-strait stability analysis examines precisely this deterrence mechanism, finding that the doctrine’s effectiveness depends on Beijing and Taipei each believing Washington’s response remains genuinely unpredictable, a condition that post-summit signalling language puts under pressure.

Taiwan’s President Lai Ching-te has maintained a carefully calibrated formula since taking office in May 2024. In a January 2024 Reuters interview, Lai stated Taiwan has “no need to formally declare independence” because the Republic of China is already a sovereign, independent country. The formulation is designed to preserve de facto sovereignty without crossing Beijing’s stated red line of a formal, legal independence declaration. It represents continuity with the Tsai Ing-wen administration.

Beijing treats it as functionally separatist regardless. The Democratic Progressive Party’s framing, however careful its legal and diplomatic language, is read in Beijing as a position that forecloses reunification. The formula’s limits are set not by Taipei’s intentions but by Beijing’s interpretation.

The pressure campaign operates on three parallel tracks, all of which continued through 2024-2025 irrespective of the diplomatic temperature at any given summit:

Beijing’s formal stance on the use of force has not softened. 2024 government work reports and senior official statements reiterated that China “will never promise to renounce the use of force” regarding Taiwan. Brookings has characterised Taiwan as the most likely flashpoint capable of derailing any broader US-China stabilisation, noting “very little fundamental convergence” on political and legal positions. The gap between summit-level diplomatic temperature and on-the-ground military trajectory is where the structural risk sits.

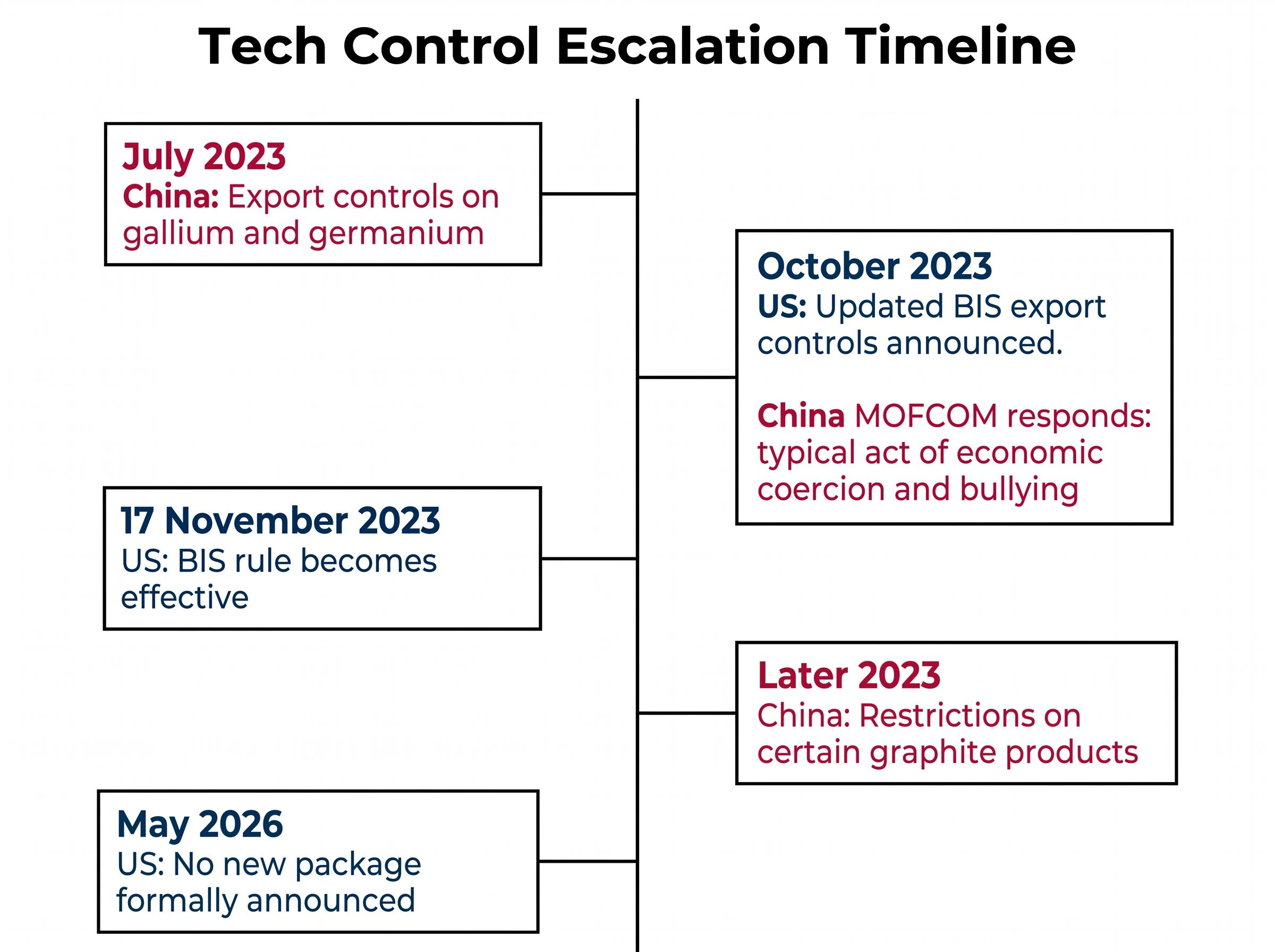

The operative US regulatory framework for AI chip exports to China remains the October 2023 Bureau of Industry and Security (BIS) rule, effective 17 November 2023. No new 2026 package has been formally announced. Understanding what these controls actually do, at a mechanical level, is necessary before assessing their market impact.

The October 2023 rules introduced a Total Processing Performance (TPP) threshold, a metric designed to capture a chip’s actual computing capability rather than relying on individual specifications that manufacturers could engineer around. The TPP framework was explicitly built to close the loophole that had allowed China-specific chip variants to ship below prior cut-offs. It also expanded licensing requirements to additional countries to prevent diversion.

The rules affect specific chip families and product lines across four categories of company. Nvidia’s flagship AI accelerators (A100, H100, H200, B100/B200) and China-specific variants (A800, H800, H20) are primary targets. AMD’s Instinct MI250/MI300 family falls under similar performance-based restrictions. Intel’s Gaudi AI accelerators and certain advanced CPUs are covered when they exceed defined thresholds. Semiconductor manufacturing equipment vendors, including ASML, Applied Materials, Lam Research, KLA, and Tokyo Electron, face licensing restrictions on tools enabling logic at 14nm/16nm and below, DRAM at 18nm half-pitch and below, and NAND with 128+ layers.

| Company | Affected Product Family | Restriction Type | China Revenue Exposure |

|---|---|---|---|

| Nvidia | A100, H100, H200, B100/B200, A800, H800, H20 | TPP threshold, licence required | ~20-25% of data-centre revenue (pre-tightening) |

| AMD | MI250, MI300 (Instinct family) | Performance-based licence required | Not quantified publicly |

| Intel | Gaudi accelerators, select advanced CPUs | Threshold-based licence required | Not quantified publicly |

| ASML / Equipment vendors | Advanced lithography, deposition, etch tools | Licence required for sub-14nm logic, sub-18nm DRAM, 128+ layer NAND | ~29% of ASML 2023 sales (includes tools below strictest thresholds) |

Beijing’s response has been consistent and sharp. China’s Ministry of Commerce (MOFCOM) called the October 2023 update “a typical act of economic coercion and bullying.” Retaliatory measures followed: export controls on gallium and germanium in July 2023, and restrictions on certain graphite products later that year.

The BIS policy shift from a presumption-of-denial to a case-by-case review standard, effective 15 January 2026, means the controlling barrier on Nvidia’s China access has moved from Washington to Beijing, a structural inversion that makes the revenue opportunity authorised in principle but commercially blocked in practice.

Beijing’s formal position (MOFCOM, October 2023): The updated US export controls represent “a typical act of economic coercion and bullying.”

The AI chip controls exist at a level that sits above the trade relationship entirely. Understanding this distinction is the single most important conceptual tool for interpreting any headline claiming chip controls are “on the table” in a trade deal.

The controls are embedded within a “small yard, high fence” strategic doctrine: a narrow set of technologies deemed strategically significant, protected by restrictions designed to be durable rather than negotiable. The Atlantic Council has framed this doctrine as unlikely to be traded away for tariff or market-access concessions. The Council on Foreign Relations (CFR) has characterised export controls as a “central pillar” of technology competition policy, unlikely to be rolled back quickly.

Georgetown’s analysis of the small yard, high fence doctrine explains how the framework was designed from the outset to separate a narrow set of strategically sensitive technologies from the reciprocal concession logic that governs standard trade negotiations, grounding the controls in national-security law rather than commerce law.

CFR assessment: US export controls on advanced computing and semiconductor equipment have become a “central pillar” of technology competition policy, unlikely to be rolled back quickly.

Three features make the controls structurally durable:

CSIS analysis from 2024 noted that further US tightening could prompt China to broaden its own export controls on critical minerals, increasing supply-chain volatility for semiconductor producers globally. Both capitals now treat advanced AI chips as a core national-security domain. Any investor framework treating chip controls as a tariff-style negotiable concession is built on a category error.

The structural risk has specific names and specific revenue lines attached to it.

Nvidia derived approximately 20-25% of its data-centre revenue from China (including Hong Kong) prior to the October 2023 tightening, according to analyst estimates cited by Reuters. TSMC reported that China (including Hong Kong) accounted for 11% of its 2023 net revenue, per its 2023 Annual Report. TSMC also carries second-order exposure: curbs on Nvidia’s ability to ship chips that TSMC manufactures at advanced nodes create utilisation risk even when direct China revenue appears manageable. ASML disclosed that China represented approximately 29% of its 2023 sales, though much of that volume was in tools below the strictest control thresholds, per its 2023 Annual Report.

Institutional investors at BlackRock, Goldman Sachs, and Vanguard treat Nvidia’s China exposure as a call option on geopolitical resolution rather than a base-case revenue driver, a framing that reframes the 20-25% data-centre revenue figure not as a recoverable loss but as an asymmetric upside that requires structural change in the bilateral relationship before it can be monetised.

| Company | China Revenue Share | Exposure Type |

|---|---|---|

| Nvidia | ~20-25% of data-centre revenue (pre-tightening) | Direct: licence-restricted chip sales |

| TSMC | 11% of 2023 net revenue | Direct + second-order (advanced-node utilisation risk) |

| ASML | ~29% of 2023 sales | Direct, though partially below strictest thresholds |

Bloomberg and Financial Times analyses from 2024-2025 have identified a recurring repricing pattern in semiconductor equities tied to the US-China technology competition. The trigger sequence follows a recognisable pattern:

The risk is not theoretical. It has already materialised in equity markets and, given the structural durability of both the controls and the Taiwan tensions, is likely to recur.

The Beijing summit produced four concrete headline outcomes, per the China Commerce Ministry statement of 16 May 2026: tariff reductions agreed in principle, agricultural purchase commitments, aircraft engine supply guarantees, and the establishment of bilateral trade and investment councils. These are real, near-term economic signals. They represent genuine diplomatic substance.

What the summit resolved and what it did not are distinct categories:

The split market verdict on the summit’s two days of talks was visible in the geographic divergence: the Dow Jones closed above 50,000 on 14 May while Asian equities retreated on 15 May, a pattern that maps directly to the distinction between trade-layer relief and unresolved security-layer tensions that different regional investor bases weight differently.

Three specific developments could convert the structural fault lines into acute market events:

None of these is a base-case scenario. All are plausible on a 12-24 month horizon. The trade agreements and the structural fault lines are not contradictions that cancel each other out. They are distinct layers operating simultaneously, on different policy timescales, in different institutional registers.

The Beijing summit represents a genuine improvement in diplomatic temperature. It does not resolve the two structural issues most likely to generate market disruption. Taiwan and AI chip controls operate in a different policy register from tariff negotiations: they are grounded in national-security frameworks, backed by bipartisan consensus, and tied to strategic competition that no single summit can settle.

The investor framework that emerges from this analysis draws a clear line between trade-layer agreements, which are negotiable, time-sensitive, and responsive to summit diplomacy, and security-layer tensions, which are structural, durable, and operating on a different policy timeline. Trump’s “no commitment either way” formulation on Taiwan is the clearest single signal that the US posture has shifted in ways that markets have not fully priced.

Investors who price only the trade optimism and ignore the structural fault lines are mispricing the tail risk in technology and semiconductor portfolios. The summit was real. So are the tensions it left unresolved.

For investors wanting to build a position-level framework around the exposure data outlined above, our deep-dive into semiconductor stock valuations examines name-by-name forward P/E multiples across Micron, Intel, Nvidia, and ASML, with specific attention to which names have run ahead of earnings and which carry valuation support that a geopolitical repricing event would not erase.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding policy developments and market impacts are speculative and subject to change based on geopolitical developments and government actions.

Strategic ambiguity is the longstanding US doctrine of neither confirming nor ruling out military intervention in Taiwan, which functions as a deterrent to both Chinese aggression and Taiwanese formal independence. Investors care because any perceived softening of this posture can reprice geopolitical risk across semiconductor and technology equities exposed to the Taiwan Strait.

The core framework is the October 2023 Bureau of Industry and Security rule, which uses a Total Processing Performance threshold to restrict exports of advanced AI accelerators to China, covering Nvidia's A100, H100, H200, and B-series chips, AMD's Instinct MI series, and semiconductor equipment from ASML, Applied Materials, Lam Research, and KLA. These controls are grounded in national-security law rather than trade law, making them structurally durable regardless of summit outcomes.

Analysts at the Atlantic Council and Council on Foreign Relations assess this as very unlikely, because the controls are grounded in national-security authorities rather than trade law, enjoy bipartisan Congressional support, and form part of a 'small yard, high fence' doctrine explicitly designed to sit outside the reciprocal concession logic of trade negotiations.

Nvidia derived approximately 20-25% of its data-centre revenue from China, including Hong Kong, prior to the October 2023 tightening. Institutional investors at firms including BlackRock, Goldman Sachs, and Vanguard are reported to treat this exposure as a call option on geopolitical resolution rather than a base-case revenue driver.

The article identifies three triggers: a formal Taiwan independence move, a new BIS chip restriction package tightening TPP thresholds or expanding country coverage, and a significant escalation in PLA activity in the Taiwan Strait beyond the current baseline of regularised incursions. None is a base-case scenario, but all are considered plausible on a 12-24 month horizon.