Citi Puts Memory Supply Above Chip Design in AI Stock Rankings

56 mins ago

Megaport (ASX: MP1) shares surged approximately 33% on 14 May 2026, marking one of the largest single-day moves in the company’s listed history. The catalyst: three AI infrastructure contracts announced through its Latitude.sh subsidiary, carrying a combined total contract value (TCV) of US$182.9 million. The contracts nearly double Megaport’s compute annualised recurring revenue (ARR) base, a figure that demands scrutiny beyond the headline share price reaction. What follows is a breakdown of what the contracts deliver in financial terms, whether the balance sheet can absorb the US$101 million capital expenditure requirement without a further raise, and what retail investors should monitor before drawing conclusions from today’s move.

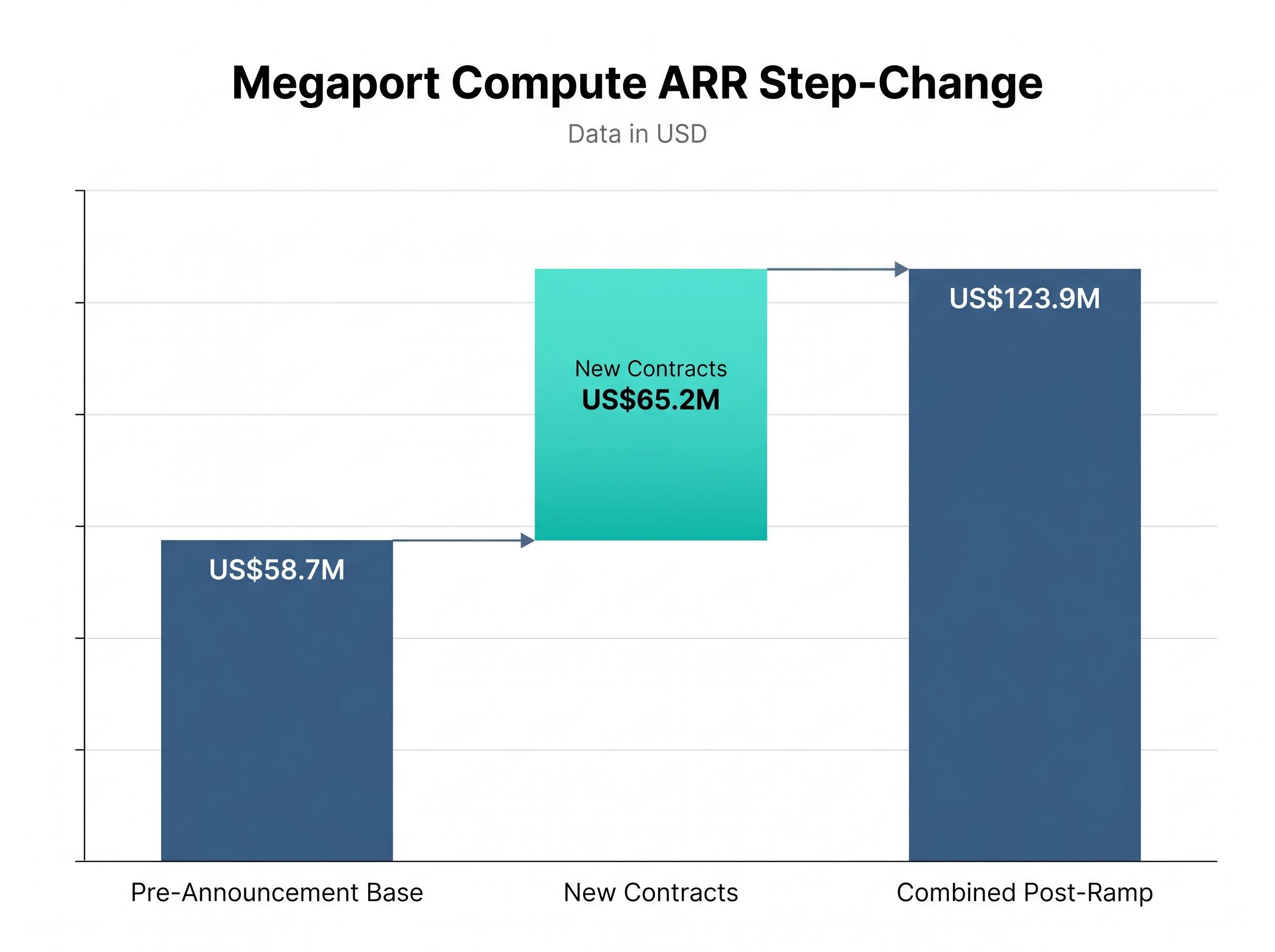

The announcement comprises three separate agreements delivered through Latitude.sh as managed GPU infrastructure. Two carry 36-month terms and account for roughly 90% of the TCV. The third is a 24-month agreement. Together, the US$182.9 million TCV (approximately A$254 million) converts to US$65.2 million (approximately A$90.6 million) in annualised recurring revenue.

That ARR figure sits against a pre-announcement compute ARR base of US$58.7 million (A$82.7 million). The new contracts, once fully ramped, would push combined compute ARR to approximately US$123.9 million.

Compute ARR before and after: Pre-announcement US$58.7 million vs. combined post-ramp US$123.9 million, a near-doubling from a single contract announcement.

Revenue from these contracts is fixed and usage-independent. Megaport receives the contracted amount regardless of how intensively customers utilise the hardware, removing the volume risk that typically complicates managed infrastructure revenue forecasting. At contract expiry, all GPU and compute assets transfer into the broader Latitude.sh on-demand pool, preserving residual revenue optionality.

Hardware delivery is expected in late FY26 or early FY27, with phased deployment from H1 FY27.

The three announced deals are not Megaport’s first foray into contracted GPU infrastructure: the prior Latitude.sh compute contract signed in April 2026, a 36-month USD$25.1 million agreement with a US-based agentic AI company, established the fixed-term revenue model and capex payback framework that the larger May contracts now replicate at significantly greater scale.

| Contract | Term | Approximate TCV Share | ARR Contribution | Hardware Delivery |

|---|---|---|---|---|

| Contract 1 (36-month) | 36 months | ~45% of TCV | Included in US$65.2M total | Late FY26 / Early FY27 |

| Contract 2 (36-month) | 36 months | ~45% of TCV | Included in US$65.2M total | Late FY26 / Early FY27 |

| Contract 3 (24-month) | 24 months | ~10% of TCV | Included in US$65.2M total | Late FY26 / Early FY27 |

The contract win did not land on a struggling business. Megaport’s H1 FY26 results, the most recent reported period, showed a company already growing at pace:

The two-segment ARR picture matters. Network ARR remains the larger, more mature revenue stream. Compute ARR, the segment the new contracts accelerate, was already the faster-growing division before today.

Full-year FY26 guidance sits at A$302-317 million in revenue with a 21-24% EBITDA margin. The new ARR from the Latitude.sh contracts begins flowing in H1 FY27, given hardware delivery timelines. The primary financial impact therefore lands in FY27, not the current guidance year.

Investors should not expect FY26 revenue to be revised materially upward on this announcement alone. The contracts are additive to the existing outlook, but the revenue recognition timeline places the step-change one financial year ahead.

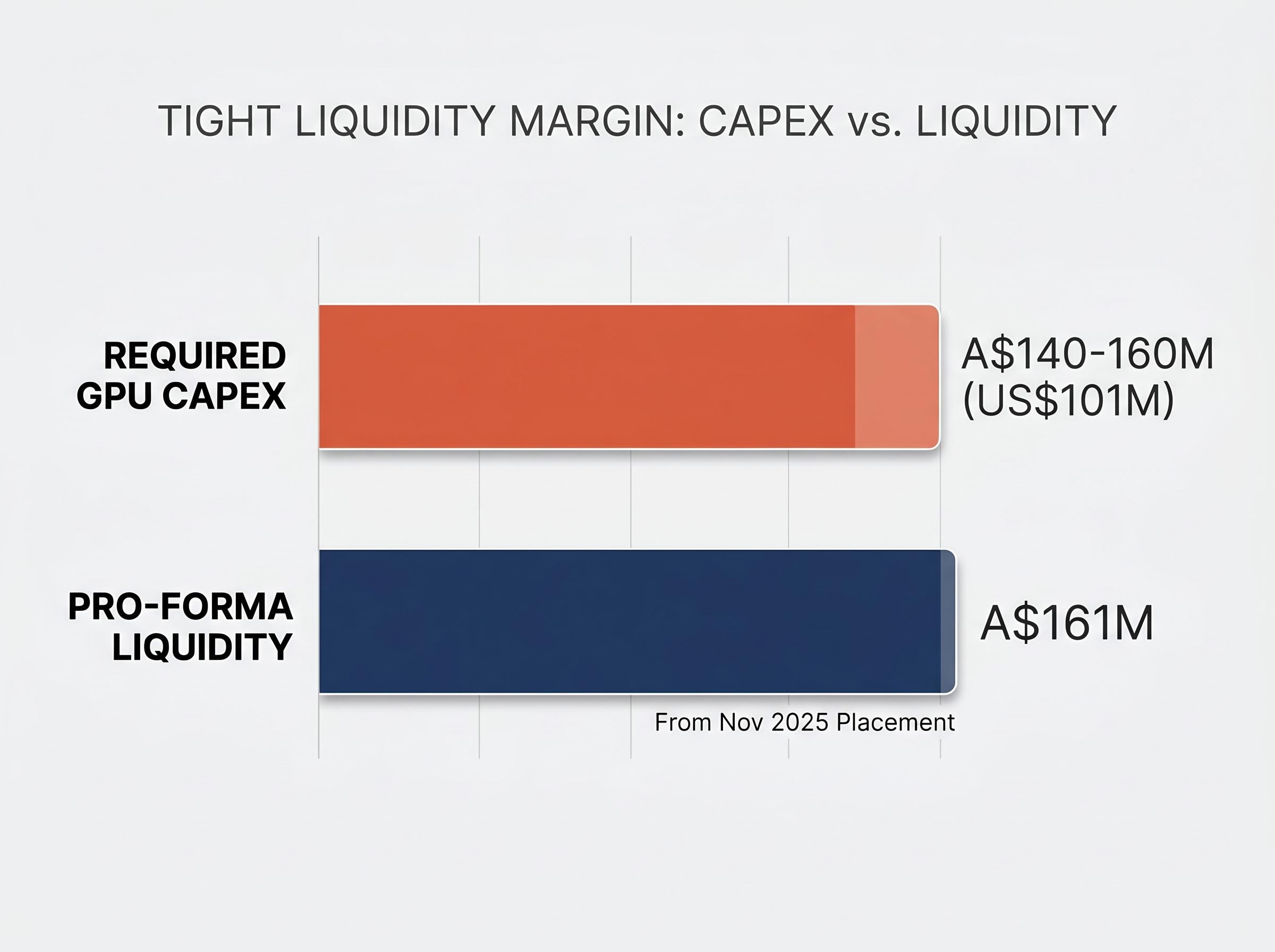

The capex requirement is US$101 million, directed primarily at NVIDIA GPU, compute, networking, and storage hardware. At prevailing AUD/USD exchange rates, that converts to approximately A$140-160 million.

Compare that figure to Megaport’s available cash. The A$200 million equity placement raised in November 2025 to fund the Latitude.sh acquisition was allocated as follows:

| Use of Placement Funds | Allocated Amount (A$) |

|---|---|

| India network expansion | $43 million |

| Transaction costs | $20 million |

| Additional liquidity buffer | $29 million |

| Pro-forma liquidity (residual) | $161 million |

The arithmetic is tight: US$101 million in GPU capex (approximately A$140-160 million) against A$161 million in pro-forma liquidity leaves a narrow margin.

The question investors should be asking is whether capex deployment can be staged across the 24-36 month contract periods to match incoming contracted revenue, or whether near-term liquidity comes under pressure before the revenue stream begins. Management has framed the return profile as an estimated two-year capex payback period, but hardware delivery in late FY26 or early FY27 means the capital outlay precedes the revenue by several quarters.

If capex phasing does not align with the contracted revenue ramp, or if additional AI contract wins require further capital deployment, a follow-on equity raise cannot be ruled out. That possibility is the single most significant balance sheet consideration for current and prospective holders.

Megaport’s original business is Network-as-a-Service (NaaS), a software-defined platform connecting enterprises to cloud providers and data centres across more than 1,100 enabled locations globally. NaaS means customers can provision network connections programmatically, without physical infrastructure procurement.

Latitude.sh, acquired through the A$200 million placement in November 2025, adds managed GPU and compute infrastructure delivered as a service. Customers access dedicated NVIDIA GPU capacity without procuring and managing the hardware themselves.

The combined platform positions Megaport against two distinct competitive categories, and neither offers the same bundled proposition.

| Provider | Managed GPU | Network Integration | Data Sovereignty | Pricing Model |

|---|---|---|---|---|

| Megaport / Latitude.sh | Yes (dedicated) | Bundled NaaS layer | Flexible, customer-directed | Fixed, usage-independent |

| Hyperscalers (AWS, Azure, GCP) | Yes (standardised) | Proprietary network | Limited flexibility | Variable, usage-based |

| Local colos (NextDC, MAQ) | No (space and power only) | Tenant-provisioned | Location-specific | Lease-based |

Megaport’s unique position is combining the NaaS layer with the managed GPU layer under one platform. Customers get network and compute provisioned together rather than contracting two separate providers. Management has positioned this vertical integration as the enabler of larger, higher-value contracts, and the three announced deals offer early evidence of that thesis. For enterprise customers with data sovereignty requirements, cost predictability demands, or latency-sensitive AI workloads, the bundled offering addresses a gap that neither hyperscalers nor colocation providers fill directly.

GPUaaS adoption in Australia and New Zealand is forecast to reach 84% of organisations by 2027, with enterprise compute demand growing at a 17% compound annual rate through that period, a demand backdrop that explains why managed GPU contracts of the scale Megaport has announced are emerging as commercially viable at this point in the market cycle.

Whether the three contracts represent repeatable demand or a concentrated, one-off opportunity is the question that determines whether today’s ARR addition proves durable.

Broker coverage of Megaport spans several major houses including Macquarie, UBS, Morgan Stanley, Barrenjoey, Bell Potter, and Jefferies. Updated ratings and 12-month price targets from notes published on or after 14 May 2026 will determine whether professional estimates have caught up to the post-announcement share price, or whether the stock has already moved through consensus.

Investors should monitor the distribution of Buy, Hold, and Sell ratings, along with the consensus price target range. The analytical tension worth watching is whether any broker maintains a cautious stance on valuation despite acknowledging the positive contract news. A gap between the post-announcement share price and consensus targets would signal that the market has priced in more than the professional view currently supports. Conversely, if updated targets sit above the current price, the re-rating may have further room to run.

Retail investors often interpret a 33% single-day move as a signal that professional analysts are equally bullish. The more reliable signal is the distance between the moved share price and where consensus sits after target revisions. That gap, whether positive or negative, tells investors whether the market has overshot or whether further upside is supported by the numbers.

GPU supply constraints have already caused enterprise hardware prices to surge up to 60% for high-capacity models in 2026, with major suppliers reporting sold-out production capacity through year-end; the same supply pressure that is driving up hardware costs across the industry directly affects the cost certainty and delivery timeline assumptions embedded in Megaport’s US$101 million capex programme.

US$101 million in GPU capex against A$161 million in pro-forma liquidity. If additional contract wins require further capital, or if phasing does not match revenue ramp, a follow-on equity raise at elevated share price levels would dilute existing holders.

A 33% share price move in one session reflects genuine contract value. Investors who buy into the momentum without stress-testing these three risk vectors are making a different bet than those who have examined the balance sheet arithmetic, supply chain timeline, and concentration profile.

Single-stock AI concentration risk is precisely what a 33% single-session move amplifies: investors who entered Megaport positions before the announcement now hold a materially larger weighting to a single AI infrastructure thesis than they may have intended, a dynamic the dot-com era demonstrated could unwind sharply even when the underlying technology thesis proved correct.

The financial impact of the Latitude.sh contracts is an FY27 story. Hardware delivery in late FY26 or early FY27, followed by phased deployment from H1 FY27, means investors buying today are pricing in a revenue stream that has not yet been recognised.

In the months ahead, the metrics to monitor include capex deployment updates, broker estimate revisions for FY27, signs of additional AI contract wins building on the three announced, and any disclosure about customer identity or contract renewal discussions.

Megaport is executing on a genuine structural theme, and the contract announcement represents a material acceleration of its compute ARR trajectory. The 33% single-day move, however, compresses the margin of safety. The balance sheet question, whether the growth story can be funded from existing resources or requires dilutive capital, is the variable that will determine whether today’s price move proves to be a re-rating or an overshoot.

For investors wanting a systematic framework to assess whether the post-announcement re-rating is durable or vulnerable to reversal, our dedicated guide to multiple compression in ASX growth stocks walks through the eight technical and fundamental signals that preceded 18-82% declines across the ASX SaaS cohort in 2025-2026, including the specific broker consensus lag and price-action patterns that appeared months before the worst drawdowns.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this article are subject to market conditions and various risk factors. Past performance does not guarantee future results.

Annualised recurring revenue (ARR) is the yearly value of contracted, predictable revenue, expressed as an annual figure. For Megaport, the new Latitude.sh contracts would nearly double its compute ARR from US$58.7 million to approximately US$123.9 million once fully ramped, making it a key metric for assessing the company's growth trajectory.

Megaport shares surged approximately 33% on 14 May 2026 after its Latitude.sh subsidiary announced three AI infrastructure contracts with a combined total contract value of US$182.9 million, which nearly doubles the company's compute ARR base and represents one of the largest contract announcements in the company's listed history.

Hardware delivery is expected in late FY26 or early FY27, with phased deployment from H1 FY27, meaning the primary financial impact lands in FY27 rather than the current guidance year. Investors buying at today's price are pricing in a revenue stream that has not yet been recognised.

Megaport had approximately A$161 million in pro-forma liquidity following its November 2025 equity placement, while the GPU hardware capex requirement is estimated at US$101 million (roughly A$140-160 million), leaving a narrow margin. If additional contract wins require further capital or if capex phasing does not align with revenue ramp, a follow-on equity raise cannot be ruled out.

Latitude.sh is a managed GPU and compute infrastructure platform acquired by Megaport through an A$200 million equity placement in November 2025. It allows enterprise customers to access dedicated NVIDIA GPU capacity without managing hardware themselves, and when combined with Megaport's existing Network-as-a-Service platform, creates a bundled network and compute offering that neither hyperscalers nor colocation providers directly replicate.